Well, pig ignorance and a blithe disregard of the interests of preferred shareholders has struck again, with no announcement on the BCE Inc. preferred share information page regarding the three new series that will result from the BAF conversion.

However, a certain amount of checking permits the identification of at least two tickers:

| New Ticker |

BCE Series |

Description |

Old (and continuing) ticker |

| BCE.PR.M |

“AM” |

FixedReset

4.85%+209 |

BAF.PR.A |

| BCE.PR.O |

“AO” |

FixedReset

4.55%+309 |

BAF.PR.C |

BCE.PR.Q

????????? |

“AQ” |

FixedReset

4.25%+264 |

BAF.PR.E |

For the first two, the correspondence of the first two columns has been established from the name information purchased from the Toronto Stock Exchange. The correspondence of the second column with the third has been established from the security descriptions contained within the Certificate of Amendment to the articles of BCE Inc., which may be found on SEDAR with the search results “BCE Inc. Sep 22 2014 16:50:17 ET Security holders documents – English PDF 847 K”.

I regret, as always, not being able to provide a link to this public document; however, bank-owned SEDAR prohibits direct links and hides them behind a secret API. This is in order to protect their monopoly. This monopoly has been granted to them by the Canadian Securities Administrators, of which the OSC is an important member. The banks are paying the OSC to help them preserve their hegemony over the Canadian financial system. So investors and the general public can stuff it.

Correspondence of the third and fourth columns was determined by looking up the description of the BAF issues in PrefLetter.

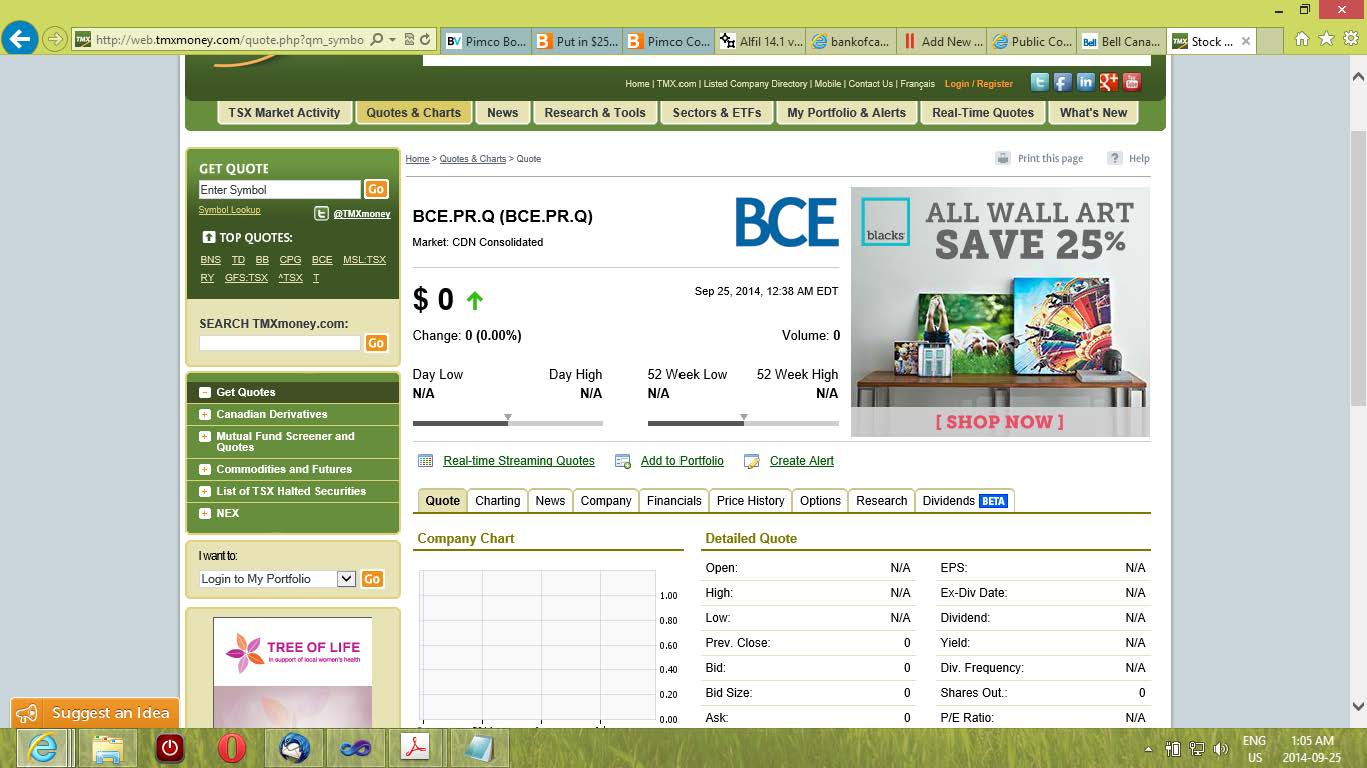

The third issue presents some problems. If we check TMX Money for BCE.PR.Q, we get the result:

Click for Big

Click for BigThis is the standard result for a new ticker the day before it starts trading – I assume it results from the symbol being in the database, but none of the other data that would normally be reported on this page is present. I am unable to obtain such a screen by typing in “BCE.PR.?”, where “?” is any unused letter (other than “M” and “O”, for which satisfactory assignments have been determined), or BCE.PF.A or BCE.PF.Q.

However, the name information file purchased from the Exchange refers to this as Series Q, not as Series AQ. One might at first hope that this is simply a typo, but on the other hand the “Q” series is referenced in both the long name and in the short name.

Further, a quick check of the BCE preferred share information page reveals that there actually is a BCE preferred share Series Q that is not currently trading. It is the RatchetRate counterpart to the FixedFloater BCE.PR.R, and the opportunity to convert into BCE.PR.Q was offered to the R-holders in 2010 but hardly anybody wanted them so everything stayed as R. It will be noted that Series Q was issued in 1995; holders of BCE.PR.R will get another chance to convert in 2015.

It will be noted that other information available from the Exchange – for a price! – indicates the listing date of BCE.PR.Q is 1995/11/21 … so if it weren’t for the fact that I can’t find any other ‘null response’ on TMX Money for a BCE ticker symbol, there would be no reason to suppose that there is any BAF.PR.E / BCE.PR.Q correspondence.

So basically, Series AQ, the former BAF.PR.E, may or may not trade on September 25 as BCE.PR.Q; if it does, then God only knows what Series Q will trade as if it comes into existence next year and God only knows if or when the Exchange will correct their name descriptions. If it doesn’t trade at BCE.PR.Q tomorrow, I don’t know what it will trade as.

This screw up was brought to you courtesy of the bank-owned Toronto Stock Exchange; as we all know, banks in Canada have a near monopoly position over the Canadian financial system, helped along by their special extra monopoly-enhancing payments to the regulators, and employ hundreds of thousands of people, not a single one of whom has any brains at all. Their work in this matter was done on behalf of BCE Inc., which is (surprise!) another near-monopoly which also provides employment exclusively for the brainless.