Click for Big

The Canadian economy added more than 30,000 jobs during February as the labour market continues a run of strength …

During the month, 30,300 positions were created, handily beating the consensus estimate of 11,000 jobs added, Statistics Canada said Friday in its Labour Force Survey. The unemployment rate ticked higher, to 5.6 per cent, but remains near historic lows.

The entirety of February’s gain was in full-time work from private-sector employers. Wholesale and retail trade (22,600 jobs created) and manufacturing (16,000) were standout sectors, while Quebec added the largest number of jobs (20,000) by province and saw its jobless rate tumble to 4.5 per cent, the lowest since comparable data became available in 1976.

… and south of the border were jobs, jobs, jobs!

Still, the report from the Department of Labor offered a refreshing breath of positive economic news. Employers expanded payrolls by 273,000 jobs in February, while revisions to data from previous months added 85,000 more jobs to the tally. The jobless rate ticked down to 3.5 percent.

…

“JOBS, JOBS, JOBS!!!” President Trump wrote on Twitter.

…

There were a few signs of weakness in the report. Wage growth, which was already slowing from last year’s peak, was less impressive. Average hourly wages were up 0.2 percent, bringing down the year-over-year gains to 3 percent.

There was just one little problem:

Wall Street was gripped by another wave of worry over the spreading coronavirus on Friday. Stocks tumbled, investors rushed into the safety of government bonds, and oil prices nose-dived.

Financial markets have traded wildly for more than two weeks, as investors have tried to come to grips with the sudden rise in the number of virus cases, and the threat to the economy posed by measures to contain them.

Friday was no exception. The S&P 500 fell about 4 percent at its lowest point before recovering somewhat and ending down less than 2 percent.

Perhaps the most notable move in financial markets was a slide in yields on government bonds to levels that would have been considered unthinkable just two weeks ago. The yield on the 10-year Treasury note fell to as low as 0.68 percent in early trading Friday. Such a steep drop reflects near panic, analysts said, given that there was little news overnight.

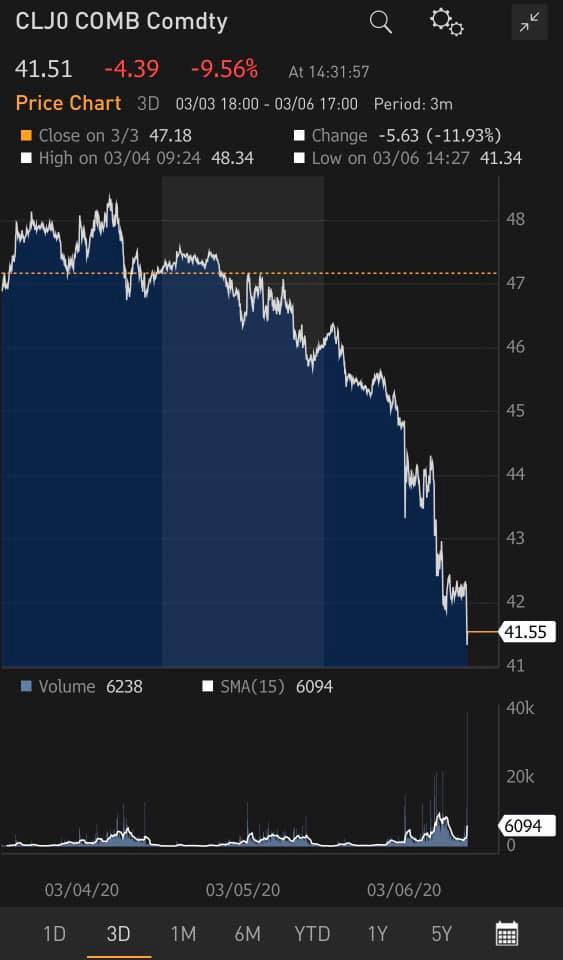

Oil prices slid 10 percent as the world’s major producers failed to reach an agreement to reduce production as demand falls.

Oil down 10% in a day? Mohammed El-Erian posted a chart:

Click for Big

Ten percent in a day on a commodity! One wonders how many fortunes have been won and lost.

And all this has ramped up negative rate speculation:

A collapse in Treasury yields as concerns about the spreading coronavirus sends investors scurrying for low-risk government securities has led some to start preparing for the possibility that the U.S. debt yields could turn negative.

The Federal Reserve on Tuesday made its first emergency cut since the financial crisis, dropping the federal funds rate by 50 basis points to the 1.0% to 1.25% band.

The move has not satisfied markets, however, with stock markets cratering and Treasury yields continuing to plunge to record lows. Interest rate futures traders are now pricing in a 41% probability that rates will be zero-bound by June, according to the CME Group’s FedWatch Tool.

…

The Fed is reluctant to cut rates into negative territory as it risks disrupting the large U.S. money market sector. There are also questions over whether negative rates have been successful at stimulating growth in other countries.“We have a very, very large money market complex,” said Subadra Rajappa, head of U.S. interest rate strategy at Societe Generale in New York. “The Fed has resisted taking interest rates to negative territory because they don’t want to disrupt the liquidity in the financial system.”

TXPR closed at 574.91, down 0.96% on the day. Volume today was 3.44-million, highest of the past 30 trading days days and edging second-place March 4

CPD closed at 11.45, down 0.95% on the day. Volume of 106,124 was well off the pace set in the last two weeks.

ZPR closed at 9.01, down 1.74% on the day. Volume of 443,505 was nothing special in the context of the past two weeks.

Five-year Canada yields were down 6bp to 0.68% today.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -1.3120 % | 1,830.4 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -1.3120 % | 3,358.7 |

| Floater | 5.84 % | 6.12 % | 50,259 | 13.62 | 4 | -1.3120 % | 1,935.7 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0957 % | 3,466.9 |

| SplitShare | 4.79 % | 4.44 % | 51,325 | 4.09 | 7 | -0.0957 % | 4,140.2 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0957 % | 3,230.4 |

| Perpetual-Premium | 5.61 % | 5.14 % | 74,439 | 4.35 | 12 | -0.3833 % | 3,039.6 |

| Perpetual-Discount | 5.29 % | 5.31 % | 69,803 | 14.91 | 24 | -0.4468 % | 3,303.9 |

| FixedReset Disc | 6.15 % | 5.23 % | 191,136 | 14.79 | 64 | -1.1154 % | 1,952.8 |

| Deemed-Retractible | 5.21 % | 5.31 % | 86,836 | 14.85 | 27 | -0.1383 % | 3,242.1 |

| FloatingReset | 5.21 % | 5.04 % | 69,480 | 15.42 | 3 | -1.4526 % | 2,167.7 |

| FixedReset Prem | 5.21 % | 4.91 % | 156,111 | 14.89 | 22 | -1.0316 % | 2,597.7 |

| FixedReset Bank Non | 1.93 % | 3.24 % | 106,288 | 1.86 | 3 | -0.3518 % | 2,750.2 |

| FixedReset Ins Non | 6.00 % | 5.19 % | 105,414 | 14.91 | 22 | -1.3108 % | 1,975.7 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| HSE.PR.A | FixedReset Disc | -6.14 % | This was actually a surprisingly tight quote. The issue traded 16,250 shares today in a range of 9.00-49, which sounds negative, but the closing quote was 8.72-87 – so anybody who wanted some below nine bucks should have stepped up!

YTW SCENARIO |

| RY.PR.S | FixedReset Disc | -3.53 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 17.48 Evaluated at bid price : 17.48 Bid-YTW : 4.92 % |

| SLF.PR.H | FixedReset Ins Non | -3.48 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 13.60 Evaluated at bid price : 13.60 Bid-YTW : 5.20 % |

| HSE.PR.C | FixedReset Disc | -3.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 14.53 Evaluated at bid price : 14.53 Bid-YTW : 7.18 % |

| BMO.PR.B | FixedReset Prem | -2.97 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 23.85 Evaluated at bid price : 24.16 Bid-YTW : 4.91 % |

| TRP.PR.B | FixedReset Disc | -2.96 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 9.52 Evaluated at bid price : 9.52 Bid-YTW : 5.08 % |

| BMO.PR.Y | FixedReset Disc | -2.94 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 16.20 Evaluated at bid price : 16.20 Bid-YTW : 5.24 % |

| NA.PR.E | FixedReset Disc | -2.88 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 16.50 Evaluated at bid price : 16.50 Bid-YTW : 5.33 % |

| MFC.PR.H | FixedReset Ins Non | -2.87 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 17.92 Evaluated at bid price : 17.92 Bid-YTW : 5.38 % |

| IAF.PR.G | FixedReset Ins Non | -2.80 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 16.67 Evaluated at bid price : 16.67 Bid-YTW : 5.31 % |

| HSE.PR.E | FixedReset Disc | -2.70 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 15.50 Evaluated at bid price : 15.50 Bid-YTW : 6.96 % |

| BAM.PF.J | FixedReset Prem | -2.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 23.20 Evaluated at bid price : 24.45 Bid-YTW : 4.86 % |

| TD.PF.H | FixedReset Prem | -2.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 23.73 Evaluated at bid price : 24.10 Bid-YTW : 4.99 % |

| MFC.PR.M | FixedReset Ins Non | -2.58 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 15.46 Evaluated at bid price : 15.46 Bid-YTW : 5.23 % |

| IAF.PR.I | FixedReset Ins Non | -2.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 17.50 Evaluated at bid price : 17.50 Bid-YTW : 5.21 % |

| CM.PR.T | FixedReset Disc | -2.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 21.37 Evaluated at bid price : 21.37 Bid-YTW : 5.03 % |

| BAM.PR.C | Floater | -2.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 10.02 Evaluated at bid price : 10.02 Bid-YTW : 6.14 % |

| PWF.PR.P | FixedReset Disc | -2.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 11.80 Evaluated at bid price : 11.80 Bid-YTW : 4.83 % |

| BMO.PR.F | FixedReset Disc | -1.97 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 21.92 Evaluated at bid price : 22.35 Bid-YTW : 4.91 % |

| BIK.PR.A | FixedReset Prem | -1.92 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2024-03-31 Maturity Price : 25.00 Evaluated at bid price : 25.06 Bid-YTW : 5.71 % |

| BIP.PR.D | FixedReset Disc | -1.91 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 21.64 Evaluated at bid price : 22.07 Bid-YTW : 5.65 % |

| W.PR.M | FixedReset Prem | -1.91 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 23.75 Evaluated at bid price : 25.16 Bid-YTW : 5.17 % |

| MFC.PR.F | FixedReset Ins Non | -1.89 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 10.40 Evaluated at bid price : 10.40 Bid-YTW : 4.99 % |

| HSE.PR.G | FixedReset Disc | -1.88 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 15.70 Evaluated at bid price : 15.70 Bid-YTW : 6.81 % |

| IFC.PR.C | FixedReset Ins Non | -1.85 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 15.90 Evaluated at bid price : 15.90 Bid-YTW : 5.30 % |

| EMA.PR.C | FixedReset Disc | -1.84 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 16.50 Evaluated at bid price : 16.50 Bid-YTW : 5.49 % |

| SLF.PR.J | FloatingReset | -1.83 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 10.75 Evaluated at bid price : 10.75 Bid-YTW : 5.04 % |

| BNS.PR.H | FixedReset Prem | -1.80 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 23.44 Evaluated at bid price : 24.55 Bid-YTW : 4.93 % |

| BAM.PF.H | FixedReset Prem | -1.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 24.35 Evaluated at bid price : 24.80 Bid-YTW : 5.11 % |

| GWO.PR.N | FixedReset Ins Non | -1.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 11.60 Evaluated at bid price : 11.60 Bid-YTW : 4.22 % |

| CM.PR.Y | FixedReset Disc | -1.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 22.13 Evaluated at bid price : 22.70 Bid-YTW : 4.98 % |

| BAM.PR.B | Floater | -1.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 10.02 Evaluated at bid price : 10.02 Bid-YTW : 6.14 % |

| MFC.PR.G | FixedReset Ins Non | -1.74 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 16.97 Evaluated at bid price : 16.97 Bid-YTW : 5.30 % |

| MFC.PR.N | FixedReset Ins Non | -1.74 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 15.29 Evaluated at bid price : 15.29 Bid-YTW : 4.85 % |

| PWF.PR.S | Perpetual-Discount | -1.73 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 22.10 Evaluated at bid price : 22.10 Bid-YTW : 5.50 % |

| BAM.PF.D | Perpetual-Discount | -1.73 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 21.89 Evaluated at bid price : 22.14 Bid-YTW : 5.63 % |

| TRP.PR.F | FloatingReset | -1.72 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 12.00 Evaluated at bid price : 12.00 Bid-YTW : 5.58 % |

| TD.PF.L | FixedReset Disc | -1.71 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 21.53 Evaluated at bid price : 21.80 Bid-YTW : 4.87 % |

| RY.PR.M | FixedReset Disc | -1.69 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 16.27 Evaluated at bid price : 16.27 Bid-YTW : 5.08 % |

| BAM.PF.I | FixedReset Prem | -1.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 23.41 Evaluated at bid price : 24.60 Bid-YTW : 4.89 % |

| BMO.PR.C | FixedReset Disc | -1.62 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 20.07 Evaluated at bid price : 20.07 Bid-YTW : 5.08 % |

| TRP.PR.G | FixedReset Disc | -1.56 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 16.46 Evaluated at bid price : 16.46 Bid-YTW : 5.54 % |

| BAM.PR.N | Perpetual-Discount | -1.55 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 21.35 Evaluated at bid price : 21.62 Bid-YTW : 5.58 % |

| CM.PR.Q | FixedReset Disc | -1.52 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 16.15 Evaluated at bid price : 16.15 Bid-YTW : 5.40 % |

| TD.PF.J | FixedReset Disc | -1.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 17.90 Evaluated at bid price : 17.90 Bid-YTW : 5.08 % |

| BAM.PR.K | Floater | -1.47 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 10.05 Evaluated at bid price : 10.05 Bid-YTW : 6.12 % |

| TRP.PR.A | FixedReset Disc | -1.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 13.50 Evaluated at bid price : 13.50 Bid-YTW : 5.22 % |

| TD.PF.D | FixedReset Disc | -1.42 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 17.30 Evaluated at bid price : 17.30 Bid-YTW : 5.04 % |

| NA.PR.C | FixedReset Disc | -1.42 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 19.40 Evaluated at bid price : 19.40 Bid-YTW : 5.39 % |

| BNS.PR.I | FixedReset Disc | -1.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 17.80 Evaluated at bid price : 17.80 Bid-YTW : 4.93 % |

| BAM.PR.Z | FixedReset Disc | -1.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 17.61 Evaluated at bid price : 17.61 Bid-YTW : 5.49 % |

| IFC.PR.A | FixedReset Ins Non | -1.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 12.93 Evaluated at bid price : 12.93 Bid-YTW : 5.00 % |

| BIP.PR.A | FixedReset Disc | -1.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 17.52 Evaluated at bid price : 17.52 Bid-YTW : 6.02 % |

| BMO.PR.E | FixedReset Disc | -1.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 18.10 Evaluated at bid price : 18.10 Bid-YTW : 5.08 % |

| TD.PF.M | FixedReset Disc | -1.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 22.21 Evaluated at bid price : 22.82 Bid-YTW : 4.87 % |

| MFC.PR.Q | FixedReset Ins Non | -1.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 17.26 Evaluated at bid price : 17.26 Bid-YTW : 5.05 % |

| SLF.PR.B | Deemed-Retractible | -1.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 22.16 Evaluated at bid price : 22.44 Bid-YTW : 5.34 % |

| BAM.PF.G | FixedReset Disc | -1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 16.61 Evaluated at bid price : 16.61 Bid-YTW : 5.38 % |

| RY.PR.J | FixedReset Disc | -1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 16.66 Evaluated at bid price : 16.66 Bid-YTW : 5.13 % |

| BAM.PF.C | Perpetual-Discount | -1.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 22.03 Evaluated at bid price : 22.03 Bid-YTW : 5.61 % |

| TD.PF.K | FixedReset Disc | -1.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 17.90 Evaluated at bid price : 17.90 Bid-YTW : 5.02 % |

| NA.PR.G | FixedReset Disc | -1.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 17.90 Evaluated at bid price : 17.90 Bid-YTW : 5.28 % |

| BNS.PR.G | FixedReset Prem | -1.10 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-07-25 Maturity Price : 25.00 Evaluated at bid price : 25.29 Bid-YTW : 5.11 % |

| BAM.PR.T | FixedReset Disc | -1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 14.01 Evaluated at bid price : 14.01 Bid-YTW : 5.50 % |

| EIT.PR.A | SplitShare | -1.06 % | YTW SCENARIO Maturity Type : Soft Maturity Maturity Date : 2024-03-14 Maturity Price : 25.00 Evaluated at bid price : 25.30 Bid-YTW : 4.46 % |

| BAM.PR.M | Perpetual-Discount | -1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 21.48 Evaluated at bid price : 21.74 Bid-YTW : 5.55 % |

| BAM.PF.B | FixedReset Disc | 4.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 17.20 Evaluated at bid price : 17.20 Bid-YTW : 5.27 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| RY.PR.P | Perpetual-Premium | 154,325 | YTW SCENARIO Maturity Type : Call Maturity Date : 2025-02-24 Maturity Price : 25.00 Evaluated at bid price : 25.20 Bid-YTW : 5.14 % |

| GWO.PR.N | FixedReset Ins Non | 117,900 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 11.60 Evaluated at bid price : 11.60 Bid-YTW : 4.22 % |

| TD.PF.D | FixedReset Disc | 115,422 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 17.30 Evaluated at bid price : 17.30 Bid-YTW : 5.04 % |

| BMO.PR.T | FixedReset Disc | 113,623 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 15.70 Evaluated at bid price : 15.70 Bid-YTW : 4.93 % |

| NA.PR.S | FixedReset Disc | 73,013 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 16.00 Evaluated at bid price : 16.00 Bid-YTW : 5.18 % |

| BAM.PF.B | FixedReset Disc | 61,100 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-06 Maturity Price : 17.20 Evaluated at bid price : 17.20 Bid-YTW : 5.27 % |

| There were 60 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| CM.PR.Y | FixedReset Disc | Quote: 22.70 – 24.10 Spot Rate : 1.4000 Average : 0.8594 YTW SCENARIO |

| HSE.PR.E | FixedReset Disc | Quote: 15.50 – 16.09 Spot Rate : 0.5900 Average : 0.3716 YTW SCENARIO |

| GWO.PR.Q | Deemed-Retractible | Quote: 23.76 – 24.29 Spot Rate : 0.5300 Average : 0.3509 YTW SCENARIO |

| BAM.PF.J | FixedReset Prem | Quote: 24.45 – 24.89 Spot Rate : 0.4400 Average : 0.2784 YTW SCENARIO |

| BIK.PR.A | FixedReset Prem | Quote: 25.06 – 25.48 Spot Rate : 0.4200 Average : 0.2776 YTW SCENARIO |

| TRP.PR.D | FixedReset Disc | Quote: 15.30 – 15.80 Spot Rate : 0.5000 Average : 0.3678 YTW SCENARIO |