There will be a slight delay with the release of the November, 2016, PrefLetter.

I hope to have it out by Tuesday evening; perhaps earlier.

There will be a slight delay with the release of the November, 2016, PrefLetter.

I hope to have it out by Tuesday evening; perhaps earlier.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.1607 % | 1,724.6 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.1607 % | 3,150.5 |

| Floater | 4.35 % | 4.51 % | 43,200 | 16.37 | 4 | -0.1607 % | 1,815.6 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0859 % | 2,904.9 |

| SplitShare | 4.82 % | 4.37 % | 43,044 | 4.34 | 6 | 0.0859 % | 3,469.1 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0859 % | 2,706.7 |

| Perpetual-Premium | 5.39 % | 4.92 % | 74,408 | 3.93 | 23 | -0.2638 % | 2,683.5 |

| Perpetual-Discount | 5.23 % | 5.22 % | 87,774 | 15.09 | 15 | -0.6617 % | 2,861.7 |

| FixedReset | 4.78 % | 4.27 % | 179,889 | 6.84 | 93 | -0.0331 % | 2,133.1 |

| Deemed-Retractible | 5.09 % | 5.18 % | 122,960 | 4.53 | 32 | -0.3124 % | 2,773.2 |

| FloatingReset | 2.80 % | 3.39 % | 43,989 | 4.91 | 12 | 0.4958 % | 2,320.1 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| NA.PR.S | FixedReset | -2.45 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-11 Maturity Price : 19.11 Evaluated at bid price : 19.11 Bid-YTW : 4.44 % |

| GWO.PR.Q | Deemed-Retractible | -1.20 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.75 Bid-YTW : 5.43 % |

| NA.PR.W | FixedReset | -1.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-11 Maturity Price : 18.61 Evaluated at bid price : 18.61 Bid-YTW : 4.39 % |

| CU.PR.I | FixedReset | -1.07 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2020-12-01 Maturity Price : 25.00 Evaluated at bid price : 26.80 Bid-YTW : 2.57 % |

| GWO.PR.H | Deemed-Retractible | -1.05 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.45 Bid-YTW : 5.94 % |

| MFC.PR.B | Deemed-Retractible | -1.01 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.60 Bid-YTW : 6.31 % |

| MFC.PR.C | Deemed-Retractible | -1.00 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.72 Bid-YTW : 6.75 % |

| CU.PR.F | Perpetual-Discount | -1.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-11 Maturity Price : 21.46 Evaluated at bid price : 21.78 Bid-YTW : 5.16 % |

| HSE.PR.A | FixedReset | 1.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-11 Maturity Price : 12.63 Evaluated at bid price : 12.63 Bid-YTW : 5.12 % |

| SLF.PR.G | FixedReset | 1.25 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.62 Bid-YTW : 9.83 % |

| TRP.PR.B | FixedReset | 1.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-11 Maturity Price : 12.45 Evaluated at bid price : 12.45 Bid-YTW : 4.37 % |

| IFC.PR.A | FixedReset | 1.36 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.40 Bid-YTW : 9.03 % |

| MFC.PR.L | FixedReset | 1.75 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.19 Bid-YTW : 7.27 % |

| SLF.PR.J | FloatingReset | 4.01 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.76 Bid-YTW : 10.10 % |

| SLF.PR.K | FloatingReset | 4.36 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.75 Bid-YTW : 8.32 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BMO.PR.B | FixedReset | 597,110 | YTW SCENARIO Maturity Type : Call Maturity Date : 2022-02-25 Maturity Price : 25.00 Evaluated at bid price : 25.73 Bid-YTW : 4.31 % |

| TD.PF.H | FixedReset | 473,226 | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-10-31 Maturity Price : 25.00 Evaluated at bid price : 25.71 Bid-YTW : 4.30 % |

| BAM.PR.Z | FixedReset | 94,168 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-11 Maturity Price : 20.07 Evaluated at bid price : 20.07 Bid-YTW : 4.93 % |

| TD.PF.G | FixedReset | 78,502 | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-04-30 Maturity Price : 25.00 Evaluated at bid price : 26.80 Bid-YTW : 3.79 % |

| BNS.PR.E | FixedReset | 69,023 | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-04-25 Maturity Price : 25.00 Evaluated at bid price : 26.70 Bid-YTW : 3.90 % |

| SLF.PR.H | FixedReset | 49,000 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.50 Bid-YTW : 8.05 % |

| There were 23 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| IFC.PR.D | FloatingReset | Quote: 19.20 – 21.00 Spot Rate : 1.8000 Average : 1.6136 YTW SCENARIO |

| FTS.PR.H | FixedReset | Quote: 14.25 – 14.46 Spot Rate : 0.2100 Average : 0.1317 YTW SCENARIO |

| TRP.PR.A | FixedReset | Quote: 15.88 – 16.13 Spot Rate : 0.2500 Average : 0.1717 YTW SCENARIO |

| SLF.PR.E | Deemed-Retractible | Quote: 21.76 – 22.01 Spot Rate : 0.2500 Average : 0.1766 YTW SCENARIO |

| BAM.PF.H | FixedReset | Quote: 26.56 – 26.85 Spot Rate : 0.2900 Average : 0.2181 YTW SCENARIO |

| MFC.PR.O | FixedReset | Quote: 26.80 – 27.01 Spot Rate : 0.2100 Average : 0.1478 YTW SCENARIO |

Brookfield Asset Management Inc. has announced:

that it has agreed to issue 10,000,000 Class A Preferred Shares, Series 46 on a bought deal basis to a syndicate of underwriters led by TD Securities Inc. and Scotiabank for distribution to the public. The Preferred Shares, Series 46 will be issued at a price of C$25.00 per share, for gross proceeds of C$250,000,000. Holders of the Preferred Shares, Series 46 will be entitled to receive a cumulative quarterly fixed dividend yielding 4.80% annually for the initial period ending March 31, 2022. Thereafter, the dividend rate will be reset every five years at a rate equal to the greater of: (i) the 5-year Government of Canada bond yield plus 3.85% and (ii) 4.80%.

Brookfield has granted the underwriters an option, exercisable until 48 hours prior to closing, to purchase up to an additional 2,000,000 Preferred Shares, Series 46 which, if exercised, would increase the gross offering size to C$300,000,000. The Preferred Shares, Series 46 will be offered in all provinces of Canada by way of a supplement to Brookfield’s existing short form base shelf prospectus. The Preferred Shares, Series 46 may not be offered or sold in the United States or to U.S. persons absent registration or an applicable exemption from the registration requirements under the U.S. Securities Act.

Brookfield intends to use the net proceeds of the issue of Preferred Shares, Series 46 for general corporate purposes. The offering of Preferred Shares, Series 46 is expected to close on or about November 18, 2016.

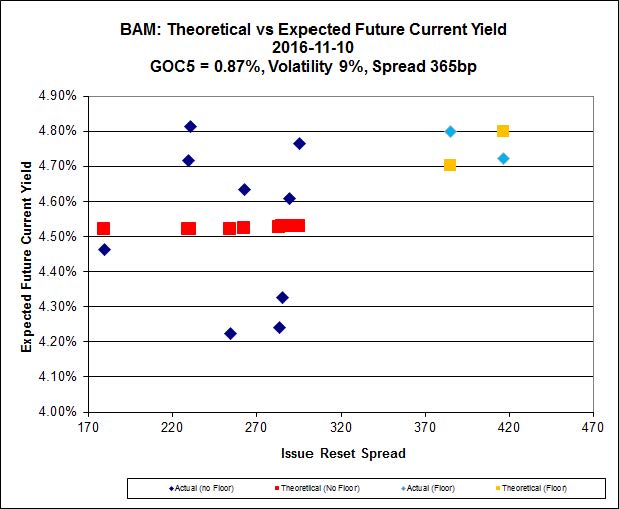

As is usually the case for the BAM series, Implied Volatility analysis yields a mess:

Update, 2016-11-14: They later announced:

that as a result of strong investor demand for its previously announced offering, the underwriters have exercised their option to increase the size of the offering to 12,000,000 Class A Preferred Shares, Series 46. The Preferred Shares, Series 46 will be issued at a price of C$25.00 per share, for gross proceeds of C$300,000,000. The Preferred Shares, Series 46 are being issued on a bought deal basis to a syndicate of underwriters led by TD Securities Inc. and Scotiabank for distribution to the public.

The Preferred Shares, Series 46 will be offered in all provinces of Canada by way of a supplement to Brookfield’s existing short form base shelf prospectus. The Preferred Shares, Series 46 may not be offered or sold in the United States or to U.S. persons absent registration or an applicable exemption from the registration requirements under the U.S. Securities Act.

Brookfield intends to use the net proceeds of the issue of Preferred Shares, Series 46 for general corporate purposes. The offering of Preferred Shares, Series 46 is expected to close on or about November 18, 2016.

There is continued excitement over potential US fiscal stimulus:

A bond-market gauge on Thursday hit its highest level since the summer of 2015. The 10-year break-even inflation rate indicated expected annual inflation of 1.89% over the next 10 years. That measure, reflecting the gap in yields between Treasurys and their inflation-protected counterparts, known as TIPS, was 1.73% two days ago, according to Tradeweb.

The yield on the 10-year Treasury note, which rises when bond prices fall, climbed another 0.05 percentage point on Thursday to 2.118%. It has jumped a quarter of a percentage point since before the U.S. election result, the biggest two-day rise since 2011. Nominal bond rates have been rising faster than those protected against inflation, meaning that inflation protection is increasingly viewed as the more attractive investment.

…

One spark for the latest inflation trade came when Mr. Trump mentioned infrastructure spending prominently Wednesday morning in his victory speech, investors say. Others believe efforts to repeal financial regulations enacted by President Barack Obama’s administration could expand bank lending activity, and that restrictions on trade could boost wages in an already strong labor market.

The New York Times has a bit more colour:

For the last few years, the world has suffered from a chronic shortage of demand, depressing inflation and interest rates worldwide.

If those conditions persist, a Trump administration may have some room to expand deficits without triggering a spike in interest rates that would undo any economic boost those deficits create.

But many economists don’t see it working out that way. Mark Zandi, chief economist at Moody’s Analytics, was skeptical in a much-discussed paper released earlier in the year estimating the economic impact of a Trump administration. He assumed that if Mr. Trump’s policies were taken at face value, it would increase the deficit from 3.5 percent of G.D.P. this year to more than 10 percent by the end of Mr. Trump’s term. He said this would cause the Federal Reserve to raise interest rates above 6 percent in 2018 to prevent inflation.

Who’s up for a 6% Fed policy rate? Who wants to know what will happen to the loony and Canadian house prices then?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.9972 % | 1,727.4 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.9972 % | 3,155.5 |

| Floater | 4.34 % | 4.50 % | 43,648 | 16.38 | 4 | 0.9972 % | 1,818.6 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.3182 % | 2,902.4 |

| SplitShare | 4.82 % | 4.69 % | 61,965 | 4.34 | 6 | 0.3182 % | 3,466.1 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.3182 % | 2,704.4 |

| Perpetual-Premium | 5.38 % | 4.77 % | 77,378 | 2.00 | 23 | -0.3453 % | 2,690.6 |

| Perpetual-Discount | 5.19 % | 5.19 % | 87,349 | 15.15 | 15 | -0.8013 % | 2,880.8 |

| FixedReset | 4.77 % | 4.15 % | 180,458 | 6.89 | 93 | 0.9571 % | 2,133.8 |

| Deemed-Retractible | 5.08 % | 5.22 % | 121,838 | 4.55 | 32 | -0.5333 % | 2,781.9 |

| FloatingReset | 2.77 % | 3.30 % | 44,564 | 4.92 | 12 | 0.5496 % | 2,308.6 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| CCS.PR.C | Deemed-Retractible | -2.01 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.91 Bid-YTW : 5.80 % |

| MFC.PR.B | Deemed-Retractible | -1.76 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.83 Bid-YTW : 6.15 % |

| MFC.PR.C | Deemed-Retractible | -1.66 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.94 Bid-YTW : 6.59 % |

| SLF.PR.B | Deemed-Retractible | -1.59 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.47 Bid-YTW : 5.87 % |

| SLF.PR.D | Deemed-Retractible | -1.36 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.73 Bid-YTW : 6.66 % |

| SLF.PR.C | Deemed-Retractible | -1.36 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.80 Bid-YTW : 6.61 % |

| BAM.PF.C | Perpetual-Discount | -1.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-10 Maturity Price : 22.09 Evaluated at bid price : 22.35 Bid-YTW : 5.49 % |

| SLF.PR.E | Deemed-Retractible | -1.22 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.89 Bid-YTW : 6.60 % |

| BAM.PF.D | Perpetual-Discount | -1.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-10 Maturity Price : 22.51 Evaluated at bid price : 22.81 Bid-YTW : 5.43 % |

| BAM.PR.M | Perpetual-Discount | -1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-10 Maturity Price : 21.86 Evaluated at bid price : 22.10 Bid-YTW : 5.44 % |

| GWO.PR.I | Deemed-Retractible | -1.12 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.07 Bid-YTW : 6.48 % |

| BAM.PR.N | Perpetual-Discount | -1.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-10 Maturity Price : 21.94 Evaluated at bid price : 22.17 Bid-YTW : 5.42 % |

| FTS.PR.F | Perpetual-Discount | -1.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-10 Maturity Price : 23.95 Evaluated at bid price : 24.20 Bid-YTW : 5.14 % |

| BIP.PR.A | FixedReset | 1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-10 Maturity Price : 21.48 Evaluated at bid price : 21.48 Bid-YTW : 5.08 % |

| MFC.PR.J | FixedReset | 1.04 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.40 Bid-YTW : 6.47 % |

| BNS.PR.D | FloatingReset | 1.06 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.97 Bid-YTW : 5.92 % |

| MFC.PR.K | FixedReset | 1.09 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.57 Bid-YTW : 7.51 % |

| RY.PR.H | FixedReset | 1.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-10 Maturity Price : 19.33 Evaluated at bid price : 19.33 Bid-YTW : 4.01 % |

| TD.PF.C | FixedReset | 1.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-10 Maturity Price : 19.22 Evaluated at bid price : 19.22 Bid-YTW : 4.03 % |

| FTS.PR.H | FixedReset | 1.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-10 Maturity Price : 14.21 Evaluated at bid price : 14.21 Bid-YTW : 3.96 % |

| BAM.PF.E | FixedReset | 1.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-10 Maturity Price : 20.25 Evaluated at bid price : 20.25 Bid-YTW : 4.34 % |

| NA.PR.Q | FixedReset | 1.15 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.56 Bid-YTW : 3.64 % |

| GWO.PR.N | FixedReset | 1.16 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.98 Bid-YTW : 10.24 % |

| IAG.PR.G | FixedReset | 1.21 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.89 Bid-YTW : 6.30 % |

| BAM.PF.F | FixedReset | 1.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-10 Maturity Price : 21.27 Evaluated at bid price : 21.55 Bid-YTW : 4.33 % |

| SLF.PR.G | FixedReset | 1.33 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.44 Bid-YTW : 9.89 % |

| NA.PR.W | FixedReset | 1.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-10 Maturity Price : 18.82 Evaluated at bid price : 18.82 Bid-YTW : 4.15 % |

| BMO.PR.Y | FixedReset | 1.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-10 Maturity Price : 21.38 Evaluated at bid price : 21.70 Bid-YTW : 4.00 % |

| CM.PR.P | FixedReset | 1.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-10 Maturity Price : 19.26 Evaluated at bid price : 19.26 Bid-YTW : 4.03 % |

| TD.PF.B | FixedReset | 1.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-10 Maturity Price : 19.13 Evaluated at bid price : 19.13 Bid-YTW : 4.06 % |

| MFC.PR.F | FixedReset | 1.39 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.87 Bid-YTW : 10.43 % |

| BAM.PF.G | FixedReset | 1.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-10 Maturity Price : 21.61 Evaluated at bid price : 21.87 Bid-YTW : 4.29 % |

| BAM.PF.B | FixedReset | 1.45 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-10 Maturity Price : 18.88 Evaluated at bid price : 18.88 Bid-YTW : 4.64 % |

| BMO.PR.W | FixedReset | 1.53 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-10 Maturity Price : 19.24 Evaluated at bid price : 19.24 Bid-YTW : 3.98 % |

| HSE.PR.A | FixedReset | 1.54 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-10 Maturity Price : 12.50 Evaluated at bid price : 12.50 Bid-YTW : 4.91 % |

| PWF.PR.P | FixedReset | 1.55 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-10 Maturity Price : 13.73 Evaluated at bid price : 13.73 Bid-YTW : 4.22 % |

| BAM.PF.A | FixedReset | 1.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-10 Maturity Price : 20.45 Evaluated at bid price : 20.45 Bid-YTW : 4.57 % |

| RY.PR.M | FixedReset | 1.60 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-10 Maturity Price : 20.95 Evaluated at bid price : 20.95 Bid-YTW : 4.04 % |

| FTS.PR.M | FixedReset | 1.61 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-10 Maturity Price : 20.15 Evaluated at bid price : 20.15 Bid-YTW : 4.20 % |

| IFC.PR.C | FixedReset | 1.67 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.47 Bid-YTW : 7.02 % |

| TRP.PR.H | FloatingReset | 1.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-10 Maturity Price : 10.90 Evaluated at bid price : 10.90 Bid-YTW : 3.96 % |

| RY.PR.J | FixedReset | 1.72 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-10 Maturity Price : 21.28 Evaluated at bid price : 21.28 Bid-YTW : 4.09 % |

| TRP.PR.B | FixedReset | 1.82 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-10 Maturity Price : 12.29 Evaluated at bid price : 12.29 Bid-YTW : 4.14 % |

| TRP.PR.E | FixedReset | 1.88 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-10 Maturity Price : 18.95 Evaluated at bid price : 18.95 Bid-YTW : 4.30 % |

| MFC.PR.I | FixedReset | 1.89 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.51 Bid-YTW : 5.94 % |

| TRP.PR.A | FixedReset | 1.91 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-10 Maturity Price : 16.01 Evaluated at bid price : 16.01 Bid-YTW : 4.33 % |

| FTS.PR.K | FixedReset | 1.93 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-10 Maturity Price : 18.45 Evaluated at bid price : 18.45 Bid-YTW : 4.00 % |

| BAM.PR.T | FixedReset | 1.98 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-10 Maturity Price : 16.52 Evaluated at bid price : 16.52 Bid-YTW : 4.69 % |

| MFC.PR.H | FixedReset | 1.99 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.05 Bid-YTW : 5.15 % |

| SLF.PR.H | FixedReset | 2.06 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.38 Bid-YTW : 8.08 % |

| MFC.PR.M | FixedReset | 2.06 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.79 Bid-YTW : 6.90 % |

| IFC.PR.D | FloatingReset | 2.13 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.20 Bid-YTW : 6.90 % |

| NA.PR.S | FixedReset | 2.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-10 Maturity Price : 19.59 Evaluated at bid price : 19.59 Bid-YTW : 4.14 % |

| TRP.PR.F | FloatingReset | 2.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-10 Maturity Price : 14.50 Evaluated at bid price : 14.50 Bid-YTW : 4.09 % |

| MFC.PR.N | FixedReset | 2.27 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.85 Bid-YTW : 6.79 % |

| CU.PR.I | FixedReset | 2.30 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2020-12-01 Maturity Price : 25.00 Evaluated at bid price : 27.09 Bid-YTW : 2.28 % |

| SLF.PR.I | FixedReset | 2.31 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.37 Bid-YTW : 6.50 % |

| VNR.PR.A | FixedReset | 2.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-10 Maturity Price : 19.25 Evaluated at bid price : 19.25 Bid-YTW : 4.66 % |

| BAM.PR.X | FixedReset | 2.47 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-10 Maturity Price : 14.96 Evaluated at bid price : 14.96 Bid-YTW : 4.34 % |

| PWF.PR.A | Floater | 2.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-10 Maturity Price : 11.90 Evaluated at bid price : 11.90 Bid-YTW : 3.97 % |

| FTS.PR.G | FixedReset | 2.64 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-10 Maturity Price : 18.69 Evaluated at bid price : 18.69 Bid-YTW : 3.99 % |

| CU.PR.C | FixedReset | 2.64 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-10 Maturity Price : 19.82 Evaluated at bid price : 19.82 Bid-YTW : 3.94 % |

| MFC.PR.G | FixedReset | 2.67 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.52 Bid-YTW : 5.87 % |

| TRP.PR.C | FixedReset | 2.70 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-10 Maturity Price : 13.71 Evaluated at bid price : 13.71 Bid-YTW : 4.12 % |

| IFC.PR.A | FixedReset | 2.80 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.18 Bid-YTW : 9.05 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| RY.PR.I | FixedReset | 224,005 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.38 Bid-YTW : 3.54 % |

| BMO.PR.B | FixedReset | 198,315 | YTW SCENARIO Maturity Type : Call Maturity Date : 2022-02-25 Maturity Price : 25.00 Evaluated at bid price : 25.73 Bid-YTW : 4.31 % |

| TD.PF.H | FixedReset | 196,546 | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-10-31 Maturity Price : 25.00 Evaluated at bid price : 25.76 Bid-YTW : 4.25 % |

| PWF.PR.K | Perpetual-Discount | 113,209 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-10 Maturity Price : 23.71 Evaluated at bid price : 23.98 Bid-YTW : 5.19 % |

| MFC.PR.O | FixedReset | 107,079 | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-06-19 Maturity Price : 25.00 Evaluated at bid price : 26.85 Bid-YTW : 4.05 % |

| TD.PF.C | FixedReset | 106,945 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-10 Maturity Price : 19.22 Evaluated at bid price : 19.22 Bid-YTW : 4.03 % |

| There were 72 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| IFC.PR.D | FloatingReset | Quote: 19.20 – 21.00 Spot Rate : 1.8000 Average : 1.4091 YTW SCENARIO |

| SLF.PR.K | FloatingReset | Quote: 16.05 – 16.75 Spot Rate : 0.7000 Average : 0.5277 YTW SCENARIO |

| IAG.PR.G | FixedReset | Quote: 20.89 – 21.32 Spot Rate : 0.4300 Average : 0.2579 YTW SCENARIO |

| TRP.PR.G | FixedReset | Quote: 21.68 – 22.04 Spot Rate : 0.3600 Average : 0.2267 YTW SCENARIO |

| PWF.PR.T | FixedReset | Quote: 20.25 – 20.60 Spot Rate : 0.3500 Average : 0.2357 YTW SCENARIO |

| CCS.PR.C | Deemed-Retractible | Quote: 23.91 – 24.25 Spot Rate : 0.3400 Average : 0.2331 YTW SCENARIO |

Those hoping for higher global interest rates via expansionary fiscal policy may soon get their wish:

Donald Trump’s gracious victory speech did two things. It defused much of the negative impact of the shock; and it reminded everyone that the US would have a more expansionary fiscal policy under a Trump presidency than it would have done under a Clinton one. This latter point may take time to be reflected in the markets, and the negative tone on international trade will put pressure on emerging markets. But it is quite plausible that US shares will rise rather than fall over the next few weeks. The dollar should recover swiftly too.

The reason for this is the easing of fiscal policy. With a supportive Congress it should be possible for the new President to get his proposed cuts in both corporation tax and income tax into law next year. Big business did not support a Trump victory but it will benefit from it. Of course, recession fears remain, for this has been a long expansion and the economy is pushing towards full capacity, but US growth next year may surprise on the up side, not the down. Additional spending on infrastructure will take time to feed through – there is no such thing as a shovel-ready project – but such investment will inevitably add to growth in the medium-term.

It is hard, however, to see growth being fast enough to close the budget deficit. A looser fiscal policy will be countered by a tighter monetary one. There was great hostility in the Trump campaign towards the Federal Reserve and to its chair Janet Yellen. But the Fed is independent and it would be unwise of any new administration to pick a fight with it. Right now the markets estimate that the chances of another rise in interest rates in December have shrunk from a near-certainty to an even bet. But this election increases the intellectual case for higher rates. Once they have settled down the markets may come to accept that such rises are inevitable and welcome.

There’s good support for this view:

The Committee for a Responsible Budget said this has made it difficult to evaluate Mr. Trump’s proposals, but estimated they could add $5.3-trillion (U.S.) to the federal debt over 10 years.

…

The initial impact of Mr. Trump’s protectionist policies may not be all bad. Economist Barry Eichengreen argued earlier this year that while tariffs threaten to fan trade wars and geopolitical tensions, the initial impact would be to boost U.S. wages and inflation, something the Federal Reserve’s easy money policies have so far struggled to accomplish.Mr. Zandi’s team at Moody’s Analytics estimates that fully implementing Mr. Trump’s trade and immigration proposals could drive up inflation, eventually triggering aggressive Fed rate hikes and a recession, a concern shared by some investors.

PerpetualDiscounts now yield 5.13%, equivalent to 6.67% interest at the standard equivalency factor of 1.3x. Long corporates now yield about 3.9%, so the pre-tax interest-equivalent spread (in this context, the “Seniority Spread”) is now about 275bp, a sharp narrowing from the 290bp reported on November 2.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.2314 % | 1,710.3 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.2314 % | 3,124.4 |

| Floater | 4.38 % | 4.52 % | 43,726 | 16.34 | 4 | -0.2314 % | 1,800.6 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.3830 % | 2,893.2 |

| SplitShare | 4.84 % | 4.92 % | 62,229 | 5.02 | 6 | -0.3830 % | 3,455.1 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.3830 % | 2,695.8 |

| Perpetual-Premium | 5.36 % | 4.75 % | 77,640 | 2.00 | 23 | 0.0309 % | 2,699.9 |

| Perpetual-Discount | 5.15 % | 5.13 % | 85,063 | 15.24 | 15 | -0.1447 % | 2,904.1 |

| FixedReset | 4.82 % | 4.22 % | 181,241 | 6.87 | 93 | 0.3719 % | 2,113.6 |

| Deemed-Retractible | 5.05 % | 5.17 % | 120,327 | 4.54 | 32 | -0.0690 % | 2,796.8 |

| FloatingReset | 2.79 % | 3.28 % | 44,081 | 4.92 | 12 | 0.1194 % | 2,296.0 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| GRP.PR.A | SplitShare | -2.42 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2023-05-25 Maturity Price : 25.00 Evaluated at bid price : 25.05 Bid-YTW : 6.34 % |

| IFC.PR.D | FloatingReset | -1.05 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.80 Bid-YTW : 7.21 % |

| BNS.PR.D | FloatingReset | 1.02 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.76 Bid-YTW : 6.14 % |

| MFC.PR.F | FixedReset | 1.03 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.68 Bid-YTW : 10.63 % |

| MFC.PR.L | FixedReset | 1.07 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.92 Bid-YTW : 7.34 % |

| FTS.PR.K | FixedReset | 1.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-09 Maturity Price : 18.10 Evaluated at bid price : 18.10 Bid-YTW : 4.08 % |

| BMO.PR.Q | FixedReset | 1.25 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.30 Bid-YTW : 6.05 % |

| NA.PR.S | FixedReset | 1.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-09 Maturity Price : 19.18 Evaluated at bid price : 19.18 Bid-YTW : 4.23 % |

| MFC.PR.G | FixedReset | 1.35 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.96 Bid-YTW : 6.26 % |

| HSE.PR.C | FixedReset | 1.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-09 Maturity Price : 19.95 Evaluated at bid price : 19.95 Bid-YTW : 5.03 % |

| MFC.PR.K | FixedReset | 1.38 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.37 Bid-YTW : 7.67 % |

| IFC.PR.A | FixedReset | 1.42 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.74 Bid-YTW : 9.46 % |

| CU.PR.C | FixedReset | 1.42 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-09 Maturity Price : 19.31 Evaluated at bid price : 19.31 Bid-YTW : 4.04 % |

| MFC.PR.H | FixedReset | 1.44 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.60 Bid-YTW : 5.44 % |

| IAG.PR.G | FixedReset | 1.47 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.64 Bid-YTW : 6.47 % |

| SLF.PR.I | FixedReset | 1.48 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.91 Bid-YTW : 6.84 % |

| IFC.PR.C | FixedReset | 1.59 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.15 Bid-YTW : 7.26 % |

| SLF.PR.J | FloatingReset | 1.70 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.15 Bid-YTW : 10.70 % |

| MFC.PR.J | FixedReset | 1.71 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.19 Bid-YTW : 6.62 % |

| MFC.PR.I | FixedReset | 1.78 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.11 Bid-YTW : 6.22 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BNS.PR.O | Deemed-Retractible | 107,080 | YTW SCENARIO Maturity Type : Call Maturity Date : 2016-12-09 Maturity Price : 25.25 Evaluated at bid price : 25.37 Bid-YTW : 1.42 % |

| BNS.PR.R | FixedReset | 100,519 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.71 Bid-YTW : 3.41 % |

| IAG.PR.G | FixedReset | 72,199 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.64 Bid-YTW : 6.47 % |

| PWF.PR.T | FixedReset | 41,968 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-09 Maturity Price : 20.10 Evaluated at bid price : 20.10 Bid-YTW : 4.00 % |

| MFC.PR.L | FixedReset | 33,487 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.92 Bid-YTW : 7.34 % |

| BAM.PR.T | FixedReset | 32,247 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-09 Maturity Price : 16.20 Evaluated at bid price : 16.20 Bid-YTW : 4.78 % |

| There were 24 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| GWO.PR.N | FixedReset | Quote: 13.82 – 14.33 Spot Rate : 0.5100 Average : 0.3854 YTW SCENARIO |

| W.PR.M | FixedReset | Quote: 26.15 – 26.46 Spot Rate : 0.3100 Average : 0.1861 YTW SCENARIO |

| EML.PR.A | FixedReset | Quote: 26.21 – 26.54 Spot Rate : 0.3300 Average : 0.2116 YTW SCENARIO |

| TRP.PR.F | FloatingReset | Quote: 14.18 – 14.48 Spot Rate : 0.3000 Average : 0.2028 YTW SCENARIO |

| BNS.PR.Y | FixedReset | Quote: 21.01 – 21.23 Spot Rate : 0.2200 Average : 0.1398 YTW SCENARIO |

| POW.PR.D | Perpetual-Discount | Quote: 24.71 – 24.93 Spot Rate : 0.2200 Average : 0.1406 YTW SCENARIO |

The markets could be interesting tomorrow:

Panicked investors rushed to unwind bets they’d piled on amid predictions Clinton would sweep to victory. Futures on the S&P 500 Index plunged more than 4 percent and Mexico’s peso — which tends to weaken as Trump’s prospects improve — sank by the most in two decades. U.S. Treasuries, the yen and gold all soared by the most since Britain’s surprise vote to leave the European Union sent shockwaves through markets in late June.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.2308 % | 1,714.3 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.2308 % | 3,131.6 |

| Floater | 4.37 % | 4.51 % | 43,346 | 16.36 | 4 | -0.2308 % | 1,804.8 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0330 % | 2,904.4 |

| SplitShare | 4.82 % | 4.52 % | 45,725 | 2.04 | 6 | 0.0330 % | 3,468.4 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0330 % | 2,706.2 |

| Perpetual-Premium | 5.36 % | 4.76 % | 73,751 | 2.00 | 23 | -0.0412 % | 2,699.0 |

| Perpetual-Discount | 5.14 % | 5.14 % | 87,446 | 15.26 | 15 | -0.1303 % | 2,908.3 |

| FixedReset | 4.84 % | 4.19 % | 187,398 | 6.86 | 93 | 0.0853 % | 2,105.7 |

| Deemed-Retractible | 5.04 % | 4.93 % | 121,907 | 0.22 | 32 | 0.0294 % | 2,798.8 |

| FloatingReset | 2.79 % | 3.29 % | 44,518 | 4.92 | 12 | 0.0811 % | 2,293.3 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| SLF.PR.J | FloatingReset | -1.67 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 12.93 Bid-YTW : 10.93 % |

| IFC.PR.A | FixedReset | -1.46 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.52 Bid-YTW : 9.67 % |

| TRP.PR.E | FixedReset | -1.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-08 Maturity Price : 18.50 Evaluated at bid price : 18.50 Bid-YTW : 4.40 % |

| PWF.PR.P | FixedReset | -1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-08 Maturity Price : 13.51 Evaluated at bid price : 13.51 Bid-YTW : 4.29 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| IFC.PR.A | FixedReset | 65,099 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.52 Bid-YTW : 9.67 % |

| RY.PR.Z | FixedReset | 64,575 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-08 Maturity Price : 19.15 Evaluated at bid price : 19.15 Bid-YTW : 3.99 % |

| BNS.PR.P | FixedReset | 52,200 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.73 Bid-YTW : 3.18 % |

| BMO.PR.S | FixedReset | 41,093 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-08 Maturity Price : 19.52 Evaluated at bid price : 19.52 Bid-YTW : 4.05 % |

| BIP.PR.C | FixedReset | 40,895 | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-09-30 Maturity Price : 25.00 Evaluated at bid price : 25.65 Bid-YTW : 4.91 % |

| TD.PF.H | FixedReset | 40,750 | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-10-31 Maturity Price : 25.00 Evaluated at bid price : 25.75 Bid-YTW : 4.25 % |

| There were 31 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| GWO.PR.N | FixedReset | Quote: 13.87 – 14.25 Spot Rate : 0.3800 Average : 0.2488 YTW SCENARIO |

| VNR.PR.A | FixedReset | Quote: 18.90 – 19.35 Spot Rate : 0.4500 Average : 0.3441 YTW SCENARIO |

| MFC.PR.F | FixedReset | Quote: 13.54 – 13.84 Spot Rate : 0.3000 Average : 0.2010 YTW SCENARIO |

| TRP.PR.E | FixedReset | Quote: 18.50 – 18.80 Spot Rate : 0.3000 Average : 0.2174 YTW SCENARIO |

| NA.PR.S | FixedReset | Quote: 18.94 – 19.19 Spot Rate : 0.2500 Average : 0.1767 YTW SCENARIO |

| BNS.PR.Z | FixedReset | Quote: 20.74 – 20.98 Spot Rate : 0.2400 Average : 0.1683 YTW SCENARIO |

DBRS has announced that it:

has today confirmed Brookfield Office Properties Inc.’s (BPO or the Company) Senior Unsecured Notes (the Notes) rating at BBB and Cumulative Redeemable Preferred Shares, Class AAA rating at Pfd-3, both with Stable trends. This rating action removes the ratings from Under Review with Developing Implications.

…

In July 2016, BPY completed an internal restructuring to consolidate the ownership of its core retail and office assets within the United States by transferring to a subsidiary of BPO its core retail investments (the Transaction).

…

In DBRS’s view, the Transaction modestly improves BPO’s business risk assessment by increasing the size and scale of the Company’s real estate investments, which complement asset quality and diversification by asset type, partially offset by geographic concentration in the United States. DBRS estimates annual EBITDA will increase to $1.7 billion from $1.0 billion on a pro forma basis in Q1 2016. DBRS also believes the core retail investments complement the quality of BPO’s office assets and will provide a stable and diverse source of cash flow for the Company.The Transaction also has a modestly positive impact on BPO’s financial risk assessment by improving key financial metrics. DBRS estimates an improvement in BPO’s EBITDA interest coverage (including capitalized interest) to 1.72 times (x) from 1.59x and debt-to-EBITDA to 13.5x from 14.2x, respectively.

With the improvement of EBITDA interest coverage (including capitalized interest) to levels above 1.70x, BPO has met DBRS’s 12-month expectation. DBRS expects BPO to improve this key metric above 2.00x and its fixed-charge coverage to 1.75x over the longer term, which is more consistent with the current rating category.

The core retail investments are held by various entities that now structurally sit in between BPO and its key U.S. operating assets. Three of these entities (the BPO Co-Borrowers), along with certain subsidiaries of BPY, are co-borrowers of a $2.5 billion external credit facility (the Credit Facility). While the BPO Co-Borrowers have not yet drawn on the Credit Facility (currently, $1.14 billion has been drawn by the other co-borrowers), the Credit Facility’s agreement states that all borrowers (including the BPO Co-Borrowers) are jointly and severally liable for any amounts drawn. As such, the Notes are structurally subordinated (see the discussion on structural subordination below) to the lenders of the Credit Facility. DBRS has also assumed the Credit Facility is fully drawn and included this amount in its calculation of BPO’s key financial metrics.

STRUCTURAL SUBORDINATION

As discussed above, the BPO Co-Borrowers are jointly and severally liable for any amounts drawn from the Credit Facility. The transfer of the core retail investments to a subsidiary of BPO has structurally placed the lenders of the Credit Facility closer to BPO’s key U.S. operating subsidiaries relative to the holders of BPO’s Notes. As such, the lenders of the Credit Facility now rank ahead of BPO’s Noteholders in their claim to the cash flow and assets of the Company’s key U.S. operating subsidiaries and core retail investment in an event of default scenario.DBRS has not lowered the rating of the Notes by one notch, as DBRS believes the issue of subordination is mitigated by several credit-enhancing factors. These factors are as follows: (1) The core retail investment is self-sustaining and generates more-than-sufficient cash flow to fund its own capital requirements and any amounts drawn on the Credit Facility. (2) The core retail investment has added significant asset value ($9.1 billion) relative to the debt incurred by BPO. (3) BPO will benefit from substantial distributions from the core retail investment. (4) BPO’s operating subsidiaries and investments (excluding the core retail investment and key U.S. operating subsidiaries) will continue to provide an adequate source of cash flow distributions as well as account for a significant proportion of the Company’s assets.

DBRS notes, however, that any material deterioration in the credit quality of the core retail investment (e.g., caused by an increase in debt and/or reduced cash flow) or any material increase in subordination could result in the reduced effectiveness of the above-noted mitigating factors. In such an event, a one-notch downgrade of BPO’s ratings would be warranted.

The November 1, 2016 announcement of a continued review was reported on PrefBlog.

Affected issues are: BPO.PR.A, BPO.PR.C, BPO.PR.J, BPO.PR.K, BPO.PR.N, BPO.PR.P, BPO.PR.R, BPO.PR.S, BPO.PR.T, BPO.PR.W, BPO.PR.X and BPO.PR.Y.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.4638 % | 1,718.2 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.4638 % | 3,138.9 |

| Floater | 4.36 % | 4.52 % | 44,025 | 16.35 | 4 | 0.4638 % | 1,808.9 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1058 % | 2,903.4 |

| SplitShare | 4.82 % | 4.50 % | 44,769 | 2.05 | 6 | 0.1058 % | 3,467.3 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1058 % | 2,705.3 |

| Perpetual-Premium | 5.36 % | 4.70 % | 71,064 | 2.00 | 23 | 0.0516 % | 2,700.2 |

| Perpetual-Discount | 5.14 % | 5.12 % | 88,503 | 15.24 | 15 | 0.0624 % | 2,912.1 |

| FixedReset | 4.84 % | 4.22 % | 189,285 | 6.86 | 93 | -0.1100 % | 2,104.0 |

| Deemed-Retractible | 5.05 % | 3.63 % | 120,770 | 0.39 | 32 | 0.0422 % | 2,797.9 |

| FloatingReset | 2.79 % | 3.34 % | 44,687 | 4.93 | 12 | -0.1535 % | 2,291.4 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| SLF.PR.K | FloatingReset | -2.45 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.95 Bid-YTW : 8.82 % |

| GWO.PR.N | FixedReset | -2.40 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.85 Bid-YTW : 10.36 % |

| BAM.PF.A | FixedReset | -1.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-07 Maturity Price : 19.86 Evaluated at bid price : 19.86 Bid-YTW : 4.71 % |

| TRP.PR.B | FixedReset | -1.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-07 Maturity Price : 12.03 Evaluated at bid price : 12.03 Bid-YTW : 4.23 % |

| TRP.PR.C | FixedReset | -1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-07 Maturity Price : 13.27 Evaluated at bid price : 13.27 Bid-YTW : 4.26 % |

| BMO.PR.Q | FixedReset | -1.23 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.03 Bid-YTW : 6.33 % |

| BAM.PR.X | FixedReset | -1.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-07 Maturity Price : 14.36 Evaluated at bid price : 14.36 Bid-YTW : 4.52 % |

| BAM.PR.C | Floater | 1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-07 Maturity Price : 10.50 Evaluated at bid price : 10.50 Bid-YTW : 4.55 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| TD.PF.H | FixedReset | 121,845 | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-10-31 Maturity Price : 25.00 Evaluated at bid price : 25.75 Bid-YTW : 4.25 % |

| MFC.PR.J | FixedReset | 117,700 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.75 Bid-YTW : 6.94 % |

| BMO.PR.B | FixedReset | 112,365 | YTW SCENARIO Maturity Type : Call Maturity Date : 2022-02-25 Maturity Price : 25.00 Evaluated at bid price : 25.80 Bid-YTW : 4.24 % |

| PWF.PR.K | Perpetual-Discount | 76,250 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-11-07 Maturity Price : 24.01 Evaluated at bid price : 24.26 Bid-YTW : 5.12 % |

| BMO.PR.L | Deemed-Retractible | 65,990 | YTW SCENARIO Maturity Type : Call Maturity Date : 2016-12-07 Maturity Price : 25.25 Evaluated at bid price : 25.40 Bid-YTW : -4.86 % |

| BNS.PR.Z | FixedReset | 59,625 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.57 Bid-YTW : 6.09 % |

| There were 34 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| IAG.PR.G | FixedReset | Quote: 20.32 – 20.61 Spot Rate : 0.2900 Average : 0.2009 YTW SCENARIO |

| BAM.PR.X | FixedReset | Quote: 14.36 – 14.66 Spot Rate : 0.3000 Average : 0.2125 YTW SCENARIO |

| BMO.PR.Z | Perpetual-Premium | Quote: 25.15 – 25.34 Spot Rate : 0.1900 Average : 0.1252 YTW SCENARIO |

| BNS.PR.B | FloatingReset | Quote: 23.47 – 23.62 Spot Rate : 0.1500 Average : 0.0972 YTW SCENARIO |

| MFC.PR.B | Deemed-Retractible | Quote: 23.06 – 23.23 Spot Rate : 0.1700 Average : 0.1176 YTW SCENARIO |

| TD.PR.Z | FloatingReset | Quote: 23.45 – 23.63 Spot Rate : 0.1800 Average : 0.1344 YTW SCENARIO |

Malachite Aggressive Preferred Fund’s Net Asset Value per Unit as of the close October 31, 2016, was $8.1827.

| Returns to October 31, 2016 | ||||

| Period | MAPF | BMO-CM “50” Index | TXPR Total Return |

CPD – according to Blackrock |

| One Month | +1.53% | +2.12% | +2.32% | N/A |

| Three Months | +4.24% | +3.33% | +3.36% | N/A |

| One Year | +6.83% | +5.84% | +5.01% | +4.42% |

| Two Years (annualized) | -6.99% | -5.34% | -5.77% | N/A |

| Three Years (annualized) | -1.79% | -2.17% | -1.98% | -2.38% |

| Four Years (annualized) | -1.65% | -1.56% | -1.80% | N/A |

| Five Years (annualized) | +0.80% | -0.05% | -0.30% | -0.74% |

| Six Years (annualized) | +1.06% | +1.01% | +0.48% | |

| Seven Years (annualized) | +3.72% | +2.80% | +2.06% | |

| Eight Years (annualized) | +10.14% | +4.56% | +3.71% | |

| Nine Years (annualized) | +8.26% | +2.55% | +1.73% | |

| Ten Years (annualized) | +7.07% | +1.78% | ||

| Eleven Years (annualized) | +7.00% | +2.07% | ||

| Twelve Years (annualized) | +6.96% | +2.23% | ||

| Thirteen Years (annualized) | +7.58% | +2.49% | ||

| Fourteen Years (annualized) | +8.83% | +2.83% | ||

| Fifteen Years (annualized) | +9/33% | +2.64% | ||

| MAPF returns assume reinvestment of distributions, and are shown after expenses but before fees. | ||||

| CPD Returns are for the NAV and are after all fees and expenses. | ||||

| Figures for National Bank Preferred Equity Income Fund (formerly Omega Preferred Equity) (which are after all fees and expenses) for 1-, 3- and 12-months are +2.06%, +3.30% and +5.14%, respectively, according to Morningstar after all fees & expenses. Three year performance is -0.52%; five year is +0.84% | ||||

| Figures for Manulife Preferred Income Class Adv [into which was merged Manulife Preferred Income Fund (formerly AIC Preferred Income Fund)] (which are after all fees and expenses) for 1-, 3- and 12-months are +2.60%, +4.57% & +5.46%, respectively. It will be noted that AIC Preferred Income Fund was in existence prior to August, 2009, but long term performance figures have been suppressed. | ||||

| Figures for Horizons Active Preferred Share ETF (which are after all fees and expenses) for 1-, 3- and 12-months are +2.39%, +3.81% & +6.27%, respectively. Three year performance is -0.67%, five-year is +1.06% | ||||

| Figures for National Bank Preferred Equity Fund (formerly Altamira Preferred Equity Fund) are +2.41%, +3.56% and +5.25% for one-, three- and twelve months, respectively. Three year performance is -1.91%

According to the fund’s fact sheet as of June 30, 2016, the fund’s inception date was October 30, 2015. I do not know how they justify this nonsensical statement, but will assume that prior performance is being suppressed in some perfectly legal manner that somebody at National considers ethical. |

||||

| The figure for BMO S&P/TSX Laddered Preferred Share Index ETF is +% for the past twelve months. Two year performance is -%, three year is -%. | ||||

| Figures for NexGen Canadian Preferred Share Tax Managed Fund (Dividend Tax Credit Class, the best performing) are -%, +% and -% for one-, three- and twelve-months, respectively. | ||||

| Figures for BMO Preferred Share Fund are +4.29% and +6.99% for the past three- and twelve-months, respectively. Three year performance is -3.23%. | ||||

| Figures for PowerShares Canadian Preferred Share Index Class, Series F are +6.50% for the past twelve months. The three-year figure is -1.82%; five years is -0.94% | ||||

| Figures for the First Asset Preferred Share Investment Trust (PSF.UN) are no longer available since the fund has merged with First Asset Preferred Share ETF (FPR) | ||||

MAPF returns assume reinvestment of dividends, and are shown after expenses but before fees. Past performance is not a guarantee of future performance. You can lose money investing in Malachite Aggressive Preferred Fund or any other fund. For more information, see the fund’s main page. The fund is available either directly from Hymas Investment Management or through a brokerage account at Odlum Brown Limited.

| Calculation of MAPF Sustainable Income Per Unit | ||||||

| Month | NAVPU | Portfolio Average YTW |

Leverage Divisor |

Securities Average YTW |

Capital Gains Multiplier |

Sustainable Income per current Unit |

| June, 2007 | 9.3114 | 5.16% | 1.03 | 5.01% | 1.3240 | 0.3524 |

| September | 9.1489 | 5.35% | 0.98 | 5.46% | 1.3240 | 0.3773 |

| December, 2007 | 9.0070 | 5.53% | 0.942 | 5.87% | 1.3240 | 0.3993 |

| March, 2008 | 8.8512 | 6.17% | 1.047 | 5.89% | 1.3240 | 0.3938 |

| June | 8.3419 | 6.034% | 0.952 | 6.338% | 1.3240 | $0.3993 |

| September | 8.1886 | 7.108% | 0.969 | 7.335% | 1.3240 | $0.4537 |

| December, 2008 | 8.0464 | 9.24% | 1.008 | 9.166% | 1.3240 | $0.5571 |

| March 2009 | $8.8317 | 8.60% | 0.995 | 8.802% | 1.3240 | $0.5872 |

| June | 10.9846 | 7.05% | 0.999 | 7.057% | 1.3240 | $0.5855 |

| September | 12.3462 | 6.03% | 0.998 | 6.042% | 1.3240 | $0.5634 |

| December 2009 | 10.5662 | 5.74% | 0.981 | 5.851% | 1.1141 | $0.5549 |

| March 2010 | 10.2497 | 6.03% | 0.992 | 6.079% | 1.1141 | $0.5593 |

| June | 10.5770 | 5.96% | 0.996 | 5.984% | 1.1141 | $0.5681 |

| September | 11.3901 | 5.43% | 0.980 | 5.540% | 1.1141 | $0.5664 |

| December 2010 | 10.7659 | 5.37% | 0.993 | 5.408% | 1.0298 | $0.5654 |

| March, 2011 | 11.0560 | 6.00% | 0.994 | 5.964% | 1.0298 | $0.6403 |

| June | 11.1194 | 5.87% | 1.018 | 5.976% | 1.0298 | $0.6453 |

| September | 10.2709 | 6.10% Note |

1.001 | 6.106% | 1.0298 | $0.6090 |

| December, 2011 | 10.0793 | 5.63% Note |

1.031 | 5.805% | 1.0000 | $0.5851 |

| March, 2012 | 10.3944 | 5.13% Note |

0.996 | 5.109% | 1.0000 | $0.5310 |

| June | 10.2151 | 5.32% Note |

1.012 | 5.384% | 1.0000 | $0.5500 |

| September | 10.6703 | 4.61% Note |

0.997 | 4.624% | 1.0000 | $0.4934 |

| December, 2012 | 10.8307 | 4.24% | 0.989 | 4.287% | 1.0000 | $0.4643 |

| March, 2013 | 10.9033 | 3.87% | 0.996 | 3.886% | 1.0000 | $0.4237 |

| June | 10.3261 | 4.81% | 0.998 | 4.80% | 1.0000 | $0.4957 |

| September | 10.0296 | 5.62% | 0.996 | 5.643% | 1.0000 | $0.5660 |

| December, 2013 | 9.8717 | 6.02% | 1.008 | 5.972% | 1.0000 | $0.5895 |

| March, 2014 | 10.2233 | 5.55% | 0.998 | 5.561% | 1.0000 | $0.5685 |

| June | 10.5877 | 5.09% | 0.998 | 5.100% | 1.0000 | $0.5395 |

| September | 10.4601 | 5.28% | 0.997 | 5.296% | 1.0000 | $0.5540 |

| December, 2014 | 10.5701 | 4.83% | 1.009 | 4.787% | 1.0000 | $0.5060 |

| March, 2015 | 9.9573 | 4.99% | 1.001 | 4.985% | 1.0000 | $0.4964 |

| June, 2015 | 9.4181 | 5.55% | 1.002 | 5.539% | 1.0000 | $0.5217 |

| September, 2015 | 7.8140 | 6.98% | 0.999 | 6.987% | 1.0000 | $0.5460 |

| December, 2015 | 8.1379 | 6.85% | 0.997 | 6.871% | 1.0000 | $0.5592 |

| March, 2016 | 7.4416 | 7.79% | 0.998 | 7.805% | 1.0000 | $0.5808 |

| June | 7.6704 | 7.67% | 1.011 | 7.587% | 1.0000 | $0.5819 |

| September | 8.0590 | 7.35% | 0.993 | 7.402% | 1.0000 | $0.5965 |

| October, 2016 | 8.1827 | 7.46% | 1.001 | 7.453% | 1.0000 | $0.6099 |

| NAVPU is shown after quarterly distributions of dividend income and annual distribution of capital gains. Portfolio YTW includes cash (or margin borrowing), with an assumed interest rate of 0.00% The Leverage Divisor indicates the level of cash in the account: if the portfolio is 1% in cash, the Leverage Divisor will be 0.99 Securities YTW divides “Portfolio YTW” by the “Leverage Divisor” to show the average YTW on the securities held; this assumes that the cash is invested in (or raised from) all securities held, in proportion to their holdings. The Capital Gains Multiplier adjusts for the effects of Capital Gains Dividends. On 2009-12-31, there was a capital gains distribution of $1.989262 which is assumed for this purpose to have been reinvested at the final price of $10.5662. Thus, a holder of one unit pre-distribution would have held 1.1883 units post-distribution; the CG Multiplier reflects this to make the time-series comparable. Note that Dividend Distributions are not assumed to be reinvested. Sustainable Income is the resultant estimate of the fund’s dividend income per current unit, before fees and expenses. Note that a “current unit” includes reinvestment of prior capital gains; a unitholder would have had the calculated sustainable income with only, say, 0.9 units in the past which, with reinvestment of capital gains, would become 1.0 current units. |

||||||

| DeemedRetractibles are comprised of all Straight Perpetuals (both PerpetualDiscount and PerpetualPremium) issued by BMO, BNS, CM, ELF, GWO, HSB, IAG, MFC, NA, RY, SLF and TD, which are not exchangable into common at the option of the company (definition refined in May, 2011). These issues are analyzed as if their prospectuses included a requirement to redeem at par on or prior to 2022-1-31 (banks) or 2025-1-31 (insurers and insurance holding companies), in addition to the call schedule explicitly defined. See OSFI Does Not Grandfather Extant Tier 1 Capital, CM.PR.D, CM.PR.E, CM.PR.G: Seeking NVCC Status and the January, February, March and June, 2011, editions of PrefLetter for the rationale behind this analysis.

The same reasoning is also applied to FixedResets from these issuers, other than explicitly defined NVCC from banks. |

||||||

| Yields for September, 2011, to January, 2012, were calculated by imposing a cap of 10% on the yields of YLO issues held, in order to avoid their extremely high calculated yields distorting the calculation and to reflect the uncertainty in the marketplace that these yields will be realized. From February to September 2012, yields on these issues have been set to zero. All YLO issues held were sold in October 2012. | ||||||

These calculations were performed assuming constant contemporary GOC-5 and 3-Month Bill rates, as follows:

| Canada Yields Assumed in Calculations | ||

| Month-end | GOC-5 | 3-Month Bill |

| September, 2015 | 0.78% | 0.40% |

| December, 2015 | 0.71% | 0.46% |

| March, 2016 | 0.70% | 0.44% |

| June | 0.57% | 0.47% |

| September | 0.58% | 0.53% |

| October, 2016 | 0.71% | 0.48% |

Significant positions were held in NVCC non-compliant regulated FixedReset issues on September 30, 2016; all of these currently have their yields calculated with the presumption that they will be called by the issuers at par prior to 2022-1-31 (banks) or 2025-1-31 (insurers and insurance holding companies) or on a different date (SplitShares) This presents another complication in the calculation of sustainable yield, which also assumes that redemption proceeds will be reinvested at the same rate.

I will also note that the sustainable yield calculated above is not directly comparable with any yield calculation currently reported by any other preferred share fund as far as I am aware. The Sustainable Yield depends on:

i) Calculating Yield-to-Worst for each instrument and using this yield for reporting purposes;

ii) Using the contemporary value of Five-Year Canadas to estimate dividends after reset for FixedResets. The assumption regarding the five-year Canada rate has become more important as the proportion of low-spread FixedResets in the portfolio has increased.

iii) Making the assumption that deeply discounted NVCC non-compliant issues from both banks and insurers, both Straight and FixedResets will be redeemed at par on their DeemedMaturity date as discussed above.

First Asset Investment Management Inc. has announced:

that the merger of Preferred Share Investment Trust (TSX: PSF.UN) (the “Fund”) with First Asset Preferred Share ETF (the “First Asset ETF”) (TSX: FPR) was implemented after the close of business on November 1, 2016.

In connection with the Merger, each issued and outstanding unit of the Fund received 0.29955 Unit of the First Asset ETF.

According to FPR’s investment objectives:

First Asset Preferred Share ETF’s investment objective is to provide unitholders with regular distributions; and the opportunity for capital appreciation from the performance of a portfolio comprised primarily of preferred shares of North American issuers. This actively managed portfolio will be comprised primarily of investment grade preferred shares and to a lesser extent investment grade corporate debt and convertible bonds. At least 75% of the Preferred Shares and Corporate Debt in the portfolio of FPR shall be rated investment grade at the end of every reporting period (June 30th and December 31st).

This has the very sad, unfortunate and most lamentable effect of suppressing the performance history of PSF.UN. As reported in the MAPF Performance: September 2016 report, as of September 30, 2016, the historical performance looked like this:

Figures for the First Asset Preferred Share Investment Trust (PSF.UN) are +0.11%, +2.45% and -1.67% for the past one, three and twelve months, respectively. The two-, three-, four- and five-year figures are -14.52%, -9.01%, -7.09% and -5.10%, respectively.