Fortis Inc. has announced:

that it has entered into an agreement with a syndicate of underwriters led by Scotiabank and RBC Capital Markets (collectively, the “Underwriters”), pursuant to which the Underwriters have agreed to purchase, on a bought deal basis, from Fortis and sell to the public (the “Offering”) 12,000,000 Cumulative Redeemable Fixed Rate Reset First Preference Shares, Series M of the Corporation (the “Series M First Preference Shares”). The purchase price of $25.00 per Series M First Preference Share will result in gross proceeds for Fortis of $300,000,000.

Fortis has granted the Underwriters the option to purchase up to an additional 1,800,000 Series M First Preference Shares to cover over-allotments, if any, and for market stabilization purposes, during the 30 days following the closing of the Offering (the “Over-Allotment Option”). If the Over-Allotment Option is exercised in full, the Offering will result in gross proceeds to the Corporation of $345,000,000.

The net proceeds of the Offering will be used to repay a portion of the amounts borrowed by Fortis under its acquisition credit facility in connection with the acquisition of UNS Energy Corporation completed on August 15, 2014.

The holders of Series M First Preference Shares will be entitled to receive fixed cumulative preferential cash dividends, if, as and when declared by the Board of Directors of the Corporation (the “Board of Directors”), for the initial period commencing on the date of issue and ending on but excluding December 1, 2019 (the “Initial Period”) at a rate of 4.10%, in an amount equal to $1.0250 per Series M First Preference Share per annum paid in equal quarterly instalments. The first of such dividends, if declared, will be payable on December 1, 2014 for the period commencing on the date of issue in the amount of $0.2050 per Series M First Preference Share. The dividend rate will be reset on December 1, 2019 and thereafter every five years at a level of 2.48% above the five‑year Government of Canada Bond yield.

At the end of the Initial Period and every five years thereafter, the holders of Series M First Preference Shares will, subject to certain conditions and the right of the Corporation to redeem those shares, have the option to convert any or all of their Series M First Preference Shares into an equal number of Cumulative Redeemable Floating Rate First Preference Shares, Series N of the Corporation (the “Series N First Preference Shares”). The holders of Series N First Preference Shares will be entitled to receive floating rate cumulative preferential cash dividends, if, as and when declared by the Board of Directors, at the rate of the three-month Government of Canada Treasury Bill average yield plus 2.48%, reset on a quarterly basis.

The Offering is subject to the receipt of all necessary regulatory and stock exchange approvals. Closing is expected to occur on or about September 19, 2014 but not later than October 24, 2014.

They announced later:

that due to strong investor demand it has agreed to increase the aggregate size of its previously announced bought deal offering of Cumulative Redeemable Fixed Rate Reset First Preference Shares, Series M (the “Series M First Preference Shares”) from $300,000,000 to $600,000,000 (the “Offering”). The Offering is being made pursuant to an agreement with a syndicate of underwriters led by Scotiabank and RBC Capital Markets (collectively, the “Underwriters”) who have agreed to purchase 24,000,000 Series M First Preference Shares at a price of $25.00 per share.

The Offering will result in gross proceeds to the Corporation of $600,000,000. There will be no over-allotment option on the Offering. All other terms of the Offering are as set forth in the press release relating to the Offering issued by Fortis earlier today.

That’s a whopper! This issue will join FTS’ other three FixedResets:

| FTS FixedResets | |||||

| Ticker | Initial Rate | Issue Reset Spread | Bid Price 2014-9-2 | Bid YTW 2014-9-3 | YTW Scenario 2014-9-3 |

| FTS.PR.G | 3.883% | 213bp | 24.69 | 3.69% | Perpetuity |

| FTS.PR.H | 4.25% | 145bp | 20.96 | 3.67% | Perpetuity |

| FTS.PR.K | 4.00% | 205bp | 24.88 | 3.62% | Perpetuity |

| FTS.PR.? | 4.10% | 248bp | 25.00 Issue Price |

3.95% | Perpetuity |

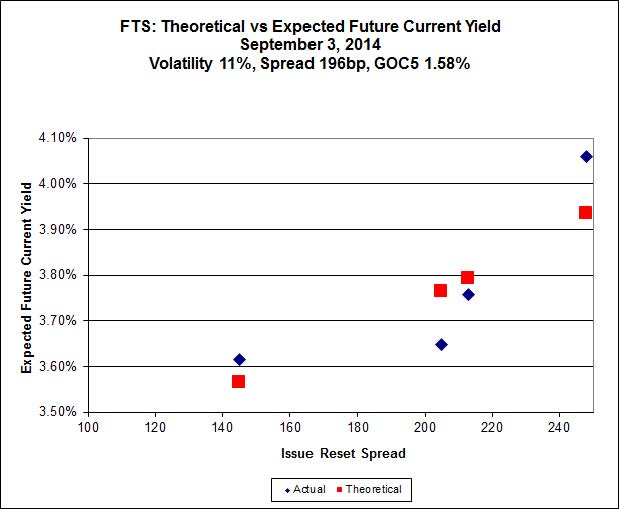

And according to Implied Volatility analysis, it is cheap relative to the other FTS issues:

Click for big

Update, 2014-9-12: Rated Pfd-2(low) [Review Developing] by DBRS.