Jobs, jobs, jobs! Not so much in the US…:

U.S. payroll gains slowed by more than forecast in December, wages picked up slightly and the jobless rate held at the lowest level since 2000, adding to signs of a full-employment economy.

Employers added 148,000 workers, compared with the 190,000 median estimate of economists surveyed by Bloomberg, held back by a drop in retail positions, a Labor Department report showed Friday. The jobless rate was at 4.1 percent for a third month, while average hourly earnings increased by 2.5 percent from a year earlier, after a 2.4 percent gain in November that was revised downward.

US markets were mildly impressed (insofar as one can assign cause and effect to market moves, which you generally can’t, but impresses the hoi polloi):

Treasuries slumped and the dollar was flat after a report showed U.S. payroll gains slowed by more than forecast in December, wages picked up slightly and the jobless rate held at the lowest level since 2000. The S&P 500 Index powered to a fresh record and registered its best week since December 2016 as investors looked past the jobs miss, speculating that Republican tax cuts will lead to higher corporate earnings. The Dow Jones Industrial Average and Nasdaq Composite Index also hit all-time highs.

…

The yield on 10-year Treasuries rose two basis points to 2.47 percent.

Meanwhile, in the frozen north:

Canada’s unemployment rate plunged to the lowest in more than 40 years, suddenly raising the odds of a Bank of Canada rate hike this month.

The jobless rate fell to 5.7 percent in December, Statistics Canada said Friday in Ottawa, the lowest in the current data series that begins in 1976. The number of jobs rose by 78,600, beating expectations and bringing the full-year employment gain to 422,500. That’s the best annual increase since 2002.

The economy showed unexpected resiliency as the year came to an end, with the figures indicating rapidly diminishing slack in the labor market that may quicken the expected pace of interest-rate increases by the Bank of Canada. Since September, Canada added 193,400 jobs — the biggest three-month gain since at least 1976.

…

Canadian bond yields and the currency soared on the surprisingly strong jobs data. The loonie strengthened to C$1.2376 per U.S. dollar, the strongest since September. The dollar buys 80.79 U.S. cents.

Bond prices plunged on expectations the jobs report may prompt the central to raise rates as early as this month. The yield on the two-year government of Canada bond jumped six basis points to 1.77 percent, close to a seven-year high. The odds of a rate hike at the Bank of Canada’s next meeting on Jan. 17 soared to 70 percent, from 40 percent yesterday, based on trading in the swaps market.

… and the banks – renowned for their forecasting prowess, provided you ignore completely random events like call volumes going up at the beginning of the year – are in a tizzy:

All but one of Canada’s six biggest commercial lenders now say the central bank will raise interest rates this month after the jobless rate dropped to its lowest in modern records.

Toronto-Dominion Bank, Bank of Nova Scotia, Royal Bank of Canada and the Canadian Imperial Bank of Commerce changed their forecasts after a Statistics Canada report Friday showed the unemployment rate unexpectedly fell to 5.7 percent in December, from 5.9 percent the previous month, on the strength of 78,600 new jobs.

At the end of the day, Perimeter reports three-month bills at 1.12% and five-year bonds at 1.96 – well above their Monday levels of 1.07% and 1.89%, respectively.

The Globe has a good story today highlighting the excellent planning and accurate forecasting of the banks’ investment industry hegemony:

But officials in the brokerage industry say the outages mostly boil down to a simple – but crucial – problem: server space. Retail demand is so unexpectedly high, particularly for stocks in the marijuana industry, that it has become overwhelming.

The brokerages won’t provide usage statistics, but according to the Investment Industry Regulatory Organization of Canada, which oversees trading activity, the volume of trades between Dec. 22 and Jan. 3 jumped 107 per cent from a year earlier. And of that surge, retail trading volumes jumped to 34 per cent of the total from 23 per cent.

…

And even when clients are not transacting, they keep logging in to watch the markets and do research. This type of activity can create just as many bandwidth problems for the servers as trading does. Demand from retail investors tends to spike at particular times – such as when the market opens and again around lunch. One day recently, one brokerage’s user activity was already near full capacity before the market even opened at 9:30 a.m.

Theoretically, banks that make a billion dollars or more every quarter should not have trouble buying servers – but the situation is more complicated than that. For one, these institutions have been cutting costs for the past few years as they got leaner, in part to take on nimble fintech startups.

Servers are also expensive assets in a world where so many firms need them, because data is a critical commodity. Until now, it didn’t seem economical for discount brokerages to have servers sitting around just in case.

This is good reporting by Kiladze and Bradshaw, but they’re too impressed by the statistic cited regarding the Dec. 22 – Jan. 3 period. This is the lightest period of the year. If volume doubles … well, nothing doubled is still nothing.

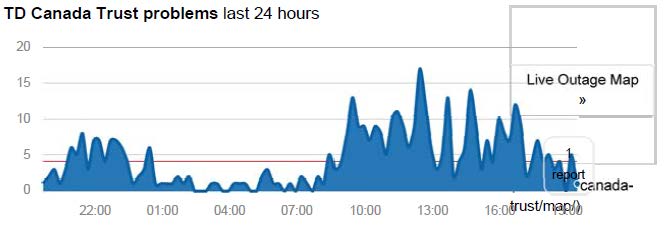

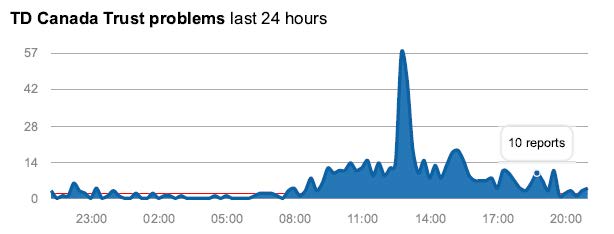

TD has some awfully angry customers:

have been trying to talk to a person at Webbroker since 7 am on Tuesday. I can only do this transaction with a person as online transaction is not allowed. (From rif to other accounts) I have called at Webbroker all hours of day and night and stayed on line for hours at a time. Last evening from 7pm until midnight and again at 4am today no response.

My local branch of TD gave me another number to call and they admitted to also knowing that it would not work, and it did not.

No one and especially an 83 year old should not have to go through a terrible experience that many or going through. It is costing many of us thousands of dollars

Some person or persons should be held accountable and they should be dismissed, and if that is the CEO great.

Seems to me that a business as rife with volume peaks as retail brokerage would design their server system so extra servers could be snapped in overnight … ‘Bob, take a truck to Future Shop and buy 1000 PCs. Fred, you and your guys don’t go home until they’re wired in.’ But what do I know?

Well, I suppose I know that when we get our next market break along the lines of late 1987, early 2001 or late 2008, retail is fucked. Let us all give thanks to the regulators for their continual efforts to place the entire industry in such good hands.

Canadian banks take full advantage of the protection from competition they enjoy and aren’t in the business of making good products. They’re in the business of making plain-vanilla, marginally acceptable products, slapping a brand-name on them and charging a premium price.

HIMIPref™ Preferred Indices

These values reflect the December 2008 revision of the HIMIPref™ Indices

Values are provisional and are finalized monthly |

| Index |

Mean

Current

Yield

(at bid) |

Median

YTW |

Median

Average

Trading

Value |

Median

Mod Dur

(YTW) |

Issues |

Day’s Perf. |

Index Value |

| Ratchet |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.8143 % |

2,694.1 |

| FixedFloater |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.8143 % |

4,943.6 |

| Floater |

3.41 % |

3.57 % |

32,704 |

18.39 |

4 |

0.8143 % |

2,849.0 |

| OpRet |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

-0.2500 % |

3,130.6 |

| SplitShare |

4.69 % |

4.09 % |

61,102 |

3.43 |

5 |

-0.2500 % |

3,738.5 |

| Interest-Bearing |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

-0.2500 % |

2,917.0 |

| Perpetual-Premium |

5.34 % |

-2.33 % |

61,183 |

0.09 |

18 |

-0.0022 % |

2,860.4 |

| Perpetual-Discount |

5.24 % |

5.24 % |

65,153 |

14.91 |

16 |

-0.1403 % |

3,018.7 |

| FixedReset |

4.19 % |

4.30 % |

138,986 |

4.09 |

98 |

0.3883 % |

2,528.1 |

| Deemed-Retractible |

5.03 % |

5.30 % |

82,401 |

5.88 |

28 |

0.0795 % |

2,961.9 |

| FloatingReset |

2.95 % |

2.78 % |

38,787 |

3.82 |

10 |

0.6449 % |

2,733.0 |

| Performance Highlights |

| Issue |

Index |

Change |

Notes |

| CCS.PR.C |

Deemed-Retractible |

-1.14 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 24.20

Bid-YTW : 5.60 % |

| EIT.PR.A |

SplitShare |

-1.02 % |

YTW SCENARIO

Maturity Type : Soft Maturity

Maturity Date : 2024-03-14

Maturity Price : 25.00

Evaluated at bid price : 25.12

Bid-YTW : 4.79 % |

| TRP.PR.F |

FloatingReset |

1.03 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2048-01-05

Maturity Price : 19.65

Evaluated at bid price : 19.65

Bid-YTW : 3.82 % |

| CM.PR.P |

FixedReset |

1.07 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2048-01-05

Maturity Price : 23.18

Evaluated at bid price : 23.51

Bid-YTW : 4.33 % |

| HSE.PR.A |

FixedReset |

1.08 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2048-01-05

Maturity Price : 17.80

Evaluated at bid price : 17.80

Bid-YTW : 4.82 % |

| TRP.PR.B |

FixedReset |

1.11 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2048-01-05

Maturity Price : 16.38

Evaluated at bid price : 16.38

Bid-YTW : 4.67 % |

| IFC.PR.A |

FixedReset |

1.13 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.63

Bid-YTW : 6.63 % |

| CM.PR.O |

FixedReset |

1.14 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2048-01-05

Maturity Price : 23.50

Evaluated at bid price : 23.90

Bid-YTW : 4.35 % |

| BAM.PR.K |

Floater |

1.16 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2048-01-05

Maturity Price : 15.75

Evaluated at bid price : 15.75

Bid-YTW : 3.57 % |

| BAM.PR.B |

Floater |

1.22 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2048-01-05

Maturity Price : 15.76

Evaluated at bid price : 15.76

Bid-YTW : 3.57 % |

| PWF.PR.T |

FixedReset |

1.23 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2048-01-05

Maturity Price : 24.31

Evaluated at bid price : 24.71

Bid-YTW : 4.35 % |

| MFC.PR.M |

FixedReset |

1.24 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 23.75

Bid-YTW : 5.06 % |

| MFC.PR.N |

FixedReset |

1.32 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 23.71

Bid-YTW : 4.99 % |

| BAM.PF.J |

FixedReset |

1.36 % |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2022-12-31

Maturity Price : 25.00

Evaluated at bid price : 26.15

Bid-YTW : 3.77 % |

| BAM.PR.X |

FixedReset |

1.42 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2048-01-05

Maturity Price : 17.81

Evaluated at bid price : 17.81

Bid-YTW : 4.89 % |

| BMO.PR.T |

FixedReset |

1.80 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2048-01-05

Maturity Price : 23.35

Evaluated at bid price : 23.75

Bid-YTW : 4.35 % |

| SLF.PR.J |

FloatingReset |

1.91 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 18.70

Bid-YTW : 7.08 % |

| TRP.PR.C |

FixedReset |

1.92 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2048-01-05

Maturity Price : 17.50

Evaluated at bid price : 17.50

Bid-YTW : 4.64 % |

| TRP.PR.E |

FixedReset |

1.94 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2048-01-05

Maturity Price : 23.28

Evaluated at bid price : 23.65

Bid-YTW : 4.47 % |

| TRP.PR.D |

FixedReset |

1.94 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2048-01-05

Maturity Price : 22.64

Evaluated at bid price : 23.09

Bid-YTW : 4.58 % |

| TRP.PR.A |

FixedReset |

1.96 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2048-01-05

Maturity Price : 20.30

Evaluated at bid price : 20.30

Bid-YTW : 4.65 % |

| TRP.PR.H |

FloatingReset |

3.16 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2048-01-05

Maturity Price : 16.30

Evaluated at bid price : 16.30

Bid-YTW : 3.62 % |

| Volume Highlights |

| Issue |

Index |

Shares

Traded |

Notes |

| BNS.PR.P |

FixedReset |

181,365 |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2018-04-25

Maturity Price : 25.00

Evaluated at bid price : 24.99

Bid-YTW : 2.82 % |

| MFC.PR.O |

FixedReset |

144,344 |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2021-06-19

Maturity Price : 25.00

Evaluated at bid price : 26.80

Bid-YTW : 3.48 % |

| RY.PR.I |

FixedReset |

117,100 |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2019-02-24

Maturity Price : 25.00

Evaluated at bid price : 25.12

Bid-YTW : 3.47 % |

| BAM.PF.A |

FixedReset |

105,877 |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2048-01-05

Maturity Price : 24.46

Evaluated at bid price : 24.90

Bid-YTW : 4.81 % |

| MFC.PR.K |

FixedReset |

74,468 |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 23.00

Bid-YTW : 5.52 % |

| CM.PR.Q |

FixedReset |

72,500 |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2020-07-31

Maturity Price : 25.00

Evaluated at bid price : 24.74

Bid-YTW : 3.95 % |

| There were 33 other index-included issues trading in excess of 10,000 shares. |

| Wide Spread Highlights |

| Issue |

Index |

Quote Data and Yield Notes |

| EIT.PR.A |

SplitShare |

Quote: 25.12 – 25.57

Spot Rate : 0.4500

Average : 0.3175

YTW SCENARIO

Maturity Type : Soft Maturity

Maturity Date : 2024-03-14

Maturity Price : 25.00

Evaluated at bid price : 25.12

Bid-YTW : 4.79 % |

| PWF.PR.L |

Perpetual-Discount |

Quote: 24.50 – 24.85

Spot Rate : 0.3500

Average : 0.2315

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2048-01-05

Maturity Price : 24.21

Evaluated at bid price : 24.50

Bid-YTW : 5.28 % |

| SLF.PR.H |

FixedReset |

Quote: 21.53 – 21.98

Spot Rate : 0.4500

Average : 0.3361

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.53

Bid-YTW : 5.84 % |

| HSE.PR.C |

FixedReset |

Quote: 24.70 – 25.10

Spot Rate : 0.4000

Average : 0.3106

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2048-01-05

Maturity Price : 23.47

Evaluated at bid price : 24.70

Bid-YTW : 4.99 % |

| BAM.PR.K |

Floater |

Quote: 15.75 – 16.01

Spot Rate : 0.2600

Average : 0.1710

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2048-01-05

Maturity Price : 15.75

Evaluated at bid price : 15.75

Bid-YTW : 3.57 % |

| PWF.PR.P |

FixedReset |

Quote: 18.34 – 18.70

Spot Rate : 0.3600

Average : 0.2725

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2048-01-05

Maturity Price : 18.34

Evaluated at bid price : 18.34

Bid-YTW : 4.55 % |