There’s are some interesting ventures assigning credit scores to marginal borrowers:

They have no bank account, no credit score, no financial identity. So a quarter of humanity hasn’t been able to borrow money. Until now.

Several dozen startups say they have developed ways to bring those 2 billion people into the international financial system, monitoring cell phone use and other personal habits to predict creditworthiness. For example, people who don’t let their phone batteries run low tend to do the same for their debt balance. Borrowers who get more calls than they make are better risks, and applicants who state their loan purpose in a few words are better borrowers than those who end up writing an essay.

…

A key to creditworthiness is personal daily routine. People who charge the same amount of airtime on the same day every week are better credit risks than those who purchase a large amount, then let their accounts sit empty, according to Van Der Tuin of First Access. When phones stay in the same place every day, that is often a sign that the owner is at work.Moreover, in emerging market countries mobile phones are increasingly serving as ledgers of money movement. So monitoring phone records becomes a simple substitute for examining a bank account. At the same time, traditional credit risk assessments, according to the startups, have ignored the added importance of social capital. Beyond serving as de facto bank statements, mobile and online footprints indicate how well borrowers are treated by their community.

It was a positive day for the Canadian preferred share market, with PerpetualDiscounts up 8bp, FixedResets winning 36bp and DeemedRetractibles gaining 4bp. The Performance Highlights table, while still much longer than was the norm a year ago, is unusually short when judged by 2015 standards. Volume was below average.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 19.31 to be $0.87 rich, while TRP.PR.G, resetting 2020-11-30 at +154, is $0.53 cheap at its bid price of 20.47.

Click for Big

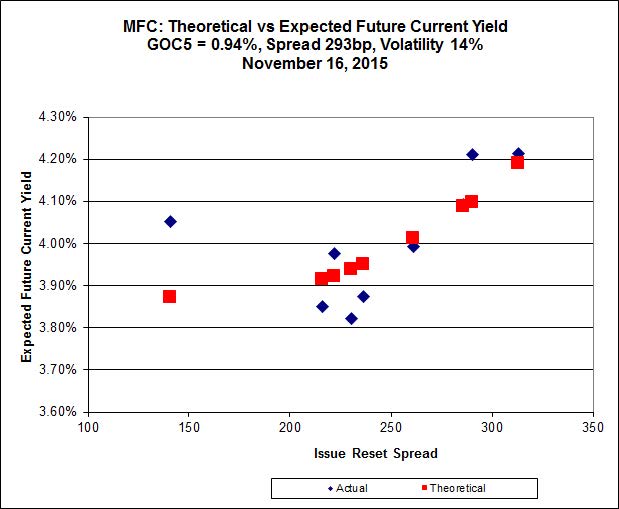

Most expensive is MFC.PR.N, resetting at +230bp on 2020-3-19, bid at 21.20 to be 0.64 rich, while MFC.PR.F resetting at +141bp on 2016-6-19, is bid at 14.50 to be 0.68 cheap.

Click for Big

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 16.52 to be $1.59 cheap. BAM.PF.G, resetting at +284bp on 2020-6-30 is bid at 22.00 and appears to be $1.01 rich.

Click for Big

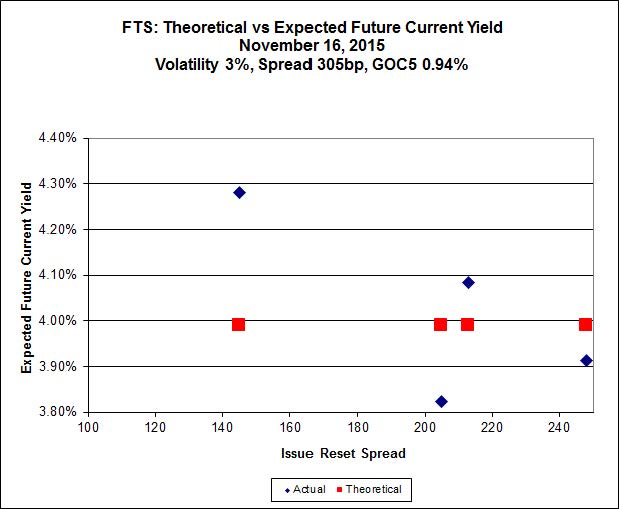

FTS.PR.K, with a spread of +205bp, and bid at 19.55, looks $0.82 expensive and resets 2019-3-1. FTS.PR.H, with a spread of +145bp and resetting 2020-6-1, is bid at 13.96 and is $1.01 cheap.

Click for Big

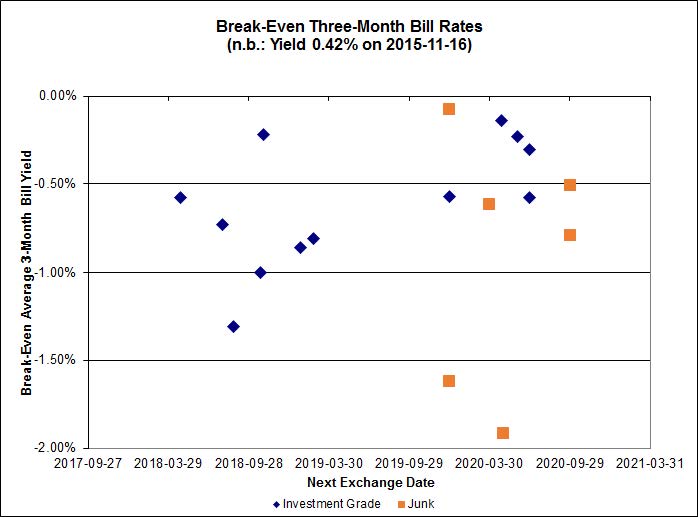

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.61%, with no outliers. There are three junk outliers above 0.00% and one below -2.00%.

Click for Big

The light blue point is an estimate for the potential BCE.PR.R / BCE.PF.Q pair, the latter of which is not trading. Its price has been set to the average defined by the other BCE Ratchet Rate preferreds.

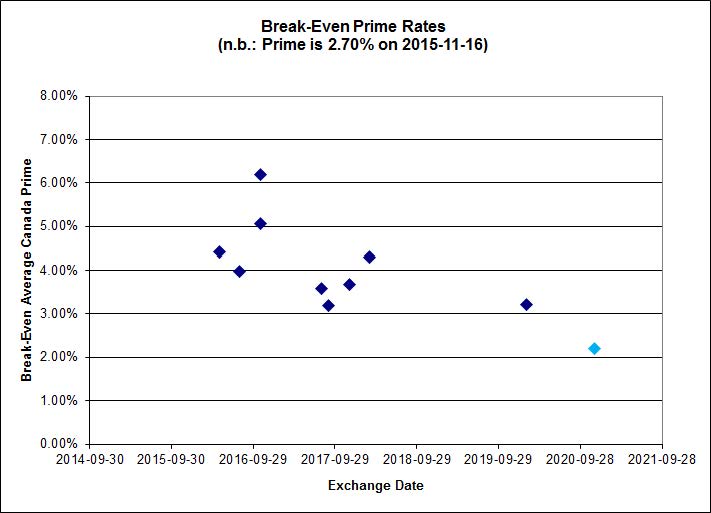

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 4.27 % | 5.12 % | 33,004 | 17.68 | 1 | 0.0000 % | 1,819.2 |

| FixedFloater | 6.14 % | 5.39 % | 28,258 | 17.05 | 1 | 2.0462 % | 3,175.8 |

| Floater | 3.88 % | 3.92 % | 69,743 | 17.55 | 3 | -0.3549 % | 2,033.4 |

| OpRet | 4.87 % | 3.88 % | 35,356 | 0.77 | 1 | 0.5383 % | 2,733.2 |

| SplitShare | 4.75 % | 5.85 % | 140,232 | 4.36 | 5 | -0.2533 % | 3,198.2 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.2533 % | 2,495.4 |

| Perpetual-Premium | 5.79 % | 0.76 % | 72,285 | 0.08 | 6 | 0.4304 % | 2,508.7 |

| Perpetual-Discount | 5.53 % | 5.60 % | 84,242 | 14.45 | 33 | 0.0783 % | 2,588.0 |

| FixedReset | 4.82 % | 4.32 % | 221,875 | 15.44 | 76 | 0.3610 % | 2,122.8 |

| Deemed-Retractible | 5.15 % | 5.15 % | 112,263 | 5.40 | 33 | 0.0395 % | 2,582.0 |

| FloatingReset | 2.58 % | 3.79 % | 54,565 | 5.77 | 10 | 0.3836 % | 2,189.4 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| FTS.PR.J | Perpetual-Discount | -1.74 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-16 Maturity Price : 21.40 Evaluated at bid price : 21.40 Bid-YTW : 5.57 % |

| FTS.PR.F | Perpetual-Discount | -1.73 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-16 Maturity Price : 21.75 Evaluated at bid price : 22.00 Bid-YTW : 5.58 % |

| CU.PR.C | FixedReset | -1.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-16 Maturity Price : 20.62 Evaluated at bid price : 20.62 Bid-YTW : 4.12 % |

| CM.PR.Q | FixedReset | -1.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-16 Maturity Price : 22.00 Evaluated at bid price : 22.51 Bid-YTW : 4.10 % |

| PVS.PR.D | SplitShare | -1.26 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2021-10-08 Maturity Price : 25.00 Evaluated at bid price : 23.55 Bid-YTW : 5.89 % |

| BAM.PF.E | FixedReset | -1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-16 Maturity Price : 20.22 Evaluated at bid price : 20.22 Bid-YTW : 4.66 % |

| BAM.PR.M | Perpetual-Discount | -1.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-16 Maturity Price : 20.84 Evaluated at bid price : 20.84 Bid-YTW : 5.79 % |

| HSE.PR.C | FixedReset | -1.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-16 Maturity Price : 21.20 Evaluated at bid price : 21.20 Bid-YTW : 5.00 % |

| GWO.PR.N | FixedReset | -1.09 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.65 Bid-YTW : 10.06 % |

| ELF.PR.H | Perpetual-Discount | 1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-16 Maturity Price : 24.02 Evaluated at bid price : 24.52 Bid-YTW : 5.65 % |

| MFC.PR.N | FixedReset | 1.05 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.20 Bid-YTW : 5.79 % |

| MFC.PR.H | FixedReset | 1.09 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.15 Bid-YTW : 4.73 % |

| VNR.PR.A | FixedReset | 1.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-16 Maturity Price : 21.68 Evaluated at bid price : 22.12 Bid-YTW : 4.32 % |

| SLF.PR.J | FloatingReset | 1.12 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.60 Bid-YTW : 9.37 % |

| PWF.PR.R | Perpetual-Discount | 1.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-16 Maturity Price : 24.19 Evaluated at bid price : 24.69 Bid-YTW : 5.60 % |

| MFC.PR.K | FixedReset | 1.43 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.87 Bid-YTW : 6.50 % |

| SLF.PR.H | FixedReset | 1.47 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.27 Bid-YTW : 6.65 % |

| IAG.PR.G | FixedReset | 1.53 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.19 Bid-YTW : 4.97 % |

| RY.PR.J | FixedReset | 1.54 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-16 Maturity Price : 21.93 Evaluated at bid price : 22.39 Bid-YTW : 4.07 % |

| TRP.PR.E | FixedReset | 1.95 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-16 Maturity Price : 19.31 Evaluated at bid price : 19.31 Bid-YTW : 4.56 % |

| BAM.PR.G | FixedFloater | 2.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-16 Maturity Price : 25.00 Evaluated at bid price : 15.46 Bid-YTW : 5.39 % |

| TRP.PR.D | FixedReset | 2.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-16 Maturity Price : 18.73 Evaluated at bid price : 18.73 Bid-YTW : 4.64 % |

| NA.PR.W | FixedReset | 2.42 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-16 Maturity Price : 19.92 Evaluated at bid price : 19.92 Bid-YTW : 4.22 % |

| TRP.PR.B | FixedReset | 2.75 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-16 Maturity Price : 13.10 Evaluated at bid price : 13.10 Bid-YTW : 4.26 % |

| HSE.PR.A | FixedReset | 2.92 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-16 Maturity Price : 14.46 Evaluated at bid price : 14.46 Bid-YTW : 4.78 % |

| ELF.PR.G | Perpetual-Discount | 3.69 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-16 Maturity Price : 21.33 Evaluated at bid price : 21.33 Bid-YTW : 5.64 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| SLF.PR.J | FloatingReset | 107,990 | Nesbitt crossed 95,000 at 13.60. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.60 Bid-YTW : 9.37 % |

| RY.PR.P | Perpetual-Discount | 86,500 | Haywood bought 65,000 from RBC at 24.75. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-16 Maturity Price : 24.34 Evaluated at bid price : 24.72 Bid-YTW : 5.37 % |

| BNS.PR.P | FixedReset | 50,500 | RBC crossed 49,200 at 24.45. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.57 Bid-YTW : 3.49 % |

| TRP.PR.D | FixedReset | 30,394 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-16 Maturity Price : 18.73 Evaluated at bid price : 18.73 Bid-YTW : 4.64 % |

| TD.PF.F | Perpetual-Discount | 29,600 | RBC crossed 25,000 at 23.70. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-16 Maturity Price : 23.36 Evaluated at bid price : 23.67 Bid-YTW : 5.20 % |

| BNS.PR.Z | FixedReset | 25,045 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.54 Bid-YTW : 5.90 % |

| There were 26 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| BAM.PF.E | FixedReset | Quote: 20.22 – 21.00 Spot Rate : 0.7800 Average : 0.4902 YTW SCENARIO |

| BAM.PR.Z | FixedReset | Quote: 20.85 – 21.58 Spot Rate : 0.7300 Average : 0.5360 YTW SCENARIO |

| HSE.PR.E | FixedReset | Quote: 22.45 – 22.80 Spot Rate : 0.3500 Average : 0.2401 YTW SCENARIO |

| FTS.PR.H | FixedReset | Quote: 13.96 – 14.50 Spot Rate : 0.5400 Average : 0.4328 YTW SCENARIO |

| TD.PF.E | FixedReset | Quote: 23.20 – 23.60 Spot Rate : 0.4000 Average : 0.2976 YTW SCENARIO |

| BAM.PR.E | Ratchet | Quote: 16.00 – 16.50 Spot Rate : 0.5000 Average : 0.4044 YTW SCENARIO |

Several dozen startups say they have developed ways to bring those 2 billion people into the international financial system

When markets are saturated, find new markets. Slavery used to entail chains; now it is debt.

Do you suggest that third-world lending be criminalized, ‘for their own good’?

Just making an observation; not suggesting anything. Are you suggesting that those trying to get their hands on 2 billion are criminals? 😉