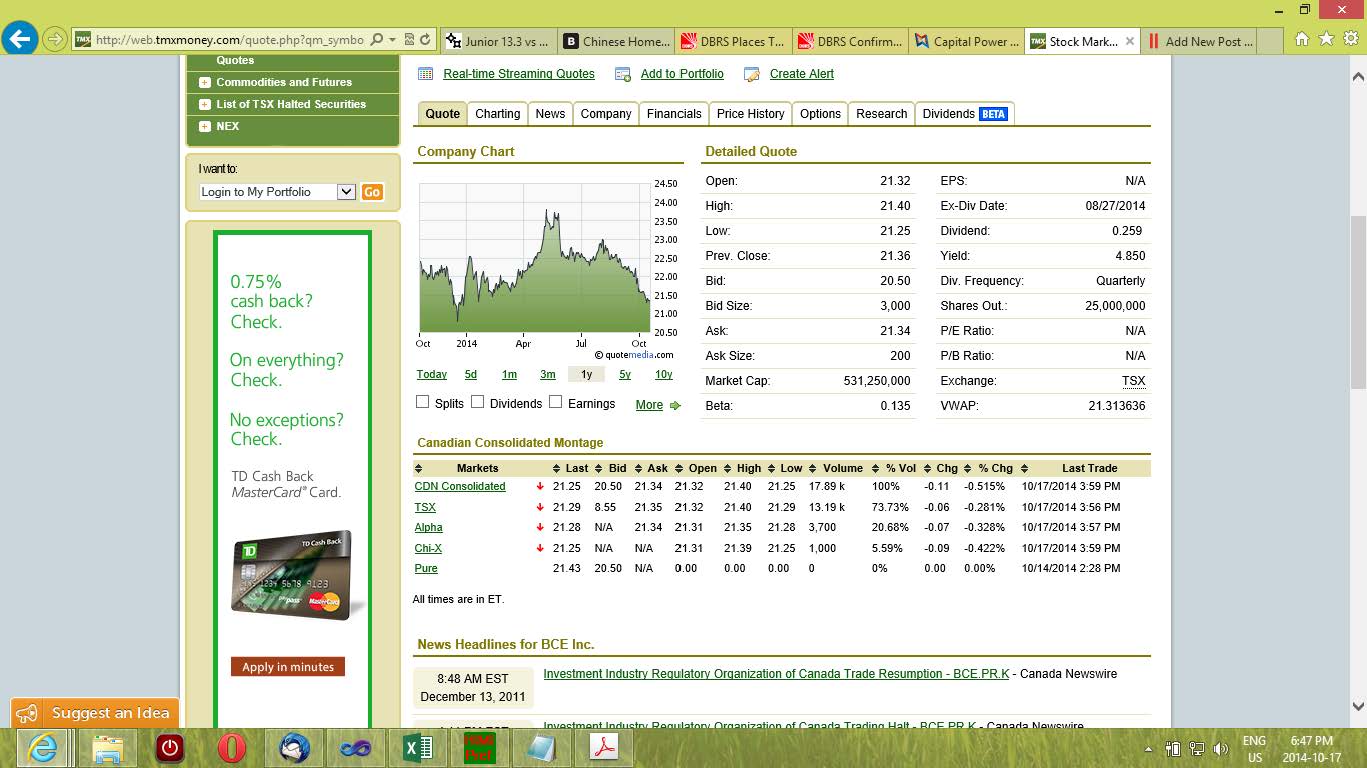

Today’s Toronto Stock Exchange Screw-Up regards BCE.PR.K:

Click for Big

Look that that quote on the Toronto Stock Exchange – which, together with its Venture sibling, comprise Canada’s premier equities markets: 8.55-21.35, a small spread of only $12.80. Since the Exchange refuses to sell me closing quotes, instead selling me “Last” quotes, I’m not sure what the actual closing quote might have been – since I don’t feel like spending extra money to get the detail of the last few minutes. So it might have been a post-4pm bid cancellation, it might be another shining example of how TSX’s Market Maker system maximizes market efficiency. I’ll let youse guys figure it out.

Anyway, HIMPref™ threw up when I tried to tell it the reported bid price, so I have substituted $20.50, which is the bid on Pure.

Meanwhile, Capital Power, proud issuer of CPX.PR.A, CPX.PR.C and CPX.PR.E, issued a profit warning:

Capital Power Corporation (Capital Power, or the Company) (TSX:CPX) provided an update today on its third quarter 2014 financial results and its financial guidance for 2014.

In the third quarter of 2014, Capital Power’s owned plants achieved strong plant availability of 97% which was consistent with expectations. However, due to lower plant availability at the acquired Sundance PPA units, other plant derates, and lower Alberta wind generation, overall electricity generation production was below expectations. Accordingly, the Company expects third quarter net income and funds from operations to be below previous expectations. These non-Capital Power operated plant outages occurred primarily in July coinciding with a period of pricing volatility with Alberta spot power prices averaging $122 per megawatt hour (MWh) in the month compared with $45 per MWh in August and $24 per MWh in September. As a result, with commercial production 100% sold forward in July, the Company was required to cover a short market position that negatively impacted its portfolio optimization position in the quarter.

The Company has updated its outlook for funds from operations for the year, which are now expected at the low end of the forecast range of $360 million to $400 million.

In addition, net income for the third quarter of 2014 was negatively impacted by a non-cash write-down of deferred tax assets of $73 million. The write-down related to the accounting impact of U.S. income tax loss carry forwards that can no longer be recognized for accounting purposes based on the Company’s current long term forecast for U.S. taxable income. The forecast showed a decline in taxable income over the latter years of the forecast. For income tax purposes, these U.S net operating losses do not expire until the 2027 to 2033 period. Accordingly, they retain economic value and could result in the Company recording deferred tax assets in the future. The Company continues to pursue U.S. contracted power opportunities and the U.S. business development pipeline is active. Importantly, the write-down is a non-cash item and has no impact on operations or other key performance measures.

Capital Power will be releasing its third quarter 2014 results on October 24, 2014 after the TSX market closes.

I haven’t seen anything yet from the Credit Rating Agencies as to whether or not they consider this serious.

Advantaged Preferred Share Trust (PFR), which made it into one of my articles, was confirmed at STA-2 (middle) by DBRS:

DBRS has today confirmed the stability rating of STA-2 (middle) to the retractable units (the Units) issued by Advantaged Preferred Share Trust (the Trust).

Proceeds from the Trust’s offerings have been used to enter into a forward agreement with Royal Bank of Canada in order to gain exposure to a diversified portfolio of preferred shares (the Portfolio). The forward agreement provides Unitholders with a return equivalent to a direct investment in the Portfolio. The Portfolio is passively managed by RBC Dominion Securities Inc. (the Administrator).

On August 26, 2010, DBRS assigned a stability rating of STA-2 (middle) to the Units issued by the Trust in accordance with the new methodology for rating structured income funds published in May 2010. The rating was mainly based on the strong credit quality of the Trust’s preferred share portfolio and the limited flexibility of the Administrator to invest in riskier assets. The rating was last confirmed on October 18, 2013, at STA-2 (middle).

Since October 2013, the performance of the Portfolio has been fairly stable. The weighted-average yield of the Portfolio is approximately 5.01% as of September 30, 2014. The Trust’s current net income (including a regular additional payment under the forward agreement to offset operating expenses) covers 98.6% of the distribution paid out to Unitholders. As a result, the rating of STA-2 (middle) on the Units has been confirmed. The main constraints to the rating are the interest rate risk of the Portfolio and the potential for capital losses and reductions in income resulting from underlying securities being called for redemption by their respective issuers.

We’re always hearing about Chinese property buyers in Vancouver, but they’re all over the States as well:

This flood of money, arriving from China despite strict currency controls, has helped the city build a $20 million high school performing arts center and the local Mercedes dealership expand. “Thank God for them coming over here,” says Peggy Fong Chen, a broker in Arcadia for many years. “They saved our recession.” The new residents are from China’s rising millionaire class—entrepreneurs who’ve made fortunes building railroads in Tibet, converting bioenergy in Beijing, and developing real estate in Chongqing. One co-owner of a $6.5 million house is a 19-year-old college student, the daughter of the chief executive of a company the state controls.

Arcadia is a concentrated version of what’s happening across the U.S. The Hurun Report, a magazine in Shanghai about China’s wealthy elite, estimates that almost two-thirds of the country’s millionaires have already emigrated or plan to do so. They’re scooping up homes from Seattle to New York, buying luxury goods on Fifth Avenue, and paying full freight to send their kids to U.S. colleges. Chinese nationals hold roughly $660 billion in personal wealth offshore, according to Boston Consulting Group, and the National Association of Realtors says $22 billion of that was spent in the past year acquiring U.S. homes.

It was a strong day for the Canadian preferred share market, with PerpetualDiscounts gaining 6bp, FixedResets winning 32bp and DeemedRetractibles up 11bp. Volatility was high, highlighted by losing Floating Rate issues and winning FixedResets. Volume was well above average (so there, prefQC!).

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 3.13 % | 3.12 % | 22,087 | 19.40 | 1 | -1.2768 % | 2,668.1 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -1.8156 % | 3,987.2 |

| Floater | 2.99 % | 3.19 % | 63,568 | 19.26 | 4 | -1.8156 % | 2,677.3 |

| OpRet | 4.04 % | 2.55 % | 102,222 | 0.08 | 1 | 0.0394 % | 2,733.6 |

| SplitShare | 4.31 % | 4.10 % | 85,562 | 3.82 | 5 | -0.4050 % | 3,143.0 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0394 % | 2,499.6 |

| Perpetual-Premium | 5.49 % | 0.14 % | 72,621 | 0.08 | 18 | 0.1977 % | 2,452.7 |

| Perpetual-Discount | 5.33 % | 5.15 % | 95,278 | 15.11 | 18 | 0.0647 % | 2,587.0 |

| FixedReset | 4.22 % | 3.69 % | 169,202 | 16.44 | 75 | 0.3170 % | 2,550.3 |

| Deemed-Retractible | 5.03 % | 2.54 % | 102,803 | 0.44 | 42 | 0.1062 % | 2,557.9 |

| FloatingReset | 2.55 % | -4.24 % | 62,578 | 0.08 | 6 | 0.1830 % | 2,550.8 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BAM.PR.C | Floater | -2.83 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-10-17 Maturity Price : 16.48 Evaluated at bid price : 16.48 Bid-YTW : 3.20 % |

| BAM.PR.B | Floater | -2.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-10-17 Maturity Price : 16.53 Evaluated at bid price : 16.53 Bid-YTW : 3.19 % |

| BAM.PR.K | Floater | -2.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-10-17 Maturity Price : 16.53 Evaluated at bid price : 16.53 Bid-YTW : 3.19 % |

| BAM.PR.E | Ratchet | -1.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-10-17 Maturity Price : 23.56 Evaluated at bid price : 23.97 Bid-YTW : 3.12 % |

| PVS.PR.B | SplitShare | -1.20 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2019-01-10 Maturity Price : 25.00 Evaluated at bid price : 24.80 Bid-YTW : 4.71 % |

| FTS.PR.H | FixedReset | 1.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-10-17 Maturity Price : 20.36 Evaluated at bid price : 20.36 Bid-YTW : 3.72 % |

| POW.PR.G | Perpetual-Premium | 1.27 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-04-15 Maturity Price : 25.00 Evaluated at bid price : 26.23 Bid-YTW : 4.75 % |

| MFC.PR.F | FixedReset | 1.31 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.35 Bid-YTW : 4.50 % |

| SLF.PR.I | FixedReset | 1.36 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2016-12-31 Maturity Price : 25.00 Evaluated at bid price : 26.15 Bid-YTW : 2.21 % |

| IFC.PR.A | FixedReset | 1.84 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.83 Bid-YTW : 4.19 % |

| FTS.PR.K | FixedReset | 2.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-10-17 Maturity Price : 23.22 Evaluated at bid price : 25.03 Bid-YTW : 3.55 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| TD.PR.O | Deemed-Retractible | 331,587 | TD crossed blocks of 300,000 and 13,400, both at 24.98, and sold 15,000 to Nesbitt at the same price. YTW SCENARIO Maturity Type : Call Maturity Date : 2014-11-30 Maturity Price : 25.00 Evaluated at bid price : 24.98 Bid-YTW : 4.00 % |

| BMO.PR.W | FixedReset | 231,516 | RBC crossed 50,000 at 25.02. Nesbitt crossed blocks of 50,000 and 100,000 at the same price. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-10-17 Maturity Price : 23.21 Evaluated at bid price : 25.16 Bid-YTW : 3.64 % |

| MFC.PR.M | FixedReset | 182,128 | Nesbitt crossed 33,200 at 25.35; TD crossed 99,900 at the same price. YTW SCENARIO Maturity Type : Call Maturity Date : 2019-12-19 Maturity Price : 25.00 Evaluated at bid price : 25.33 Bid-YTW : 3.78 % |

| TD.PR.S | FixedReset | 171,393 | Nesbitt crossed 45,000 at 25.15; RBC crossed 105,400 at the same price. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.16 Bid-YTW : 3.14 % |

| CU.PR.D | Perpetual-Discount | 155,587 | Desjardins crossed 153,400 at 24.04. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-10-17 Maturity Price : 23.66 Evaluated at bid price : 24.04 Bid-YTW : 5.15 % |

| RY.PR.I | FixedReset | 151,473 | Nesbitt crossed 33,000 at 25.57, then another 111,100 at 25.63. YTW SCENARIO Maturity Type : Call Maturity Date : 2019-02-24 Maturity Price : 25.00 Evaluated at bid price : 25.58 Bid-YTW : 3.09 % |

| NA.PR.W | FixedReset | 133,285 | Scotia crossed 50,000 at 24.75, then bought 12,100 from National at the same price. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-10-17 Maturity Price : 23.05 Evaluated at bid price : 24.75 Bid-YTW : 3.73 % |

| TD.PF.B | FixedReset | 100,325 | RBC crossed blocks of 29,900 and 32,000, both at 25.04. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-10-17 Maturity Price : 23.23 Evaluated at bid price : 25.15 Bid-YTW : 3.63 % |

| There were 40 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| PWF.PR.P | FixedReset | Quote: 22.16 – 22.75 Spot Rate : 0.5900 Average : 0.3901 YTW SCENARIO |

| BAM.PR.B | Floater | Quote: 16.53 – 16.99 Spot Rate : 0.4600 Average : 0.2650 YTW SCENARIO |

| BAM.PR.C | Floater | Quote: 16.48 – 16.91 Spot Rate : 0.4300 Average : 0.2626 YTW SCENARIO |

| CIU.PR.C | FixedReset | Quote: 20.42 – 21.23 Spot Rate : 0.8100 Average : 0.6474 YTW SCENARIO |

| SLF.PR.I | FixedReset | Quote: 26.15 – 26.55 Spot Rate : 0.4000 Average : 0.2442 YTW SCENARIO |

| TRP.PR.C | FixedReset | Quote: 20.63 – 21.20 Spot Rate : 0.5700 Average : 0.4149 YTW SCENARIO |