TransCanada Corporation has announced:

that it will issue 20 million cumulative redeemable minimum rate reset first preferred shares, series 15 (the “Series 15 Preferred Shares”) at a price of $25.00 per share for aggregate gross proceeds of $500 million on a bought deal basis to a syndicate of underwriters in Canada led by Scotiabank, BMO Capital Markets, CIBC Capital Markets, RBC Capital Markets and TD Securities Inc.

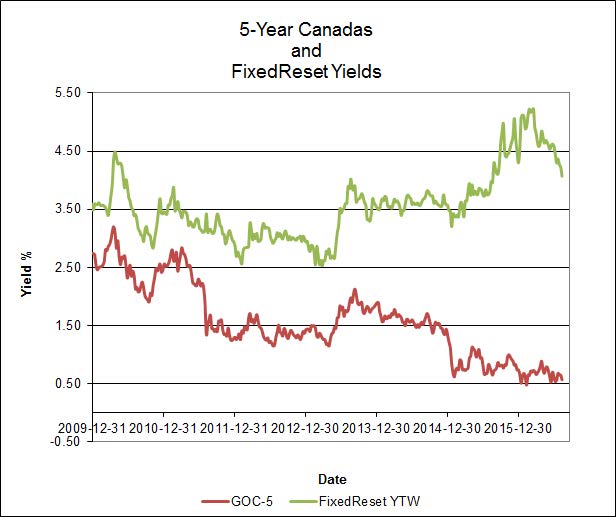

The holders of Series 15 Preferred Shares will be entitled to receive fixed cumulative dividends at an annual rate of $1.2250 per share, payable quarterly on the last business day of February, May, August and November, as and when declared by the board of directors of TransCanada. The Series 15 Preferred Shares will yield 4.90 per cent per annum for the initial fixed rate period ending May 31, 2022 with the first dividend payment date scheduled for February 28, 2017. The dividend rate will reset on May 31, 2022 and on the last business day of May in every fifth year thereafter to a rate equal to the sum of the then five-year Government of Canada bond yield plus 3.85 per cent, provided that, in any event, such rate shall not be less than 4.90 per cent per annum. The Series 15 Preferred Shares are redeemable by TransCanada, at its option, on May 31, 2022 and on the last business day of May in every fifth year thereafter at a price of $25.00 per share plus accrued and unpaid dividends.

The holders of Series 15 Preferred Shares will have the right to convert their shares into cumulative redeemable first preferred shares, series 16 (the “Series 16 Preferred Shares”), subject to certain conditions, on May 31, 2022 and on the last business day of May in every fifth year thereafter. The holders of Series 16 Preferred Shares will be entitled to receive quarterly floating rate cumulative dividends, as and when declared by the board of directors of TransCanada, at an annualized rate equal to the sum of the then 90-day Government of Canada treasury bill rate plus 3.85 per cent.

TransCanada has granted to the underwriters an option, exercisable at any time up to 48 hours prior to the closing of the offering, to purchase up to an additional 2 million Series 15 Preferred Shares at a price of $25.00 per share.

The anticipated closing date is November 21, 2016. The net proceeds of the offering will be used for general corporate purposes and to reduce short term indebtedness of TransCanada and its affiliates, which short term indebtedness was used to fund TransCanada’s capital program and for general corporate purposes.

The Series 15 Preferred Shares will be offered to the public in Canada pursuant to a prospectus supplement that will be filed with securities regulatory authorities in Canada under TransCanada’s short form base shelf prospectus dated December 23, 2015. The securities referred to herein have not been and will not be registered under the United States Securities Act of 1933, as amended, and may not be offered or sold in the United States absent registration or an applicable exemption from registration requirements.

They later announced:

that as a result of strong investor demand for its previously announced offering of cumulative redeemable minimum rate reset first preferred shares, series 15 (the “Series 15 Preferred Shares”), the size of the offering has been increased to 40 million shares. The offering no longer includes the previously granted underwriters’ option. The aggregate gross proceeds of the offering will now be $1.0 billion. The syndicate of underwriters is led by Scotiabank, BMO Capital Markets, CIBC Capital Markets, RBC Capital Markets and TD Securities Inc.

The anticipated closing date is November 21, 2016. The net proceeds of the offering will be used for general corporate purposes and to reduce short term indebtedness of TransCanada and its affiliates, which short term indebtedness was used to fund TransCanada’s capital program and for general corporate purposes.

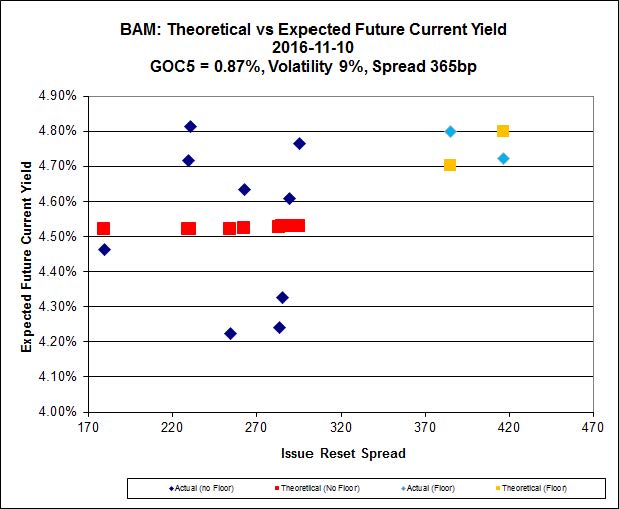

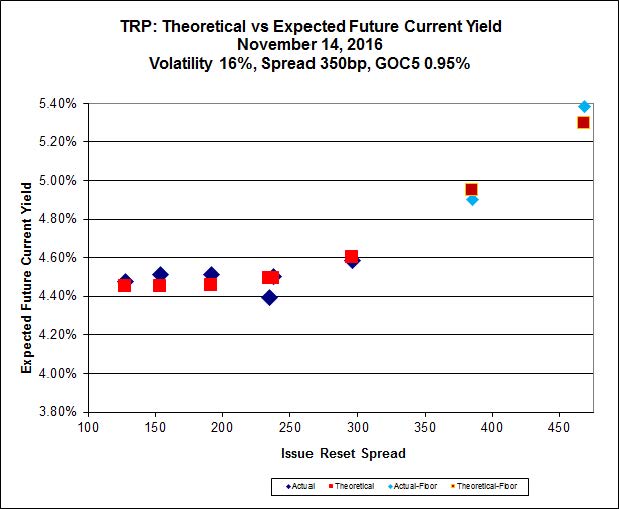

Surprisingly, this issue looks a shade expensive when the TRP series is subjected to Implied Volatility analysis:

Click for Big

However, there will be those who say that the presence of the minimum reset guarantee more than offsets the $0.25 richness of the issue price.