There was some unpleasant Canadian economic news:

Canada’s economy shrank between January and March, the first contraction in four years and the largest since the 2009 recession as collapsing energy prices prompted a plunge in business investment.

Gross domestic product fell at a 0.6 percent annualized pace in the first quarter, Statistics Canada said Friday in Ottawa. The drop exceeded all 22 economist forecasts in a Bloomberg News survey, in which the median call was for an expansion of 0.3 percent. The agency revised its fourth-quarter growth estimate to 2.2 percent, from 2.4 percent previously.

…

Canada’s dollar weakened 0.7 percent to C$1.2521 per U.S. dollar at 9:20 a.m. Toronto time. Government bond yields fell, with debt due in two years down 4 basis points to 0.58 percent.In the U.S., gross domestic product shrank at a 0.7 percent annualized rate, revised from a previously reported 0.2 percent gain, according to Commerce Department figures issued Friday in Washington.

…

Business gross fixed capital formation — or business investment — fell at a 9.7 percent annualized pace in the first quarter, the most since the first three months of 2009. Support activities for mining and oil and gas extraction fell by 30 percent.Consumer spending growth slowed to an annualized 0.4 percent rate, the slowest since the start of 2009, from 2.1 percent in the fourth quarter. Transportation fell for the first time in 10 quarters, as vehicle purchases declined.

Exports fell 1.1 percent, the second straight quarterly decline. Imports dropped 1.5 percent.

Crude oil is Canada’s top export, and lower prices triggered a deterioration in housing markets in Alberta, site of major oil sands deposits.

On a monthly basis, Canada’s gross domestic product fell 0.2 percent in March, the third straight decline. The contraction was led by a 2.6 percent fall in mining, quarrying, and oil and gas extraction. Economists forecast a monthly GDP expansion of 0.2 percent.

Returning to yesterday‘s scandalmongering, there are rumours that Hastert was blackmailed due to a little old-fashioned pederasty in the ’80’s (some might say, “old school”). But what really gets my goat is the smarmy propaganda from the IRS:

The USA PATRIOT Act of 2001 increased the scope of these laws to help trace funds used for terrorism.

Ha! There’s even more bullshit from the FBI, although they now admit the Patriot Act hasn’t accomplished much vis a vis terror. However, that hasn’t stopped the sleazebags in Canada from cranking up the old fearometer, although it doesn’t work as well as it used to.

The month closed with another poor day for the Canadian preferred share market, with PerpetualDiscounts down 12bp, FixedResets losing 27bp and DeemedRetractibles off 9bp. A lengthy Performance Highlights table is notable for the number of FixedReset losers. Volume was slightly below average.

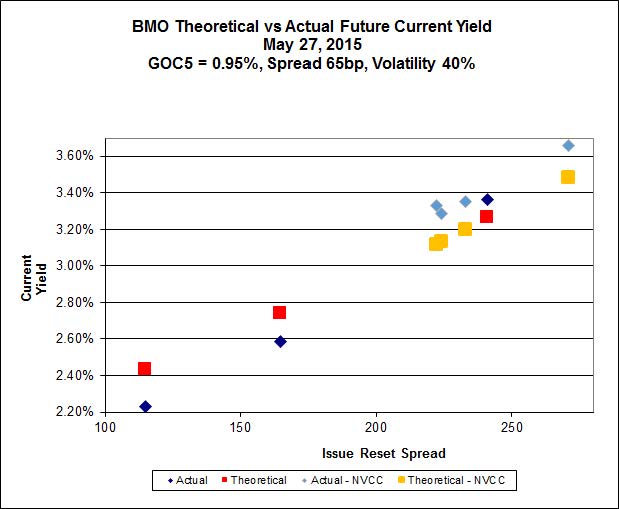

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

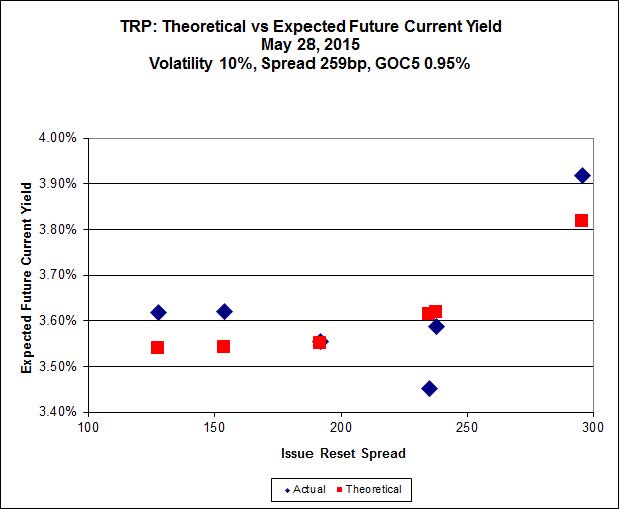

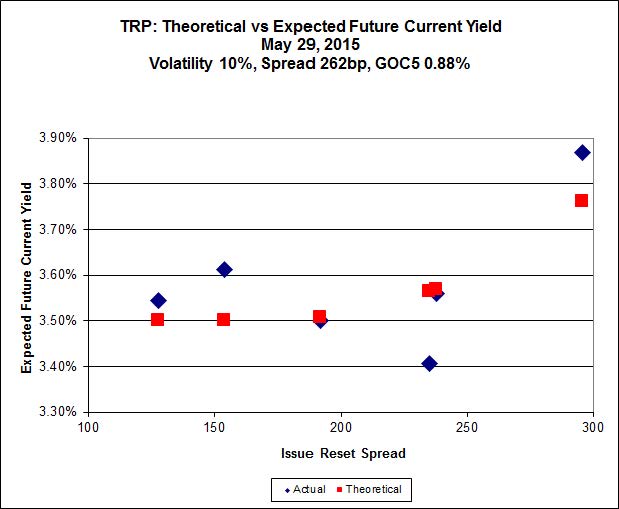

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 23.70 to be $1.05 rich, while TRP.PR.G, resetting 2020-11-30 at +296, is $0.70 cheap at its bid price of 24.82.

Click for Big

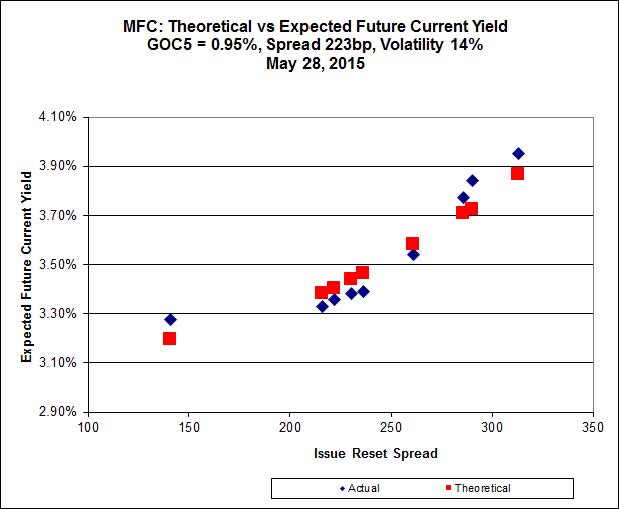

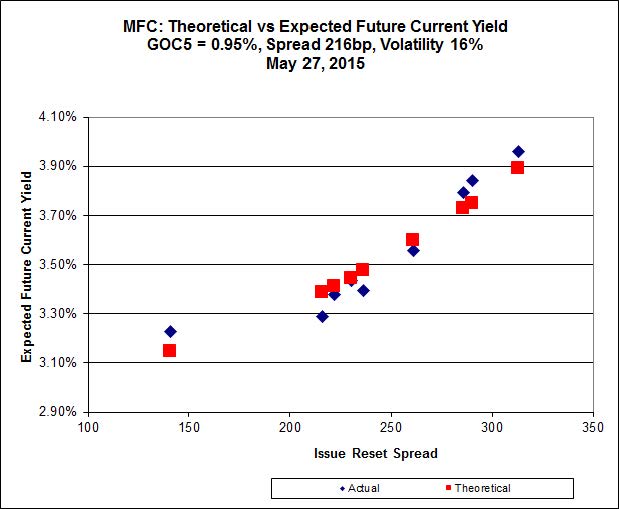

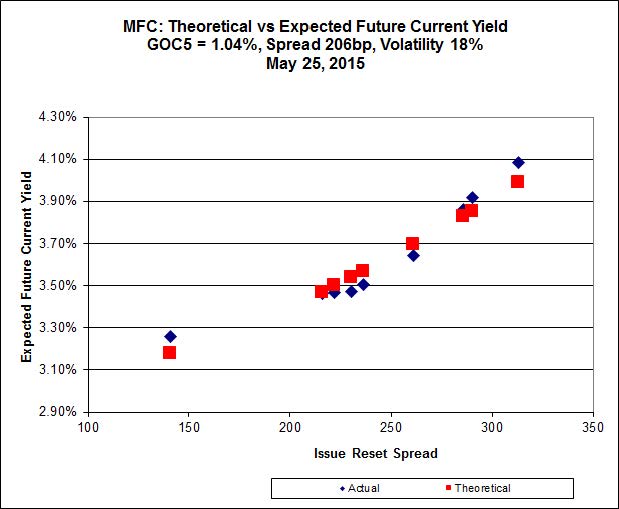

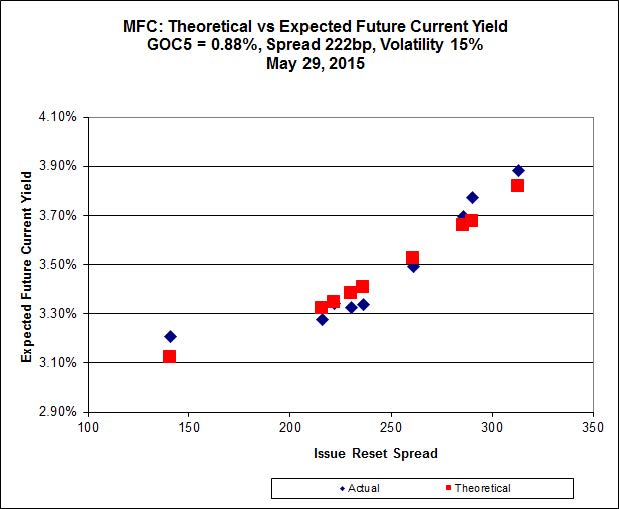

Another excellent fit, but the numbers are perplexing. Implied Volatility for MFC continues to be a conundrum. It is still too high if we consider that NVCC rules will never apply to these issues; it is still too low if we consider them to be NVCC non-compliant issues (and therefore with Deemed Maturities in the call schedule).

Most expensive is MFC.PR.M, resetting at +236 on 2019-12-19, bid at 24.26 to be $0.49 rich, while MFC.PR.G, resetting at +290bp on 2016-12-19, is bid at 25.05 to be $0.66 cheap.

Click for Big

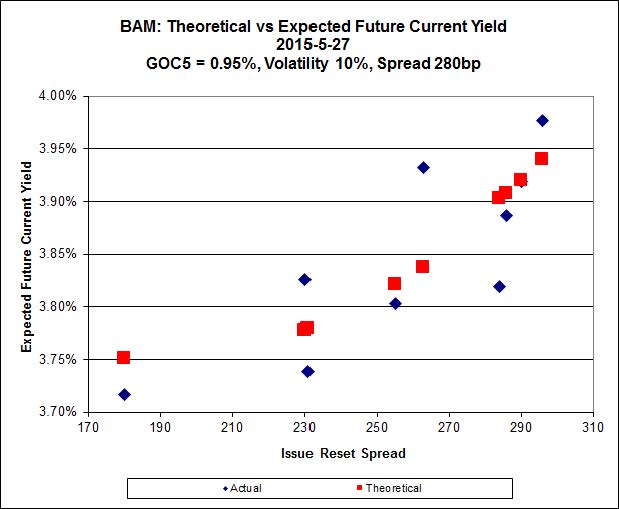

The cheapest issue relative to its peers is BAM.PF.B, resetting at +263bp on 2019-3-31, bid at 22.90 to be $0.48 cheap. BAM.PF.G, resetting at +284bp 2020-6-30 is bid at 24.90 and appears to be $0.51 rich.

Click for Big

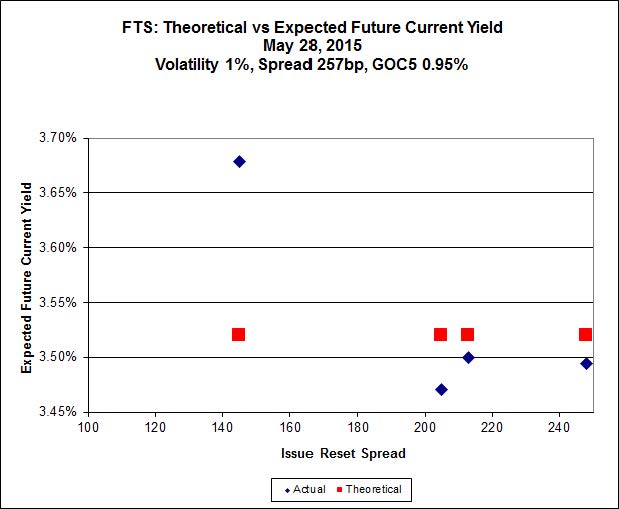

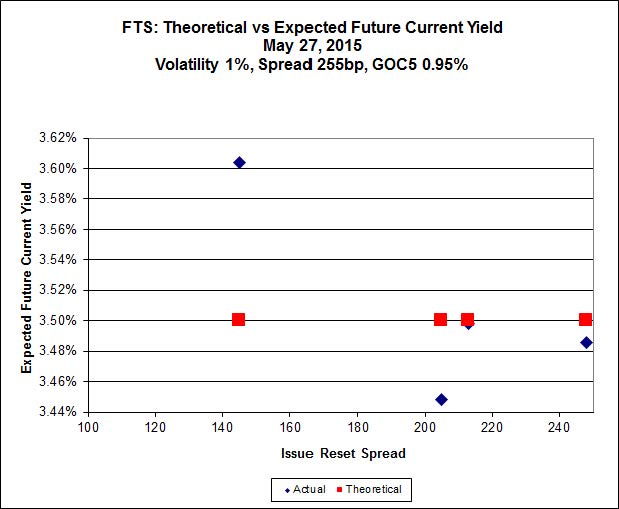

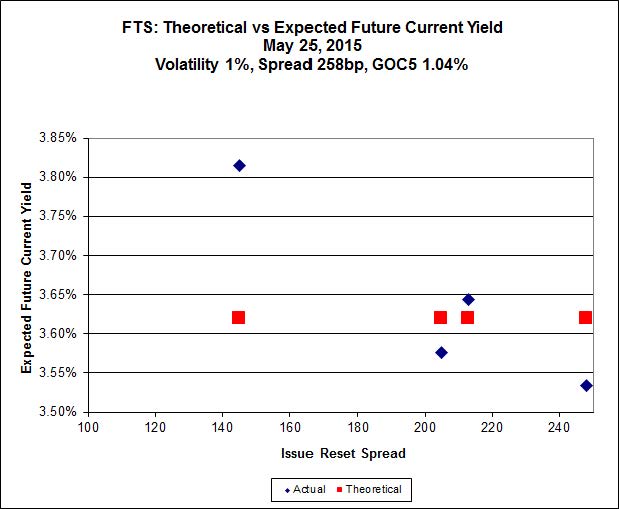

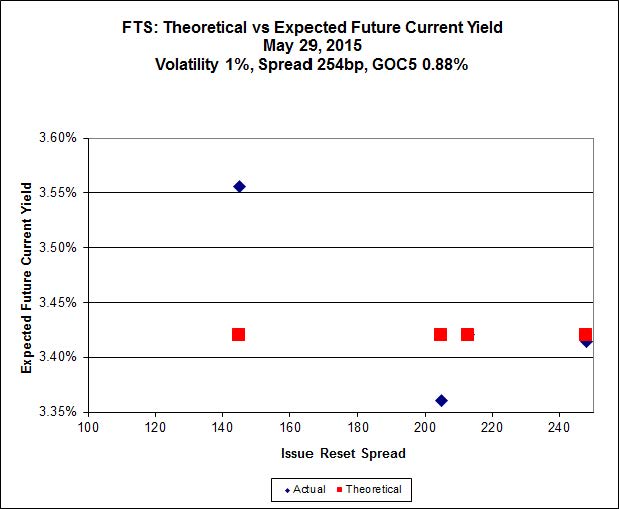

FTS.PR.H, with a spread of +145bp, and bid at 16.38, looks $0.65 cheap and resets 2015-6-1. FTS.PR.K, with a spread of +205bp and resetting 2019-3-1, is bid at 21.80 and is $0.38 rich.

Click for Big

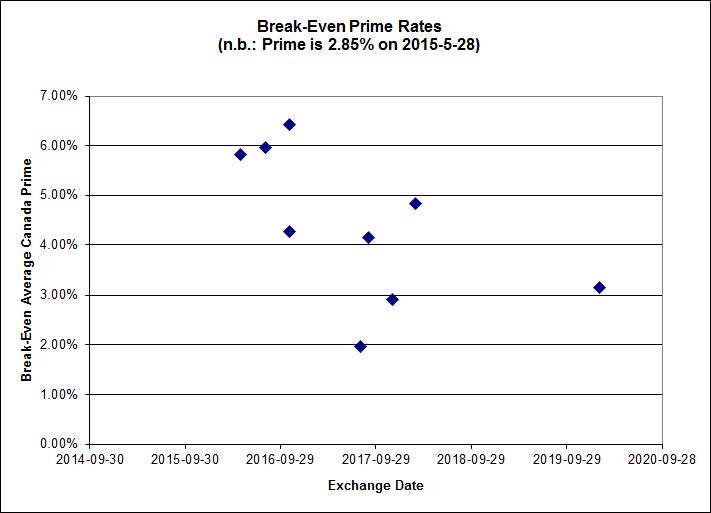

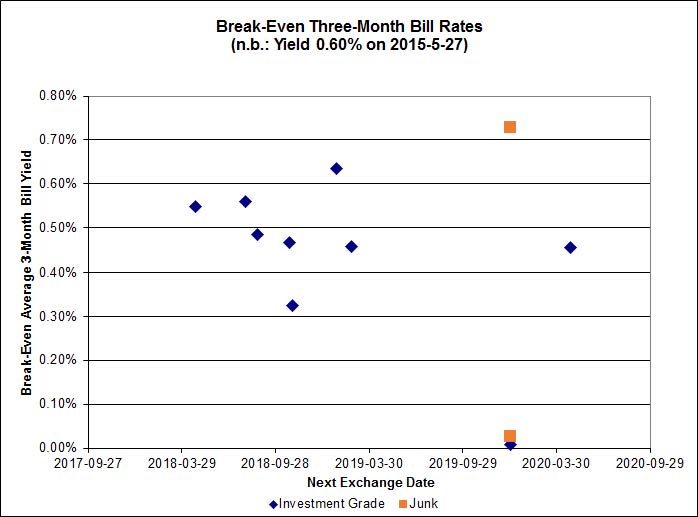

Investment-grade pairs predict an average over the next five-odd years of about 0.45%, and the TRP.PR.A / TRP.PR.F pair is no longer an abnormal outlier. On the junk side, four pairs are outside the range of the graph: FFH.PR.E / FFH.PR.F at -1.09%; AIM.PR.A / AIM.PR.B at -0.71%; BRF.PR.A / BRF.PR.B at -0.60%; and FFH.PR.C / FFH.PR.D at +1.12%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.2097 % | 2,261.0 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.2097 % | 3,953.4 |

| Floater | 3.21 % | 3.37 % | 54,815 | 18.76 | 4 | 0.2097 % | 2,403.6 |

| OpRet | 4.44 % | -12.58 % | 31,193 | 0.09 | 2 | 0.0593 % | 2,781.8 |

| SplitShare | 4.58 % | 4.46 % | 69,276 | 3.33 | 3 | -0.0801 % | 3,257.1 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0593 % | 2,543.7 |

| Perpetual-Premium | 5.46 % | 4.71 % | 61,897 | 0.58 | 18 | 0.0524 % | 2,519.6 |

| Perpetual-Discount | 5.09 % | 5.07 % | 116,873 | 15.37 | 15 | -0.1207 % | 2,765.1 |

| FixedReset | 4.46 % | 3.80 % | 266,309 | 16.46 | 86 | -0.2661 % | 2,391.3 |

| Deemed-Retractible | 4.98 % | 3.47 % | 108,299 | 0.58 | 34 | -0.0860 % | 2,636.0 |

| FloatingReset | 2.55 % | 2.93 % | 59,748 | 6.14 | 7 | -0.0304 % | 2,338.3 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| GWO.PR.N | FixedReset | -2.99 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.04 Bid-YTW : 7.03 % |

| TRP.PR.C | FixedReset | -2.62 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-29 Maturity Price : 16.75 Evaluated at bid price : 16.75 Bid-YTW : 3.98 % |

| SLF.PR.H | FixedReset | -2.34 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.73 Bid-YTW : 5.02 % |

| MFC.PR.B | Deemed-Retractible | -2.03 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.22 Bid-YTW : 5.61 % |

| BAM.PF.C | Perpetual-Discount | -1.85 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-29 Maturity Price : 21.96 Evaluated at bid price : 22.28 Bid-YTW : 5.52 % |

| MFC.PR.K | FixedReset | -1.69 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.20 Bid-YTW : 4.38 % |

| BMO.PR.T | FixedReset | -1.36 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-29 Maturity Price : 22.78 Evaluated at bid price : 23.89 Bid-YTW : 3.50 % |

| RY.PR.Z | FixedReset | -1.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-29 Maturity Price : 22.90 Evaluated at bid price : 24.10 Bid-YTW : 3.45 % |

| TRP.PR.D | FixedReset | -1.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-29 Maturity Price : 22.29 Evaluated at bid price : 22.90 Bid-YTW : 3.85 % |

| SLF.PR.G | FixedReset | -1.22 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.99 Bid-YTW : 7.09 % |

| IFC.PR.C | FixedReset | -1.18 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.26 Bid-YTW : 4.26 % |

| TRP.PR.B | FixedReset | -1.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-29 Maturity Price : 15.24 Evaluated at bid price : 15.24 Bid-YTW : 3.83 % |

| ENB.PR.H | FixedReset | -1.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-29 Maturity Price : 17.95 Evaluated at bid price : 17.95 Bid-YTW : 4.64 % |

| TD.PF.B | FixedReset | -1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-29 Maturity Price : 22.72 Evaluated at bid price : 23.74 Bid-YTW : 3.55 % |

| MFC.PR.C | Deemed-Retractible | -1.04 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.83 Bid-YTW : 5.67 % |

| CM.PR.O | FixedReset | -1.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-29 Maturity Price : 22.75 Evaluated at bid price : 23.81 Bid-YTW : 3.61 % |

| NA.PR.W | FixedReset | -1.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-29 Maturity Price : 22.86 Evaluated at bid price : 24.15 Bid-YTW : 3.47 % |

| BMO.PR.W | FixedReset | -1.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-29 Maturity Price : 22.58 Evaluated at bid price : 23.51 Bid-YTW : 3.54 % |

| BIP.PR.A | FixedReset | 1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-29 Maturity Price : 23.05 Evaluated at bid price : 24.71 Bid-YTW : 4.62 % |

| TRP.PR.F | FloatingReset | 1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-29 Maturity Price : 19.00 Evaluated at bid price : 19.00 Bid-YTW : 3.32 % |

| ENB.PR.F | FixedReset | 1.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-29 Maturity Price : 19.33 Evaluated at bid price : 19.33 Bid-YTW : 4.72 % |

| BAM.PR.B | Floater | 1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-29 Maturity Price : 14.93 Evaluated at bid price : 14.93 Bid-YTW : 3.37 % |

| CIU.PR.C | FixedReset | 1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-29 Maturity Price : 16.56 Evaluated at bid price : 16.56 Bid-YTW : 3.75 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| HSE.PR.C | FixedReset | 105,036 | TD crossed 88,500 at 24.99. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-29 Maturity Price : 23.16 Evaluated at bid price : 24.92 Bid-YTW : 4.21 % |

| HSE.PR.A | FixedReset | 96,175 | TD crossed 88,500 at 17.15. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-29 Maturity Price : 16.95 Evaluated at bid price : 16.95 Bid-YTW : 4.28 % |

| BNS.PR.Z | FixedReset | 54,670 | RBC bought 15,000 from Nesbitt at 23.69, then crossed 14,700 at 23.75. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.52 Bid-YTW : 3.60 % |

| CU.PR.E | Perpetual-Discount | 50,350 | Desjardins crossed 48,200 at 24.90. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-29 Maturity Price : 24.32 Evaluated at bid price : 24.78 Bid-YTW : 4.94 % |

| RY.PR.D | Deemed-Retractible | 38,847 | Nesbitt crossed 28,000 at 25.32. YTW SCENARIO Maturity Type : Call Maturity Date : 2015-06-28 Maturity Price : 25.25 Evaluated at bid price : 25.32 Bid-YTW : 1.82 % |

| BMO.PR.M | FixedReset | 37,165 | Scotia crossed 35,700 at 25.10. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.10 Bid-YTW : 2.99 % |

| There were 28 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| MFC.PR.N | FixedReset | Quote: 23.91 – 24.65 Spot Rate : 0.7400 Average : 0.5463 YTW SCENARIO |

| POW.PR.G | Perpetual-Premium | Quote: 26.10 – 26.59 Spot Rate : 0.4900 Average : 0.3372 YTW SCENARIO |

| BAM.PF.C | Perpetual-Discount | Quote: 22.28 – 22.74 Spot Rate : 0.4600 Average : 0.3288 YTW SCENARIO |

| BMO.PR.T | FixedReset | Quote: 23.89 – 24.20 Spot Rate : 0.3100 Average : 0.1935 YTW SCENARIO |

| HSB.PR.C | Deemed-Retractible | Quote: 25.40 – 25.80 Spot Rate : 0.4000 Average : 0.2839 YTW SCENARIO |

| IFC.PR.C | FixedReset | Quote: 24.26 – 24.64 Spot Rate : 0.3800 Average : 0.2672 YTW SCENARIO |