Performance of the HIMIPref™ Indices for October, 2009, was:

| Total Return | ||

| Index | Performance October 2009 |

Three Months to October 30, 2009 |

| Ratchet | -3.31% * | +20.90% * |

| FixFloat | -10.41% | +10.56% |

| Floater | -3.31% | +20.90% |

| OpRet | +0.19% | +1.72% |

| SplitShare | -0.04% | +4.13% |

| Interest | +0.19%**** | +1.72%**** |

| PerpetualPremium | -1.08% | +0.20% |

| PerpetualDiscount | -3.30% | +1.67% |

| FixedReset | -0.06% | +0.63% |

| * The last member of the RatchetRate index was transferred to Scraps at the February, 2009, rebalancing; subsequent performance figures are set equal to the Floater index | ||

| **** The last member of the InterestBearing index was transferred to Scraps at the June, 2009, rebalancing; subsequent performance figures are set equal to the OperatingRetractible index | ||

| Passive Funds (see below for calculations) | ||

| CPD | -1.26% | +1.21% |

| DPS.UN | -2.46% | +2.49% |

| Index | ||

| BMO-CM 50 | % | % |

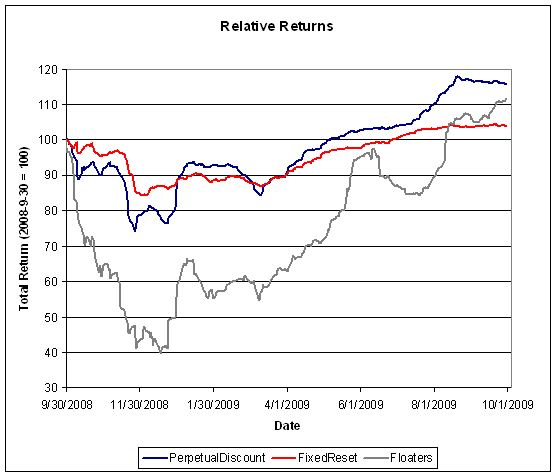

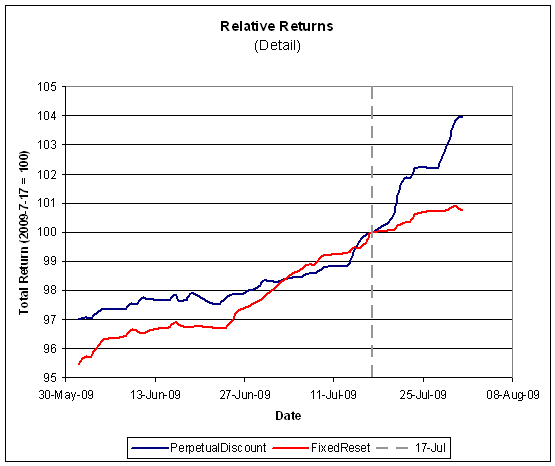

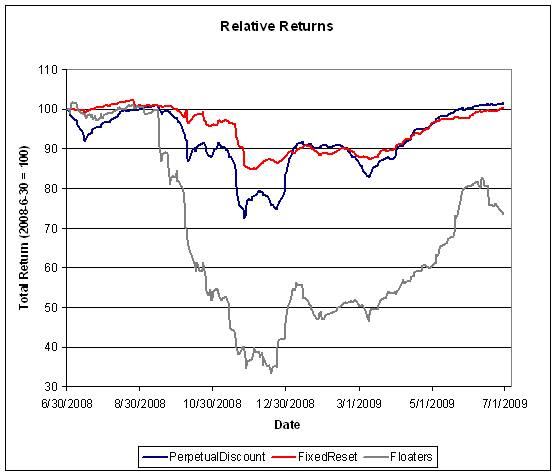

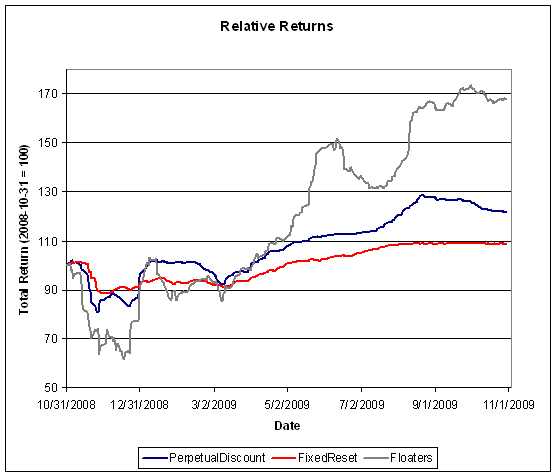

PerpetualDiscounts had a poor month (although not as bad as October 2008, when they lost 8.16%!); FixedResets were basically unaffected by the decline. The pre-tax interest equivalent spread of PerpetualDiscounts over Long Corporates (which I also refer to as the Seniority Spread) closed the month at 250bp compared to the September 30 value of 215bp.

Meanwhile, Floaters continued their wild ride.

Click for big

Compositions of the passive funds were discussed in the September edition of PrefLetter.

Claymore has published NAV and distribution data (problems with the page in IE8 can be kludged by using compatibility view) for its exchange traded fund (CPD) and I have derived the following table:

| CPD Return, 1- & 3-month, to October 30, 2009 | ||||

| Date | NAV | Distribution | Return for Sub-Period | Monthly Return |

| July 31, 2009 | 16.42 | |||

| August 31, 2009 | 16.93 | 0.00 | +3.11% | |

| September 25 | 16.63 | 0.21 | -0.53% | -0.59% |

| September 30 | 16.62 | 0.00 | -0.06% | |

| October 30, 2009 | 16.41 | -1.26% | ||

| Quarterly Return | +1.21% | |||

Claymore currently holds $315,167,224 (advisor & common combined) in CPD assets, up $15-million on the month and a stunning increase from the $84,005,161 reported in the Dec 31/08 Annual Report

The DPS.UN NAV for October 28 has been published so we may calculate the approximate October returns.

| DPS.UN NAV Return, October-ish 2009 | ||||

| Date | NAV | Distribution | Return for sub-period | Return for period |

| September 30, 2009 | 19.82 | |||

| October 28, 2009 | 19.32 | -2.52% | ||

| Estimated October Ending Stub | +0.06% * | |||

| Estimated October Return | -2.46% | |||

| *CPD had a NAVPU of 16.40 on October 28 and 16.41 on October 30, hence the total return for the period for CPD was +0.06%. The return for DPS.UN in this period is presumed to be equal. | ||||

| The October return for DPS.UN’s NAV is therefore the product of two period returns, -2.52% and +0.06% to arrive at an estimate for the calendar month of -2.46% | ||||

Now, to see the DPS.UN quarterly NAV approximate return, we refer to the calculations for August and September:

| DPS.UN NAV Returns, three-month-ish to end-October-ish, 2009 | |

| August-ish | +5.71% |

| September-ish | -0.60% |

| October-ish | -2.46% |

| Three-months-ish | +2.49% |