Remember all that gloomy stuff posted for the past week? Well, don’t. We’re rich!

What you need to know about Thursday’s [US] economic data:

GROSS DOMESTIC PRODUCT (2Q REVISED)

- •Climbed at a revised 3.7 percent annualized rate, exceeding all forecasts in a Bloomberg survey and up from an initial estimate of 2.3 percent

- •All four components — consumer spending, business investment, trade and government outlays — contributed more to growth than first estimated

- •Inventories showed biggest back-to-back quarterly increases on record

- •Gross domestic income grew at a 0.6 percent pace in second quarter

…

JOBLESS CLAIMS (WEEK ENDED AUG. 22)

- •Applications fell by 6,000 to 271,000 with Michigan and Kansas posting biggest drops

- •Claims hovering close to mid-July level of 255,000 that was fewest since 1973

Just ignore the inevitable carpers:

The federal government today released two very different estimates of the U.S. economy’s growth rate in the second quarter. The one that got all the attention was the robust 3.7 percent annual rate of increase in gross domestic product. Not many people noticed that gross domestic income increased at an annual rate of just 0.6 percent.

That’s a big discrepancy for two numbers that should theoretically be the same, since they’re two ways of measuring the same thing: the size of the economy. If you believe the GDP number, you’re happy. If you believe the GDI number, you’re thinking the U.S. is skating close to a recession.

The Bureau of Economic Analysis always gives more prominence to the GDP number in its quarterly press release. But today, for the second time in a quarterly report, it released an average of GDP and GDI growth rates. That average came in at 2.1 percent after rounding—and in this case, that’s probably closer to the truth than either number alone.

So oil popped:

Oil jumped the most in more than six years, caught up in a relief rally that swept the globe as the U.S. economy grew more than predicted.

West Texas Intermediate futures rose 10 percent, the biggest gain since March 2009. U.S. gross domestic product grew at a 3.7 percent annualized rate in the second quarter, exceeding all estimates of economists surveyed by Bloomberg. The Standard & Poor’s 500 Index headed for its biggest two-day gain since 2009 as Chinese shares snapped a five-day losing streak.

Prices extended gains after Royal Dutch Shell Plc issued a force majeure on Bonny Light exports from Nigeria as it worked to repair two crude pipelines shut because of thefts and a leak.

And everybody was happy, happy, happy:

A relief rally swept around the globe, with the Dow Jones Industrial Average capping its biggest two-day gain since 2008 and Chinese shares snapping a five-day tumble. Oil jumped the most in more than six years after data showed the U.S. economy grew more than forecast in the second quarter.

American stocks briefly spiked lower in late afternoon trading, as the Standard & Poor’s 500 Index cut an advance of as much as 2.5 percent to less than 0.5 percent before reversing course and rallying again, indicating markets are still vulnerable to sudden swings.

Shares surged from Asia to the U.S. after the biggest advance in the S&P 500 in four years on Wednesday helped restore some appetite for riskier assets. The rally halted the selloff that’s engulfed markets since China devalued its currency on Aug. 11, an unexpected move that ignited concern that the slowdown in the world’s second largest economy may threaten global growth.

… except maybe bond investors:

Treasury notes fell for a third straight day on a report showing U.S. economic growth exceeded forecasts last quarter and as global stocks rallied.

…

The benchmark two-year yield rose two basis points, or 0.02 percentage point, to 0.69 percent as of 5 p.m. in New York, according to Bloomberg Bond Trader data. The 0.625 percent security due in August 2017 fell 1/32, or 31 cents per $1,000 face amount, to 99 7/8.The 30-year bond advanced, halting a three-day decline. The prospect of the Fed’s first interest-rate increase in nearly a decade damped expectations for inflation, and can erode longer-maturity bonds’ fixed payments.

…

Traders are pricing in a 53 percent chance of a Fed boost before the end of this year, up from 46 percent two days ago, assuming the benchmark will average 0.375 percent after the first rise.

Here’s a story a like for a lot of reasons. First, the little gal sticks it to the big boys. Second, it’s an illustration of a trend I predict towards customization and personal services (since “things” are so easy to make in a mechanical way nowadays). And, of course, pictures of women in underwear, which is always pleasant. Indie lingerie in Canada:

Uncomfortable watching intimates being developed cheaply and in a rush, and fatigued by taking direction from “men talking about what’s really hot on a woman and what women want… and then [asking me] to cut the ass out of a panty,” Russell broke out on her own in 2010. After careful planning and with strong connections in her pocket, she decided to make underwear on her own terms – and to make it better.

As it turns out, Russell is one of several young indie entrepreneurs in Canada who are applying a slow-living, small-batch ethic to underwear and, in the process, overturning established ideas about what lingerie is, how it should fit and who it’s really for.

Alesha Frederickson started March & August Underthings on January 1, 2014, with a resolution to shift the panty paradigm. She believed the lingerie available in her hometown, Winnipeg, left a lot to be desired: It was off-the-rack, unflattering and there wasn’t much variety between babydoll-style teen-focused items and the offerings from fast-fashion brands. Both, according to Frederickson, were “designed to be like a present to unwrap, like a gift to the person who was viewing, not wearing, it.”

…

In 2011, [former La Senza technical designer Sofia Sokoloff] started Sokoloff Lingerie for the middle market. She was 23 years old at the time and studying industrial management at the École supérieur de mode de Montréal. In the past four years, her brand has grown quickly: She now has two seamstresses and her own production floor that regularly makes more than 1,000 units per month. She went from two points of sale in 2011 to nearly 30 today, and most recently found a distributor in Dubai to sell her collections come fall.

…

Sokoloff was recently recognized as an industry leader when she was named the Les Offices jeunesse internationaux du Québec 2015 prizewinner – a provincial award for young entrepreneurs who are helping to make a name for Quebec on the international market. She also represented Canada earlier this month at the Curve Expo lingerie and swimwear showcase in New York City.

It was a fine day for the Canadian preferred share market, with PerpetualDiscounts up 41bp, FixedResets winning 63bp and DeemedRetractibles gaining 21bp. Yet another very lengthy Performance Highlights table is dominated by FixedReset winners with ENB issues at the top of the pile. Volume was average.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

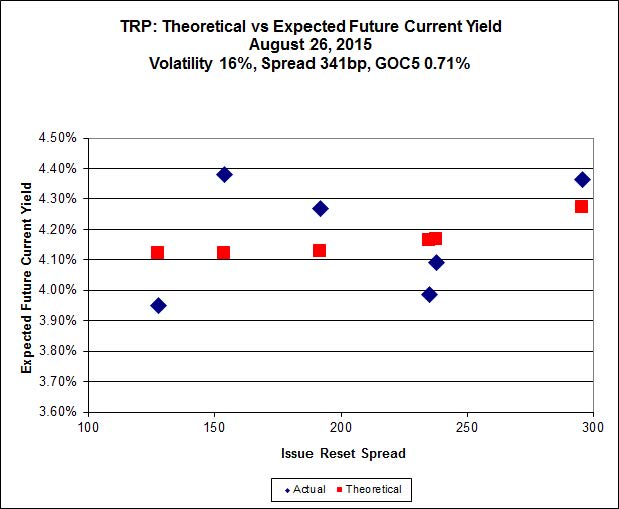

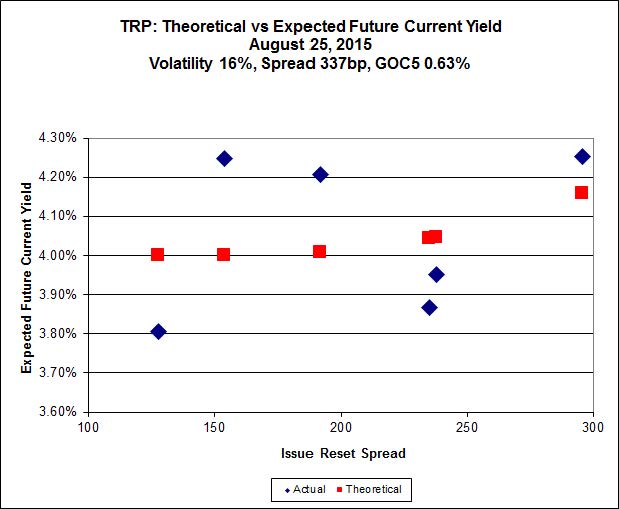

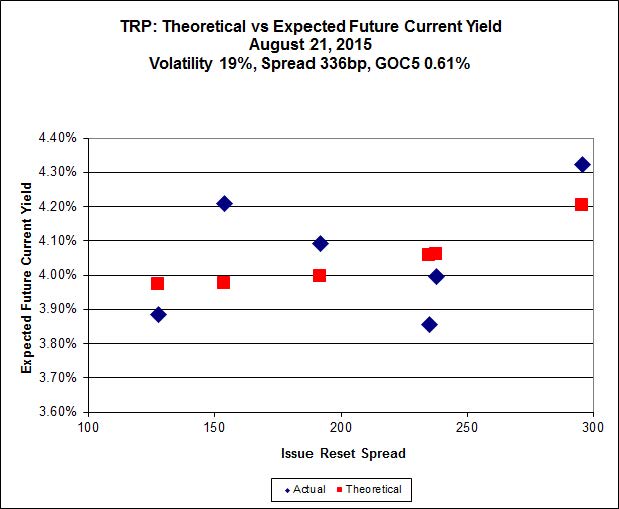

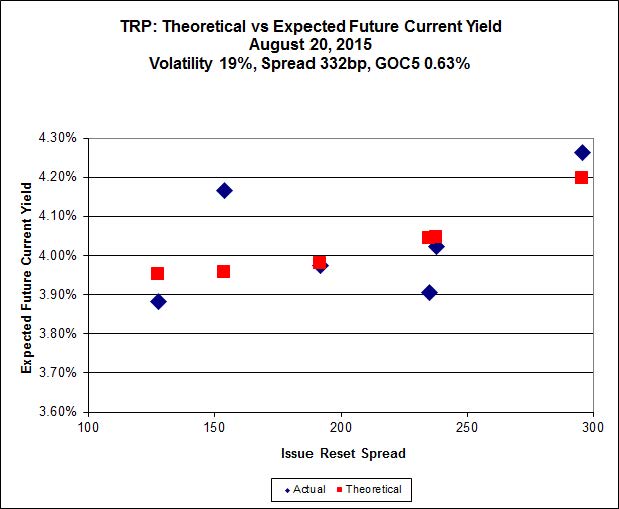

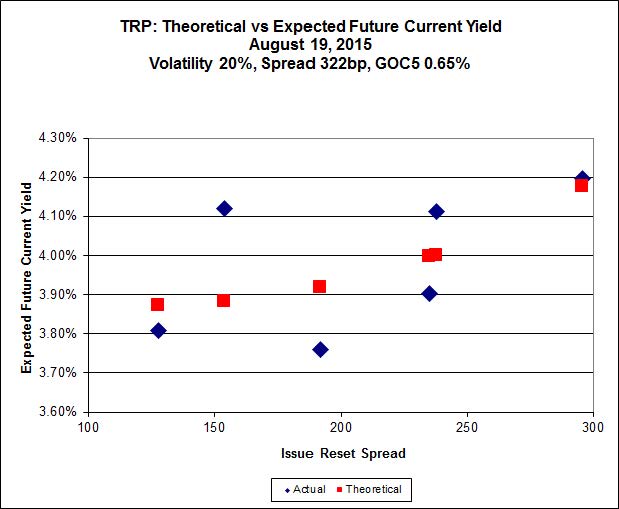

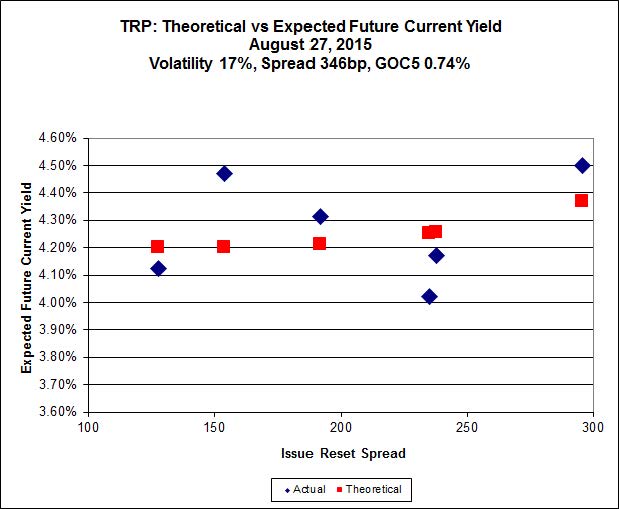

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 19.21 to be $1.04 rich, while TRP.PR.C, resetting 2016-1-30 at +164, is $0.82 cheap at its bid price of 12.75.

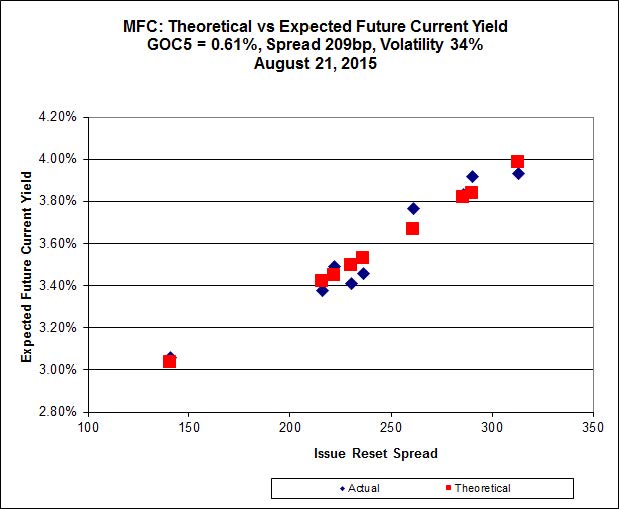

Click for Big

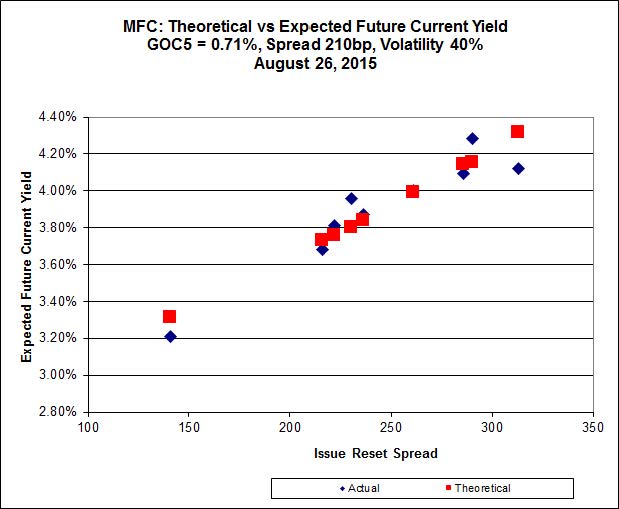

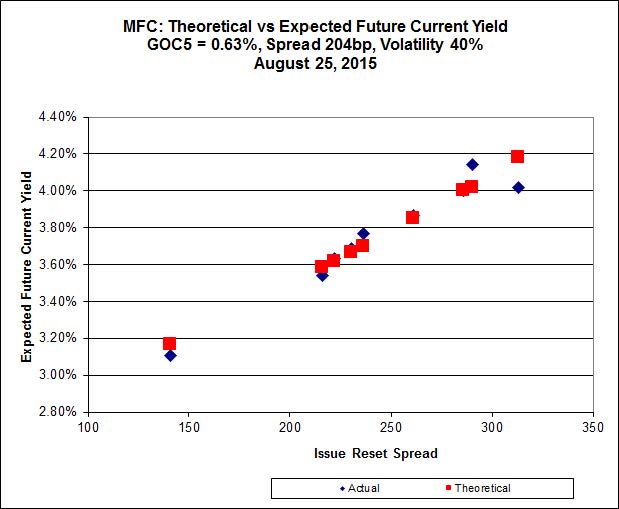

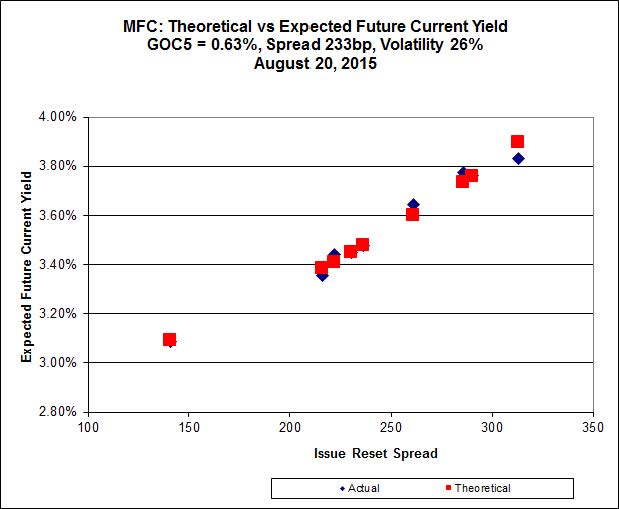

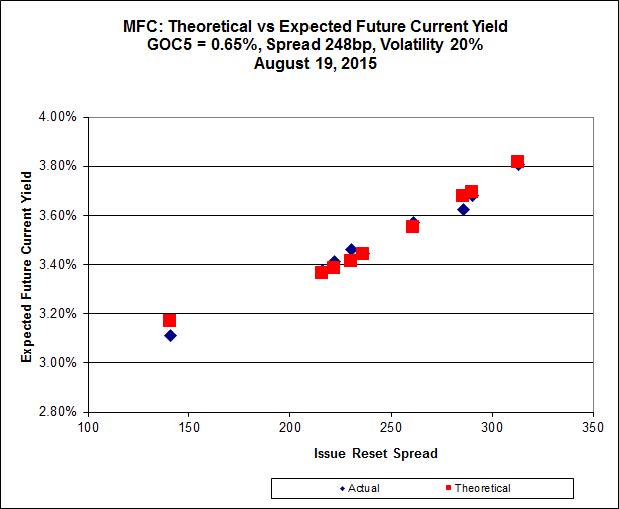

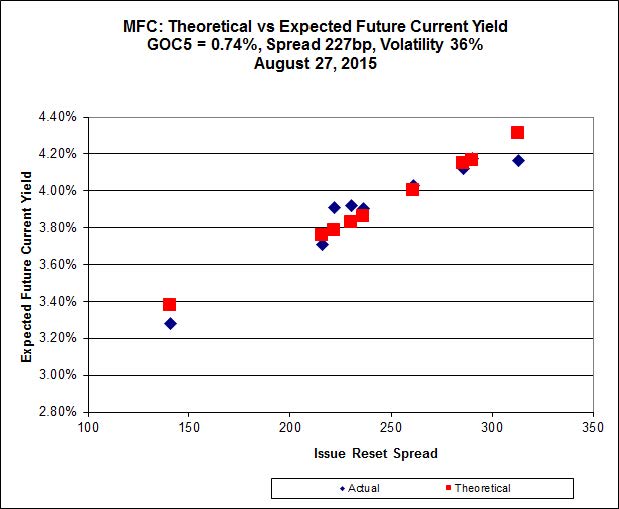

Another good fit today for MFC, with Implied Volatility dropping a bit today.

Most expensive is MFC.PR.H, resetting at +313bp on 2017-3-19, bid at 23.22 to be 0.78 rich, while MFC.PR.K, resetting at +222bp on 2018-9-19, bid at 18.92 to be 0.65 cheap.

Click for Big

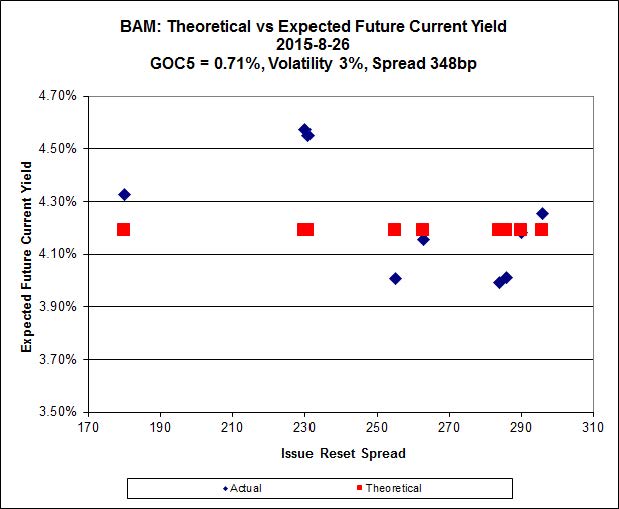

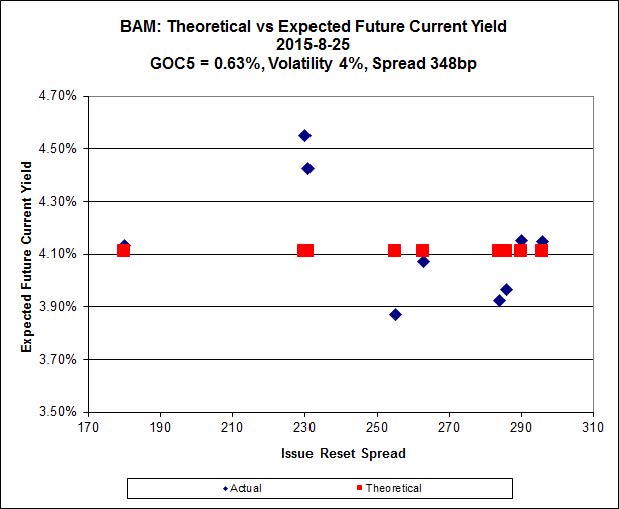

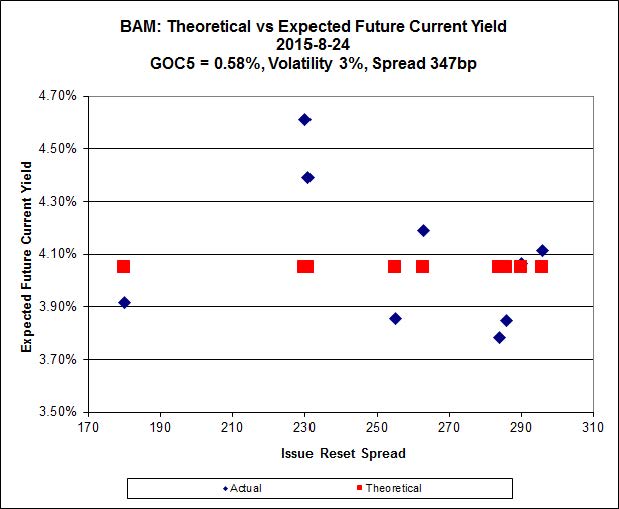

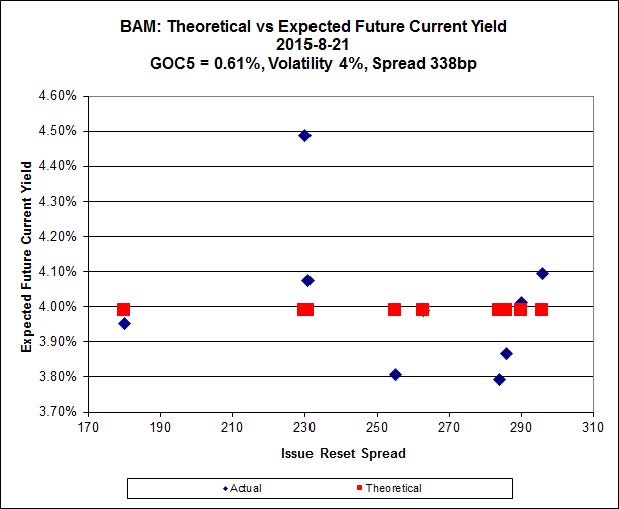

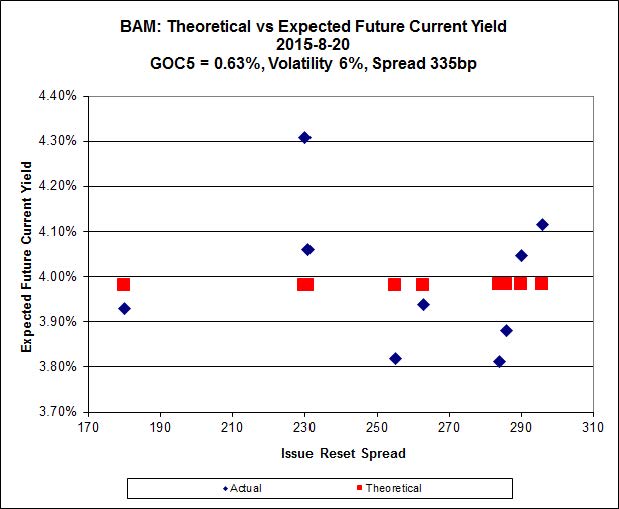

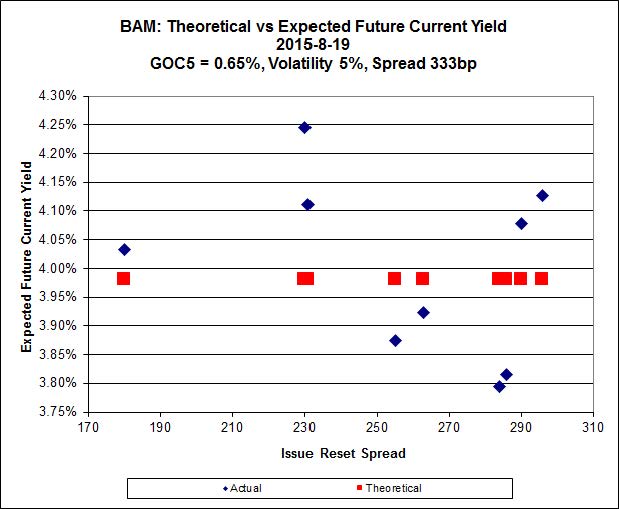

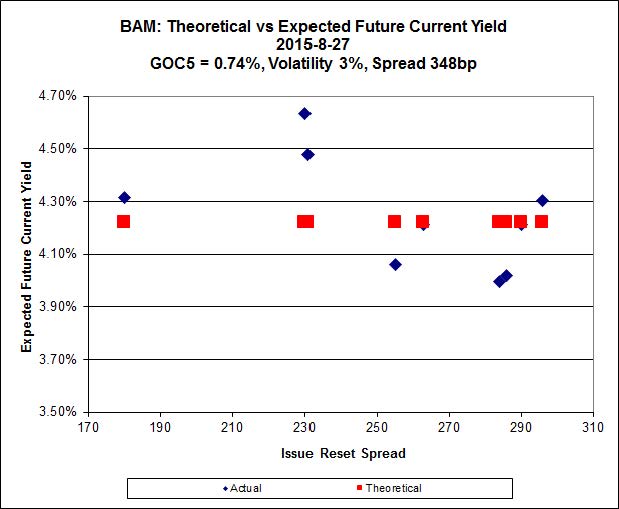

The fit on the BAM issues continues to be horrible.

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 16.40 to be $1.61 cheap. BAM.PF.G, resetting at +284bp on 2020-6-30 is bid at 22.41 and appears to be $1.20 rich.

Click for Big

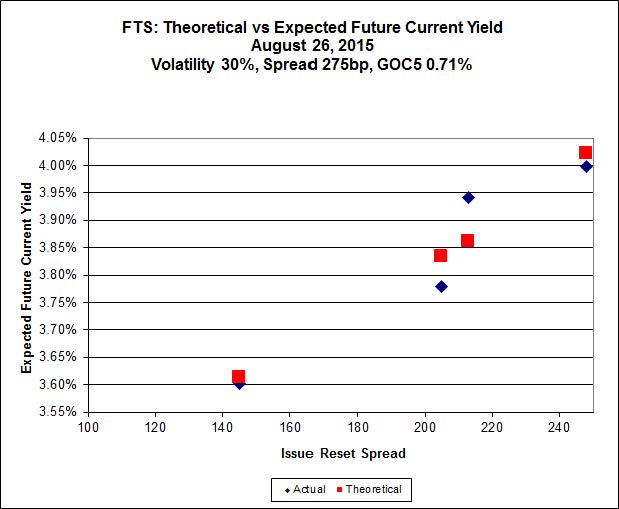

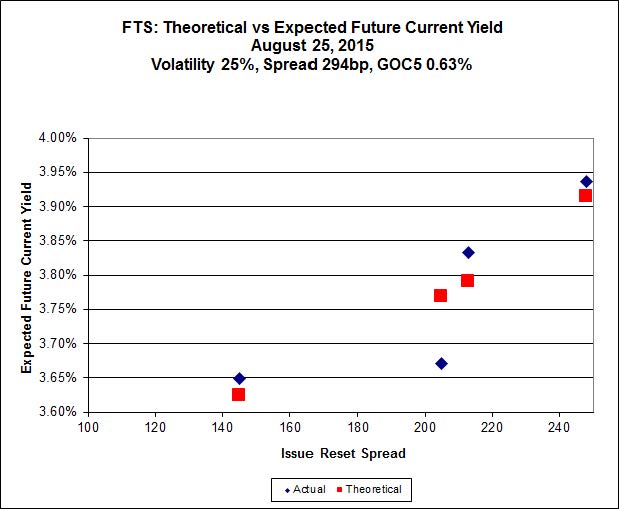

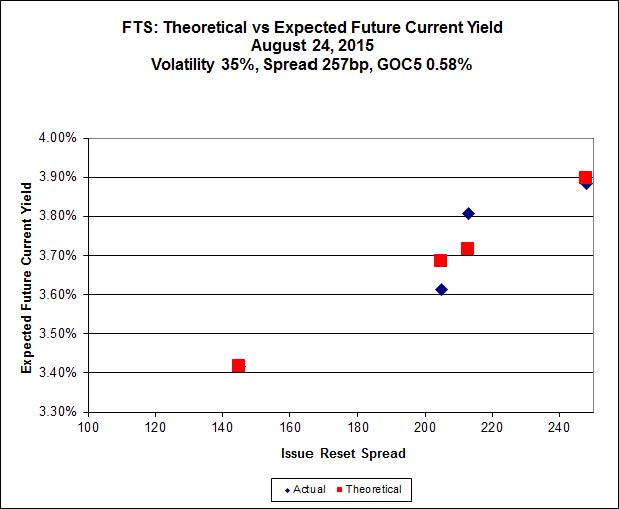

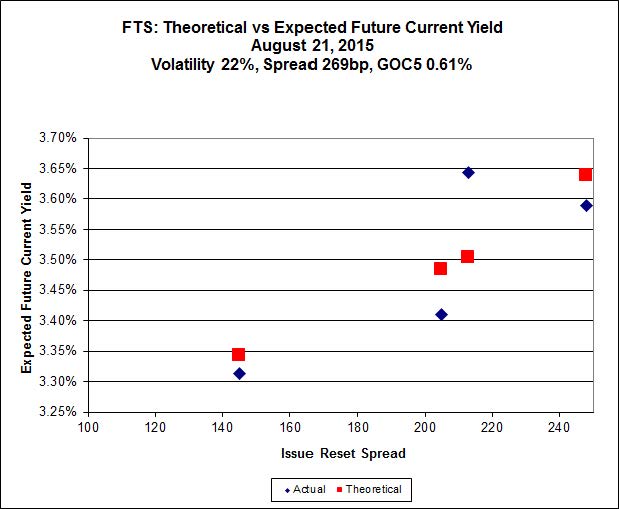

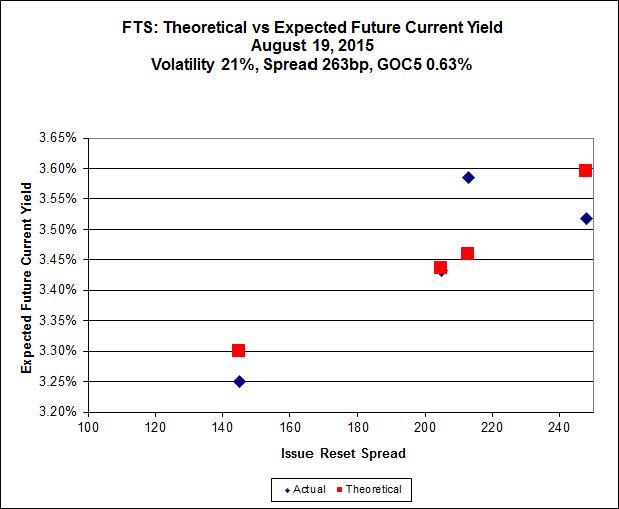

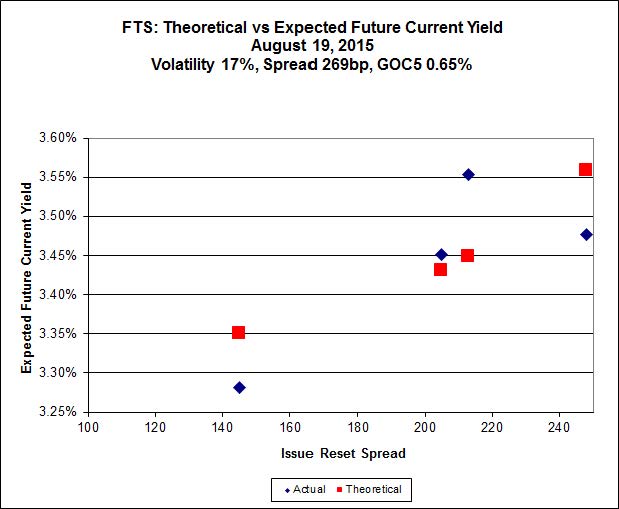

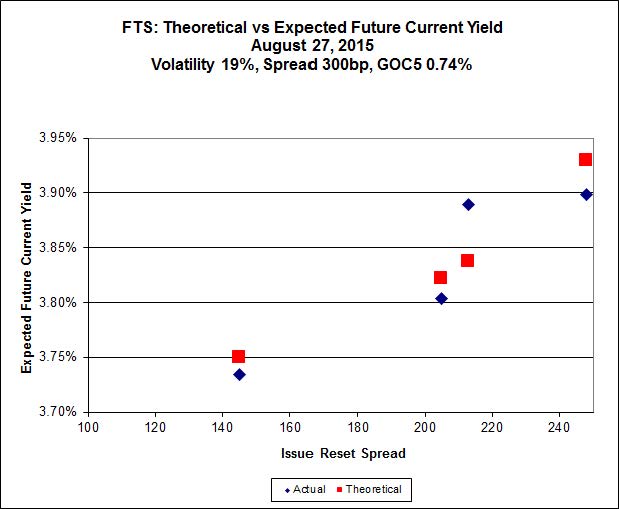

Implied Volatility fell substantially today but remains unreasonably high.

FTS.PR.M, with a spread of +248bp, and bid at 20.65, looks $0.16 expensive and resets 2019-12-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 18.45 and is $0.25 cheap.

Click for Big

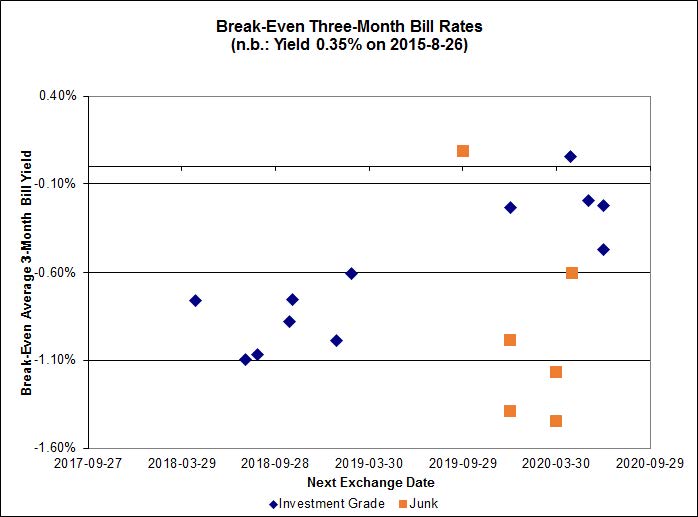

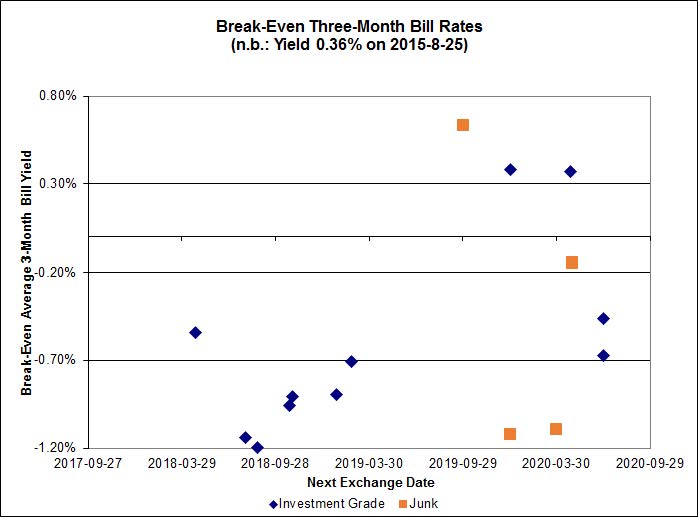

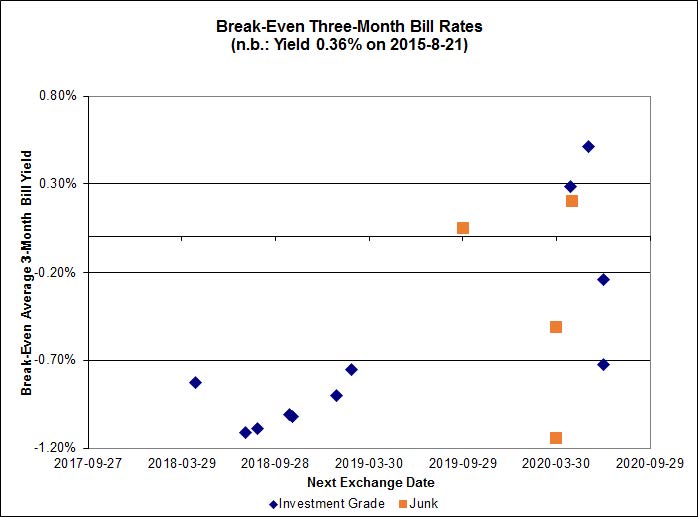

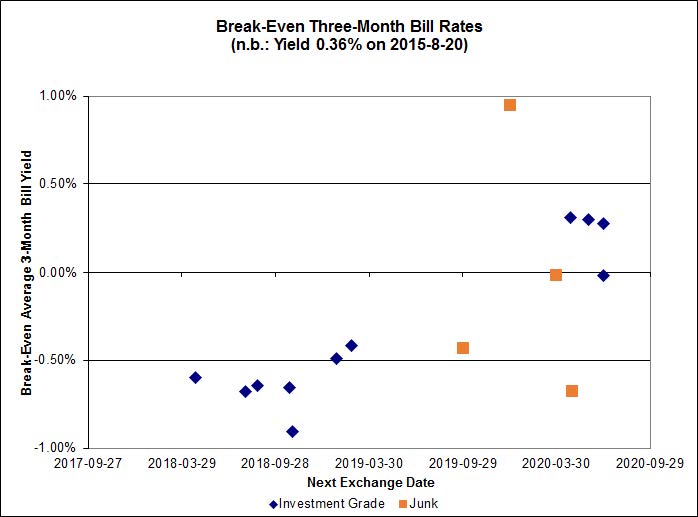

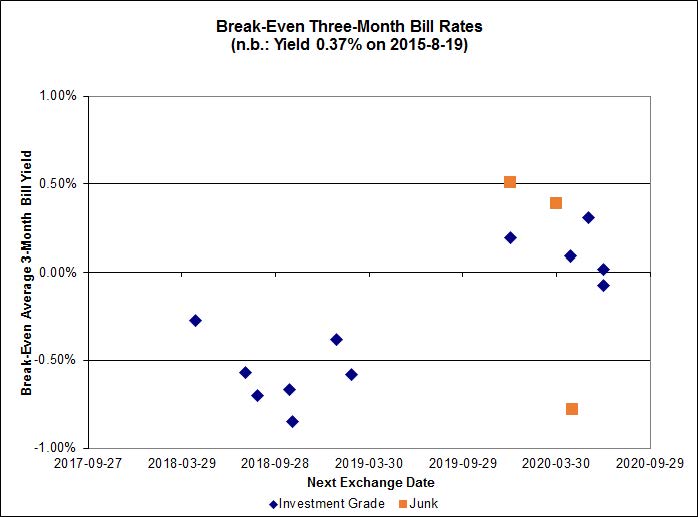

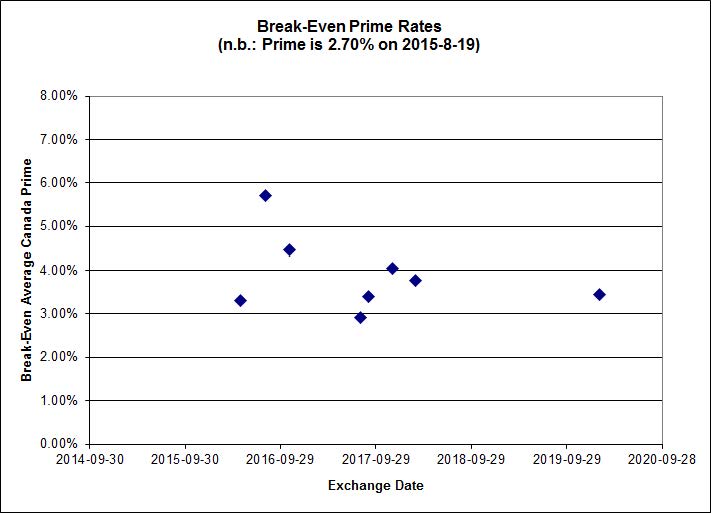

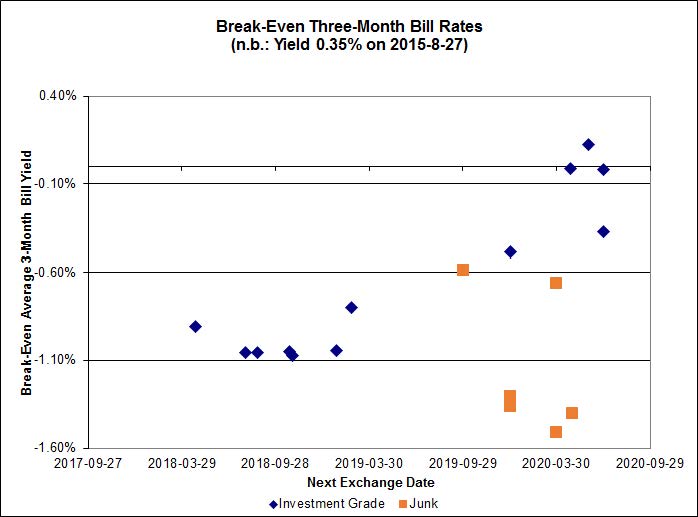

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.65%, with no outliers. Note that the distribution is bimodal, with NVCC non-compliant bank issues averaging -1.00% and the unregulated issues averaging -0.15%. There are no junk outliers.

Click for Big

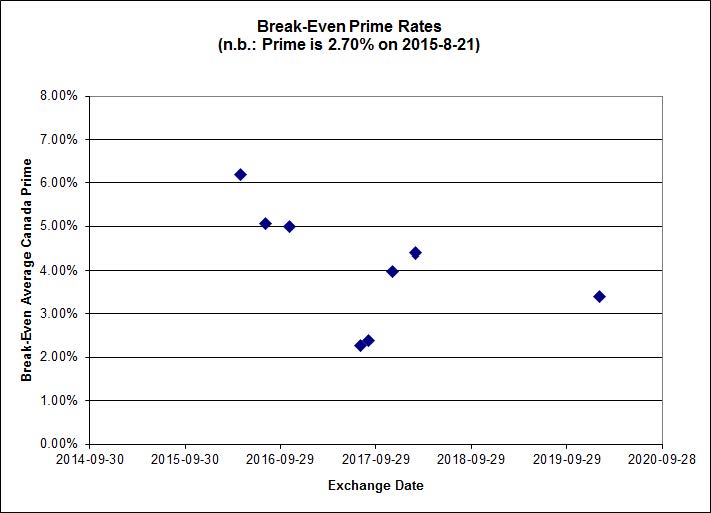

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 1.5822 % | 1,628.4 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 1.5822 % | 2,847.1 |

| Floater | 4.51 % | 4.58 % | 58,478 | 16.20 | 3 | 1.5822 % | 1,731.1 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.3269 % | 2,767.8 |

| SplitShare | 4.65 % | 5.04 % | 57,880 | 3.12 | 3 | 0.3269 % | 3,243.7 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.3269 % | 2,530.8 |

| Perpetual-Premium | 5.73 % | 5.56 % | 63,094 | 2.03 | 9 | 0.2436 % | 2,482.3 |

| Perpetual-Discount | 5.51 % | 5.57 % | 78,914 | 14.55 | 29 | 0.4087 % | 2,564.2 |

| FixedReset | 5.02 % | 4.30 % | 197,369 | 15.62 | 87 | 0.6251 % | 2,105.8 |

| Deemed-Retractible | 5.18 % | 5.27 % | 104,080 | 5.56 | 34 | 0.2125 % | 2,552.9 |

| FloatingReset | 2.39 % | 3.61 % | 47,921 | 5.96 | 9 | -0.2059 % | 2,177.4 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| HSE.PR.E | FixedReset | -3.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-27 Maturity Price : 21.34 Evaluated at bid price : 21.63 Bid-YTW : 4.99 % |

| TRP.PR.G | FixedReset | -2.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-27 Maturity Price : 20.55 Evaluated at bid price : 20.55 Bid-YTW : 4.44 % |

| FTS.PR.H | FixedReset | -2.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-27 Maturity Price : 14.66 Evaluated at bid price : 14.66 Bid-YTW : 3.70 % |

| TRP.PR.B | FixedReset | -1.71 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-27 Maturity Price : 12.25 Evaluated at bid price : 12.25 Bid-YTW : 3.98 % |

| IAG.PR.A | Deemed-Retractible | -1.64 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.50 Bid-YTW : 6.59 % |

| MFC.PR.K | FixedReset | -1.51 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.92 Bid-YTW : 6.71 % |

| PWF.PR.P | FixedReset | -1.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-27 Maturity Price : 15.57 Evaluated at bid price : 15.57 Bid-YTW : 3.63 % |

| BMO.PR.Q | FixedReset | -1.11 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.41 Bid-YTW : 4.73 % |

| TRP.PR.D | FixedReset | -1.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-27 Maturity Price : 18.70 Evaluated at bid price : 18.70 Bid-YTW : 4.30 % |

| GWO.PR.N | FixedReset | 1.00 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.15 Bid-YTW : 8.20 % |

| TD.PR.Y | FixedReset | 1.05 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.96 Bid-YTW : 3.02 % |

| W.PR.H | Perpetual-Discount | 1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-27 Maturity Price : 23.63 Evaluated at bid price : 23.90 Bid-YTW : 5.83 % |

| MFC.PR.B | Deemed-Retractible | 1.09 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.35 Bid-YTW : 6.77 % |

| PWF.PR.K | Perpetual-Discount | 1.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-27 Maturity Price : 22.39 Evaluated at bid price : 22.65 Bid-YTW : 5.51 % |

| PVS.PR.D | SplitShare | 1.17 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2021-10-08 Maturity Price : 25.00 Evaluated at bid price : 24.30 Bid-YTW : 5.04 % |

| W.PR.J | Perpetual-Discount | 1.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-27 Maturity Price : 23.63 Evaluated at bid price : 23.90 Bid-YTW : 5.94 % |

| POW.PR.B | Perpetual-Discount | 1.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-27 Maturity Price : 23.54 Evaluated at bid price : 23.81 Bid-YTW : 5.69 % |

| ELF.PR.F | Perpetual-Discount | 1.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-27 Maturity Price : 22.66 Evaluated at bid price : 22.90 Bid-YTW : 5.86 % |

| CM.PR.Q | FixedReset | 1.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-27 Maturity Price : 22.04 Evaluated at bid price : 22.60 Bid-YTW : 3.81 % |

| PWF.PR.T | FixedReset | 1.36 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-27 Maturity Price : 22.42 Evaluated at bid price : 23.05 Bid-YTW : 3.43 % |

| TRP.PR.A | FixedReset | 1.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-27 Maturity Price : 15.42 Evaluated at bid price : 15.42 Bid-YTW : 4.38 % |

| BAM.PR.X | FixedReset | 1.52 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-27 Maturity Price : 14.72 Evaluated at bid price : 14.72 Bid-YTW : 4.55 % |

| NA.PR.S | FixedReset | 1.53 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-27 Maturity Price : 20.61 Evaluated at bid price : 20.61 Bid-YTW : 3.92 % |

| RY.PR.M | FixedReset | 1.61 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-27 Maturity Price : 21.73 Evaluated at bid price : 22.15 Bid-YTW : 3.74 % |

| ELF.PR.H | Perpetual-Discount | 1.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-27 Maturity Price : 23.78 Evaluated at bid price : 24.25 Bid-YTW : 5.73 % |

| PWF.PR.F | Perpetual-Discount | 1.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-27 Maturity Price : 24.00 Evaluated at bid price : 24.25 Bid-YTW : 5.46 % |

| ENB.PR.B | FixedReset | 1.71 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-27 Maturity Price : 14.27 Evaluated at bid price : 14.27 Bid-YTW : 5.48 % |

| HSE.PR.C | FixedReset | 2.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-27 Maturity Price : 21.13 Evaluated at bid price : 21.13 Bid-YTW : 4.73 % |

| MFC.PR.N | FixedReset | 2.11 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.40 Bid-YTW : 6.62 % |

| ENB.PR.D | FixedReset | 2.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-27 Maturity Price : 14.41 Evaluated at bid price : 14.41 Bid-YTW : 5.46 % |

| RY.PR.H | FixedReset | 2.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-27 Maturity Price : 21.20 Evaluated at bid price : 21.20 Bid-YTW : 3.63 % |

| FTS.PR.G | FixedReset | 2.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-27 Maturity Price : 18.45 Evaluated at bid price : 18.45 Bid-YTW : 3.96 % |

| BAM.PR.C | Floater | 2.45 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-27 Maturity Price : 10.45 Evaluated at bid price : 10.45 Bid-YTW : 4.58 % |

| BAM.PR.T | FixedReset | 2.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-27 Maturity Price : 17.03 Evaluated at bid price : 17.03 Bid-YTW : 4.60 % |

| BAM.PR.K | Floater | 2.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-27 Maturity Price : 10.40 Evaluated at bid price : 10.40 Bid-YTW : 4.60 % |

| BIP.PR.A | FixedReset | 2.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-27 Maturity Price : 21.30 Evaluated at bid price : 21.30 Bid-YTW : 5.00 % |

| ENB.PR.F | FixedReset | 2.92 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-27 Maturity Price : 15.16 Evaluated at bid price : 15.16 Bid-YTW : 5.41 % |

| ENB.PR.P | FixedReset | 2.94 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-27 Maturity Price : 15.40 Evaluated at bid price : 15.40 Bid-YTW : 5.37 % |

| ENB.PF.A | FixedReset | 3.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-27 Maturity Price : 16.86 Evaluated at bid price : 16.86 Bid-YTW : 5.28 % |

| ENB.PF.C | FixedReset | 3.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-27 Maturity Price : 17.05 Evaluated at bid price : 17.05 Bid-YTW : 5.22 % |

| MFC.PR.G | FixedReset | 3.46 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.80 Bid-YTW : 5.38 % |

| FTS.PR.M | FixedReset | 3.51 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-27 Maturity Price : 20.65 Evaluated at bid price : 20.65 Bid-YTW : 4.02 % |

| ENB.PF.E | FixedReset | 3.66 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-27 Maturity Price : 17.00 Evaluated at bid price : 17.00 Bid-YTW : 5.28 % |

| ENB.PR.N | FixedReset | 3.66 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-27 Maturity Price : 15.85 Evaluated at bid price : 15.85 Bid-YTW : 5.39 % |

| ENB.PR.T | FixedReset | 3.71 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-27 Maturity Price : 15.65 Evaluated at bid price : 15.65 Bid-YTW : 5.30 % |

| ENB.PR.J | FixedReset | 4.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-27 Maturity Price : 16.85 Evaluated at bid price : 16.85 Bid-YTW : 5.10 % |

| ENB.PR.H | FixedReset | 5.85 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-27 Maturity Price : 14.30 Evaluated at bid price : 14.30 Bid-YTW : 5.18 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| GWO.PR.P | Deemed-Retractible | 121,057 | Nesbitt crossed 120,000 at 24.55. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.55 Bid-YTW : 5.81 % |

| PWF.PR.L | Perpetual-Discount | 119,900 | Nesbitt crossed 119,900 at 23.75. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-27 Maturity Price : 23.25 Evaluated at bid price : 23.51 Bid-YTW : 5.47 % |

| BNS.PR.Q | FixedReset | 82,500 | TD crossed blocks of 39,900 and 40,000, both at 24.87. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.82 Bid-YTW : 3.16 % |

| TD.PF.B | FixedReset | 65,490 | TD crossed 40,000 at 20.73. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-27 Maturity Price : 20.74 Evaluated at bid price : 20.74 Bid-YTW : 3.72 % |

| ENB.PR.Y | FixedReset | 62,688 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-27 Maturity Price : 15.20 Evaluated at bid price : 15.20 Bid-YTW : 5.33 % |

| ENB.PF.C | FixedReset | 54,355 | RBC crossed 40,000 at 17.02. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-27 Maturity Price : 17.05 Evaluated at bid price : 17.05 Bid-YTW : 5.22 % |

| There were 34 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| MFC.PR.B | Deemed-Retractible | Quote: 21.35 – 22.22 Spot Rate : 0.8700 Average : 0.5029 YTW SCENARIO |

| IAG.PR.A | Deemed-Retractible | Quote: 21.50 – 22.18 Spot Rate : 0.6800 Average : 0.3913 YTW SCENARIO |

| RY.PR.J | FixedReset | Quote: 22.62 – 23.41 Spot Rate : 0.7900 Average : 0.5158 YTW SCENARIO |

| HSE.PR.C | FixedReset | Quote: 21.13 – 22.05 Spot Rate : 0.9200 Average : 0.6783 YTW SCENARIO |

| IFC.PR.C | FixedReset | Quote: 20.55 – 21.20 Spot Rate : 0.6500 Average : 0.4603 YTW SCENARIO |

| PWF.PR.S | Perpetual-Discount | Quote: 22.65 – 23.26 Spot Rate : 0.6100 Average : 0.4409 YTW SCENARIO |