Today’s big news was the FOMC release:

Information received since the Federal Open Market Committee met in July suggests that economic activity is expanding at a moderate pace. Household spending and business fixed investment have been increasing moderately, and the housing sector has improved further; however, net exports have been soft. The labor market continued to improve, with solid job gains and declining unemployment. On balance, labor market indicators show that underutilization of labor resources has diminished since early this year. Inflation has continued to run below the Committee’s longer-run objective, partly reflecting declines in energy prices and in prices of non-energy imports. Market-based measures of inflation compensation moved lower; survey-based measures of longer-term inflation expectations have remained stable.

…

To support continued progress toward maximum employment and price stability, the Committee today reaffirmed its view that the current 0 to 1/4 percent target range for the federal funds rate remains appropriate. In determining how long to maintain this target range, the Committee will assess progress–both realized and expected–toward its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments. The Committee anticipates that it will be appropriate to raise the target range for the federal funds rate when it has seen some further improvement in the labor market and is reasonably confident that inflation will move back to its 2 percent objective over the medium term.

…

The Committee currently anticipates that, even after employment and inflation are near mandate-consistent levels, economic conditions may, for some time, warrant keeping the target federal funds rate below levels the Committee views as normal in the longer run.

…

Voting against the action was Jeffrey M. Lacker, who preferred to raise the target range for the federal funds rate by 25 basis points at this meeting.

The number of EI beneficiaries rose 2 per cent to 545,200 in July from a month earlier, Statistics Canada said Thursday, led by increases in British Columbia, Ontario and Alberta. That level is 7.1 per cent higher than a year ago.

In Alberta, the province most exposed to lower oil prices, the number of EI beneficiaries climbed for the ninth straight month. EI numbers rose 1.8 per cent from a month earlier – a slower pace than in previous months – and are 72.2 per cent higher than in July of last year.

British Columbia and Ontario saw the biggest monthly percentage increases while Quebec and Saskatchewan also registered gains. Numbers fell in Manitoba and Newfoundland.

It was a mildly negative day for the Canadian preferred share market, with PerpetualDiscounts gaining 5bp, FixedResets off 8bp and DeemedRetractibles down 19bp. The Performance Highlights table is reasonably balanced. Volume was low.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

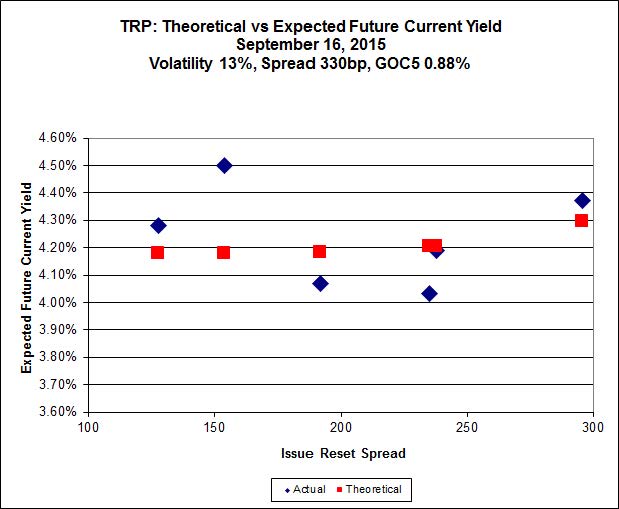

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 20.00 to be $0.81 rich, while TRP.PR.C, resetting 2016-1-30 at +164, is $1.04 cheap at its bid price of 13.39.

Click for Big

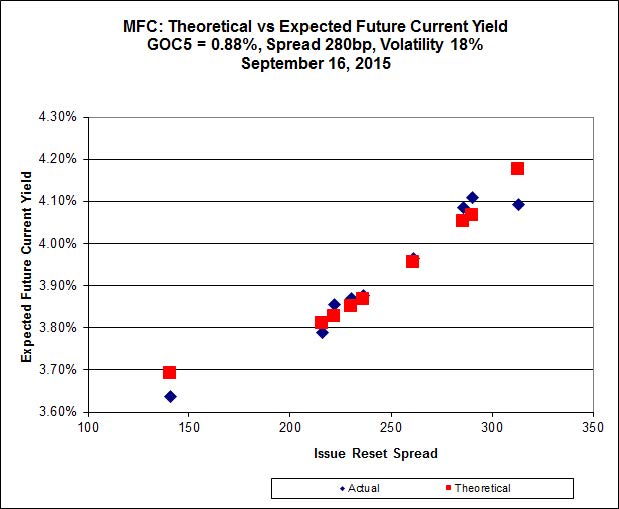

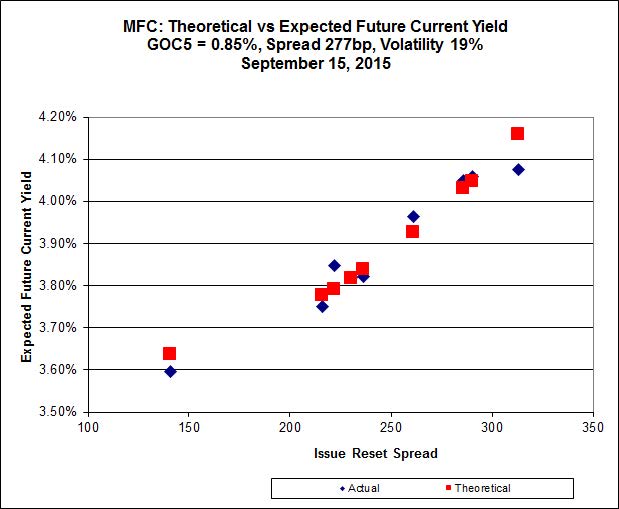

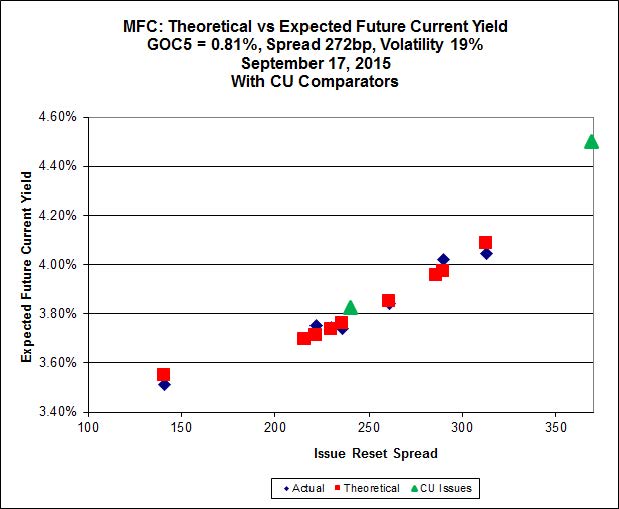

Another good fit today for MFC, with Implied Volatility falling a bit today.

Most expensive is MFC.PR.H, resetting at +313bp on 2017-3-19, bid at 24.36 to be 0.25 rich, while MFC.PR.G, resetting at +290bp on 2016-12-19, is bid at 23.07 to be 0.28 cheap.

Click for Big

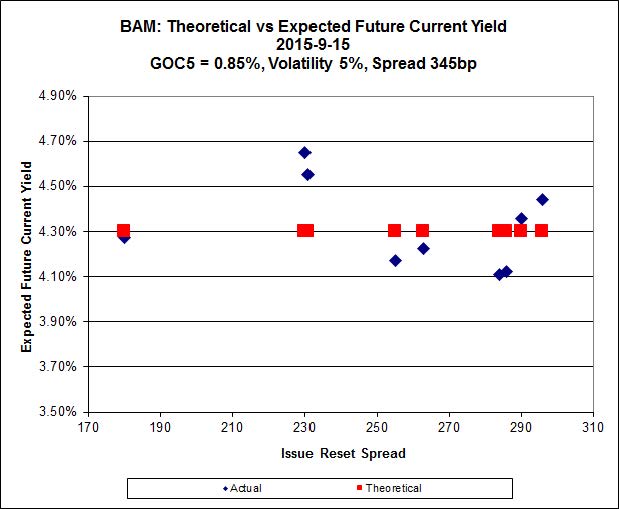

The fit on the BAM issues continues to be horrible.

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 17.00 to be $1.30 cheap. BAM.PF.G, resetting at +284bp on 2020-6-30 is bid at 22.48 and appears to be $1.06 rich.

Click for Big

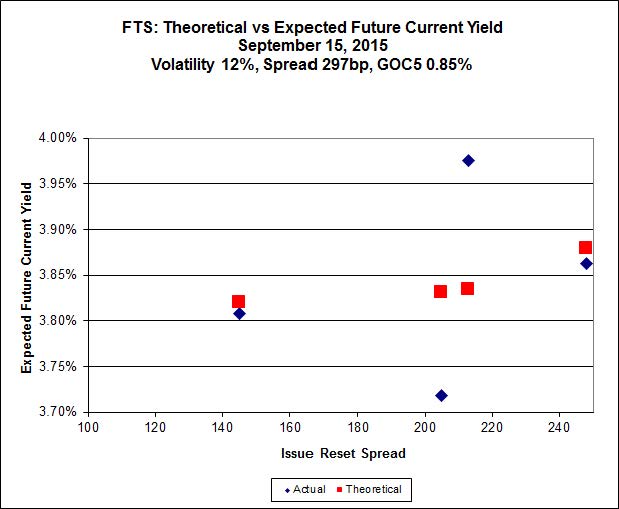

FTS.PR.M, with a spread of +248bp, and bid at 22.20, looks $0.61 expensive and resets 2019-12-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 18.79 and is $0.50 cheap.

Click for Big

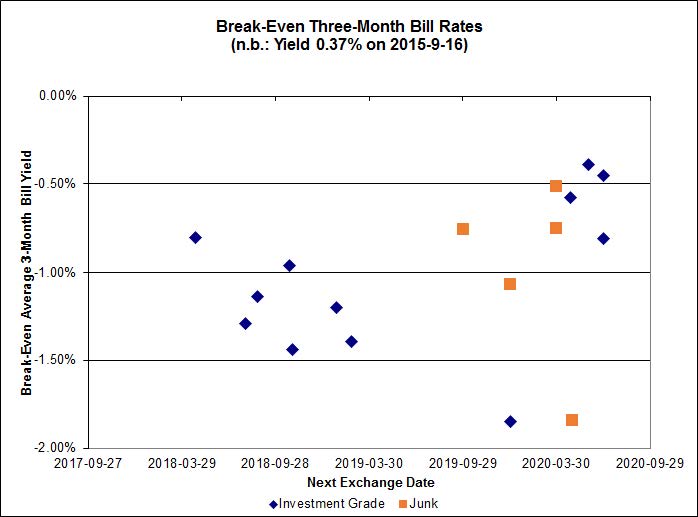

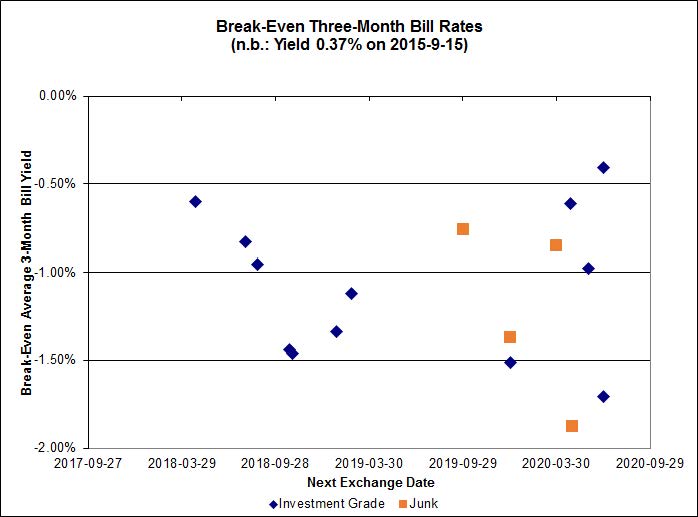

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.89%, with no outliers. The distribution’s bimodality has vanished. There are two junk outliers above 0.00%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0944 % | 1,666.9 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0944 % | 2,914.6 |

| Floater | 4.46 % | 4.45 % | 57,298 | 16.54 | 3 | 0.0944 % | 1,772.1 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.2970 % | 2,774.9 |

| SplitShare | 4.64 % | 4.94 % | 60,339 | 3.06 | 3 | -0.2970 % | 3,252.0 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.2970 % | 2,537.4 |

| Perpetual-Premium | 5.72 % | 4.73 % | 54,130 | 0.08 | 8 | -0.1087 % | 2,491.2 |

| Perpetual-Discount | 5.45 % | 5.53 % | 67,104 | 14.59 | 30 | 0.0511 % | 2,600.8 |

| FixedReset | 4.73 % | 4.10 % | 173,820 | 16.12 | 74 | -0.0843 % | 2,151.7 |

| Deemed-Retractible | 5.15 % | 5.08 % | 93,885 | 5.50 | 33 | -0.1926 % | 2,581.9 |

| FloatingReset | 2.47 % | 3.88 % | 49,687 | 5.91 | 9 | -0.0764 % | 2,155.5 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| SLF.PR.J | FloatingReset | -2.84 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.35 Bid-YTW : 9.34 % |

| IFC.PR.A | FixedReset | -1.80 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.34 Bid-YTW : 8.48 % |

| IAG.PR.G | FixedReset | -1.64 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.81 Bid-YTW : 4.93 % |

| PWF.PR.T | FixedReset | -1.58 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-17 Maturity Price : 22.41 Evaluated at bid price : 23.02 Bid-YTW : 3.59 % |

| SLF.PR.B | Deemed-Retractible | -1.48 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.02 Bid-YTW : 6.54 % |

| FTS.PR.K | FixedReset | -1.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-17 Maturity Price : 18.75 Evaluated at bid price : 18.75 Bid-YTW : 4.06 % |

| HSE.PR.E | FixedReset | -1.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-17 Maturity Price : 22.06 Evaluated at bid price : 22.60 Bid-YTW : 4.82 % |

| PWF.PR.S | Perpetual-Discount | -1.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-17 Maturity Price : 21.99 Evaluated at bid price : 22.31 Bid-YTW : 5.44 % |

| BMO.PR.M | FixedReset | -1.27 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.01 Bid-YTW : 3.63 % |

| BNS.PR.P | FixedReset | -1.27 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.05 Bid-YTW : 3.81 % |

| NA.PR.S | FixedReset | -1.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-17 Maturity Price : 21.52 Evaluated at bid price : 21.52 Bid-YTW : 3.91 % |

| RY.PR.I | FixedReset | -1.21 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.50 Bid-YTW : 3.56 % |

| TD.PF.F | Perpetual-Discount | -1.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-17 Maturity Price : 23.83 Evaluated at bid price : 24.17 Bid-YTW : 5.13 % |

| PVS.PR.D | SplitShare | -1.03 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2021-10-08 Maturity Price : 25.00 Evaluated at bid price : 24.05 Bid-YTW : 5.29 % |

| TD.PF.D | FixedReset | -1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-17 Maturity Price : 22.37 Evaluated at bid price : 23.16 Bid-YTW : 3.83 % |

| GWO.PR.S | Deemed-Retractible | -1.02 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.25 Bid-YTW : 5.68 % |

| MFC.PR.N | FixedReset | 1.02 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.76 Bid-YTW : 5.85 % |

| MFC.PR.J | FixedReset | 1.09 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.25 Bid-YTW : 5.06 % |

| SLF.PR.G | FixedReset | 1.10 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.62 Bid-YTW : 8.01 % |

| MFC.PR.I | FixedReset | 1.14 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.15 Bid-YTW : 4.81 % |

| HSE.PR.C | FixedReset | 1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-17 Maturity Price : 20.75 Evaluated at bid price : 20.75 Bid-YTW : 4.89 % |

| SLF.PR.H | FixedReset | 1.31 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.85 Bid-YTW : 7.32 % |

| GWO.PR.N | FixedReset | 1.40 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.25 Bid-YTW : 8.18 % |

| FTS.PR.M | FixedReset | 1.42 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-17 Maturity Price : 21.82 Evaluated at bid price : 22.20 Bid-YTW : 3.85 % |

| MFC.PR.M | FixedReset | 1.44 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.20 Bid-YTW : 5.64 % |

| POW.PR.B | Perpetual-Discount | 1.47 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-17 Maturity Price : 23.88 Evaluated at bid price : 24.13 Bid-YTW : 5.54 % |

| TRP.PR.F | FloatingReset | 2.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-17 Maturity Price : 14.70 Evaluated at bid price : 14.70 Bid-YTW : 3.87 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| RY.PR.L | FixedReset | 45,613 | RBC crossed 38,000 at 25.65. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.49 Bid-YTW : 3.61 % |

| TD.PF.F | Perpetual-Discount | 41,450 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-17 Maturity Price : 23.83 Evaluated at bid price : 24.17 Bid-YTW : 5.13 % |

| FTS.PR.G | FixedReset | 40,390 | Scotia crossed 40,000 at 18.90. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-17 Maturity Price : 18.79 Evaluated at bid price : 18.79 Bid-YTW : 4.07 % |

| BAM.PR.B | Floater | 36,847 | Nesbitt crossed 25,000 at 10.70. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-17 Maturity Price : 10.71 Evaluated at bid price : 10.71 Bid-YTW : 4.41 % |

| PWF.PR.P | FixedReset | 31,282 | Scotia crossed 22,800 at 15.40. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-17 Maturity Price : 15.36 Evaluated at bid price : 15.36 Bid-YTW : 3.94 % |

| BAM.PF.A | FixedReset | 31,000 | RBC crossed 24,400 at 21.72. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-17 Maturity Price : 21.32 Evaluated at bid price : 21.62 Bid-YTW : 4.38 % |

| There were 17 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| FTS.PR.K | FixedReset | Quote: 18.75 – 19.59 Spot Rate : 0.8400 Average : 0.6315 YTW SCENARIO |

| BNS.PR.P | FixedReset | Quote: 24.05 – 24.47 Spot Rate : 0.4200 Average : 0.2499 YTW SCENARIO |

| SLF.PR.B | Deemed-Retractible | Quote: 22.02 – 22.45 Spot Rate : 0.4300 Average : 0.2965 YTW SCENARIO |

| FTS.PR.G | FixedReset | Quote: 18.79 – 19.25 Spot Rate : 0.4600 Average : 0.3417 YTW SCENARIO |

| MFC.PR.C | Deemed-Retractible | Quote: 21.18 – 21.62 Spot Rate : 0.4400 Average : 0.3260 YTW SCENARIO |

| PVS.PR.D | SplitShare | Quote: 24.05 – 24.40 Spot Rate : 0.3500 Average : 0.2443 YTW SCENARIO |