Assiduous Reader PL writes in and says:

I know that getting and correctly interpreting market reaction to information quicker whether one minute or one second than the other players will always be an advantage. And though I think there should be a small transaction tax on all of us to reduce this madness I know this may never happen in North America, even though it is happening in Europe I believe.

HOWEVER the one HFT practice that should be stopped is the fake orders. Any bid or offer should be required to stay in for one minute during trading hours. If they want to enter BS orders then let them do them before market opens.

I never buy or sell anything in the first half hour anyway. Your thoughts on eliminating fake deliberately deceptive orders.?

I disagree with your characterization of short-duration orders as “fake”. They may not be posted on the exchange for very long (as little as a few milliseconds), but for the entire time they’re up, they may be executed against.

This is a controversial subject – Panther Energy Trading LLC was victimized by the CFTC for spoofing:

According to the Order, Coscia and Panther made money by employing a computer algorithm that was designed to unlawfully place and quickly cancel orders in exchange-traded futures contracts. For example, Coscia and Panther would place a relatively small order to sell futures that they did want to execute, which they quickly followed with several large buy orders at successively higher prices that they intended to cancel. By placing the large buy orders, Coscia and Panther sought to give the market the impression that there was significant buying interest, which suggested that prices would soon rise, raising the likelihood that other market participants would buy from the small order Coscia and Panther were then offering to sell. Although Coscia and Panther wanted to give the impression of buy-side interest, they entered the large buy orders with the intent that they be canceled before these orders were actually executed. Once the small sell order was filled according to the plan, the buy orders would be cancelled, and the sequence would quickly repeat but in reverse – a small buy order followed by several large sell orders. With this back and forth, Coscia and Panther profited on the executions of the small orders many times over the period in question.

David Meister, the CFTC’s Enforcement Director, said, “While forms of algorithmic trading are of course lawful, using a computer program that is written to spoof the market is illegal and will not be tolerated. We will use the Dodd Frank anti-disruptive practices provision against schemes like this one to protect market participants and promote market integrity, particularly in the growing world of electronic trading platforms.”

I take the view that you can’t cheat an honest man. If somebody is spoofed into taking the ‘wrong’ side of the market in this way, he has only himself to blame. The markets exist for the formation and movement of long term capital – these short-term games are basically irrelevant to this purpose, but to the extent they do exist, they narrow spreads for real-money players. Speculators – such as HFT, traditional brokerages and fools – should be of interest to policy makers only to the extent that they provide liquidity to real money. We should not be doing a damn thing to protect traders whose Big Idea is ‘buy things when they start to go up’. As I said on May 7, 2010:

The way to eliminate stupid dumb trading is to ensure that stupid dumb traders lose all their money, go bankrupt and die.

The CFTC – under Dodd-Frank – takes the view that these are simply short-term versions of pump-and-dump, despite the fact that no execution actually occurred. If Panther had executed wash trades through separate accounts, giving rise to actual volume, they would have a better case for this … but with pump-and-dump, I also take the view that the law is merely molly-coddling of incompetent fools. If 21.50 is too much to pay for XZY stock … then don’t buy XZY at 21.50. It’s as simple as that.

I cancelled an order today within one minute of placing it. I’ll use fake numbers to illustrate: there was a bid for 500 shares at 21.50; the next bid was at 21.40. The offer was at about 21.60. I wanted to sell 1,000 shares and I thought 21.50 was a good price, so I hit the bid and got done for 500, which left me on the offer side of the market. But the offer behind me was at 21.60! Why should I improve the quote – using client money – by ten cents? So I modified the offer on the 500 shares remaining on my order to 21.58. Selling at 21.50 was good, but selling at 21.58 would be better. Selling at 21.50 with execution certainty is one thing; offering the entire world an option to buy them at 21.50 is another.

I don’t understand why you want to jail me for that.

It should also be noted that although Nanex is a firm I respect – they did excellent work on the Flash Crash – their conclusions regarding algorithmic behaviour have been challenged:

Nanex regularly misunderstands what it sees in market data and is fueling misconceptions that damage investor confidence, according to Manoj Narang, founder and chief executive officer of HFT firm Tradeworx Inc. in Red Bank, New Jersey. He compared Nanex to the “truthers” who doubt the official explanation of the Sept. 11 terrorist attacks.

There are usually benign explanations for what look to Nanex like attempts to manipulate prices through what it calls “quote stuffing,” he said. For example, he said, bursts of quotes could be trading algorithms reacting when the difference between the best bid to buy and the best offer to sell grows to more than a penny. The programs automatically cancel the orders after exchanges modify them to avoid markets where bids equal offers, according to Narang, resulting in “inadvertent repetitive behavior” by algorithms.

Assiduous Reader PL’s support for a Tobin Tax is one that keeps resurfacing like a lump of decomposing sewage:

Still, proponents of stricter regulation said they see the debate over the [Michael Lewis] book [Flash Boys] as a catalyst for possible future changes.

“The simplest approach and most direct approach is with a transaction tax,” said [ Democrat Representative Peter ] DeFazio, whose legislation would impose what he described as a “miniscule” 3-basis-point levy on the sell side of transactions.

However, it is quite apparent that Tobin taxes harm market quality. One possibility where the AR PL and I might have a meeting of minds is the potential for an exchange to impose a fee for the placement of an order – generally, once you’re permitted to place orders on the exchange, the only fees remaining are charged for executed transactions.

Schwab is upset about the number of orders:

High-frequency trading pumped out over 300,000 trade inquiries each second last year, up from just 50,000 only seven years earlier. Yet actual trade volume on the exchanges has remained relatively flat over that period. It’s an explosion of head-fake ephemeral orders – not to lock in real trades, but to skim pennies off the public markets by the billions.

…

Added systems burdens, costs and distortions of rapid-fire quote activity: Ephemeral quotes, also called “quote stuffing,” that are cancelled and reposted in milliseconds distort the tape and present risk to the resiliency and integrity of critical market data and trading infrastructure. The tremendous added costs associated with the expanded capacity and bandwidth necessary to support this added data traffic is ultimately borne in part by individual investors.

There are solutions. Today there is no restriction to pumping out millions of orders in a matter of seconds, only to reverse the majority of them. It’s the life-blood of high-frequency trading. A simple solution would be to establish cancellation fees to discourage the practice of quote stuffing. The SEC and CFTC floated the idea last year. It has great merit. Make the fees high enough and they will eliminate high-frequency trading entirely.

However, I would support a charge for order entry (or simply order cancellation, assuming that executed orders get charged by other means) only to the extent that it is imposed by the exchanges to recover costs or as a source of competitive advantage. If, once you count amortization of all the required infrastructure, it costs $1 to process 1,000,000 orders, then by all means, charge $0.000001 to process an order. If you want to make a profit and the market will bear it, then by all means, charge $0.000002 to process an order. If your customers complain that they have to process all these orders too, then by all means offer them a kiddie feed at reduced price, transmitting orders only when they have been extant for 10 milliseconds.

But don’t start imposing fees with grandiose visions of Better Living Through Higher Taxation. We all know where that ends up.

In fact, I have learned from a paper by Charles M. Jones of Columbia Business School titled What do we know about high-frequency trading? that:

Order cancellation or excess message fees: If bandwidth and data processing requirements are overwhelming some trading venue customers, it may be appropriate for trading venues to set prices accordingly and charge the participants who are imposing those costs on others. Nasdaq is currently imposing these fees in the U.S.; it is too soon to measure the effects. However, order cancellation fees will almost certainly reduce liquidity provision away from the inside quote, reducing market depth. The current initiatives should be studied carefully before broader-based message fees are considered.

He also points out – bless the man – that:

Minimum order exposure times: Under these proposals, submitted orders could not be cancelled for at least some period of time, perhaps 50 milliseconds. This would force large changes in equity markets and could severely discourage liquidity provision. The economic rationale here is particularly suspect, as the overriding goal in market design should be to encourage liquidity provision.

Securities transaction taxes: The evidence indicates that these taxes reduce share prices, increase volatility, reduce price efficiency, worsen liquidity, increase trading costs, and cause trading to move offshore.

At the cost of severe personal trauma – which I hope you guys appreciate – I have actually gone to the extent of watching a video titled ‘Michael Lewis: Programmers have Replaced Traders’. My God, but I hate watching TV and listening to lectures! Anyway, the video makes it plain that the big thing that is really at issue is the replacement of the old time smiley-boys by geeks who can actually do things, like programme these here computer whatchamacallits. Brad Katsuyama, who was discussed on PrefBlog on April 2, was on it … just another smiley boy, having his lunch eaten by people who know what they’re doing. Yawn.

Meanwhile, Schneiderman wrote an op-ed for the Daily News titled The need for speed is costing billions:

Some high-frequency trading firms engage in a practice called “latency arbitrage” — a technical euphemism that hides a threat to the integrity of our markets.

This is what we should be talking about. This is what I am investigating.

Put simply, latency arbitrage describes the trading strategy whereby high-frequency traders gain access to market prices before regular investors.

Armed with what amounts to knowledge of the future, these traders execute tens of thousands of trades in milliseconds with essentially zero risk — driving up the cost for other purchasers of stock.

Here is how it works: When traditional investors buy or sell stocks, they often use what’s called the “consolidated feed” to gather market data and determine the best bid or offer in the nation. This is particularly so in private trading venues, where regular investors like pension funds often trade.

Because high-frequency trading firms receive market prices before traders relying on the consolidated feed, they are able to see the prices early, jump in and take the best one in the blink of an eye. Regular investors are left in the dark.

Well, BooHooHoo. OK, Schneiderman, make it a law that the only market data feed allowed is the Schneiderman Consolidated Feed. Fine. I’ll co-locate with the feed provider. If that’s illegal, I’ll rent a room across the street. You’re in an argument with physics here and you ain’t gonna win.

He goes on:

That is also why I am calling for market reforms like the one put forward by experts at the University of Chicago.

He is referring to frequent batch auctions, which were discussed on PrefBlog on March 19. It was also given a brief mention in the CFTC Concept Release on Risk Controls and System Safeguards for Automated Trading Environments, which also asked a question dear to Assiduous Reader PL’s heart:

96. Should exchanges impose a minimum time period for which orders must remain on the order book before they can be withdrawn? If so, should this minimum resting time requirement apply to orders of all sizes or be restricted to orders smaller than a specific threshold? If there should be a specific threshold, how should that threshold be determined?

…

99. Would batched order processing increase the number of milliseconds that are necessary for correlations among related securities to be established? If so, what specific costs would result from this change and how do those costs compare to the potential benefits described in recent research?

The comment period on this concept release was extended to Valentine’s Day; fifty-seven comments have been published on the CFTC website. I simply do not have time to comb through all these things, especially since it would seem that this is viewed as simply a preliminary skirmish in a long war, but I did read a comment by Thomas McCabe of One Chicago LLC:

Market participants should be free to enter, cancel, or cancel/replace their orders at will, as they assume the risk of execution or non-execution. Exchanges are in a unique position to understand the strain on their systems caused by orders and should be allowed to independently govern throughput into those systems. Accordingly, we oppose the Commission mandating that exchanges impose minimum time periods for orders.

Well, yeah. I looked around a bit for critiques of batched order processing and found one on a blog by somebody claiming to have a good resume. The post is titled Beware Discrete Auctions:

But, I was intrigued by the idea of batch auctions, because I’ve heard people who think discrete auctions are better than continuous ones. I think they are not very good, and a simple example is an extreme of this, one can look at the performance of closing vs. opening prices. One is at the end of continuous trading, one where there’s no trading. What happens?

Well, I looked at over 1000 stocks, from 2000 to today. I excluded really small, low-priced stocks. The Open-Open returns have slightly higher volatility (2% higher), but more importantly, there’s a lot more ‘mean reversion’. The graph below shows the future returns(O-O or C-C), sorted each day into deciles by the immediate prior return (O-O or C-C, respectively), then averaged over all those days.

Basically, markets open at extremes that are quickly erased, allowing the market makers to pocket nice premiums for these temporary imbalances (you can’t make money off this if you aren’t a specialist). Continuous trading takes such trades away from monopolists, and allows competition to work.

Click for Big

Click for Big… and a comment to that post …

Our U Chicago Colleagues are delusional: They are trying to solve a problem that doesn’t exist.

People just need to stop using “market” orders. Would you buy a house on the “market” price, by telling your Realtor that you’ll agree to ANY price the seller wants? Probably not. And there’s no reason to do that with stocks either.

Of course, one reason to use market trades is because the trader is too lazy to figure out limits. In that case, the trader pays for that convenience.

Regarding “clogging bandwidth” there is no evidence that flash orders are causing dissarray in the exchange. Even if they were, that would just be a technical issue of the exchange, and should be handled like any DOS attack.

Third, their solution won’t work. Batching by 1 second would lead to people timing the system, and figuring out how do direct orders into one auction or another to optimize trading. It would actually add complexity into the market that would give an advantage to the HFTs. The authors should try their proposed solution at Kovler Cafe, and see if it makes getting lunch more orderly.

One problem I see with batched processing is swap orders – or paired orders that have that intent. Say I want to sell A and buy B. In such a case, when I get one side filled, I want to execute the other as quickly as possible, so I can make or exceed my spread target. Batching interferes with that.

Another problem is when I’m spending or raising X dollars on behalf of a client. If I am a good little Portfolio Manager, genuinely trying to do the best for my client, I’ll put in a bunch of orders totalling (say) 2X. As some get filled, I’ll cancel others and – with no more than average luck – be able to raise or spend X dollars at good prices on the market. Again, batched processing will make that cancellation process a bit more chancy, causing me to reduce my over-ordering, reducing liquidity in the market place and making real-money trading more expensive.

Yet another problem is for dealers executing crosses, which may or may not be contingent on other stuff (e.g., pairs trades and, in the futures market, exchange for physicals). At present, there is a quote with a spread in continuous time, with executions in discrete time; therefore, there will always be a quote and the cross can be executed anywhere inside that quote. With batching, there’s the potential for the market to be locked at inconvenient prices for lengthy periods; another obstacle to trading by real-money traders.

The Australians had this to say about latency arbitrage:

We do not regard the fact that market participants can co-locate to obtain a speed advantage as inherently unfair. Speed of access to the market has always been contestable, from the days of physical proximity on the floor, when an open outcry system operated. We recognise that not all market operators choose to operate at the co-location site with the lowest latency, but for those who do, our concern is to ensure that the facilities for doing so are made available to them on a fair basis and on transparent terms.

Our assessment is that access to these services is fair. Market operators offer economically reasonable and transparent pricing, inclusive of ongoing fee costs, that is publicly available and access to these services is available on a non-discriminatory basis. Network connections within co-location facilities are precisely measured, and all participants within the facility receive their data feed with exactly the same latency as any other participant running the same options.

…

However, market operators are required to provide market data on a fair, transparent and non-discriminatory basis. No trader is capable of detecting any submitted market message before acceptance by that operator. Many of the complaints about latency received and reviewed by ASIC appear to arise from the complainants’ misunderstanding of participant SORs.

390 Many market participants will find that the routing options and time taken by their SORs to break, and route, orders between operators is considerably longer than the reaction times of many highly automated traders. If this happens they may find that when an order reaches market A and, before the related order reaches market B, another system has generated an order for market B possibly in response to the order on market A. Market participants need to take this factor into account when programming decision logic for their SORs.

… but the Australians don’t like market rebates:

We have previously stated (e.g. in Report 237 Response to submissions on Consultation Paper 145 Australian equity market structure: Proposals (REP 237) and CP 168) that we would be concerned if pricing incentives influence behaviour in a way that is not in the best interests of clients and wider market integrity. We believe there is sufficient evidence to conclude that maker–taker models, where the market operator pays a rebate, do not promote market quality or market integrity.

Intriugingly:

Another sign of Australia’s success in limiting HFT is that fewer orders go unfilled due to a charge on orders. High-frequency strategies are usually defined by the use of computers to post and cancel orders in times measured in thousandths and even millionths of seconds. In the six years through the end of 2013, the average order-to-trade ratio in Australia was 4.2, less than half that of the NYSE, according to data compiled by Sydney-based research firm Capital Markets CRC Ltd.

I can’t find any more information on that.

So, Assiduous Reader PL, my conclusion is: You are being manipulated by the Smiley-Boys. Cancellations and resting times are simply not an issue to real money fundamental traders.

There is widespread frustration over Canada’s inadequate housing data:

The issue came to the forefront Thursday after Canadian Imperial Bank of Commerce economist Benjamin Tal released a strongly worded note, titled “Flying Blind,” in which he said “the gap between the importance of the real estate market to the economy and the lack of publicly available information on it is mind-boggling.”

His laundry list of information that’s missing includes the share of foreign investors in the condominium market, the distribution of mortgages by credit score and the average down-payment.

…

“It would be useful to have more information about personal debt and the mortgage market,” says Toronto-Dominion Bank chief economist Craig Alexander. “If we think that Canada has a problem with excessive personal debt, you need the data to actually assess the vulnerability and what the associated risks are. But the reality is we actually have quite limited information.”

…

“Because there is a bit of a void on housing data we do have a lot of ill-considered opinions on the real estate market, and it’s hard to completely refute some of the wild talk we’ve had in recent years because the data set is limited,” says BMO Nesbitt Burns chief economist Douglas Porter.

He cautions, however, that more information is not a panacea. Deeper U.S. data did not prevent a housing boom and crash in that country.

I think a good first step would be for the Bank of Canada to stop lying about 5-year mortgage rates, but I’m just a grouch.

Great-West Lifeco has announced a deal:

Great-West Lifeco Inc. today announced that its U.S. subsidiary Great-West Financial® has reached an agreement to acquire the J.P. Morgan Retirement Plan Services large-market recordkeeping business. Upon completion of the acquisition, Great-West Financial will become the second-largest retirement services provider by participants in the U.S. defined contribution market, with nearly 6.8 million participants and US$387 billion in recordkeeping assets. Terms of the transaction were not disclosed.

The J.P. Morgan Retirement Plan Services business comprises 200 clients with approximately 1.9 million participants and US$167 billion in retirement plan assets. As part of the transaction more than 1,000 staff and management affiliated with J.P. Morgan Retirement Plan Services will join Great-West Financial.

The transaction is scheduled to close in the third quarter of 2014, subject to regulatory approval in the U.S.

Jacqueline Nelson of the Globe reports:

“Great-West’s business has been more focused on the small to mid-sized market, so the JP Morgan transaction is highly complementary,” Mr. [Paul] Mahon [chief executive officer of Great-West Lifeco] said. The large market is classified as defined-contribution plans with more than $25-million (U.S.) in assets under administration, wrote analyst Peter Routledge. But JP Morgan’s plans are far larger, with average assets of $835-million, he noted.

Being in the larger market is helpful for two reasons, Mr. Mahon said. First, it lends credibility that a company can do business with the Fortune 100 employers. JP Morgan is the largest bank in the U.S. by assets, so it’s brand name has carried far with clients. If the deal boosts Great-West’s profile in the U.S. it could help the company sell other major products, such as asset management services and insurance products.

Second, and even more importantly to Mr. Mahon, different sized corporations have different requirements from plan managers. Large corporations often demand greater flexibility and technology capabilities. The acquisition allows Great-West to offer some of those advanced systems to its smaller clients.

DBRS comments:

DBRS views the transaction as a positive development and consistent with the Company’s strategy to grow its U.S. retirement services businesses. There are no changes to the ratings.

…

There is some integration risk given the very large size of these DC plans. It will be important for GWF to manage client retention well. However, switching plan record keepers is costly and time consuming for plan sponsors, so there would need to be a very significant inducement, be it positive or negative, for a plan departure to occur. DBRS views favourably the potential for incremental profits and future product placement synergies with the rest of the Company and views the financial impact of this acquisition as diminutive compared to the overall size of GWL’s balance sheet.

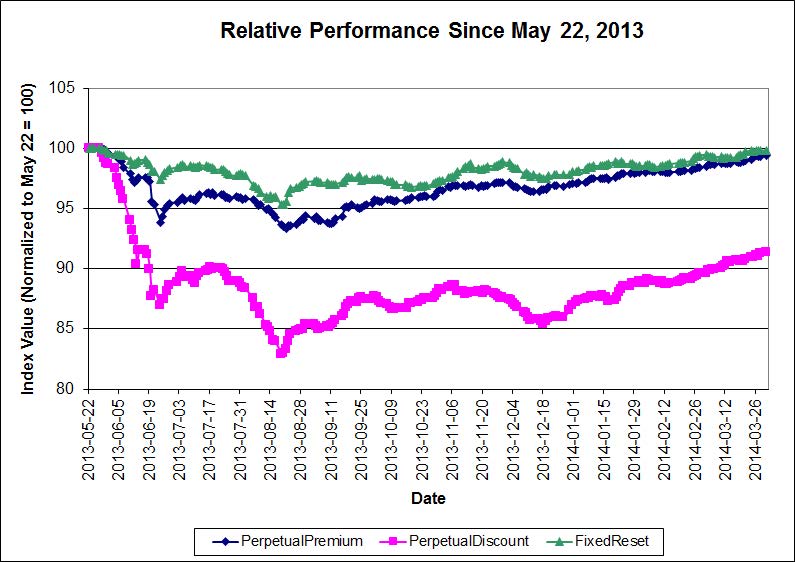

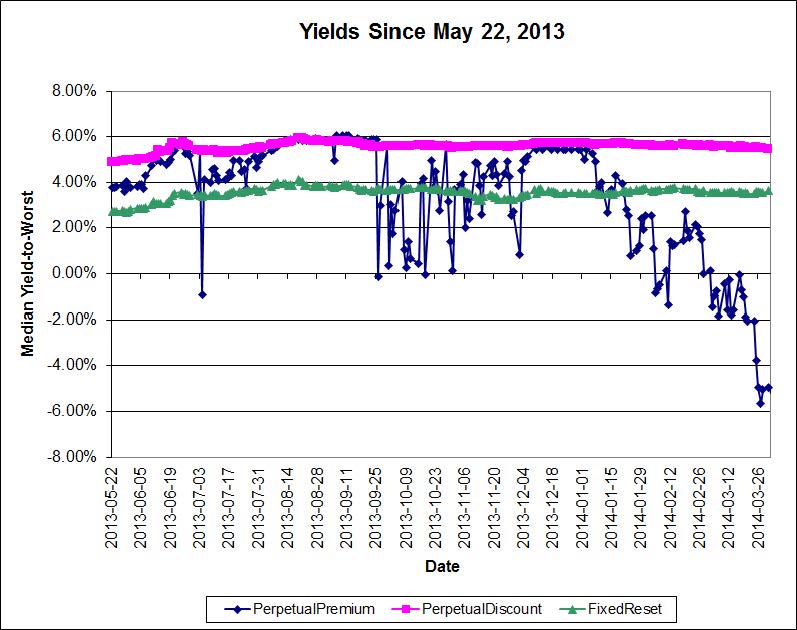

It was a good day for the Canadian preferred share market, with PerpetualDiscounts winning 16bp, FixedResets gaining 4bp and DeemedRetractibles up 7bp. Volatility was minimal. Volume was very low.

HIMIPref™ Preferred Indices

These values reflect the December 2008 revision of the HIMIPref™ Indices

Values are provisional and are finalized monthly |

| Index |

Mean

Current

Yield

(at bid) |

Median

YTW |

Median

Average

Trading

Value |

Median

Mod Dur

(YTW) |

Issues |

Day’s Perf. |

Index Value |

| Ratchet |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.3794 % |

2,475.6 |

| FixedFloater |

4.69 % |

4.30 % |

36,824 |

17.71 |

1 |

-0.0987 % |

3,615.6 |

| Floater |

2.94 % |

3.05 % |

50,373 |

19.63 |

4 |

0.3794 % |

2,673.0 |

| OpRet |

4.64 % |

-0.96 % |

103,093 |

0.21 |

3 |

0.1033 % |

2,691.1 |

| SplitShare |

4.81 % |

4.25 % |

65,274 |

4.27 |

5 |

-0.0953 % |

3,086.1 |

| Interest-Bearing |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.1033 % |

2,460.7 |

| Perpetual-Premium |

5.54 % |

-1.58 % |

104,199 |

0.09 |

13 |

0.0423 % |

2,374.6 |

| Perpetual-Discount |

5.44 % |

5.47 % |

124,550 |

14.61 |

23 |

0.1599 % |

2,469.6 |

| FixedReset |

4.69 % |

3.64 % |

215,566 |

4.31 |

79 |

0.0389 % |

2,521.0 |

| Deemed-Retractible |

5.04 % |

1.15 % |

151,472 |

0.16 |

42 |

0.0663 % |

2,480.7 |

| FloatingReset |

2.63 % |

2.49 % |

188,977 |

4.30 |

5 |

0.1763 % |

2,459.9 |

| Performance Highlights |

| Issue |

Index |

Change |

Notes |

| PWF.PR.A |

Floater |

1.28 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2044-04-03

Maturity Price : 19.85

Evaluated at bid price : 19.85

Bid-YTW : 2.66 % |

| PWF.PR.P |

FixedReset |

1.28 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2044-04-03

Maturity Price : 23.39

Evaluated at bid price : 23.75

Bid-YTW : 3.63 % |

| Volume Highlights |

| Issue |

Index |

Shares

Traded |

Notes |

| NA.PR.S |

FixedReset |

133,248 |

Scotia crossed 100,000 at 25.39.

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2019-05-15

Maturity Price : 25.00

Evaluated at bid price : 25.49

Bid-YTW : 3.82 % |

| BNS.PR.A |

FloatingReset |

122,000 |

Nesbitt crossed 115,000 at 25.26.

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2018-04-25

Maturity Price : 25.00

Evaluated at bid price : 25.29

Bid-YTW : 2.43 % |

| BMO.PR.L |

Deemed-Retractible |

98,323 |

RBC crossed 69,600 at 26.40; Scotia crossed 25,000 at the same price.

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2014-05-25

Maturity Price : 25.75

Evaluated at bid price : 26.39

Bid-YTW : -7.53 % |

| TRP.PR.E |

FixedReset |

97,350 |

Scotia crossed blocks of 40,000 and 50,000 shares, both at 25.30.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2044-04-03

Maturity Price : 23.20

Evaluated at bid price : 25.21

Bid-YTW : 3.94 % |

| ENB.PF.A |

FixedReset |

78,020 |

Recent new issue.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2044-04-03

Maturity Price : 23.19

Evaluated at bid price : 25.21

Bid-YTW : 4.25 % |

| TRP.PR.A |

FixedReset |

57,720 |

TD crossed 50,000 at 22.45.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2044-04-03

Maturity Price : 22.71

Evaluated at bid price : 23.33

Bid-YTW : 3.89 % |

| There were 18 other index-included issues trading in excess of 10,000 shares. |

| Wide Spread Highlights |

| Issue |

Index |

Quote Data and Yield Notes |

| BAM.PR.T |

FixedReset |

Quote: 24.06 – 24.42

Spot Rate : 0.3600

Average : 0.2161

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2044-04-03

Maturity Price : 23.00

Evaluated at bid price : 24.06

Bid-YTW : 4.20 % |

| CU.PR.G |

Perpetual-Discount |

Quote: 21.70 – 21.98

Spot Rate : 0.2800

Average : 0.1688

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2044-04-03

Maturity Price : 21.38

Evaluated at bid price : 21.70

Bid-YTW : 5.23 % |

| HSB.PR.D |

Deemed-Retractible |

Quote: 25.27 – 25.51

Spot Rate : 0.2400

Average : 0.1545

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2014-12-31

Maturity Price : 25.00

Evaluated at bid price : 25.27

Bid-YTW : 3.57 % |

| BNS.PR.Q |

FixedReset |

Quote: 25.30 – 25.54

Spot Rate : 0.2400

Average : 0.1564

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2018-10-25

Maturity Price : 25.00

Evaluated at bid price : 25.30

Bid-YTW : 3.28 % |

| GWO.PR.G |

Deemed-Retractible |

Quote: 24.33 – 24.57

Spot Rate : 0.2400

Average : 0.1648

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 24.33

Bid-YTW : 5.57 % |

| RY.PR.A |

Deemed-Retractible |

Quote: 25.65 – 25.85

Spot Rate : 0.2000

Average : 0.1506

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2014-05-24

Maturity Price : 25.25

Evaluated at bid price : 25.65

Bid-YTW : -3.58 % |