New Year’s is prediction season!

Bond returns will probably be ho-hum next year — just as they have been in 2015 — according to the biggest investors.

JPMorgan Chase & Co., Fidelity Investments, Pacific Investment Management Co. and Goldman Sachs Group Inc. are all cautioning investors not to be too optimistic. Goldman Sachs predicts benchmark U.S. 10-year yields will climb to 3 percent by the end of 2016 from 2.30 percent Wednesday.

…

The odds of at least one more increase in 2016 are 94 percent, futures contracts indicate, threatening to push bond yields higher worldwide.

…

An investor would lose 3.2 percent if Goldman Sachs’s yield forecast proves to be accurate, data compiled by Bloomberg show.

There is another interesting column on risk in Bloomberg, penned by Justin Fox:

Twenty years ago, Dutch journalist Sheila Sitalsing sat down with a demographer at the country’s statistics office to talk about how aging would change the Netherlands. His prediction, she recounts in a column that’s the most-read thing on the website of the Dutch newspaper de Volkskrant, was that aging would “change the atmosphere and the mentality of the country.” For example:

Things that come with being young — taking risks, seizing opportunities, daring to do things, diving into the deep end without thought and without water wings, doing drugs, making noise, calling after girls on the street corner, embracing the strange and the new — would become less common. The atmosphere would be determined by the concerns of the old: avoiding risk, being careful, preserving what you have, saying goodbye, keeping quiet, suspicion of the foreign, avoiding fuss and noise — absolutely no fuss and noise! — and seizing every possible occasion to complain at length about alleged fuss and noise.

Among other things, I was impressed that (in Holland, twenty years ago) it was possible to say anything about cat-calling girls in terms other than the deepest deprecation, and still get published!

It was a superb no-more-tax-loss-selling day for the Canadian preferred share market today, with PerpetualDiscounts up 111bp, FixedResets winning 169bp and DeemedRetractibles gaining 37bp. The Performance Highlights table is as ridiculously long as you might expect, with only a single loser. Volume was, again, pathetically low.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

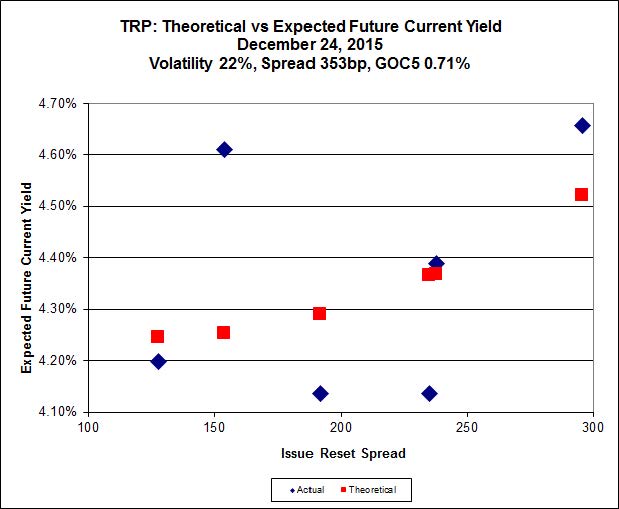

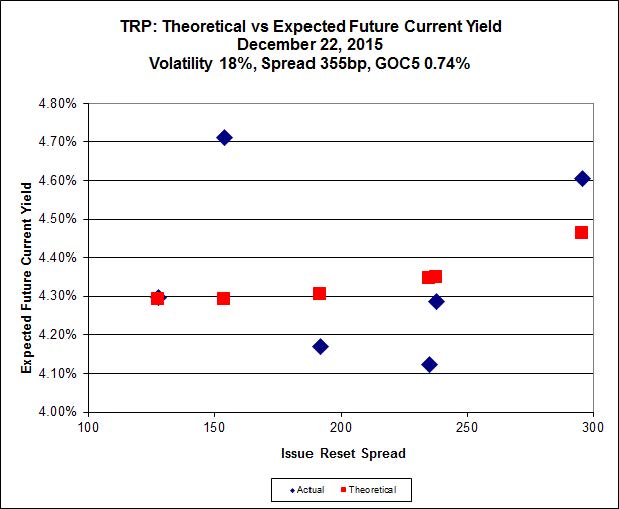

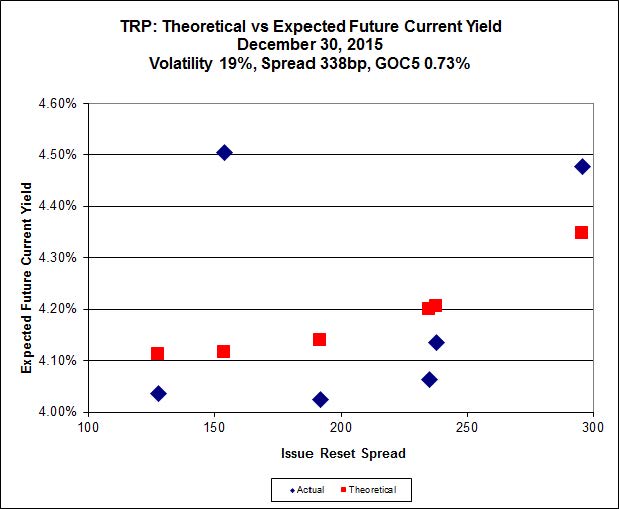

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 18.95 to be $0.62 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $1.19 cheap at its bid price of 12.60.

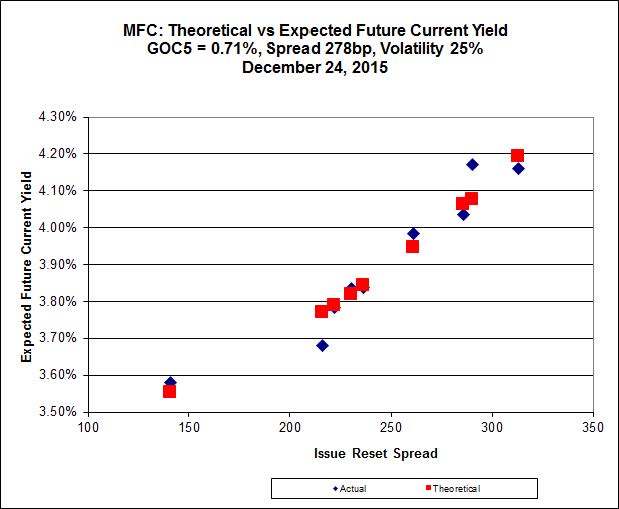

Click for Big

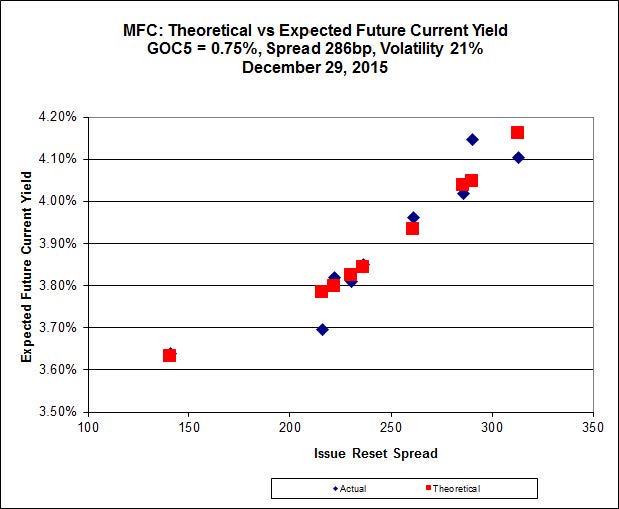

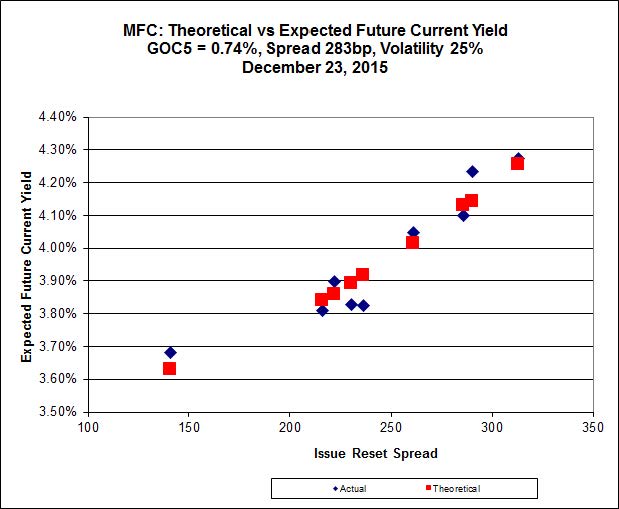

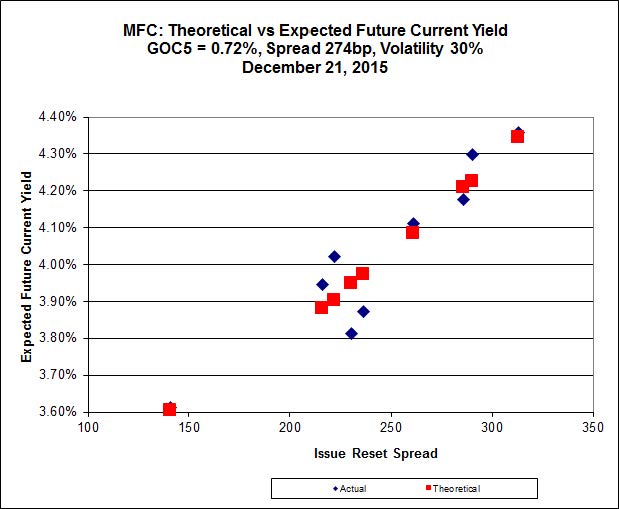

Most expensive is MFC.PR.L, resetting at +216bp on 2019-6-19, bid at 20.25 to be 0.60 rich, while MFC.PR.G, resetting at +290bp on 2016-12-19, is bid at 22.33 to be 0.67 cheap.

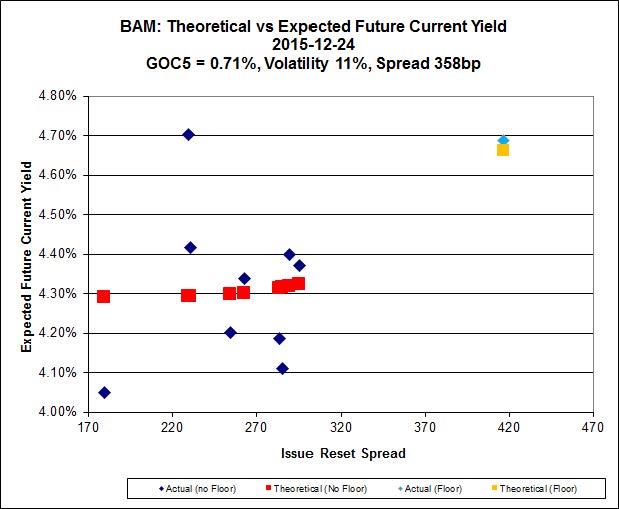

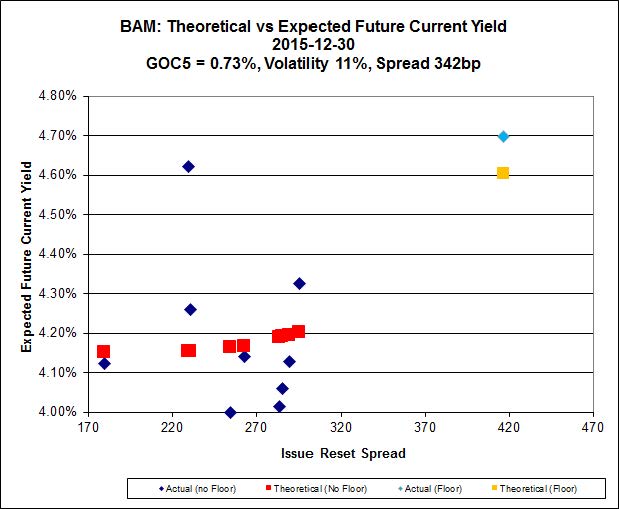

Click for Big

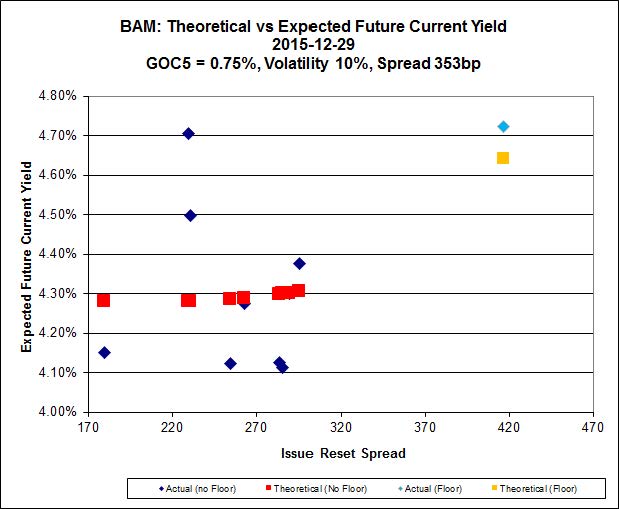

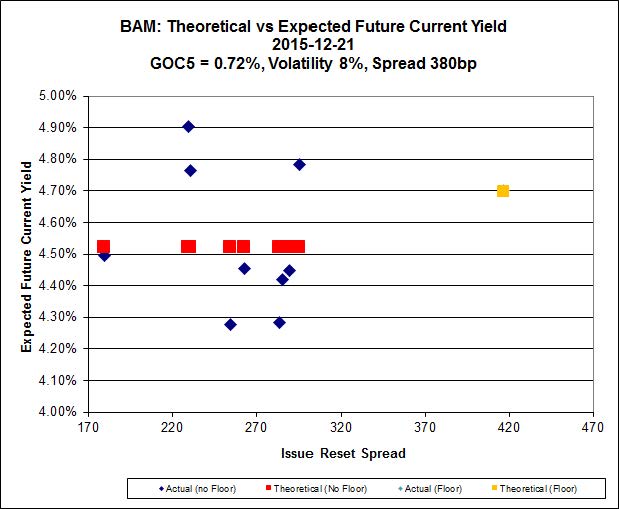

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 16.39 to be $1.85 cheap. BAM.PF.E, resetting at +255bp on 2020-3-31 is bid at 20.50 and appears to be $0.80 rich.

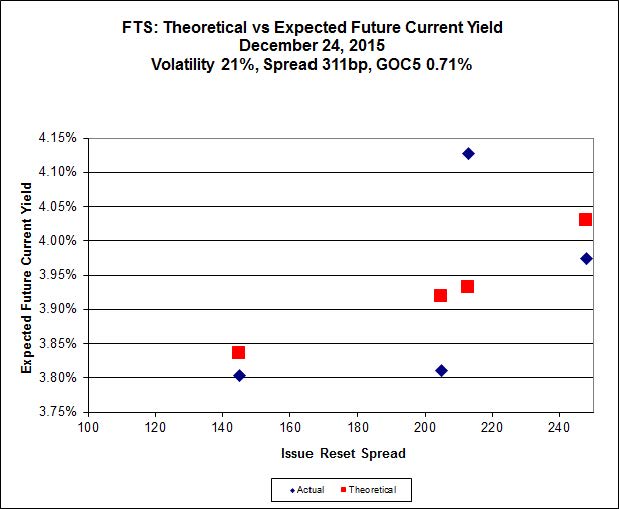

Click for Big

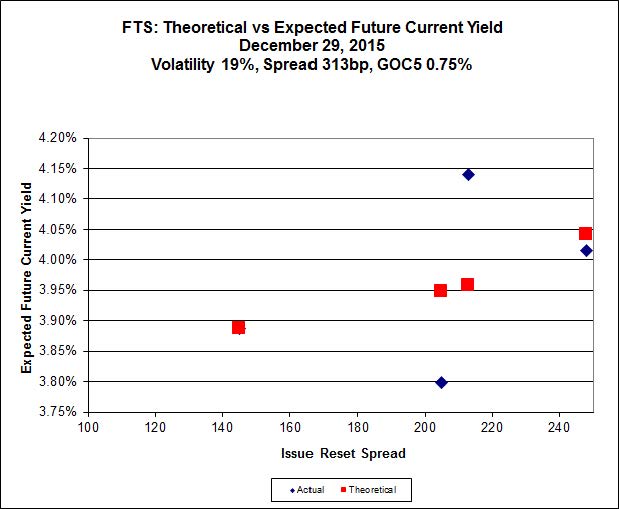

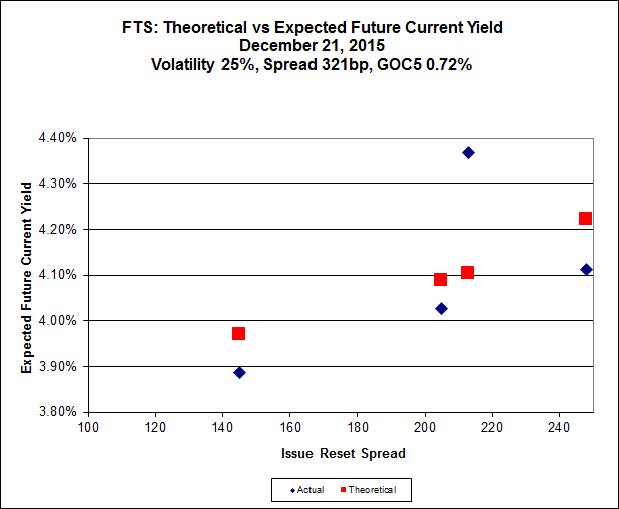

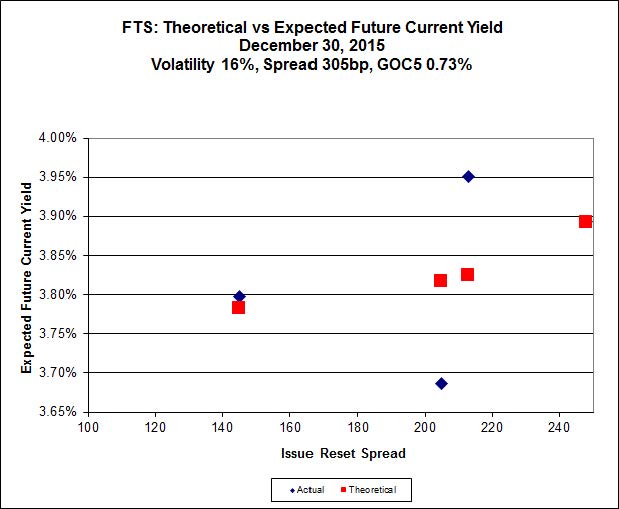

FTS.PR.K, with a spread of +205bp, and bid at 18.85, looks $0.64 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 18.10 and is $0.59 cheap.

Click for Big

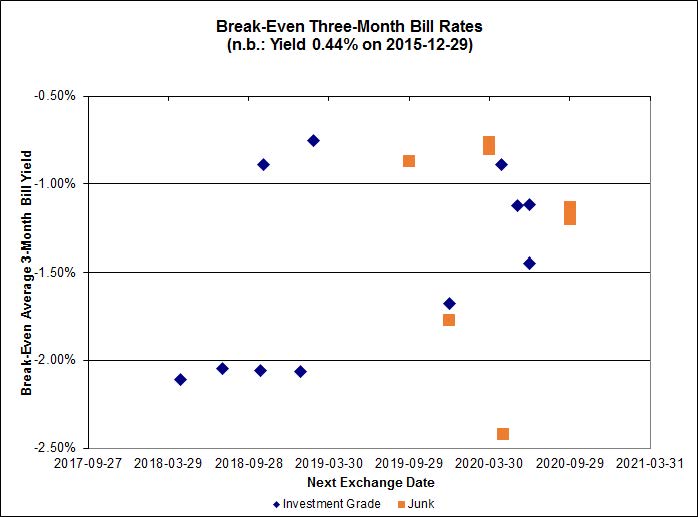

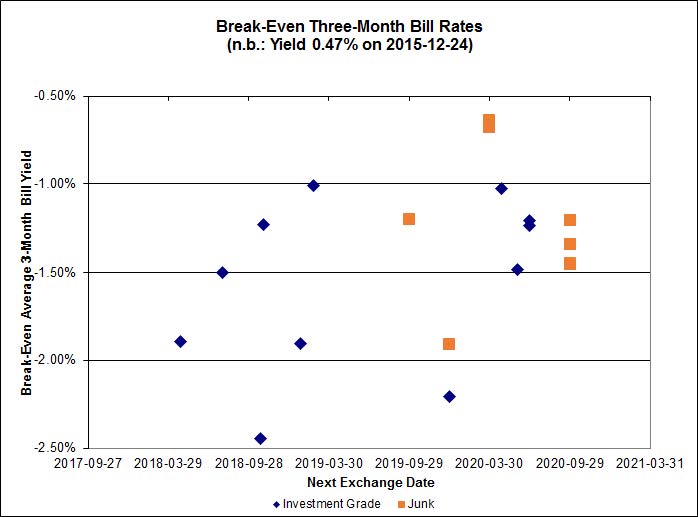

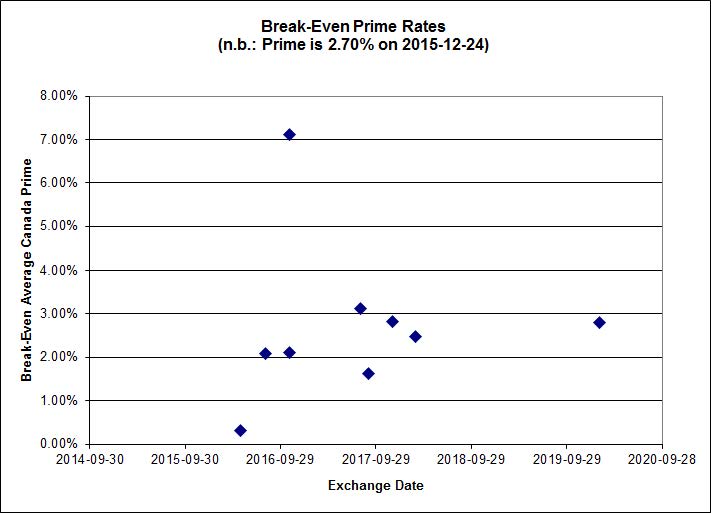

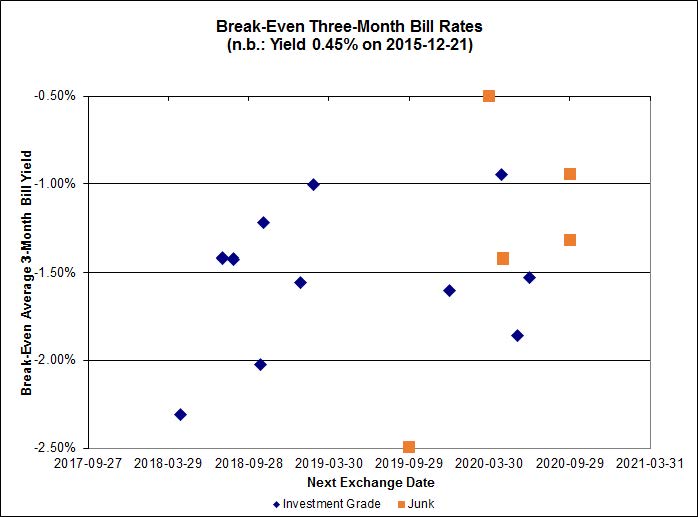

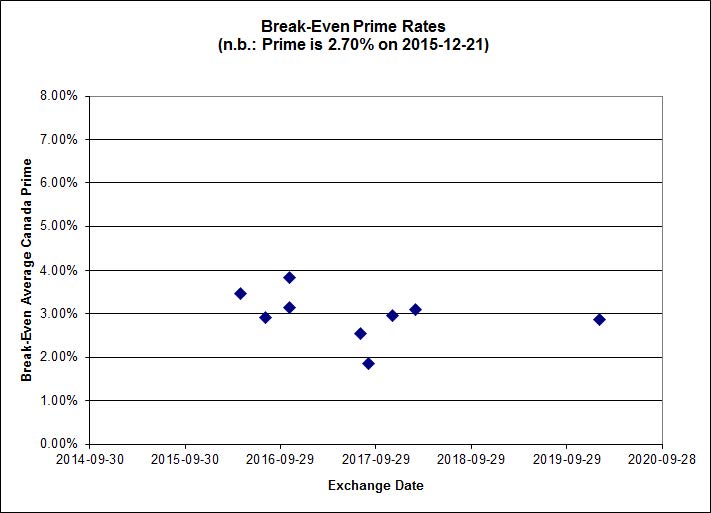

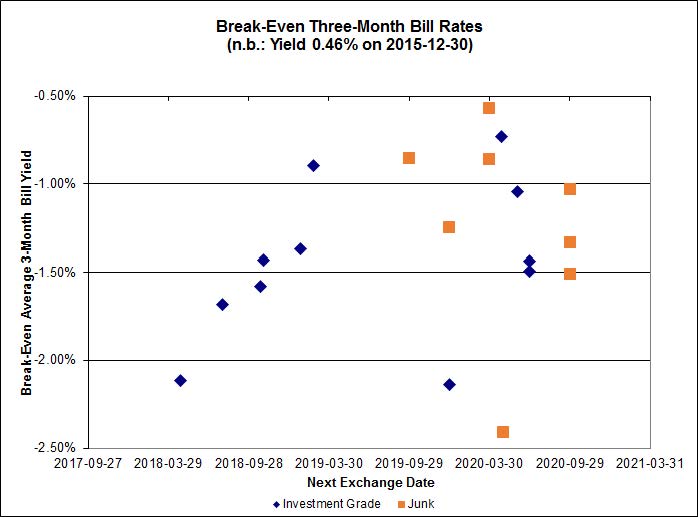

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -1.35%, with one outlier above -0.50%. There are two junk outliers above -0.50%.

Click for Big

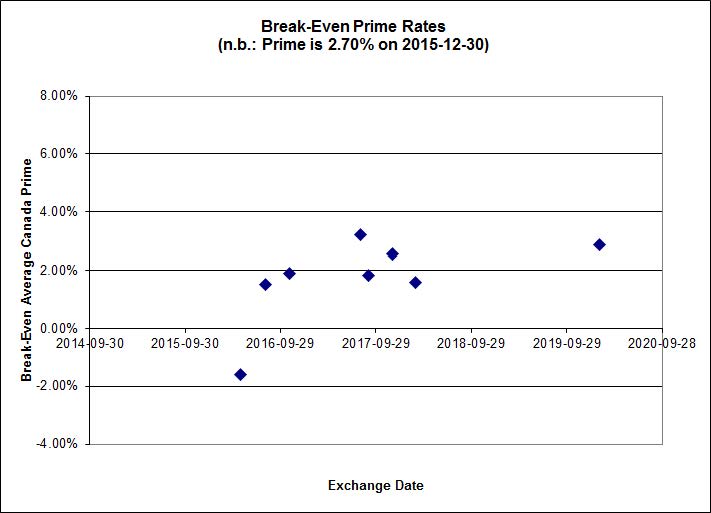

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 4.72 % | 5.71 % | 30,975 | 17.03 | 1 | 4.0462 % | 1,651.1 |

| FixedFloater | 7.06 % | 6.26 % | 37,792 | 15.89 | 1 | 0.5232 % | 2,762.9 |

| Floater | 4.17 % | 4.31 % | 81,306 | 16.79 | 4 | 2.7633 % | 1,834.4 |

| OpRet | 4.86 % | 4.17 % | 25,341 | 0.65 | 1 | 0.0000 % | 2,740.8 |

| SplitShare | 4.81 % | 5.72 % | 84,029 | 1.84 | 6 | 0.3252 % | 3,212.8 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.3252 % | 2,506.7 |

| Perpetual-Premium | 5.76 % | 5.52 % | 91,945 | 1.89 | 7 | 0.5855 % | 2,532.8 |

| Perpetual-Discount | 5.64 % | 5.71 % | 103,697 | 14.36 | 33 | 1.1113 % | 2,551.4 |

| FixedReset | 4.99 % | 4.30 % | 267,776 | 14.97 | 81 | 1.6856 % | 2,075.1 |

| Deemed-Retractible | 5.15 % | 4.78 % | 133,114 | 5.28 | 33 | 0.3729 % | 2,604.2 |

| FloatingReset | 2.77 % | 4.07 % | 69,458 | 5.63 | 11 | 0.9955 % | 2,156.2 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BAM.PF.D | Perpetual-Discount | -1.87 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 19.94 Evaluated at bid price : 19.94 Bid-YTW : 6.19 % |

| BNS.PR.Z | FixedReset | 1.06 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.99 Bid-YTW : 5.39 % |

| POW.PR.A | Perpetual-Discount | 1.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 24.25 Evaluated at bid price : 24.55 Bid-YTW : 5.71 % |

| POW.PR.B | Perpetual-Discount | 1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 23.15 Evaluated at bid price : 23.45 Bid-YTW : 5.71 % |

| SLF.PR.I | FixedReset | 1.09 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.24 Bid-YTW : 5.69 % |

| BAM.PR.R | FixedReset | 1.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 16.39 Evaluated at bid price : 16.39 Bid-YTW : 4.69 % |

| RY.PR.O | Perpetual-Discount | 1.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 22.46 Evaluated at bid price : 22.78 Bid-YTW : 5.43 % |

| MFC.PR.C | Deemed-Retractible | 1.16 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.00 Bid-YTW : 6.96 % |

| PVS.PR.D | SplitShare | 1.16 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2021-10-08 Maturity Price : 25.00 Evaluated at bid price : 22.71 Bid-YTW : 6.52 % |

| TD.PR.Y | FixedReset | 1.20 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.55 Bid-YTW : 3.41 % |

| PWF.PR.R | Perpetual-Discount | 1.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 23.95 Evaluated at bid price : 24.40 Bid-YTW : 5.71 % |

| PWF.PR.S | Perpetual-Discount | 1.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 21.57 Evaluated at bid price : 21.85 Bid-YTW : 5.57 % |

| RY.PR.N | Perpetual-Discount | 1.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 22.42 Evaluated at bid price : 22.73 Bid-YTW : 5.44 % |

| GWO.PR.H | Deemed-Retractible | 1.28 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.16 Bid-YTW : 6.57 % |

| CM.PR.Q | FixedReset | 1.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 20.55 Evaluated at bid price : 20.55 Bid-YTW : 4.29 % |

| SLF.PR.E | Deemed-Retractible | 1.30 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.06 Bid-YTW : 6.90 % |

| PWF.PR.L | Perpetual-Discount | 1.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 22.34 Evaluated at bid price : 22.61 Bid-YTW : 5.73 % |

| POW.PR.D | Perpetual-Discount | 1.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 22.22 Evaluated at bid price : 22.50 Bid-YTW : 5.56 % |

| W.PR.H | Perpetual-Discount | 1.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 22.96 Evaluated at bid price : 23.23 Bid-YTW : 5.93 % |

| ENB.PR.A | Perpetual-Discount | 1.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 22.82 Evaluated at bid price : 23.10 Bid-YTW : 6.02 % |

| BMO.PR.Z | Perpetual-Discount | 1.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 23.42 Evaluated at bid price : 23.74 Bid-YTW : 5.31 % |

| CU.PR.C | FixedReset | 1.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 19.92 Evaluated at bid price : 19.92 Bid-YTW : 4.02 % |

| RY.PR.W | Perpetual-Discount | 1.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 22.44 Evaluated at bid price : 22.70 Bid-YTW : 5.45 % |

| FTS.PR.H | FixedReset | 1.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 14.35 Evaluated at bid price : 14.35 Bid-YTW : 3.93 % |

| TD.PF.D | FixedReset | 1.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 20.79 Evaluated at bid price : 20.79 Bid-YTW : 4.30 % |

| BIP.PR.A | FixedReset | 1.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 20.61 Evaluated at bid price : 20.61 Bid-YTW : 5.28 % |

| MFC.PR.H | FixedReset | 1.44 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.98 Bid-YTW : 4.54 % |

| SLF.PR.C | Deemed-Retractible | 1.46 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.90 Bid-YTW : 6.95 % |

| TD.PF.F | Perpetual-Discount | 1.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 22.55 Evaluated at bid price : 22.88 Bid-YTW : 5.43 % |

| MFC.PR.G | FixedReset | 1.50 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.33 Bid-YTW : 5.23 % |

| PWF.PR.T | FixedReset | 1.53 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 22.60 Evaluated at bid price : 23.30 Bid-YTW : 3.48 % |

| POW.PR.G | Perpetual-Premium | 1.55 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 24.39 Evaluated at bid price : 24.86 Bid-YTW : 5.63 % |

| SLF.PR.J | FloatingReset | 1.59 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.41 Bid-YTW : 9.66 % |

| TD.PF.E | FixedReset | 1.61 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 21.72 Evaluated at bid price : 22.10 Bid-YTW : 4.11 % |

| IFC.PR.A | FixedReset | 1.61 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.40 Bid-YTW : 8.41 % |

| IAG.PR.A | Deemed-Retractible | 1.64 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.65 Bid-YTW : 6.62 % |

| ELF.PR.F | Perpetual-Discount | 1.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 22.53 Evaluated at bid price : 22.78 Bid-YTW : 5.82 % |

| TRP.PR.G | FixedReset | 1.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 20.60 Evaluated at bid price : 20.60 Bid-YTW : 4.54 % |

| BNS.PR.B | FloatingReset | 1.68 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.38 Bid-YTW : 4.12 % |

| SLF.PR.A | Deemed-Retractible | 1.70 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.09 Bid-YTW : 6.50 % |

| MFC.PR.I | FixedReset | 1.78 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.86 Bid-YTW : 4.96 % |

| W.PR.J | Perpetual-Discount | 1.84 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 23.49 Evaluated at bid price : 23.76 Bid-YTW : 5.90 % |

| PWF.PR.A | Floater | 1.85 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 12.63 Evaluated at bid price : 12.63 Bid-YTW : 3.78 % |

| NA.PR.S | FixedReset | 1.86 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 19.15 Evaluated at bid price : 19.15 Bid-YTW : 4.35 % |

| BAM.PR.C | Floater | 1.87 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 10.90 Evaluated at bid price : 10.90 Bid-YTW : 4.34 % |

| RY.PR.H | FixedReset | 1.90 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 19.35 Evaluated at bid price : 19.35 Bid-YTW : 4.11 % |

| BNS.PR.D | FloatingReset | 1.90 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.27 Bid-YTW : 6.02 % |

| BNS.PR.C | FloatingReset | 1.91 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.45 Bid-YTW : 4.26 % |

| RY.PR.M | FixedReset | 1.93 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 20.10 Evaluated at bid price : 20.10 Bid-YTW : 4.27 % |

| VNR.PR.A | FixedReset | 2.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 19.75 Evaluated at bid price : 19.75 Bid-YTW : 4.65 % |

| CU.PR.D | Perpetual-Discount | 2.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 21.77 Evaluated at bid price : 22.08 Bid-YTW : 5.60 % |

| IAG.PR.G | FixedReset | 2.09 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.00 Bid-YTW : 5.40 % |

| SLF.PR.D | Deemed-Retractible | 2.11 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.84 Bid-YTW : 6.99 % |

| TRP.PR.A | FixedReset | 2.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 16.46 Evaluated at bid price : 16.46 Bid-YTW : 4.22 % |

| TD.PF.B | FixedReset | 2.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 19.26 Evaluated at bid price : 19.26 Bid-YTW : 4.13 % |

| MFC.PR.J | FixedReset | 2.12 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.66 Bid-YTW : 5.42 % |

| CU.PR.E | Perpetual-Discount | 2.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 21.80 Evaluated at bid price : 22.13 Bid-YTW : 5.58 % |

| BAM.PR.B | Floater | 2.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 10.98 Evaluated at bid price : 10.98 Bid-YTW : 4.31 % |

| FTS.PR.J | Perpetual-Discount | 2.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 22.15 Evaluated at bid price : 22.48 Bid-YTW : 5.33 % |

| BAM.PF.G | FixedReset | 2.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 21.83 Evaluated at bid price : 22.24 Bid-YTW : 4.23 % |

| FTS.PR.I | FloatingReset | 2.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 12.41 Evaluated at bid price : 12.41 Bid-YTW : 3.88 % |

| FTS.PR.K | FixedReset | 2.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 18.85 Evaluated at bid price : 18.85 Bid-YTW : 3.96 % |

| IFC.PR.C | FixedReset | 2.35 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.01 Bid-YTW : 6.39 % |

| TD.PF.C | FixedReset | 2.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 19.25 Evaluated at bid price : 19.25 Bid-YTW : 4.12 % |

| TD.PF.A | FixedReset | 2.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 19.35 Evaluated at bid price : 19.35 Bid-YTW : 4.12 % |

| TRP.PR.C | FixedReset | 2.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 12.60 Evaluated at bid price : 12.60 Bid-YTW : 4.48 % |

| BAM.PF.E | FixedReset | 2.45 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 20.50 Evaluated at bid price : 20.50 Bid-YTW : 4.31 % |

| PWF.PR.P | FixedReset | 2.47 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 14.50 Evaluated at bid price : 14.50 Bid-YTW : 4.05 % |

| FTS.PR.M | FixedReset | 2.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 20.61 Evaluated at bid price : 20.61 Bid-YTW : 4.13 % |

| CU.PR.H | Perpetual-Discount | 2.56 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 23.33 Evaluated at bid price : 23.64 Bid-YTW : 5.60 % |

| CU.PR.G | Perpetual-Discount | 2.58 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 20.65 Evaluated at bid price : 20.65 Bid-YTW : 5.51 % |

| ELF.PR.H | Perpetual-Discount | 2.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 23.16 Evaluated at bid price : 23.59 Bid-YTW : 5.83 % |

| BAM.PF.B | FixedReset | 2.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 20.29 Evaluated at bid price : 20.29 Bid-YTW : 4.32 % |

| BMO.PR.Y | FixedReset | 2.66 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 21.20 Evaluated at bid price : 21.20 Bid-YTW : 4.19 % |

| NA.PR.W | FixedReset | 2.66 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 18.50 Evaluated at bid price : 18.50 Bid-YTW : 4.33 % |

| RY.PR.J | FixedReset | 2.71 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 20.49 Evaluated at bid price : 20.49 Bid-YTW : 4.30 % |

| RY.PR.Z | FixedReset | 2.72 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 19.26 Evaluated at bid price : 19.26 Bid-YTW : 4.08 % |

| SLF.PR.H | FixedReset | 2.72 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.50 Bid-YTW : 6.88 % |

| HSE.PR.G | FixedReset | 2.75 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 19.06 Evaluated at bid price : 19.06 Bid-YTW : 5.72 % |

| TRP.PR.B | FixedReset | 2.89 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 12.45 Evaluated at bid price : 12.45 Bid-YTW : 4.09 % |

| MFC.PR.L | FixedReset | 2.90 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.25 Bid-YTW : 6.11 % |

| MFC.PR.N | FixedReset | 3.00 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.61 Bid-YTW : 5.99 % |

| BMO.PR.W | FixedReset | 3.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 19.16 Evaluated at bid price : 19.16 Bid-YTW : 4.09 % |

| TRP.PR.H | FloatingReset | 3.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 10.22 Evaluated at bid price : 10.22 Bid-YTW : 4.26 % |

| BMO.PR.T | FixedReset | 3.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 19.30 Evaluated at bid price : 19.30 Bid-YTW : 4.10 % |

| MFC.PR.M | FixedReset | 3.22 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.85 Bid-YTW : 5.90 % |

| TRP.PR.D | FixedReset | 3.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 18.80 Evaluated at bid price : 18.80 Bid-YTW : 4.31 % |

| CM.PR.O | FixedReset | 3.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 19.55 Evaluated at bid price : 19.55 Bid-YTW : 4.09 % |

| SLF.PR.G | FixedReset | 3.51 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.64 Bid-YTW : 8.14 % |

| HSE.PR.C | FixedReset | 3.54 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 17.56 Evaluated at bid price : 17.56 Bid-YTW : 5.73 % |

| BMO.PR.S | FixedReset | 3.58 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 19.95 Evaluated at bid price : 19.95 Bid-YTW : 4.06 % |

| BAM.PF.A | FixedReset | 3.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 21.58 Evaluated at bid price : 21.99 Bid-YTW : 4.24 % |

| HSE.PR.E | FixedReset | 3.87 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 18.80 Evaluated at bid price : 18.80 Bid-YTW : 5.81 % |

| BAM.PR.E | Ratchet | 4.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 25.00 Evaluated at bid price : 14.40 Bid-YTW : 5.71 % |

| FTS.PR.G | FixedReset | 4.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 18.10 Evaluated at bid price : 18.10 Bid-YTW : 4.16 % |

| HSE.PR.A | FixedReset | 4.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 12.65 Evaluated at bid price : 12.65 Bid-YTW : 4.87 % |

| BAM.PR.T | FixedReset | 4.88 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 17.84 Evaluated at bid price : 17.84 Bid-YTW : 4.38 % |

| BAM.PR.K | Floater | 5.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 10.86 Evaluated at bid price : 10.86 Bid-YTW : 4.36 % |

| CM.PR.P | FixedReset | 5.51 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 19.15 Evaluated at bid price : 19.15 Bid-YTW : 4.08 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BAM.PR.R | FixedReset | 52,000 | Desjardins crossed 20,000 at 16.34 and another 20,000 at 16.35. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 16.39 Evaluated at bid price : 16.39 Bid-YTW : 4.69 % |

| RY.PR.Q | FixedReset | 35,037 | Recent new issue. YTW SCENARIO Maturity Type : Call Maturity Date : 2021-05-24 Maturity Price : 25.00 Evaluated at bid price : 25.75 Bid-YTW : 4.93 % |

| BNS.PR.E | FixedReset | 18,145 | Recent new issue. YTW SCENARIO Maturity Type : Call Maturity Date : 2021-04-25 Maturity Price : 25.00 Evaluated at bid price : 25.77 Bid-YTW : 4.91 % |

| TRP.PR.C | FixedReset | 14,950 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 12.60 Evaluated at bid price : 12.60 Bid-YTW : 4.48 % |

| RY.PR.H | FixedReset | 14,361 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 19.35 Evaluated at bid price : 19.35 Bid-YTW : 4.11 % |

| TD.PF.A | FixedReset | 14,200 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-30 Maturity Price : 19.35 Evaluated at bid price : 19.35 Bid-YTW : 4.12 % |

| There were 5 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| TD.PF.E | FixedReset | Quote: 22.10 – 25.00 Spot Rate : 2.9000 Average : 1.6647 YTW SCENARIO |

| CIU.PR.A | Perpetual-Discount | Quote: 20.30 – 21.25 Spot Rate : 0.9500 Average : 0.6063 YTW SCENARIO |

| BAM.PF.D | Perpetual-Discount | Quote: 19.94 – 20.66 Spot Rate : 0.7200 Average : 0.4296 YTW SCENARIO |

| FTS.PR.F | Perpetual-Discount | Quote: 22.66 – 23.54 Spot Rate : 0.8800 Average : 0.5934 YTW SCENARIO |

| MFC.PR.K | FixedReset | Quote: 19.62 – 20.50 Spot Rate : 0.8800 Average : 0.6176 YTW SCENARIO |

| TRP.PR.E | FixedReset | Quote: 18.95 – 19.69 Spot Rate : 0.7400 Average : 0.5290 YTW SCENARIO |