The latest hot new financial indicator is: How much European sovereign debt trades at negative yields?:

The European Central Bank’s imminent bond-buying plan has left $1.9 trillion of the euro region’s government securities with negative yields.

Germany sold five-year notes at an average yield of minus 0.08 percent on Wednesday, a euro-area record, meaning investors buying the securities will get less back than they paid when the debt matures in April 2020.

By the next day, German notes with a maturity out to seven years had sub-zero yields, while rates on seven other euro-area nations’ debt were also negative. While some bonds had such yields as far back as 2012, the phenomenon has gathered pace since the ECB’s decision to cut its deposit rate to below zero last year.

And there are more global rate cuts:

The dollar rallied with gold as the yuan slipped to a two-year low after China cut interest rates for the second time in three months. Oil retreated following its first monthly gain since June.

The Bloomberg Dollar Spot Index increased 0.2 percent at 1:22 p.m. in Hong Kong as China’s currency traded at its weakest level since October 2012 and the euro slipped 0.2 percent.

…

China’s second rate cut in 14 weeks was the latest in a wave of global easing that underscores diverging economic outlooks for the U.S. versus the rest of the world. A private measure of factory activity in Asia’s largest economy showed a faster-than-estimated expansion Monday as lawmakers prepare to meet in Beijing. The euro area updates on consumer prices and U.S. private spending data are due.

…

The People’s Bank of China announced a benchmark lending and deposit rate cut of a quarter percentage point Saturday. A day later, a government factory gauge for February signaled contraction for a second month, underscoring the scope for looser policy.The yuan traded at 6.2732 per dollar after the central bank reduced its reference rate to the weakest since November today. Today’s purchasing managers index from HSBC Holdings Plc and Markit Economics came in at 50.7, beating economists’ estimates for it to hold steady from a preliminary reading of 50.1. Readings above 50 denote expansion.

The Bloomberg gauge of dollar strength traded at 1,174.11, less than one point from its highest level in at least 10 years. The greenback was stronger against 13 of 16 major peers, advancing 0.5 percent against the Australian and New Zealand currencies. The euro bought $1.1179.

There are more worries about corporate bond liquidity:

Investors have a fickle relationship with credit mutual funds lately, pouring cash in one year and yanking it out the next.

As a result, the world’s biggest mutual-fund firms are preparing for when sentiment sours for a prolonged period. They’re increasing the amount of cash in their portfolio and boosting their holdings of corporate-bond exchange-traded fund shares — which trade like stocks instead of the antiquated, telephone-based system of buying and selling debt.

…

Up to 10 percent of some corporate-debt funds’ holdings now consist of ETFs, a proportion that’s been rising for the past two years, according to Tabb Group research.

…

The potential for big outflows from U.S. bonds is all the scarier now because trading volumes have failed to keep pace with the 21 percent growth in outstanding debt since 2007. While taxable bond funds have received $932 billion of deposits since the end of 2007, Wall Street’s biggest banks have cut holdings of the debt previously used to facilitate trading.“There has, indeed, been a meaningful deterioration in the ability to trade corporate bonds from the pre- to post-crisis period,” Barclays Plc analysts led by Jeffrey Meli and Bradley Rogoff wrote in a Feb. 27 report. “This has resulted in increased investor reliance on products such as ETFs” to manage liquidity.

…

Of course, there are some questions about how well ETFs will work as a liquidity tool in a downturn, too. There’s the potential for ETF shares to move away from the underlying market in a time of stress, forcing fire sales of assets that don’t trade as often.The fragile new equilibrium stems from “liquidity mismatches between the assets themselves and the instruments being used to manage daily liquidity needs,” Barclays analysts wrote. Well-intentioned regulations and “a growing demand for liquidity may have led to increased instability and fire-sale risk in corporate debt markets.”

This has even attracted the attention of one of the well-intentioned regulators:

A lack of liquidity in corporate-bond markets could pose a “systemic risk” to the economy when interest rates rise, U.S. Securities and Exchange Commission member Daniel Gallagher said.

Gallagher, a Republican, warned that the Financial Stability Oversight Council, a group of U.S. regulators that monitors emerging systemic risks, hasn’t paid enough attention to the $7.3 trillion corporate-bond market, which has ballooned over the past seven years amid low interest rates. He made the remarks Monday at a banking conference in Washington.

The SEC last year began testing whether fixed-income mutual funds could withstand a possible sell-off during a period of financial stress, people with knowledge of the matter have said. The agency hasn’t made its findings public, but some large money managers have warned the market is primed for failure when the Federal Reserve starts raising interest rates.

I’ve said it before … I’ll say it again … it’s one thing to say that the banks’ pool of capital may not be used to inventory corporates, but that pool has to be replaced. The logical replacement source is hedge funds, pension funds and insurance companies starting to act as traders but – given that fantasies of creating liquidity through exchange-like electronic marketplaces is nothing more than the psychedelic dream of morons with no knowledge of the market whatsoever – that means they’ll have to have SEC clearance to act as traders. That is, with a Salesforce (that’s expensive!) and no moronic whimpering about fairness to clients. I’m not going to hold my breath. Instead, I’ll continue to be fearful of what will happen when what happened to sub-prime paper during the Credit Crunch happens to corporate debt in the next crisis, which will kill the market for a few years and do massive damage to the economy. There might be a few bargains, though, for those with dry ammunition and permission from our wise masters at the regulatory agencies to invest in fire-sale corporate debt.

Ian McGugan in the Globe writes a piece titled Why decades of inflationary pressure may be ahead of us which drew my attention to a BIS working paper by Mikael Juselius and Elod Takats titled Can Demography Affect Inflation and Monetary Policy?:

Several countries are concurrently experiencing historically low inflation rates and ageing populations. Is there a connection, as recently suggested by some senior central bankers? We undertake a comprehensive test of this hypothesis in a panel of 22 countries over the 1955-2010 period. We find a stable and significant correlation between demography and low-frequency inflation. In particular, a larger share of dependents (ie young and old) is correlated with higher inflation, while a larger share of working age cohorts is correlated with lower inflation. The results are robust to different country samples, time periods, control variables and estimation techniques. We also find a significant, albeit unstable, relationship between demography and monetary policy.

…

Given these developments, some senior central bankers have suggested an alternative to the “pure mistake” view, arguing that low-frequency inflation may be linked to demographic change. Governor Shirakawa of the Bank of Japan (2011a, 2011b, 2012 and 2013) has argued that population ageing can lead to deflationary pressures by lowering expectations of future economic growth. While people might ignore the implications of an ageing population for a while, they revise their expectations when they recognise the extent of the economic impact. The resulting loss of demand and investment might not be easily offset by monetary policy, especially if inflation is already low and policy rates are close to the zero lower bound. President Bullard of the St Louis Federal Reserve Bank has suggested a different explanation focusing on the political economy of central banking. Bullard et al (2012) argue that the old might prefer lower inflation than the young due to the redistributive effects of inflation. Thus, to the degree their policies reflect voter preference, central banks might engineer lower inflation when populations age.The potential connection between demography and inflation has also sparked interest from researchers at policy institutions such as the International Monetary Fund. Motivated by the experience of Japan, for example, Anderson et al (2014) find that ageing causes deflationary pressures, mainly via slowing growth. Imam (2013) finds that it can weaken monetary transmission. Yoon et al (2014) find, based on a panel regression, that ageing is deflationary.

…

According to our estimates, demography accounts for around one-third of the variation in inflation and for the bulk of the deceleration between the late 1970s and early 1990s. Furthermore, our estimates reveal a stable U-shaped pattern: a larger share of dependents (ie young and old) is correlated with higher inflation, and a larger share of working age cohorts is correlated with lower inflation.

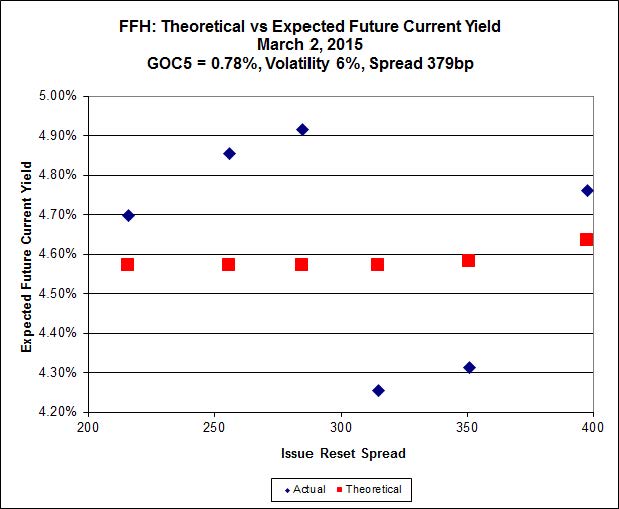

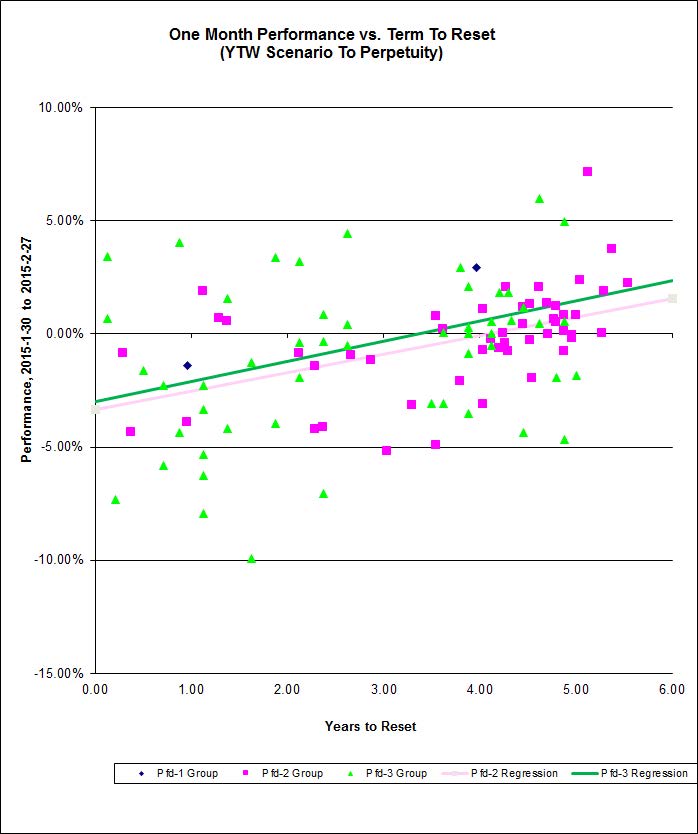

It was a mixed day for the Canadian preferred share market, with PerpetualDiscounts off 6bp, FixedResets up 43bp and DeemedRetractibles gaining 1bp. There is a lengthy Performance Highlights table, suitably dominated by winning FixedResets. Volume was very high.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

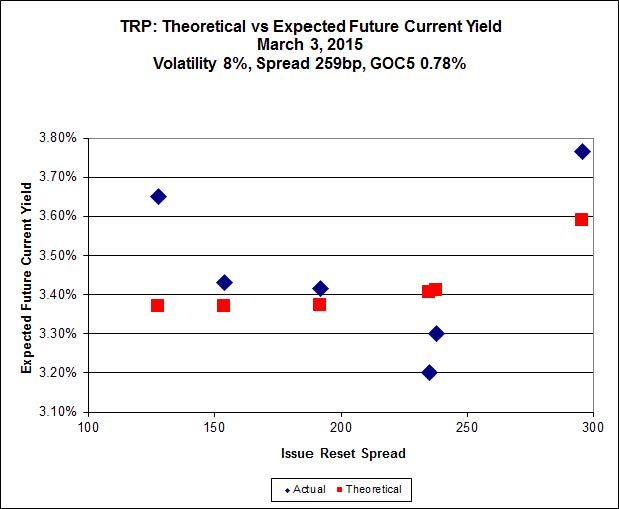

Here’s TRP:

Click for Big

The new issue, TRP.PR.G has caused a large change in the curve-fitting for the TRP series of FixedResets. TRP.PR.E, which resets 2019-10-30 at +235, is bid at 24.44 to be $1.47 rich, while TRP.PR.G, resetting 2020-11-30 at +296, is $1.22 cheap at its bid price of 24.83.

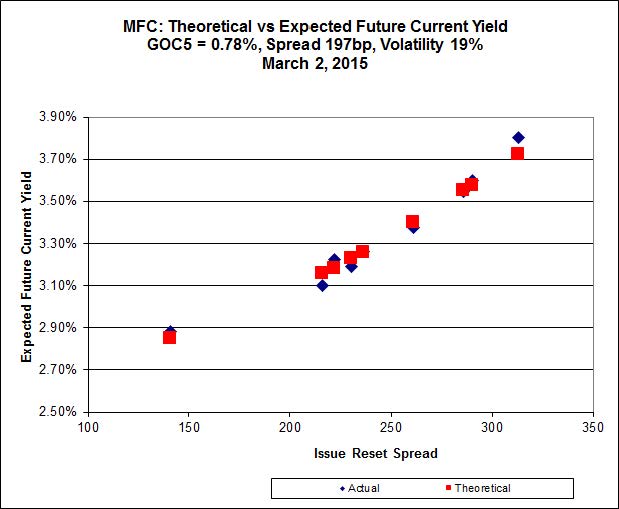

Click for Big

Another excellent fit, but the numbers are perplexing. Implied Volatility for MFC continues to be a conundrum, although it declined substantially today. It is still too high if we consider that NVCC rules will never apply to these issues; it is still too low if we consider them to be NVCC non-compliant issues (and therefore with Deemed Maturities in the call schedule).

Most expensive is MFC.PR.L, resetting at +216 on 2019-6-19, bid at 23.70 to be $0.42 rich, while MFC.PR.H, resetting at +313bp on 2017-3-19, is bid at 25.71 to be $0.56 cheap.

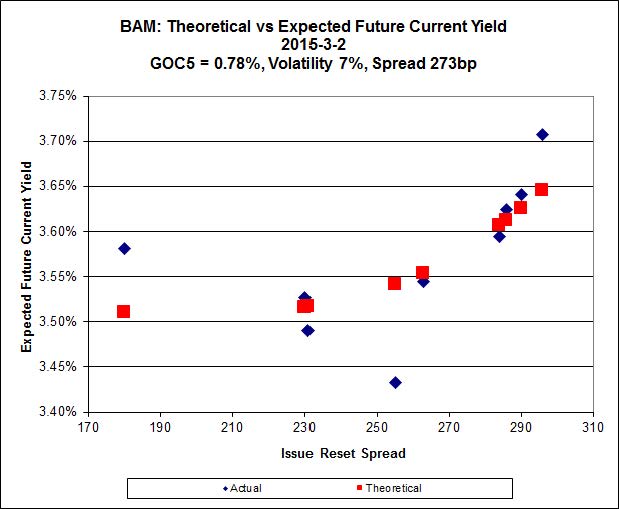

Click for Big

The fit on this series is actually quite reasonable – it’s the scale that makes it look so weird.

The cheapest issue relative to its peers is BAM.PR.Z, resetting at +296bp on 2017-12-31, bid at 25.22 to be $0.43 cheap. BAM.PF.E, resetting at +255bp 2020-3-31 is bid at 24.25 and appears to be $0.74 rich.

Click for Big

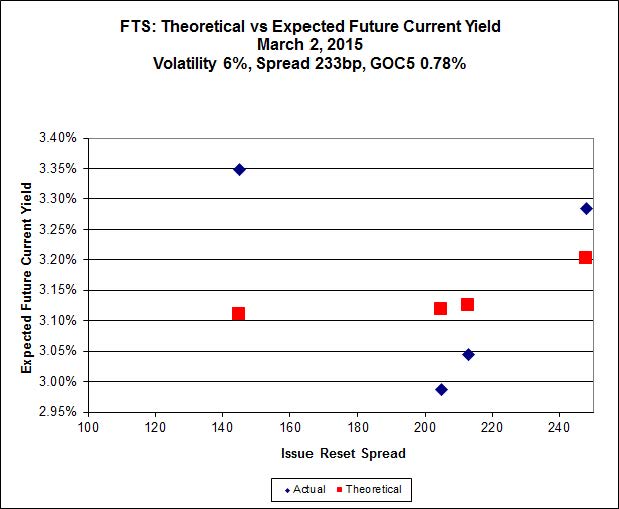

This is just weird because the middle is expensive and the ends are cheap but anyway … FTS.PR.H, with a spread of +145bp, and bid at 16.65, looks $1.28 cheap and resets 2015-6-1. FTS.PR.K, with a spread of +205bp and resetting 2019-3-1, is bid at 23.68 and is $0.99 rich.

Click for Big

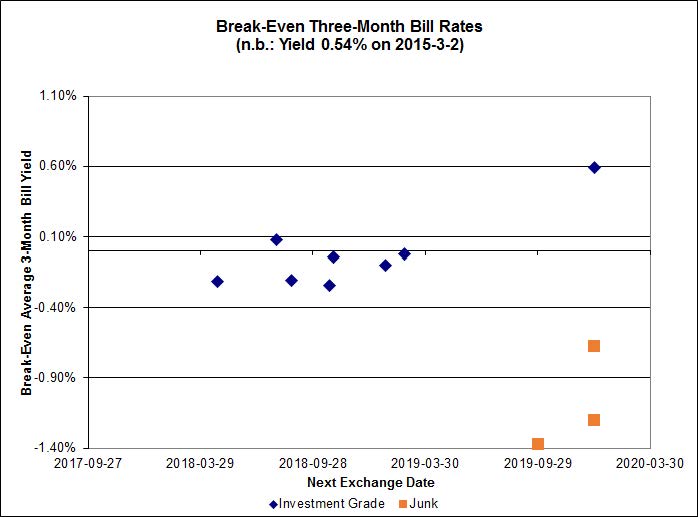

The investment grade break-even rates average close to zero.

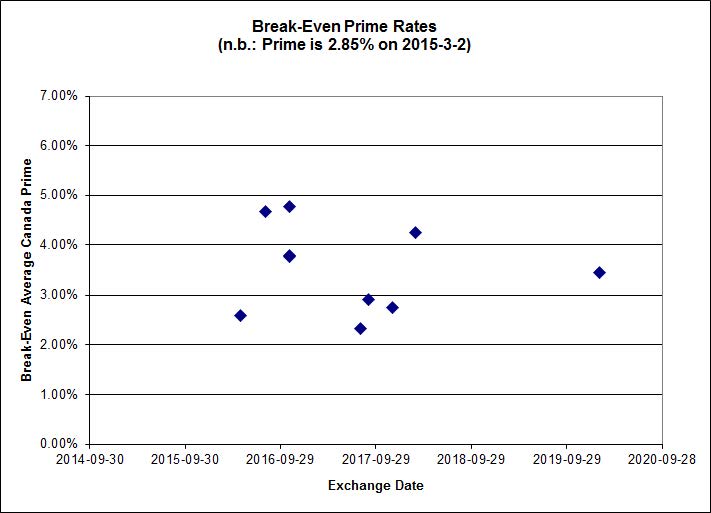

On the other hand, the market’s distaste for product linked to Money Market rates does not extend to prime, as shown by the FixedFloater/RatchetRate pairs:

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 1.9210 % | 2,346.9 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 1.9210 % | 4,103.4 |

| Floater | 3.20 % | 3.25 % | 78,183 | 19.05 | 3 | 1.9210 % | 2,494.9 |

| OpRet | 4.08 % | 1.98 % | 112,355 | 0.30 | 1 | -0.0398 % | 2,756.0 |

| SplitShare | 4.47 % | 4.58 % | 53,344 | 4.49 | 5 | -0.0239 % | 3,211.0 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0398 % | 2,520.1 |

| Perpetual-Premium | 5.30 % | -1.19 % | 56,512 | 0.08 | 25 | 0.0141 % | 2,516.6 |

| Perpetual-Discount | 4.97 % | 5.06 % | 146,066 | 15.33 | 9 | -0.0558 % | 2,801.3 |

| FixedReset | 4.44 % | 3.53 % | 233,061 | 16.91 | 80 | 0.4292 % | 2,413.2 |

| Deemed-Retractible | 4.93 % | 0.07 % | 101,561 | 0.16 | 39 | 0.0142 % | 2,651.9 |

| FloatingReset | 2.50 % | 2.90 % | 89,933 | 6.35 | 8 | 0.3219 % | 2,334.2 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| CIU.PR.C | FixedReset | -5.78 % | Not real: this is simply another example either of the Exchange’s shoddy reporting or their inability to enforce market-making responsibilities. The day’s low was 16.78, VWAP was 16.90. Volume was 1,156 shares (consolidated exchanges), which probably overwhelmed the systems, poor little dears, on nine trades including four odd lots. A fine way to welcome CIU.PR.C on the first day of its return from the Scraps index, where it had been relegated on volume concerns! YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-02 Maturity Price : 15.97 Evaluated at bid price : 15.97 Bid-YTW : 3.49 % |

| VNR.PR.A | FixedReset | -1.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-02 Maturity Price : 23.04 Evaluated at bid price : 24.01 Bid-YTW : 3.81 % |

| ENB.PR.D | FixedReset | 1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-02 Maturity Price : 19.25 Evaluated at bid price : 19.25 Bid-YTW : 4.27 % |

| HSE.PR.A | FixedReset | 1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-02 Maturity Price : 17.75 Evaluated at bid price : 17.75 Bid-YTW : 3.73 % |

| TRP.PR.C | FixedReset | 1.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-02 Maturity Price : 16.90 Evaluated at bid price : 16.90 Bid-YTW : 3.58 % |

| PWF.PR.T | FixedReset | 1.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-02 Maturity Price : 23.26 Evaluated at bid price : 25.00 Bid-YTW : 3.22 % |

| BNS.PR.P | FixedReset | 1.30 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2018-04-25 Maturity Price : 25.00 Evaluated at bid price : 25.65 Bid-YTW : 2.58 % |

| BAM.PR.C | Floater | 1.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-02 Maturity Price : 15.50 Evaluated at bid price : 15.50 Bid-YTW : 3.25 % |

| TRP.PR.D | FixedReset | 1.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-02 Maturity Price : 22.81 Evaluated at bid price : 23.94 Bid-YTW : 3.41 % |

| FTS.PR.G | FixedReset | 1.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-02 Maturity Price : 22.86 Evaluated at bid price : 23.89 Bid-YTW : 3.12 % |

| ENB.PF.C | FixedReset | 1.47 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-02 Maturity Price : 22.16 Evaluated at bid price : 22.80 Bid-YTW : 3.98 % |

| TRP.PR.E | FixedReset | 1.54 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-02 Maturity Price : 22.98 Evaluated at bid price : 24.44 Bid-YTW : 3.36 % |

| ENB.PR.F | FixedReset | 1.56 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-02 Maturity Price : 20.12 Evaluated at bid price : 20.12 Bid-YTW : 4.25 % |

| BNS.PR.Z | FixedReset | 1.58 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.16 Bid-YTW : 3.60 % |

| SLF.PR.H | FixedReset | 1.60 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.86 Bid-YTW : 4.14 % |

| CU.PR.C | FixedReset | 1.67 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-02 Maturity Price : 23.29 Evaluated at bid price : 24.40 Bid-YTW : 3.26 % |

| BNS.PR.Y | FixedReset | 1.69 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.22 Bid-YTW : 3.71 % |

| BAM.PR.B | Floater | 1.82 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-02 Maturity Price : 15.69 Evaluated at bid price : 15.69 Bid-YTW : 3.21 % |

| MFC.PR.F | FixedReset | 1.88 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.00 Bid-YTW : 5.65 % |

| TRP.PR.F | FloatingReset | 2.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-02 Maturity Price : 19.00 Evaluated at bid price : 19.00 Bid-YTW : 3.23 % |

| IFC.PR.A | FixedReset | 2.19 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.05 Bid-YTW : 5.81 % |

| IAG.PR.G | FixedReset | 2.20 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2017-06-30 Maturity Price : 25.00 Evaluated at bid price : 25.98 Bid-YTW : 2.41 % |

| ENB.PF.A | FixedReset | 2.56 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-02 Maturity Price : 22.19 Evaluated at bid price : 22.82 Bid-YTW : 3.98 % |

| BAM.PR.K | Floater | 2.58 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-02 Maturity Price : 15.50 Evaluated at bid price : 15.50 Bid-YTW : 3.25 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| TRP.PR.G | FixedReset | 1,351,456 | New issue settled today. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-02 Maturity Price : 23.06 Evaluated at bid price : 24.83 Bid-YTW : 3.66 % |

| RY.PR.J | FixedReset | 182,598 | TD crossed 50,000 at 24.98; RBC crossed 49,500 at 24.99. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-02 Maturity Price : 23.13 Evaluated at bid price : 24.96 Bid-YTW : 3.43 % |

| CU.PR.C | FixedReset | 157,914 | RBC crossed 150,000 at 23.92. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-02 Maturity Price : 23.29 Evaluated at bid price : 24.40 Bid-YTW : 3.26 % |

| ENB.PR.P | FixedReset | 118,389 | TD crossed 10,900 at 20.38; RBC crossed 98,400 at 20.57. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-02 Maturity Price : 20.42 Evaluated at bid price : 20.42 Bid-YTW : 4.21 % |

| TRP.PR.E | FixedReset | 104,106 | Scotia crossed 100,000 at 24.25. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-02 Maturity Price : 22.98 Evaluated at bid price : 24.44 Bid-YTW : 3.36 % |

| NA.PR.Q | FixedReset | 83,250 | RBC crossed 76,700 at 25.25. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.25 Bid-YTW : 3.32 % |

| There were 52 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| IFC.PR.A | FixedReset | Quote: 20.05 – 20.78 Spot Rate : 0.7300 Average : 0.4651 YTW SCENARIO |

| CIU.PR.C | FixedReset | Quote: 15.97 – 17.00 Spot Rate : 1.0300 Average : 0.7693 YTW SCENARIO |

| MFC.PR.K | FixedReset | Quote: 23.28 – 23.81 Spot Rate : 0.5300 Average : 0.3282 YTW SCENARIO |

| MFC.PR.J | FixedReset | Quote: 25.10 – 25.66 Spot Rate : 0.5600 Average : 0.3676 YTW SCENARIO |

| MFC.PR.H | FixedReset | Quote: 25.71 – 26.10 Spot Rate : 0.3900 Average : 0.2356 YTW SCENARIO |

| BAM.PF.A | FixedReset | Quote: 25.27 – 25.65 Spot Rate : 0.3800 Average : 0.2443 YTW SCENARIO |