Oil fell to the lowest level in more than six years amid speculation that a record global glut will be prolonged after OPEC effectively abandoned its longtime strategy of limiting output to control prices.

…

West Texas Intermediate for January delivery sank $2.32, or 5.8 percent, to settle at $37.65 a barrel on the New York Mercantile Exchange, the lowest close since February 2009. The volume of all futures traded was 63 percent above the 100-day average at 2:40 p.m.

…

Tumbling oil helped spur a rout in energy stocks, which were the worst performers on the Standard & Poor’s 500 Index. Williams Cos., a pipeline company, dropped 17 percent, making it the worst performer on the S&P 500 Monday. Exxon Mobil Corp. and Chevron Corp., the biggest U.S. energy producers, fell 2.9 percent and 2.6 percent, respectively. The pain wasn’t limited to the U.S., as BP Plc slipped 3.4 percent and Royal Dutch Shell Plc decreased 4.2 percent.

Oil’s struggles mean more suffering for the Canadian dollar. It fell .84 of a cent to 74 cents (U.S.) on Monday, its lowest since June of 2004. Energy products represented roughly a quarter of Canada’s exports last year, and oil’s slump has been the key factor in the loonie’s 21-per-cent nosedive against its U.S. counterpart since the middle of 2014.

…

The Toronto Stock Exchange’s oil and gas index tumbled 6 per cent, the main factor in a 2.4-per-cent slide in the S&P/TSX composite index. Energy stocks make up nearly a fifth of the composite index. Companies with the highest debt levels and focus on oil took the biggest hits. Penn West Petroleum Ltd. sank nearly18 per cent, and Baytex Energy Corp. fell 17 per cent.

Things may seem bleak, but take heart! There’s some more drone news today:

The ranks of older and frail adults are growing rapidly in the developed world, raising alarms about how society is going to help them take care of themselves in their own homes.

Naira Hovakimyan has an idea: drones.

The University of Illinois roboticist recently received a $1.5 million grant from the National Science Foundation to explore the idea of designing small autonomous drones to perform simple household chores, like retrieving a bottle of medicine from another room. Dr. Hovakimyan acknowledged that the idea might seem off-putting to many, but she believes that drones not only will be safe, but will become an everyday fixture in elder care within a decade or two.

And for preferred share investors …

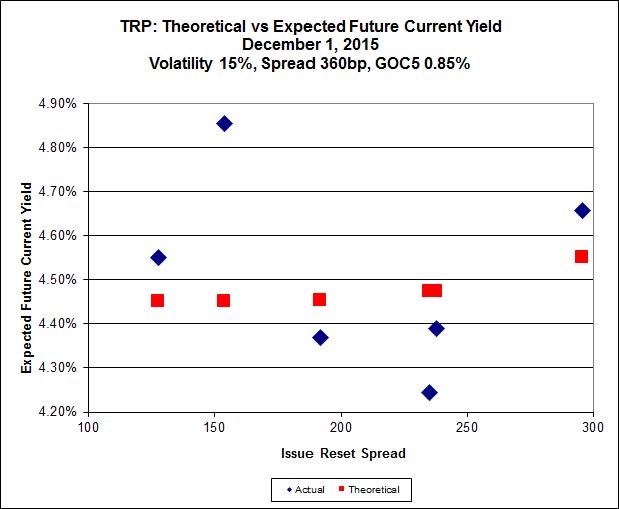

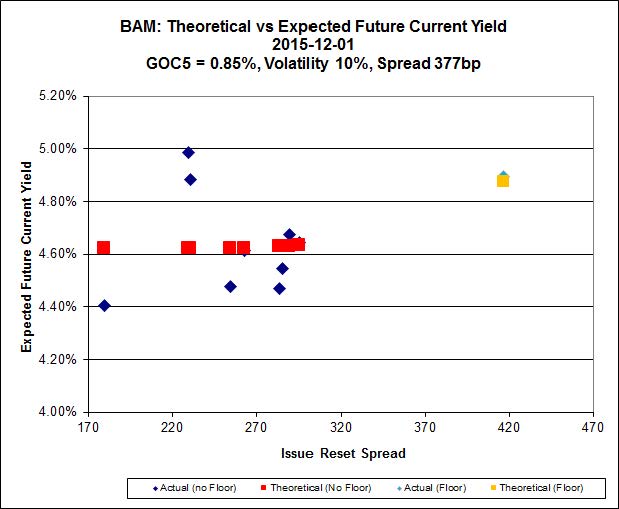

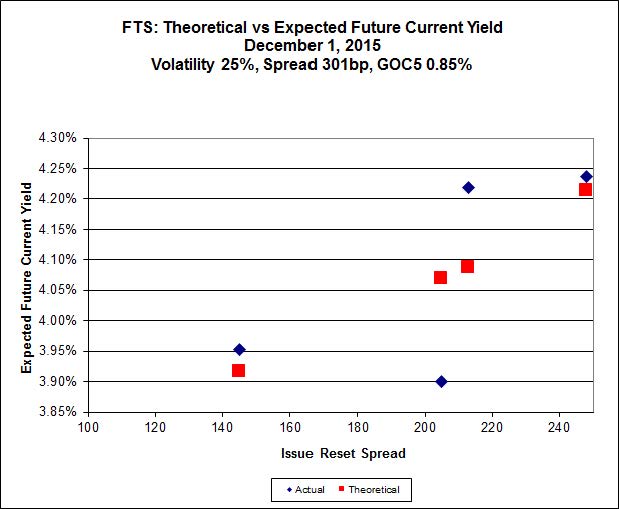

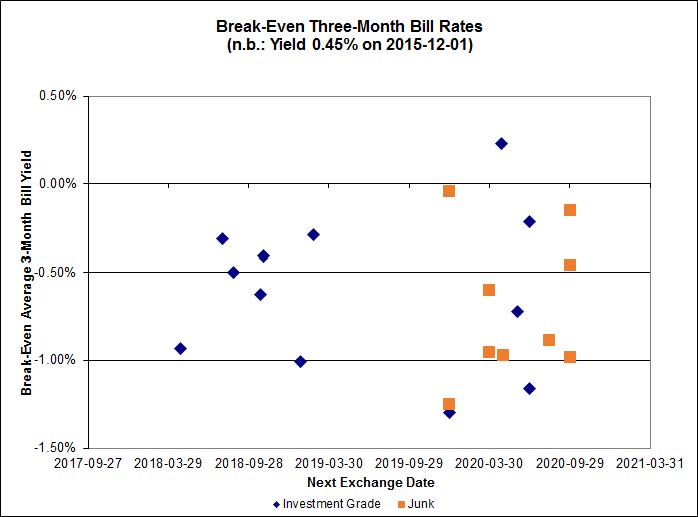

Click for Big

It was a horrible day for the Canadian preferred share market, with PerpetualDiscounts losing 124bp, FixedResets down 99bp and DeemedRetractibles off 9bp. Let’s just not talk about the Performance Highlights table, OK? Volume was very, very extremely much huge, enlivened by a stack of after-hours contingent crosses by Nesbitt.

For those keeping score, TXPR is now down about 4.12% on the month to date and is now down to October 19 levels – about 4.23% above the low of October 14.

TXPL is down about 5.33% on the month to date and is also down to October 19 levels – about 4.52% above the October 14 low.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 5.04 % | 6.12 % | 35,311 | 16.51 | 1 | -9.0909 % | 1,540.9 |

| FixedFloater | 6.86 % | 6.07 % | 31,670 | 16.18 | 1 | -4.6143 % | 2,845.1 |

| Floater | 4.30 % | 4.50 % | 74,465 | 16.34 | 4 | -1.2573 % | 1,761.9 |

| OpRet | 4.86 % | 4.02 % | 29,400 | 0.72 | 1 | -0.0397 % | 2,736.5 |

| SplitShare | 4.80 % | 5.50 % | 85,917 | 2.87 | 6 | -0.1839 % | 3,212.3 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.1839 % | 2,506.4 |

| Perpetual-Premium | 5.81 % | 5.84 % | 88,033 | 14.00 | 7 | -0.3412 % | 2,493.2 |

| Perpetual-Discount | 5.73 % | 5.81 % | 99,680 | 14.15 | 33 | -1.2382 % | 2,498.5 |

| FixedReset | 5.28 % | 4.85 % | 232,665 | 14.77 | 77 | -0.9915 % | 1,951.0 |

| Deemed-Retractible | 5.25 % | 5.34 % | 130,657 | 5.34 | 33 | -0.0855 % | 2,552.0 |

| FloatingReset | 2.75 % | 3.95 % | 62,476 | 5.71 | 11 | -0.5768 % | 2,140.0 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BAM.PR.E | Ratchet | -9.09 % | Sort-of reasonable, as the issue traded 4,600 shares in a range of 13.35-14.50 before closing at 13.50-14.59, 3×5. There were only five trades after 2:30pm, totaling 1400 shares, commencing with a trade at 14.10 and sporadically declining to 13.35. The VWAP was 14.21. I have not checked whether this lamentable state of affairs is due to inadequate Toronto Stock Exchange reporting or inadequate Toronto Stock Exchange supervision of market-makers. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 25.00 Evaluated at bid price : 13.50 Bid-YTW : 6.12 % |

| MFC.PR.L | FixedReset | -6.65 % | Not entirely unreasonable, since the issue traded 18,101 shares in a range of 17.40-18.64 before closing at 17.42-74, 3×1. VWAP was 17.96. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.42 Bid-YTW : 8.23 % |

| ELF.PR.H | Perpetual-Discount | -6.26 % | Ridiculous, as the issue traded 6,528 shares in a range of 23.25-97 before closing at 22.03-00, 5×3. VWAP was 23.47. I have not checked whether this lamentable state of affairs is due to inadequate Toronto Stock Exchange reporting or inadequate Toronto Stock Exchange supervision of market-makers. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 21.74 Evaluated at bid price : 22.03 Bid-YTW : 6.34 % |

| HSE.PR.C | FixedReset | -5.79 % | Entirely reasonable, as the issue traded 19,063 shares in a range of 18.57-19.86 before closing at 18.70-26, 1×1. VWAP was 19.17; There were quite a few trades below the closing bid after 3:30pm. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 18.70 Evaluated at bid price : 18.70 Bid-YTW : 5.54 % |

| BAM.PR.G | FixedFloater | -4.61 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 25.00 Evaluated at bid price : 13.85 Bid-YTW : 6.07 % |

| SLF.PR.I | FixedReset | -4.08 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.30 Bid-YTW : 7.12 % |

| TRP.PR.G | FixedReset | -4.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 18.68 Evaluated at bid price : 18.68 Bid-YTW : 5.17 % |

| MFC.PR.N | FixedReset | -3.94 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.54 Bid-YTW : 7.48 % |

| MFC.PR.M | FixedReset | -3.88 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.60 Bid-YTW : 7.51 % |

| IFC.PR.A | FixedReset | -3.77 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.06 Bid-YTW : 9.94 % |

| ELF.PR.F | Perpetual-Discount | -3.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 21.91 Evaluated at bid price : 22.15 Bid-YTW : 6.07 % |

| HSE.PR.E | FixedReset | -2.94 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 20.15 Evaluated at bid price : 20.15 Bid-YTW : 5.56 % |

| FTS.PR.M | FixedReset | -2.84 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 18.12 Evaluated at bid price : 18.12 Bid-YTW : 4.90 % |

| CU.PR.H | Perpetual-Discount | -2.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 22.08 Evaluated at bid price : 22.41 Bid-YTW : 5.89 % |

| MFC.PR.I | FixedReset | -2.74 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.20 Bid-YTW : 6.75 % |

| VNR.PR.A | FixedReset | -2.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 18.01 Evaluated at bid price : 18.01 Bid-YTW : 5.32 % |

| TD.PF.E | FixedReset | -2.64 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 20.69 Evaluated at bid price : 20.69 Bid-YTW : 4.58 % |

| TRP.PR.H | FloatingReset | -2.53 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 10.00 Evaluated at bid price : 10.00 Bid-YTW : 4.27 % |

| SLF.PR.H | FixedReset | -2.49 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.43 Bid-YTW : 8.62 % |

| HSE.PR.G | FixedReset | -2.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 20.80 Evaluated at bid price : 20.80 Bid-YTW : 5.37 % |

| MFC.PR.G | FixedReset | -2.28 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.10 Bid-YTW : 6.78 % |

| BAM.PR.N | Perpetual-Discount | -2.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 19.37 Evaluated at bid price : 19.37 Bid-YTW : 6.26 % |

| PWF.PR.A | Floater | -2.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 12.25 Evaluated at bid price : 12.25 Bid-YTW : 3.88 % |

| IAG.PR.A | Deemed-Retractible | -1.98 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.75 Bid-YTW : 7.16 % |

| BAM.PF.C | Perpetual-Discount | -1.94 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 19.68 Evaluated at bid price : 19.68 Bid-YTW : 6.29 % |

| BIP.PR.A | FixedReset | -1.94 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 19.76 Evaluated at bid price : 19.76 Bid-YTW : 5.66 % |

| PWF.PR.R | Perpetual-Discount | -1.86 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 23.27 Evaluated at bid price : 23.70 Bid-YTW : 5.86 % |

| TRP.PR.E | FixedReset | -1.84 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 18.11 Evaluated at bid price : 18.11 Bid-YTW : 4.83 % |

| BAM.PR.X | FixedReset | -1.84 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 13.86 Evaluated at bid price : 13.86 Bid-YTW : 5.29 % |

| CU.PR.C | FixedReset | -1.79 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 17.55 Evaluated at bid price : 17.55 Bid-YTW : 4.80 % |

| MFC.PR.H | FixedReset | -1.76 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.23 Bid-YTW : 6.31 % |

| POW.PR.D | Perpetual-Discount | -1.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 21.56 Evaluated at bid price : 21.82 Bid-YTW : 5.81 % |

| FTS.PR.K | FixedReset | -1.73 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 17.00 Evaluated at bid price : 17.00 Bid-YTW : 4.62 % |

| BAM.PR.M | Perpetual-Discount | -1.72 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 19.47 Evaluated at bid price : 19.47 Bid-YTW : 6.23 % |

| BAM.PF.D | Perpetual-Discount | -1.72 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 20.05 Evaluated at bid price : 20.05 Bid-YTW : 6.24 % |

| BAM.PR.C | Floater | -1.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 10.52 Evaluated at bid price : 10.52 Bid-YTW : 4.55 % |

| TRP.PR.B | FixedReset | -1.67 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 11.22 Evaluated at bid price : 11.22 Bid-YTW : 4.83 % |

| IFC.PR.C | FixedReset | -1.65 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.31 Bid-YTW : 8.72 % |

| CU.PR.D | Perpetual-Discount | -1.64 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 21.31 Evaluated at bid price : 21.58 Bid-YTW : 5.71 % |

| FTS.PR.H | FixedReset | -1.60 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 13.54 Evaluated at bid price : 13.54 Bid-YTW : 4.42 % |

| SLF.PR.G | FixedReset | -1.58 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.36 Bid-YTW : 9.29 % |

| PWF.PR.L | Perpetual-Discount | -1.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 22.03 Evaluated at bid price : 22.26 Bid-YTW : 5.80 % |

| MFC.PR.F | FixedReset | -1.36 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.46 Bid-YTW : 9.37 % |

| IAG.PR.G | FixedReset | -1.36 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.37 Bid-YTW : 6.56 % |

| HSE.PR.A | FixedReset | -1.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 12.38 Evaluated at bid price : 12.38 Bid-YTW : 5.31 % |

| PWF.PR.E | Perpetual-Discount | -1.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 23.41 Evaluated at bid price : 23.70 Bid-YTW : 5.87 % |

| PWF.PR.F | Perpetual-Discount | -1.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 22.28 Evaluated at bid price : 22.55 Bid-YTW : 5.89 % |

| CM.PR.P | FixedReset | -1.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 17.40 Evaluated at bid price : 17.40 Bid-YTW : 4.77 % |

| TRP.PR.D | FixedReset | -1.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 17.35 Evaluated at bid price : 17.35 Bid-YTW : 4.98 % |

| SLF.PR.C | Deemed-Retractible | -1.20 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.69 Bid-YTW : 7.73 % |

| CU.PR.E | Perpetual-Discount | -1.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 21.55 Evaluated at bid price : 21.55 Bid-YTW : 5.73 % |

| W.PR.J | Perpetual-Discount | -1.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 23.56 Evaluated at bid price : 23.83 Bid-YTW : 5.96 % |

| BNS.PR.A | FloatingReset | -1.12 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.00 Bid-YTW : 3.92 % |

| BAM.PF.G | FixedReset | -1.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 19.53 Evaluated at bid price : 19.53 Bid-YTW : 5.13 % |

| SLF.PR.E | Deemed-Retractible | -1.04 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.89 Bid-YTW : 7.64 % |

| ENB.PR.A | Perpetual-Discount | -1.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 23.48 Evaluated at bid price : 23.75 Bid-YTW : 5.82 % |

| POW.PR.A | Perpetual-Discount | -1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 23.74 Evaluated at bid price : 24.05 Bid-YTW : 5.91 % |

| BAM.PF.H | FixedReset | 1.07 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2020-12-31 Maturity Price : 25.00 Evaluated at bid price : 25.57 Bid-YTW : 4.72 % |

| NA.PR.S | FixedReset | 1.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 17.93 Evaluated at bid price : 17.93 Bid-YTW : 4.85 % |

| MFC.PR.B | Deemed-Retractible | 1.67 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.72 Bid-YTW : 7.26 % |

| GWO.PR.N | FixedReset | 1.96 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.51 Bid-YTW : 9.97 % |

| TRP.PR.C | FixedReset | 2.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 12.30 Evaluated at bid price : 12.30 Bid-YTW : 5.01 % |

| GWO.PR.S | Deemed-Retractible | 5.16 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.26 Bid-YTW : 5.66 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BMO.PR.S | FixedReset | 313,635 | Nesbitt crossed 293,800 at 18.82 after hours as a contingent cross. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 18.75 Evaluated at bid price : 18.75 Bid-YTW : 4.52 % |

| MFC.PR.M | FixedReset | 292,516 | Nesbitt crossed 274,100 at 18.60 after hours as a contingent cross. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.60 Bid-YTW : 7.51 % |

| BAM.PF.G | FixedReset | 271,995 | Nesbitt crossed 251,200 at 19.58 after hours as a contingent cross. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 19.53 Evaluated at bid price : 19.53 Bid-YTW : 5.13 % |

| BAM.PF.F | FixedReset | 265,625 | Nesbitt crossed 260,000 at 19.65 after hours as a contingent cross. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 19.60 Evaluated at bid price : 19.60 Bid-YTW : 5.09 % |

| RY.PR.J | FixedReset | 255,232 | Nesbitt crossed 228,400 at 19.83 after hours as a contingent cross. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 19.75 Evaluated at bid price : 19.75 Bid-YTW : 4.62 % |

| FTS.PR.M | FixedReset | 203,405 | Nesbitt crossed 184,800 at 18.40 after hours as a contingent cross. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 18.12 Evaluated at bid price : 18.12 Bid-YTW : 4.90 % |

| BAM.PR.T | FixedReset | 185,974 | Nesbitt crossed 166,400 at 15.43 after hours as a contingent cross. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 15.30 Evaluated at bid price : 15.30 Bid-YTW : 5.51 % |

| POW.PR.G | Perpetual-Premium | 184,737 | Nesbitt crossed 178,700 at 24.40 after hours as a contingent cross. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 23.90 Evaluated at bid price : 24.39 Bid-YTW : 5.81 % |

| HSE.PR.E | FixedReset | 171,252 | Nesbitt crossed 159,900 at 20.31 after hours as a contingent cross. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 20.15 Evaluated at bid price : 20.15 Bid-YTW : 5.56 % |

| BAM.PR.N | Perpetual-Discount | 168,241 | Nesbitt crossed 152,100 at 19.50 after hours as a contingent cross. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 19.37 Evaluated at bid price : 19.37 Bid-YTW : 6.26 % |

| TRP.PR.D | FixedReset | 154,478 | RBC crossed 14,100 at 17.55. Desjardins crossed 101,600 at 17.29. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 17.35 Evaluated at bid price : 17.35 Bid-YTW : 4.98 % |

| CU.PR.H | Perpetual-Discount | 150,827 | Nesbitt crossed 141,600 at 22.41 after hours as a contingent cross. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 22.08 Evaluated at bid price : 22.41 Bid-YTW : 5.89 % |

| RY.PR.P | Perpetual-Discount | 138,408 | Nesbitt crossed 137,000 at 24.79 after hours as a contingent cross. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 24.41 Evaluated at bid price : 24.79 Bid-YTW : 5.37 % |

| BNS.PR.M | Deemed-Retractible | 138,241 | Nesbitt crossed 126,500 at 25.01 after hours as a contingent cross. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.01 Bid-YTW : 4.60 % |

| BNS.PR.L | Deemed-Retractible | 135,762 | Nesbitt crossed 127,900 at 25.02 after hours as a contingent cross. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.01 Bid-YTW : 4.60 % |

| RY.PR.F | Deemed-Retractible | 124,132 | RBC crossed 49,400 at 24.82. Nesbitt crossed 61,700 at 24.78 after hours as a contingent cross. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.77 Bid-YTW : 4.68 % |

| BAM.PF.E | FixedReset | 117,469 | Nesbitt crossed 102,700 at 18.74 after hours as a contingent cross. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 18.37 Evaluated at bid price : 18.37 Bid-YTW : 5.10 % |

| TD.PF.F | Perpetual-Discount | 117,273 | Nesbitt crossed 114,200 at 22.72 after hours as a contingent cross. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 22.39 Evaluated at bid price : 22.69 Bid-YTW : 5.45 % |

| BAM.PR.Z | FixedReset | 116,350 | Nesbitt crossed 89,700 at 19.72 after hours as a contingent cross. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 19.56 Evaluated at bid price : 19.56 Bid-YTW : 5.17 % |

| GWO.PR.M | Deemed-Retractible | 114,826 | Nesbitt crossed 106,200 at 25.20 after hours as a contingent cross. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.20 Bid-YTW : 5.67 % |

| TRP.PR.E | FixedReset | 112,153 | Desjardins crossed 91,400 at 18.53. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 18.11 Evaluated at bid price : 18.11 Bid-YTW : 4.83 % |

| IGM.PR.B | Perpetual-Premium | 110,292 | Nesbitt crossed 108,400 at 25.28 after hours as a contingent cross. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 24.93 Evaluated at bid price : 25.28 Bid-YTW : 5.90 % |

| PWF.PR.G | Perpetual-Premium | 109,903 | Nesbitt crossed 100,200 at 25.34 after hours as a contingent cross. YTW SCENARIO Maturity Type : Call Maturity Date : 2016-01-06 Maturity Price : 25.00 Evaluated at bid price : 25.30 Bid-YTW : -1.41 % |

| BMO.PR.Z | Perpetual-Discount | 109,414 | Nesbitt crossed 102,700 at 23.85 after hours as a contingent cross. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 23.48 Evaluated at bid price : 23.80 Bid-YTW : 5.28 % |

| SLF.PR.B | Deemed-Retractible | 108,170 | Nesbitt crossed 99,500 at 21.21 after hours as a contingent cross. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.12 Bid-YTW : 7.13 % |

| MFC.PR.B | Deemed-Retractible | 104,967 | Nesbitt crossed 99,100 at 20.75 after hours as a contingent cross. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.72 Bid-YTW : 7.26 % |

| PWF.PR.K | Perpetual-Discount | 104,603 | Nesbitt crossed 101,100 at 21.87 after hours as a contingent cross. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-07 Maturity Price : 21.34 Evaluated at bid price : 21.61 Bid-YTW : 5.79 % |

| There were 68 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| VNR.PR.A | FixedReset | Quote: 18.01 – 19.00 Spot Rate : 0.9900 Average : 0.6495 YTW SCENARIO |

| ELF.PR.H | Perpetual-Discount | Quote: 22.03 – 23.00 Spot Rate : 0.9700 Average : 0.6410 YTW SCENARIO |

| HSE.PR.E | FixedReset | Quote: 20.15 – 20.98 Spot Rate : 0.8300 Average : 0.6028 YTW SCENARIO |

| TD.PF.E | FixedReset | Quote: 20.69 – 21.35 Spot Rate : 0.6600 Average : 0.4349 YTW SCENARIO |

| GWO.PR.M | Deemed-Retractible | Quote: 25.20 – 25.91 Spot Rate : 0.7100 Average : 0.5014 YTW SCENARIO |

| BAM.PR.E | Ratchet | Quote: 13.50 – 14.59 Spot Rate : 1.0900 Average : 0.8896 YTW SCENARIO |