Banner headline on Bloomberg – An FX trade didn’t work out:

A senior currency dealer at Lloyds Banking Group Plc shared details of a pending order by his firm with a trader at another company to the potential detriment of the bank, according to four people with knowledge of the matter.

The Lloyds’s dealer, Martin Chantree, alerted the other trader on Jan. 31, 2013, that his desk had received instructions from the bank’s treasury department to swap more than 300 million pounds ($499 million) for dollars and that they would continue selling regardless of price movements, said two of the people, who asked not to be identified amid a probe into alleged rigging of the currency market. The recipient of the tip worked for oil company BP Plc, the other two people said.

In the seven minutes between the communication at 10:53 a.m. and the time Lloyds began executing the order, the pound fell 16 basis points against the dollar, or 0.16 percentage point, according to data compiled by Bloomberg. As the U.K. currency tumbled, costing Lloyds an estimated $750,000, Chantree told colleagues that maybe he shouldn’t have shared the information, two of the people said.

…

Lloyds suspended Chantree on Feb. 3 after inquiries by Bloomberg News about his alleged communications in advance of the trade. The London-based bank, which is 33 percent owned by the U.K. government, approached the FCA after discovering messages, including the 10:53 a.m. voice communication in which Chantree detailed the size and timing of the order, two of the people said.

…

Between 10:53 a.m. and 11 a.m. on the day of the trade, about when Lloyds began selling, the pound-dollar exchange rate fell to 1.5790 from 1.5815, data compiled by Bloomberg show.

…

Lloyds did internal deals of that size only six or seven times a year, two of the people said. When an order came in, some traders on the second floor of the bank’s Gresham Street headquarters in London’s financial district would place their own bets before executing the trade in a way that moved the market as much as possible, one of the people said. They were able to do this because notice was typically sent to more than one trader on the desk and Lloyds’s treasury unit didn’t scrutinize whether it got the best price, the person said. There’s no indication Chantree placed such bets that morning.

Well, sure. If you’re going to do size, you’ve got to show size. And sometimes showing size means everybody on the opposite side pulls their orders … which is consistent with what happened. Why else do you think dark pools are so popular? Trading size is more of an art than a science, and sometimes it’s art with a capital F. I will be kind and assume that Lloyds has suspended its trader only because they’re terrified of the regulators nowadays.

It seems very likely that the villain of the piece is Lloyds treasury. A market order for half a billion bucks? I will need to see a long detailed explanation before I’m convinced they’re not idiots.

Lest anybody think that I always take the traders’ side, I will say: front-running orders of this type was clearly wrong. In case of this particular type, the traders do in fact owe a fiduciary client to their institutional client … but only because the client is also their employer.

We may finally be approaching the approaching the elimination of the GSEs:

The bipartisan measure, drafted with input from President Barack Obama’s administration, would replace the U.S.-owned mortgage financiers with government bond insurance that would kick in only after private capital suffered losses of at least 10 percent, Senate Banking Committee Chairman Tim Johnson and Senator Mike Crapo said in a statement today. The bill would require most borrowers to make down payments of at least 5 percent.

…

The government would play a smaller role in the market by taking a backstop position on mortgage securities, stepping in only if private interests were wiped out by catastrophic losses. A new agency called the Federal Mortgage Insurance Corp. would charge fees to issue a government guarantee on bonds that would kick in only after private investors suffered losses of at least 10 percent.

It was a mixed day for the Canadian preferred share market, with PerpetualDiscounts up 17bp, FixedResets off 10bp and DeemedRetractibles gaining 4bp. Volatility was above average due to stellar performance from Floating Rate issues, indicating that the recently postponed global hyperinflation has now been rescheduled. Volume was high.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 1.2437 % | 2,440.9 |

| FixedFloater | 4.53 % | 3.80 % | 28,424 | 17.76 | 1 | 1.2566 % | 3,742.5 |

| Floater | 2.97 % | 3.10 % | 53,774 | 19.41 | 4 | 1.2437 % | 2,635.5 |

| OpRet | 4.64 % | 0.12 % | 83,169 | 0.22 | 3 | 0.0129 % | 2,682.5 |

| SplitShare | 4.82 % | 4.38 % | 58,752 | 4.34 | 5 | 0.2237 % | 3,071.2 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0129 % | 2,452.9 |

| Perpetual-Premium | 5.63 % | -1.56 % | 92,007 | 0.08 | 11 | 0.1002 % | 2,353.3 |

| Perpetual-Discount | 5.47 % | 5.55 % | 133,316 | 14.40 | 26 | 0.1674 % | 2,425.5 |

| FixedReset | 4.72 % | 3.55 % | 230,035 | 6.84 | 77 | -0.0996 % | 2,501.2 |

| Deemed-Retractible | 5.06 % | 3.07 % | 163,086 | 0.21 | 42 | 0.0434 % | 2,463.8 |

| FloatingReset | 2.59 % | 2.59 % | 193,808 | 7.11 | 5 | 0.0724 % | 2,440.2 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| SLF.PR.G | FixedReset | -1.12 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.01 Bid-YTW : 4.59 % |

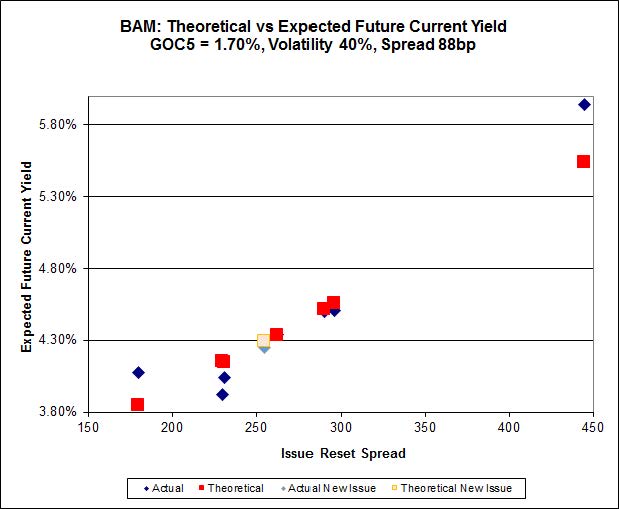

| BAM.PR.T | FixedReset | -1.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-03-11 Maturity Price : 23.22 Evaluated at bid price : 24.59 Bid-YTW : 4.06 % |

| BAM.PR.N | Perpetual-Discount | 1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-03-11 Maturity Price : 20.62 Evaluated at bid price : 20.62 Bid-YTW : 5.88 % |

| BAM.PR.G | FixedFloater | 1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-03-11 Maturity Price : 21.58 Evaluated at bid price : 20.95 Bid-YTW : 3.80 % |

| BAM.PR.C | Floater | 1.54 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-03-11 Maturity Price : 17.09 Evaluated at bid price : 17.09 Bid-YTW : 3.10 % |

| BAM.PR.B | Floater | 1.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-03-11 Maturity Price : 17.13 Evaluated at bid price : 17.13 Bid-YTW : 3.10 % |

| BAM.PR.K | Floater | 1.86 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-03-11 Maturity Price : 17.01 Evaluated at bid price : 17.01 Bid-YTW : 3.12 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| RY.PR.L | FixedReset | 444,773 | I think Jacob Securities crossed 350,600 at 25.80, but it’s not clear. TMXMoney.com agrees on the total volue, and the VWAP makes sense, but the block trade report just shows a trade and cancel at 25.80 with no replacement. Also, the price is extremely low. So who knows? RBC crossed 76,000 at 26.03, which seems like a much more credible trade. YTW SCENARIO Maturity Type : Call Maturity Date : 2019-02-24 Maturity Price : 25.00 Evaluated at bid price : 26.11 Bid-YTW : 3.34 % |

| BNS.PR.T | FixedReset | 157,054 | RBC crossed 33,000 at 25.34; Scotia crossed two blocks of 59,300 each, both at 25.32, eleven minutes apart. YTW SCENARIO Maturity Type : Call Maturity Date : 2014-04-25 Maturity Price : 25.00 Evaluated at bid price : 25.32 Bid-YTW : 1.13 % |

| RY.PR.Z | FixedReset | 121,435 | RBC crossed 97,000 at 25.45. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-03-11 Maturity Price : 23.27 Evaluated at bid price : 25.39 Bid-YTW : 3.70 % |

| BAM.PF.C | Perpetual-Discount | 107,060 | RBC crossed blocks of 16,100 and 79,900, both at 20.75. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-03-11 Maturity Price : 20.76 Evaluated at bid price : 20.76 Bid-YTW : 5.97 % |

| MFC.PR.C | Deemed-Retractible | 87,044 | Nesbitt crossed 30,000 at 21.78; RBC crossed 46,200 at 21.75. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.67 Bid-YTW : 6.22 % |

| BNS.PR.Z | FixedReset | 64,733 | Scotia bought 31,100 from anonymous at 24.00. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.00 Bid-YTW : 3.82 % |

| There were 47 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| GCS.PR.A | SplitShare | Quote: 25.08 – 25.46 Spot Rate : 0.3800 Average : 0.2618 YTW SCENARIO |

| HSE.PR.A | FixedReset | Quote: 22.54 – 22.82 Spot Rate : 0.2800 Average : 0.1723 YTW SCENARIO |

| GWO.PR.F | Deemed-Retractible | Quote: 25.31 – 25.62 Spot Rate : 0.3100 Average : 0.2156 YTW SCENARIO |

| ELF.PR.H | Perpetual-Discount | Quote: 24.15 – 24.40 Spot Rate : 0.2500 Average : 0.1598 YTW SCENARIO |

| SLF.PR.G | FixedReset | Quote: 22.01 – 22.24 Spot Rate : 0.2300 Average : 0.1527 YTW SCENARIO |

| TD.PR.Q | Deemed-Retractible | Quote: 26.08 – 26.31 Spot Rate : 0.2300 Average : 0.1627 YTW SCENARIO |