CP Rail sold a century bond!

The railroad’s $900 million [USD] 100-year bond, sold with a coupon of 6.125 percent, shows how the once-troubled company has won over investor hearts and minds under new Chief Executive Officer Hunter Harrison, even as it embarks on a share-repurchase plan that would boost its debt load.

…

The century bond sale was the biggest by CP Rail since 1986. The company also issued $300 million in 20-year bonds with a 4.8 percent coupon. The average maturity on the Bank of America Merrill Lynch 15+ Year BBB US Corporate Index is 25 years with a yield of 5.5 percent, according to Bank of America Merrill Lynch data. The last century bond was issued by Brazil’s Petrobras Global Finance in June with a 6.85 percent coupon, according to data compiled by Bloomberg. Calgary-based Enbridge Inc., a pipeline operator, issued C$100 million ($76 million) of century bonds in Canada in 2012.

BMO has announced a major acquisition:

Bank of Montreal, Canada’s fourth-largest lender, agreed to buy General Electric Co.’s transportation finance business in the U.S. and Canada.

The unit had net earning assets of about C$11.5 billion ($8.7 billion) as of June 30, the Toronto-based bank said Thursday in a statement that didn’t disclose terms. The GE unit’s management team and about 600 employees will join Bank of Montreal, according to a presentation on the bank’s website.

Bank of Montreal’s agreement is the latest in a U.S. expansion that began in 1984 with its purchase of Chicago-based Harris Bank. The lender’s last major U.S. deal was its July 2011 takeover of Milwaukee-based Marshall & Ilsley Corp., which doubled deposits and branches and strengthened its commercial lending focus across the U.S. Midwest.

The relationship between ETFs, funds and crisis liquidity has been a hot issue. Barclays weighs in with some musings on ‘first-mover’ advantage:

Illiquidity in corporate bonds would in theory spell bad news for bond funds that promise investors the ability to immediately get out of their positions. The concern here is that once investors get a whiff of an impending mass selloff in bonds, they could potentially rush for the exits to try to get ahead of it.

With liquidity already low, that could put massive pressure on debt prices. Those who manage to squeeze through the keyhole first get rewarded for their speed but end up exacerbating this downward spiral. The slowest investors, meanwhile, get left with a portfolio of bonds that’s potentially much reduced in price.

By how much, you ask? Barclays estimates about 2 percent for funds that hold junk-rated corporate debt (boldface ours):

Mutual fund investors are, thus, faced with a first mover’s advantage to redeem in large selloff days because of a combination of inflated pricing and potential rebalancing costs. The magnitude of this advantage can be very meaningful economically. Assuming a 10 percent market shock leads to 10 percent outflows, we estimate that the first mover advantage is as much as 1.78 percent, or 1.61 percent from [net asset value] inflation and 0.17 percent from rebalancing costs.The benefit to early redeemers is effectively a tax on investors who remain invested through big downturns and ironically encourages demanding more liquidity.

They suggest a ‘scaled exit fee’:

“An “exit fee” that charges investors to withdraw their money from bond funds could arguably help slow theoretical outflows. (There is, of course, a converse argument that says such a fee would merely exacerbate the rush to the exit.) Barclays argues for a more refined approach that involves scaled fees:

Redemption fees are relatively straightforward and could be set such that they exactly neutralize the advantage of redeeming first in a down market. In our worst-case scenario, a redemption fee on the order of 2.0% would do the trick. That said, redemption fees are a somewhat blunt instrument. They penalize anyone withdrawing funds equally, regardless of how much liquidity the investor is demanding. Indeed, penalizing every investor based on a worst-case scenario may not be necessary. We believe a more nuanced approach would be to enforce minimum redemption fees according to a settlement schedule, with the minimum fee declining to zero as the investor allows settlement time to increase.

We wonder what the bond fund managers would say.

Well, PrefBlog says that, as stated, the idea is moronic, a typical product of a trading house that knows all about trading and nothing about investing.

What price will the redemption be at? Say you’ve got a million bucks in the fund and give me thirty days notice that you want out. So, notice period be damned, the price you’ll get is the day of actual redemption, thirty days hence. So should I sell securities now to raise the cash? Then I’ve got cash in the fund, which is kind of not the point of a fund (although the concept of fund investment is being increasingly circumscribed by liquidity rules and policies, as discussed on June 12). And I have to hold that cash in the fund for thirty days, reducing my duration and watching the market go up (because it always goes up in situations like this). So, nope, I’m not going to do it. I’m going to sell when I can get prices that will reasonably approximate the prices I use for determining the redemption value, which is to say, maybe half an hour prior to the close on the redemption date. So thirty day’s notice hasn’t done me a lot of good, has it?

The idea can be rescued by paying a blended price. Never mind “thirty day’s” notice, give me “twenty trading day’s” notice and agreed to get paid a blended price comprised of the NAV at the end of every equally weighted trading day. Then I can confidently sell 5% of your redemption value every day without screwing my other clients. There could be problems with this; if, for instance, a very large fund was to have a commitment to sell $10-million in preferreds for cash every day for the next twenty and this information becomes public … well, there won’t be much buying interest from other players for the next 15 trading days! So that’s got to be top-secret information … and in this business, ain’t nuthin’ top-secret.

A battle is brewing in the States over the right to bear screwdrivers:

Apple doesn’t publish repair manuals or sell parts to customers, and its warranty doesn’t apply if unauthorized repair damages its device. Samsung wouldn’t say why it doesn’t share repair information, though it makes some parts available to shops. Even John Deere gives only approved technicians access to the embedded software that controls systems in its machines. The manufacturers argue these limitations keep products working safely, and that copyright law lets them protect their intellectual property so it isn’t pirated.

“Bulls–t,” says Gay Gordon-Byrne, executive director of the Digital Right to Repair Coalition, based in North Haledon, N.J. “Repair is a profit center for a lot of companies, and sometimes it is more profitable than selling hardware.” Maintaining “repair monopolies,” she says, pushes up costs and makes customers more likely to simply junk old models for new ones. Apple charges $79 to replace an iPhone 4 battery. Repair website IFixit charges $20 for a battery and DIY kit for the same job.

Gordon-Byrne’s organization and advocates such as the Electronic Frontier Foundation are supporting bills introduced this year in Massachusetts, Minnesota, and New York that would require manufacturers to sell parts and provide manuals to hardware owners and independent repair shops. Separate efforts in Congress would amend the federal Digital Millennium Copyright Act by giving explicit permission for consumers to circumvent a manufacturer’s digital lock on its software for a lawful reason such as repair.

Times are tough in the dairy business:

Record prices last year primed farmers to bolster output in the U.S., where milk production in 2015 will reach 208.7 billion pounds—the fifth consecutive record-setting year. In April the EU, seeking to liberalize trade, removed quotas that had been in place for the past 30 years, leading to increased production from Ireland, the Netherlands, and the U.K. China is producing more milk thanks to investments such as a $140 million, 20,000-cow facility that China Modern Dairy Holdings, partly owned by private equity firm KKR, unveiled in 2013. The Chinese are also consuming stockpiled milk powder and importing less. Global milk supply grew 3.7 percent last year, almost triple the growth rate of 2013, the USDA says.

…

Overcapacity “is a long-term problem that a short-term fix won’t address,” says Robbie Turner, head of European markets at Rice Dairy International.

Nope, the only fix is to squeeze out the high-cost producers during times of oversupply, giving low-cost producers room to expand during times of undersupply. It’s called “economics”, though some prefer “competition”.

It was a mixed day in the Canadian preferred share market, with PerpetualDiscounts gaining 1bp, FixedResets off 9bp and DeemedRetractibles up 2bp. FixedResets comprised the entire good side of the Performance Highlights table. Volume was very, awfully, miserably, disgustingly, quietly low.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

Here’s TRP:

Click for Big

Click for BigTRP.PR.E, which resets 2019-10-30 at +235, is bid at 20.15 to be $0.94 rich, while TRP.PR.C, resetting 2016-1-30 at +164, is $1.21 cheap at its bid price of 13.15.

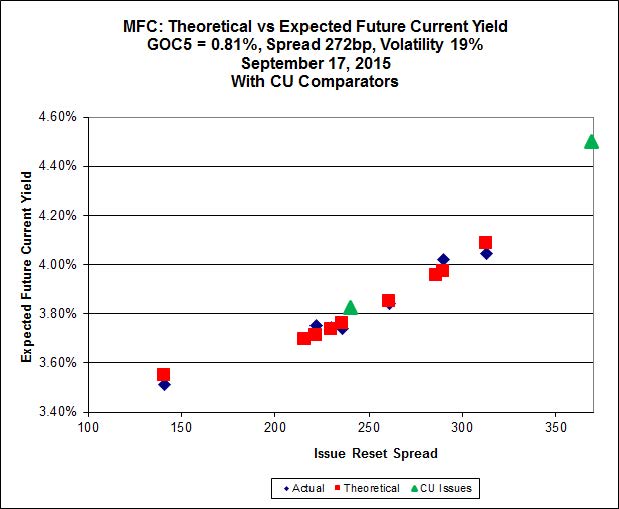

Click for Big

Click for BigAnother good fit today for MFC, with Implied Volatility falling a bit today.

Most expensive is MFC.PR.H, resetting at +313bp on 2017-3-19, bid at 24.26 to be 0.44 rich, while MFC.PR.G, resetting at +290bp on 2016-12-19, is bid at 22.76 to be 0.36 cheap.

Click for Big

Click for BigThe fit on the BAM issues continues to be horrible.

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 17.01 to be $1.41 cheap. BAM.PF.F, resetting at +286bp on 2019-9-30 is bid at 22.70 and appears to be $0.93 rich.

Click for Big

Click for BigFTS.PR.K, with a spread of +205bp, and bid at 19.73, looks $0.45 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 19.13 and is $0.62 cheap.

Click for Big

Click for BigInvestment-grade pairs predict an average three-month bill yield over the next five-odd years of -1.17%, with no outliers. Note that the distribution is bimodal, with NVCC non-compliant bank issues averaging -1.32% and the unregulated issues averaging -0.94%. There are two junk outliers below -2.00% and one above 0.00%.

Click for Big

Click for BigShall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

HIMIPref™ Preferred Indices

These values reflect the December 2008 revision of the HIMIPref™ Indices

Values are provisional and are finalized monthly |

| Index |

Mean

Current

Yield

(at bid) |

Median

YTW |

Median

Average

Trading

Value |

Median

Mod Dur

(YTW) |

Issues |

Day’s Perf. |

Index Value |

| Ratchet |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

-1.8657 % |

1,633.5 |

| FixedFloater |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

-1.8657 % |

2,856.2 |

| Floater |

4.49 % |

4.57 % |

58,488 |

16.20 |

3 |

-1.8657 % |

1,736.6 |

| OpRet |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.3523 % |

2,782.8 |

| SplitShare |

4.62 % |

4.92 % |

63,980 |

3.08 |

3 |

0.3523 % |

3,261.3 |

| Interest-Bearing |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.3523 % |

2,544.6 |

| Perpetual-Premium |

5.72 % |

2.89 % |

56,870 |

0.08 |

8 |

0.0693 % |

2,491.2 |

| Perpetual-Discount |

5.42 % |

5.50 % |

71,363 |

14.59 |

30 |

0.0129 % |

2,607.5 |

| FixedReset |

4.68 % |

4.12 % |

172,457 |

15.92 |

74 |

-0.0872 % |

2,170.9 |

| Deemed-Retractible |

5.14 % |

5.21 % |

94,479 |

5.38 |

33 |

0.0189 % |

2,585.4 |

| FloatingReset |

2.44 % |

3.89 % |

54,843 |

5.93 |

9 |

-0.2756 % |

2,171.0 |

| Performance Highlights |

| Issue |

Index |

Change |

Notes |

| TRP.PR.B |

FixedReset |

-2.35 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-10

Maturity Price : 12.47

Evaluated at bid price : 12.47

Bid-YTW : 4.18 % |

| BAM.PR.K |

Floater |

-2.23 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-10

Maturity Price : 10.50

Evaluated at bid price : 10.50

Bid-YTW : 4.57 % |

| HSE.PR.E |

FixedReset |

-2.11 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-10

Maturity Price : 21.88

Evaluated at bid price : 22.32

Bid-YTW : 4.90 % |

| TRP.PR.F |

FloatingReset |

-1.95 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-10

Maturity Price : 14.56

Evaluated at bid price : 14.56

Bid-YTW : 3.89 % |

| BAM.PR.B |

Floater |

-1.94 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-10

Maturity Price : 10.61

Evaluated at bid price : 10.61

Bid-YTW : 4.52 % |

| BAM.PR.R |

FixedReset |

-1.79 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-10

Maturity Price : 17.01

Evaluated at bid price : 17.01

Bid-YTW : 4.78 % |

| HSE.PR.C |

FixedReset |

-1.65 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-10

Maturity Price : 20.85

Evaluated at bid price : 20.85

Bid-YTW : 4.87 % |

| TD.PF.D |

FixedReset |

-1.47 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-10

Maturity Price : 22.50

Evaluated at bid price : 23.40

Bid-YTW : 3.79 % |

| MFC.PR.F |

FixedReset |

-1.42 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 16.02

Bid-YTW : 7.84 % |

| BAM.PR.C |

Floater |

-1.42 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-10

Maturity Price : 10.45

Evaluated at bid price : 10.45

Bid-YTW : 4.59 % |

| NA.PR.S |

FixedReset |

-1.39 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-10

Maturity Price : 21.70

Evaluated at bid price : 22.00

Bid-YTW : 3.81 % |

| TD.PF.B |

FixedReset |

-1.19 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-10

Maturity Price : 21.30

Evaluated at bid price : 21.59

Bid-YTW : 3.72 % |

| CM.PR.Q |

FixedReset |

-1.05 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-10

Maturity Price : 22.52

Evaluated at bid price : 23.45

Bid-YTW : 3.79 % |

| TRP.PR.C |

FixedReset |

-1.05 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-10

Maturity Price : 13.15

Evaluated at bid price : 13.15

Bid-YTW : 4.53 % |

| HSE.PR.A |

FixedReset |

-1.05 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-10

Maturity Price : 14.15

Evaluated at bid price : 14.15

Bid-YTW : 4.56 % |

| TRP.PR.A |

FixedReset |

-1.03 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-10

Maturity Price : 17.22

Evaluated at bid price : 17.22

Bid-YTW : 4.12 % |

| GWO.PR.I |

Deemed-Retractible |

-1.01 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.58

Bid-YTW : 6.47 % |

| RY.PR.Z |

FixedReset |

-1.01 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-10

Maturity Price : 21.29

Evaluated at bid price : 21.58

Bid-YTW : 3.68 % |

| MFC.PR.H |

FixedReset |

1.08 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 24.27

Bid-YTW : 4.42 % |

| TRP.PR.E |

FixedReset |

1.10 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-10

Maturity Price : 20.15

Evaluated at bid price : 20.15

Bid-YTW : 4.23 % |

| FTS.PR.H |

FixedReset |

1.11 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-10

Maturity Price : 15.52

Evaluated at bid price : 15.52

Bid-YTW : 3.71 % |

| MFC.PR.K |

FixedReset |

1.15 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.15

Bid-YTW : 6.04 % |

| SLF.PR.H |

FixedReset |

1.21 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 19.25

Bid-YTW : 6.34 % |

| BAM.PR.X |

FixedReset |

1.26 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-10

Maturity Price : 15.25

Evaluated at bid price : 15.25

Bid-YTW : 4.66 % |

| TRP.PR.G |

FixedReset |

1.72 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-10

Maturity Price : 21.56

Evaluated at bid price : 21.90

Bid-YTW : 4.29 % |

| FTS.PR.K |

FixedReset |

2.39 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-10

Maturity Price : 19.73

Evaluated at bid price : 19.73

Bid-YTW : 3.86 % |

| FTS.PR.G |

FixedReset |

2.46 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-10

Maturity Price : 19.13

Evaluated at bid price : 19.13

Bid-YTW : 4.02 % |

| IFC.PR.A |

FixedReset |

2.54 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 17.35

Bid-YTW : 7.87 % |

| Volume Highlights |

| Issue |

Index |

Shares

Traded |

Notes |

| FTS.PR.M |

FixedReset |

40,520 |

RBC crossed 10,000 at 21.68; Scotia crossed 20,200 at 21.66.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-10

Maturity Price : 21.35

Evaluated at bid price : 21.65

Bid-YTW : 3.97 % |

| BAM.PR.R |

FixedReset |

20,486 |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-10

Maturity Price : 17.01

Evaluated at bid price : 17.01

Bid-YTW : 4.78 % |

| TRP.PR.D |

FixedReset |

16,684 |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-10

Maturity Price : 19.57

Evaluated at bid price : 19.57

Bid-YTW : 4.29 % |

| RY.PR.Z |

FixedReset |

16,140 |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-10

Maturity Price : 21.29

Evaluated at bid price : 21.58

Bid-YTW : 3.68 % |

| BAM.PR.B |

Floater |

16,089 |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-10

Maturity Price : 10.61

Evaluated at bid price : 10.61

Bid-YTW : 4.52 % |

| BAM.PF.D |

Perpetual-Discount |

15,985 |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-10

Maturity Price : 21.86

Evaluated at bid price : 22.15

Bid-YTW : 5.63 % |

| There were 6 other index-included issues trading in excess of 10,000 shares. |

| Wide Spread Highlights |

| Issue |

Index |

Quote Data and Yield Notes |

| IFC.PR.C |

FixedReset |

Quote: 20.75 – 21.60

Spot Rate : 0.8500

Average : 0.6733

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.75

Bid-YTW : 6.07 % |

| TRP.PR.F |

FloatingReset |

Quote: 14.56 – 15.24

Spot Rate : 0.6800

Average : 0.5079

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-10

Maturity Price : 14.56

Evaluated at bid price : 14.56

Bid-YTW : 3.89 % |

| ELF.PR.F |

Perpetual-Discount |

Quote: 23.02 – 23.51

Spot Rate : 0.4900

Average : 0.3381

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-10

Maturity Price : 22.73

Evaluated at bid price : 23.02

Bid-YTW : 5.84 % |

| MFC.PR.M |

FixedReset |

Quote: 21.01 – 21.49

Spot Rate : 0.4800

Average : 0.3450

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.01

Bid-YTW : 5.76 % |

| GWO.PR.H |

Deemed-Retractible |

Quote: 22.45 – 22.95

Spot Rate : 0.5000

Average : 0.3764

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.45

Bid-YTW : 6.31 % |

| MFC.PR.N |

FixedReset |

Quote: 20.63 – 21.45

Spot Rate : 0.8200

Average : 0.6975

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.63

Bid-YTW : 5.93 % |