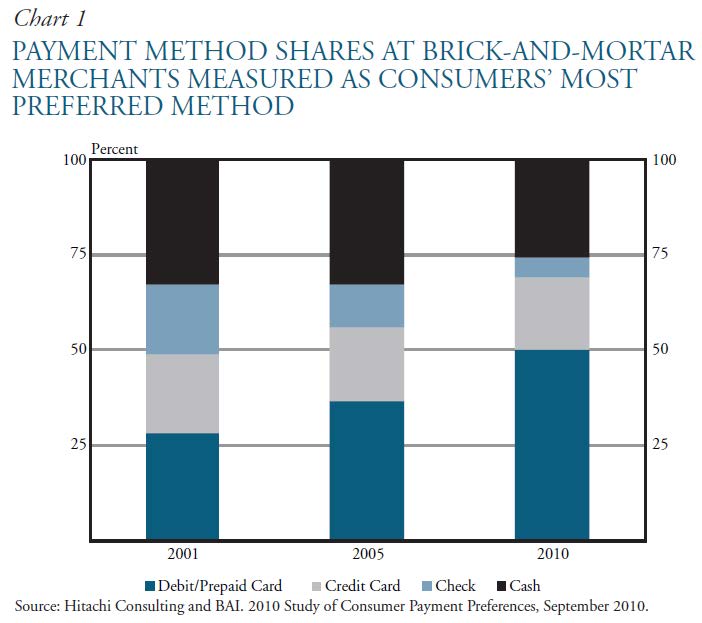

I was stunned to see the following chart in the Kansas City Fed paper by Fumiko Hayashi and Terri Bradford titled Mobile Payments: Merchants’ Perspectives:

Click for Big

Geez, I pay cash nearly every time! Does this make me an old Fudd? Mind you, though, the chart needs a footnote: if they are standing directly in front of me, then all three electronic methods will be tried several times each, after which the purchaser will pay the bill in nickels.

Yesterday I took a shot at the Fair Trade do-gooders; today it’s the environmentalists’ turn:

London has a dirty secret.

Levels of the harmful air pollutant nitrogen dioxide at a city-center monitoring station are the highest in Europe. Concentrations are greater even than in Beijing, where expatriates have dubbed the city’s smog the “airpocalypse.”

It’s the law of unintended consequences at work. European Union efforts to fight climate change favored diesel fuel over gasoline because it emits less carbon dioxide, or CO2. However, diesel’s contaminants have swamped benefits from measures that include a toll drivers pay to enter central London, a thriving bike-hire program and growing public-transport network.

…

Europe-wide policy triggered the problem. The “dieselisation” of London’s cars began with an agreement between car manufacturers and the EU in 1998 that aimed to lower the average CO2 emissions of new vehicles. Because of diesel’s greater fuel economy, it increased in favor.The European Commission, the EU regulatory arm, “is and always has been technologically neutral,” said Joe Hennon, a spokesman. “It does not favor diesel over petrol-powered cars. How to achieve CO2 reductions is up to member states.”

EU rules enforced since 2000 allowed diesel cars to spew more than three times the amount of oxides of nitrogen including NO2 as those using gasoline. New rules that took effect in September narrow that gap.

In yet another rant with no relationship at all to Canadian preferred shares (what?) how about this explanation of soaring tuition costs … not to mention a little flexing of new-found administrative muscle:

Click for Big

In interest-rate related news (for a change!) the Treasury market was on fire today:

The U.S. sale of $35 billion of five-year notes drew the lowest yield in six months as a European bond rally bolstered the attractiveness of U.S. government securities.

The notes yielded 1.513 percent at auction yesterday, the least since November. The bid-to-cover ratio, which gauges demand by comparing total bids with the amount of debt offered, was 2.73, versus an average of 2.65 at the past 10 sales. Treasuries rose earlier along with government securities across Europe as an unexpected jump in German unemployment fueled bets the European Central Bank will introduce further stimulus next week.

“It was a strong auction, given the strength that we saw coming in,” said Sean Murphy, a trader in New York at Societe Generale SA, one of 22 primary dealers obliged to bid at U.S. debt auctions. “In the global safe-bond world, the U.S. looks relatively cheap. And we are seeing that play out in the strength of Treasuries.”

The yield on the current five-year note fell five basis points, or 0.05 percentage point, to 1.48 percent at 5 p.m. yesterday in New York, according to Bloomberg Bond Trader prices. The yield on the benchmark 10-year note fell seven basis points to 2.44 percent.

…

Yields on European sovereign debt fell to record lows as the number of people out of work in Germany rose 23,937 to 2.91 million in May, the Federal Labor Agency said. Economists surveyed by Bloomberg forecast a decline of 15,000.ECB President Mario Draghi said in Portugal this week policy makers need to be “particularly watchful” of low inflation. Consumer-price increases in the euro region have been less than half the central bank’s goal of just under 2 percent since October. The ECB meets June 5.

Laurence D. Fink of Blackrock is attempting to distract regulators with other issues:

BlackRock Inc. (BLK)’s Laurence D. Fink, who oversees the world’s biggest exchange-traded fund lineup, said leveraged ETFs are a structural problem and have the potential to “blow up” the industry.

“BlackRock would never do a leveraged ETF,” Fink said in a question-and-answer session with Deutsche Bank AG co-chairman Anshu Jain today in New York. Fink said he doesn’t understand why the U.S. Securities and Exchange Commission allows them to operate.

…

Fink said today that products with embedded leverage should be supervised. Regulators should focus their efforts on products instead of the amount of assets managed when seeking to reduce risk in the financial system, he said. BlackRock is among large money managers that has been lobbying regulators and lawmakers to avoid being labeled a systemically important financial institution, or SIFI.

… and Scotia was unable to find a buyer for CI Financial:

Bank of Nova Scotia has settled on a plan to unload the majority of its stake in asset manager CI Financial Inc., opting to sell shares directly to public investors by way of a bought deal.

Scotiabank is selling 72 million shares at $31.60 each, amounting $2.3-billion, making it one of the largest public offerings in Canada.

It was a poor day for the Canadian preferred share market, with PerpetualDiscounts off 5bp, FixedResets losing 38bp and DeemedRetractibles down 16bp. The relatively lengthy Performance Highlights table is dominated by losers. Volume was high.

Update: PerpetualDiscounts now yield 5.28%, equivalent to 6.86% interest at the standard equivalency factor of 1.3x. Long Corporates now yield about 4.35%, so the pre-tax interest-equivalent spread (in this context, the Seniority Spread) is now about 250bp, a widening from the 240bp reported May 15.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0418 % | 2,494.2 |

| FixedFloater | 4.48 % | 3.73 % | 31,694 | 17.94 | 1 | 0.4263 % | 3,831.7 |

| Floater | 2.92 % | 3.06 % | 49,687 | 19.52 | 4 | 0.0418 % | 2,693.1 |

| OpRet | 4.38 % | -11.33 % | 33,755 | 0.10 | 2 | 0.0585 % | 2,709.0 |

| SplitShare | 4.80 % | 3.85 % | 62,896 | 4.18 | 5 | 0.3374 % | 3,120.9 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0585 % | 2,477.1 |

| Perpetual-Premium | 5.50 % | -10.74 % | 88,259 | 0.09 | 15 | 0.0000 % | 2,408.4 |

| Perpetual-Discount | 5.28 % | 5.28 % | 104,198 | 14.90 | 21 | -0.0524 % | 2,552.5 |

| FixedReset | 4.54 % | 3.60 % | 203,877 | 6.74 | 75 | -0.3821 % | 2,539.1 |

| Deemed-Retractible | 5.00 % | -0.23 % | 155,535 | 0.09 | 43 | -0.1611 % | 2,523.5 |

| FloatingReset | 2.66 % | 2.39 % | 151,987 | 4.01 | 6 | -0.0132 % | 2,487.7 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| SLF.PR.G | FixedReset | -1.62 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.52 Bid-YTW : 4.26 % |

| BMO.PR.Q | FixedReset | -1.32 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.61 Bid-YTW : 3.33 % |

| CU.PR.E | Perpetual-Discount | -1.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-05-28 Maturity Price : 23.65 Evaluated at bid price : 24.02 Bid-YTW : 5.11 % |

| GWO.PR.N | FixedReset | -1.17 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.90 Bid-YTW : 4.07 % |

| BAM.PF.D | Perpetual-Discount | -1.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-05-28 Maturity Price : 21.98 Evaluated at bid price : 22.26 Bid-YTW : 5.58 % |

| BNS.PR.P | FixedReset | -1.06 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2018-04-25 Maturity Price : 25.00 Evaluated at bid price : 25.12 Bid-YTW : 3.30 % |

| ENB.PR.Y | FixedReset | -1.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-05-28 Maturity Price : 22.65 Evaluated at bid price : 23.76 Bid-YTW : 4.11 % |

| PWF.PR.S | Perpetual-Discount | 1.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-05-28 Maturity Price : 23.29 Evaluated at bid price : 23.61 Bid-YTW : 5.12 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BMO.PR.S | FixedReset | 193,518 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-05-28 Maturity Price : 23.22 Evaluated at bid price : 25.18 Bid-YTW : 3.79 % |

| RY.PR.B | Deemed-Retractible | 116,152 | YTW SCENARIO Maturity Type : Call Maturity Date : 2014-08-24 Maturity Price : 25.25 Evaluated at bid price : 25.56 Bid-YTW : -0.23 % |

| BNS.PR.R | FixedReset | 107,814 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.40 Bid-YTW : 3.50 % |

| BAM.PR.P | FixedReset | 73,260 | Called for redemption. YTW SCENARIO Maturity Type : Call Maturity Date : 2014-09-30 Maturity Price : 25.00 Evaluated at bid price : 25.65 Bid-YTW : 2.58 % |

| ENB.PF.C | FixedReset | 69,411 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-05-28 Maturity Price : 23.08 Evaluated at bid price : 24.88 Bid-YTW : 4.19 % |

| BAM.PR.X | FixedReset | 65,012 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-05-28 Maturity Price : 21.86 Evaluated at bid price : 22.15 Bid-YTW : 4.07 % |

| There were 47 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| ENB.PR.Y | FixedReset | Quote: 23.76 – 24.12 Spot Rate : 0.3600 Average : 0.2078 YTW SCENARIO |

| MFC.PR.B | Deemed-Retractible | Quote: 22.60 – 22.89 Spot Rate : 0.2900 Average : 0.1866 YTW SCENARIO |

| CU.PR.E | Perpetual-Discount | Quote: 24.02 – 24.35 Spot Rate : 0.3300 Average : 0.2304 YTW SCENARIO |

| TRP.PR.E | FixedReset | Quote: 25.16 – 25.40 Spot Rate : 0.2400 Average : 0.1417 YTW SCENARIO |

| BAM.PR.K | Floater | Quote: 17.25 – 17.50 Spot Rate : 0.2500 Average : 0.1518 YTW SCENARIO |

| BAM.PR.B | Floater | Quote: 17.26 – 17.60 Spot Rate : 0.3400 Average : 0.2558 YTW SCENARIO |

Canadian prefs have been hit down the last few days? Do you think this is relative to Canada itself. USA prefs have been strong moving up with us treasuries and corporates. Are you seeing other nations including Canada sell off and investors foreign to USA including Canada shifting assets overseas????

riekreik

Maybe it is partly due to the number of new pref reset issues coming to market, replacing all those high yield/high spread resets issued during the financial crisis. As each one comes out (to be competitively priced (discounted slightly) in bought deals), it causes prices to drop 1-3% on related issuer issues. I think there has been at least 3-5 issues in the last few months.

Canadian prefs have been hit down the last few days?

Yep! However, TXPR total return is now 1,528.97 compared to 1,528.87 on April 30, so we’re still ahead on the month … for now!

Do you think this is relative to Canada itself.

The market does what it wants to do when the market wants to do it. AltaRed, above, has as good a guess as mine.

Are you seeing other nations including Canada sell off and investors foreign to USA including Canada shifting assets overseas????

Because of the tax effects, investors in Canadian preferred shares are overwhelmingly retail investors in their taxable accounts and Canadian taxable corporations.

I WOULD like to think that the new one would fit into the pricing of the rest of the respected universe.

I mean bmo is +224, td is +224, rbs +226, enb +264 (not really comparable to the big banks perhaps) and bmo (first one) is +233 back on 4/14. Not much really changed from 4/14 to 5/28 bmo most recent issue.

last 4 days you have a seen a few get clobbered – certainly it can make sense for ry pref I and L but others seem to have rolled over a bit – taking a break perhaps – but I don’t see the much movement in the Canadian 2 thru 10 years and the premium over the benchmark has narrowed over the last 1.5 months (233 bmo now 224) – so for sure you might see fix resets close to the new issue rate move in response.

Oh well Ill watch more – but up too late again. Goodnight

I WOULD like to think that the new one would fit into the pricing of the rest of the respected universe.

They usually do, more or less.

For Straight Perpetuals, they will often fix the coupon so that it equals the current yield on the lowest coupon comparator. This gives the stockbrokers a chance to tell their clients how competitive it is, while completely ignoring Implied Volatility, which means the new issue (at par by definition, with large and negative convexity) should yield more.

There’s usually a little less jiggery-pokery with FixedResets, which usually – as in the current case – come with a small, but not insighificant new issue concession. However, during the depths of the Credit Crunch, the mispricing between new and extant issues would resolve itself not by the new issue going to a premium, but by the whole damn market going down to eliminate the concession.

Jiggery-Pokery with FixedReset new issues usually takes the form of a long Initial Fixed Rate period, so they can price the Initial Dividend Rate off the market, but price the Issue Reset Spread off, say, the Canada Six and a Half Year bond. This can lead to substantial savings on reset.

James, get with the times, no one pays cash.

You’re like one of those annoying old ladies in front of me at the grocery store who has a little change purse and it takes forever to count out the loose nickels.

I walk by, tap my debit card on the machine, and I’m gone.

ltr

Paying cash results in zero yield; paying with plastic gets you 1% or more (just pay your credit card in full by the due date).

Would you ignore a difference in yield of 1%?

Yeah, I agree. I try and use my credit card much more now because of the cash rebate I get at the end of the year and the fact that the tap and go system is so convenient.

Well, guys, when your car insurance goes up because you’re spending too much on booze … when your life insurance goes up because you’re spending too much on smokes … when Public Health calls you in for a check-up because your purchase pattern at Honest Jimmy’s Tavern and Very Short Term Hotel is highly correlated with STD infection … when your wife wonders why you’re getting so much addressed ad mail from Ashley Madison all of a sudden … when your wife’s lawyer finds out where you really were during that important business conference eight years ago … DON’T COME CRYING TO ME!

hehe, good one James.

I don’t know if I share your paranoia, and wonder if this is truly the reason behind your penchant for cash as opposed to just being a fuddy-duddy. 😉

I’m not convinced that the access to credit card/debit card transactions is so readily available as you indicate, but I may be wrong, and hope I’m not. It’s amazing what a blind eye I can turn for a 1% return.

ltr

wonder if this is truly the reason behind your penchant for cash as opposed to just being a fuddy-duddy. 😉

Me too! But it’s either the truth or a great excuse, so I’m happy.

I’m not convinced that the access to credit card/debit card transactions is so readily available as you indicate

At present, I don’t believe it is. But the point is that

i) The data exists, and

ii) You don’t control it

This is extremely valuable data. The grocery stores, for instance, are fascinated by the fact that their young male customers tend to buy chocolates and condoms together, and would be even more fascinated to learn that they spend even more money at Vixxxy’s Massage the next day, which could lead to interesting coupon offers.

The corporations would love to make your life easier. Governments want to help keep you safe. And the genie’s in the bottle …