Brookfield Asset Management Inc. has announced:

the completion of its previously announced Class A Preference Shares, Series 42 issue in the amount of C$300,000,000. The offering was underwritten by a syndicate led by TD Securities Inc., RBC Capital Markets, CIBC and Scotiabank.

Brookfield issued 12,000,000 Series 42 Shares at a price of C$25.00 per share, for total gross proceeds of C$300,000,000. Holders of the Series 42 Shares will be entitled to receive a cumulative quarterly fixed dividend yielding 4.50% annually for the initial period ending June 30, 2020. Thereafter, the dividend rate will be reset every five years at a rate equal to the 5-year Government of Canada bond yield plus 2.84%. The Series 42 Shares will commence trading on the Toronto Stock Exchange this morning under the ticker symbol BAM.PF.G.

BAM.PF.G is a FixedReset, 4.50%+284, announced October 1. It will be tracked by HIMIPref™ and has been assigned to the FixedResets subindex.

The issue traded 1,056,420 shares today (consolidated exchanges) in a range of 24.95-05 before closing at what TMX Money claims to be a locked market at 25.00, 6×10, with the bid on the TSX and the offer on Pure. Vital statistics are:

| BAM.PF.G | FixedReset | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-10-08 Maturity Price : 23.12 Evaluated at bid price : 25.00 Bid-YTW : 4.34 % |

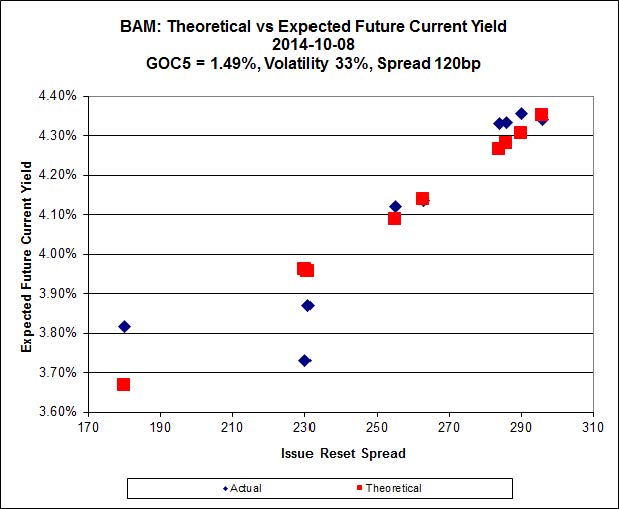

The Implied Volatility calculation for the BAM FixedResets is interesting, partly because of the very high level of Implied Volatility, but mainly because it highlights a huge gap that has opened up between BAM.PR.R (FixedReset 5.40%+230, commenced trading January, 2010) and BAM.PR.T (FixedReset 4.50%+231, commenced trading October, 2010). These are now bid at 25.4 and 24.55, respectively, despite having virtually identical Issue Reset Spreads. The next Exchange Dates for these issues differ by only nine months, which is really to short a time to introduce complicated arguments about the expected path of interest rates which would be wrong anyway. There should be some pricing difference due to the difference in the dividends currently paid, but the BAM.PR.R has only 7 payments to go until reset – the total dividend advantage is just under forty cents; one might reasonably expect the price difference to be a little under forty cents (given discounting of the dividend stream and the effect of price on post-reset expected dividend yield). But it ain’t.

[…] was issued as BAM.PF.G,a FixedReset 4.50%+284, that commenced trading 2014-10-8 after being announced 2014-10-1. The ticker changed to BN.PF.G on 2022-12-12. The issue reset to […]