Click for Big

DBRS had some interesting Brexit commentary:

DBRS considers that diverging views on Brexit among citizens in the UK could inadvertently lead to the breakup of the Union. DBRS reviews the implications of no-deal scenarios and their potential impact on the unity of the United Kingdom. At one extreme is a “severe” hard Brexit whereby the UK crashes out of the EU permanently with no airbags or restraints on its impact. DBRS concludes that such a Brexit could quickly change the support for Scottish independence and even over time the support for the unification of Ireland, increasing the breakup risk of the UK. These considerations are exacerbated by a weakening economic environment that intensifies divisions within the UK.

…

Scottish independence is the most likely cause of a breakup of the UK. The Scottish government has proposed a second referendum on independence. The first referendum in September 2014 was rejected by 55.0% of voters. Reportedly, that outcome was influenced by concerns that Scotland would lose its EU membership. Should the UK leave the EU without an agreement, that consideration would no longer stand in the way. Given that almost two thirds of Scottish voters voted to remain in the Brexit referendum, the issue of Scotland remaining a member of the EU has continued to be an important component in the debate over Scottish independence. In the event that the UK leaves the EU, DBRS expects that calls for Scottish independence would become even louder, especially in a no-deal scenario.

Boris Johnson has faced a double defeat in the Commons after MPs turned down his motion for a general election.

Earlier, MPs backed a bill aimed at blocking a no-deal Brexit if the PM hadn’t agreed a plan with the EU ahead of the 31 October deadline.

Mr Johnson said the bill “scuppered” negotiations and the only way forward now was an election.

But Labour leader Jeremy Corbyn accused the PM of “playing a disingenuous game” to force a no-deal Brexit.

He said his party would back an election after the bill had been passed, but not before.

Both the SNP and the Liberal Democrats also criticised the prime minister’s motion as a plot to make sure the UK left the EU without a deal.

Meanwhile the the BoC stood pat:

The Bank of Canada today maintained its target for the overnight rate at 1 ¾ percent. The Bank Rate is correspondingly 2 percent and the deposit rate is 1 ½ percent.

As the US-China trade conflict has escalated, world trade has contracted and business investment has weakened. This is weighing more heavily on global economic momentum than the Bank had projected in its July Monetary Policy Report (MPR). Meanwhile, growth in the United States has moderated but remains solid, supported by consumer and government spending. Commodity prices have drifted down as concerns about global growth prospects have increased. These concerns, combined with policy responses by some central banks, have pushed bond yields to historic lows and inverted yield curves in a number of economies, including Canada.

In Canada, growth in the second quarter was strong and exceeded the Bank’s July expectation, although some of this strength is expected to be temporary. The rebound was driven by stronger energy production and robust export growth, both recovering from very weak performance in the first quarter. Housing activity has regained strength more quickly than expected as resales and housing starts catch up to underlying demand, supported by lower mortgage rates. This could add to already-high household debt levels, although mortgage underwriting rules should help to contain the buildup of vulnerabilities. Wages have picked up further, boosting labour income, yet consumption spending was unexpectedly soft in the quarter. Business investment contracted sharply after a strong first quarter, amid heightened trade uncertainty. Given this composition of growth, the Bank expects economic activity to slow in the second half of the year.

Inflation is at the 2 percent target. CPI inflation in July was stronger than expected, largely because of temporary factors. These include higher prices for air travel, mobile phones, and some food items, which are offsetting the effects of lower gasoline prices. Measures of core inflation all remain around 2 percent.

In sum, Canada’s economy is operating close to potential and inflation is on target. However, escalating trade conflicts and related uncertainty are taking a toll on the global and Canadian economies. In this context, the current degree of monetary policy stimulus remains appropriate. As the Bank works to update its projection in light of incoming data, Governing Council will pay particular attention to global developments and their impact on the outlook for Canadian growth and inflation.

Sean Kilpatrick comments in the Globe:

Heading into the rate announcement, the bank was expected to keep rates unchanged this month. However, some economists were predicting a rate cut as soon as the bank’s next decision, in late October. The Canadian dollar climbed after the statement’s release, as the bank’s tone dampened market expectations that a rate cut is on the horizon.

… and, by the time the close rolled around:

Separately, data showed Canada posted a bigger-than-expected trade deficit in July, a sign that the boost to the domestic economy from trade in the second quarter may not be repeated.

…

The Canadian dollar posted its biggest gain in seven months against the greenback on Wednesday on lowered expectations for a Bank of Canada interest rate cut in October after the central bank’s policy decision made no mention of future moves.

TXPR closed at 586.52, up 0.77% on the day. Volume was 2.36-million, about average in the context of the past thirty days.

CPD closed at 11.74, up 0.95% on the day. Volume of 155,166 was quite high but not extraordinary in the context of the past 30 days.

ZPR closed at 9.39, up 1.29% on the day. Volume of 232,279 was a little above average in the context of the past 30 days.

Five-year Canada yields were up 2bp to 1.15% today.

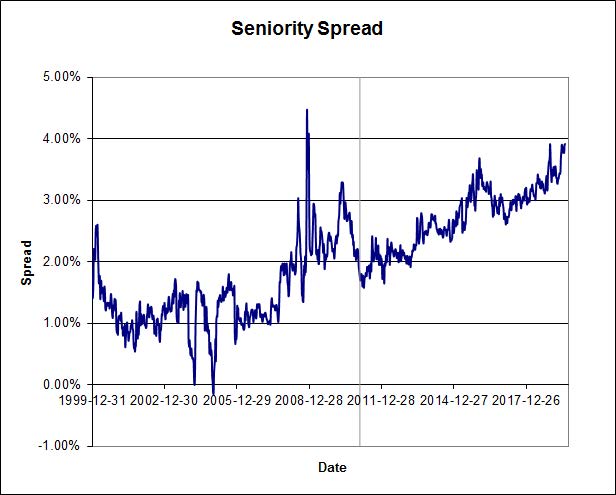

PerpetualDiscounts now yield 5.64%, equivalent to 7.33% interest at the standard equivalency factor of 1.3x. Long corporates now yield 3.18%, so the pre-tax interest-equivalent spread (in this context, the “Seniority Spread”) has narrowed slightly (and perhaps spuriously) to 415bp, close to the post-Credit Crunch record of 420bp set August 28. The latter value is second only to the 445bp recorded November 26, 2008, a day on which

The TXPR index was down 5.94% on the BCE news.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0000 % | 1,802.5 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0000 % | 3,307.6 |

| Floater | 6.63 % | 6.72 % | 67,519 | 12.79 | 4 | 0.0000 % | 1,906.2 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0507 % | 3,381.1 |

| SplitShare | 4.66 % | 4.43 % | 60,602 | 4.06 | 7 | -0.0507 % | 4,037.7 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0507 % | 3,150.4 |

| Perpetual-Premium | 5.61 % | -18.56 % | 62,090 | 0.09 | 6 | 0.2283 % | 2,982.5 |

| Perpetual-Discount | 5.50 % | 5.64 % | 67,087 | 14.40 | 28 | 0.3490 % | 3,108.4 |

| FixedReset Disc | 5.66 % | 5.33 % | 179,307 | 14.80 | 73 | 1.4043 % | 2,018.5 |

| Deemed-Retractible | 5.32 % | 6.10 % | 68,840 | 7.91 | 27 | 0.2757 % | 3,092.9 |

| FloatingReset | 4.66 % | 7.14 % | 65,489 | 7.99 | 3 | -0.0810 % | 2,281.4 |

| FixedReset Prem | 5.27 % | 4.21 % | 138,125 | 1.63 | 14 | 0.3848 % | 2,571.9 |

| FixedReset Bank Non | 1.98 % | 4.28 % | 95,153 | 2.33 | 3 | -0.3338 % | 2,649.9 |

| FixedReset Ins Non | 5.56 % | 8.01 % | 101,669 | 8.02 | 21 | 1.1704 % | 2,072.5 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BNS.PR.I | FixedReset Disc | 1.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 19.81 Evaluated at bid price : 19.81 Bid-YTW : 4.97 % |

| BAM.PR.M | Perpetual-Discount | 1.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 20.35 Evaluated at bid price : 20.35 Bid-YTW : 5.95 % |

| TD.PF.A | FixedReset Disc | 1.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 16.50 Evaluated at bid price : 16.50 Bid-YTW : 5.19 % |

| TD.PF.D | FixedReset Disc | 1.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 18.24 Evaluated at bid price : 18.24 Bid-YTW : 5.43 % |

| RY.PR.Z | FixedReset Disc | 1.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 17.13 Evaluated at bid price : 17.13 Bid-YTW : 5.06 % |

| MFC.PR.C | Deemed-Retractible | 1.14 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2030-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.42 Bid-YTW : 7.02 % |

| GWO.PR.S | Deemed-Retractible | 1.16 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2030-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.55 Bid-YTW : 6.00 % |

| BIP.PR.A | FixedReset Disc | 1.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 17.20 Evaluated at bid price : 17.20 Bid-YTW : 6.84 % |

| TD.PF.K | FixedReset Disc | 1.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 19.51 Evaluated at bid price : 19.51 Bid-YTW : 5.15 % |

| TD.PF.C | FixedReset Disc | 1.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 16.25 Evaluated at bid price : 16.25 Bid-YTW : 5.29 % |

| BNS.PR.G | FixedReset Prem | 1.25 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-07-25 Maturity Price : 25.00 Evaluated at bid price : 25.89 Bid-YTW : 3.87 % |

| CM.PR.T | FixedReset Disc | 1.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 22.56 Evaluated at bid price : 23.50 Bid-YTW : 4.95 % |

| MFC.PR.R | FixedReset Ins Non | 1.30 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2030-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.45 Bid-YTW : 5.75 % |

| IFC.PR.G | FixedReset Ins Non | 1.30 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2030-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.70 Bid-YTW : 8.01 % |

| NA.PR.S | FixedReset Disc | 1.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 16.95 Evaluated at bid price : 16.95 Bid-YTW : 5.47 % |

| NA.PR.C | FixedReset Disc | 1.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 20.37 Evaluated at bid price : 20.37 Bid-YTW : 5.64 % |

| CM.PR.P | FixedReset Disc | 1.36 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 15.70 Evaluated at bid price : 15.70 Bid-YTW : 5.47 % |

| GWO.PR.P | Deemed-Retractible | 1.36 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2030-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.90 Bid-YTW : 5.96 % |

| MFC.PR.I | FixedReset Ins Non | 1.37 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2030-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.54 Bid-YTW : 7.81 % |

| BAM.PF.B | FixedReset Disc | 1.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 16.98 Evaluated at bid price : 16.98 Bid-YTW : 5.96 % |

| TRP.PR.A | FixedReset Disc | 1.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 12.55 Evaluated at bid price : 12.55 Bid-YTW : 6.12 % |

| TD.PF.B | FixedReset Disc | 1.42 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 17.18 Evaluated at bid price : 17.18 Bid-YTW : 5.13 % |

| CM.PR.R | FixedReset Disc | 1.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 20.61 Evaluated at bid price : 20.61 Bid-YTW : 5.53 % |

| BMO.PR.W | FixedReset Disc | 1.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 16.28 Evaluated at bid price : 16.28 Bid-YTW : 5.20 % |

| BAM.PF.A | FixedReset Disc | 1.54 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 18.48 Evaluated at bid price : 18.48 Bid-YTW : 5.93 % |

| RY.PR.M | FixedReset Disc | 1.55 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 17.66 Evaluated at bid price : 17.66 Bid-YTW : 5.35 % |

| MFC.PR.H | FixedReset Ins Non | 1.61 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2030-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.24 Bid-YTW : 6.89 % |

| IAF.PR.I | FixedReset Ins Non | 1.63 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2030-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.70 Bid-YTW : 7.88 % |

| IFC.PR.C | FixedReset Ins Non | 1.64 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2030-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.36 Bid-YTW : 8.24 % |

| CM.PR.S | FixedReset Disc | 1.66 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 17.80 Evaluated at bid price : 17.80 Bid-YTW : 5.39 % |

| BMO.PR.F | FixedReset Disc | 1.71 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 22.70 Evaluated at bid price : 23.80 Bid-YTW : 4.98 % |

| RY.PR.J | FixedReset Disc | 1.72 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 18.30 Evaluated at bid price : 18.30 Bid-YTW : 5.33 % |

| BAM.PR.T | FixedReset Disc | 1.73 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 14.12 Evaluated at bid price : 14.12 Bid-YTW : 6.24 % |

| PWF.PR.T | FixedReset Disc | 1.75 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 17.45 Evaluated at bid price : 17.45 Bid-YTW : 5.35 % |

| HSE.PR.E | FixedReset Disc | 1.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 17.30 Evaluated at bid price : 17.30 Bid-YTW : 6.81 % |

| BMO.PR.Y | FixedReset Disc | 1.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 18.40 Evaluated at bid price : 18.40 Bid-YTW : 5.27 % |

| MFC.PR.M | FixedReset Ins Non | 1.82 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2030-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.69 Bid-YTW : 9.14 % |

| GWO.PR.N | FixedReset Ins Non | 1.84 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2030-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.85 Bid-YTW : 9.12 % |

| HSE.PR.C | FixedReset Disc | 1.91 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 16.01 Evaluated at bid price : 16.01 Bid-YTW : 6.69 % |

| NA.PR.G | FixedReset Disc | 1.95 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 19.34 Evaluated at bid price : 19.34 Bid-YTW : 5.44 % |

| MFC.PR.Q | FixedReset Ins Non | 1.95 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2030-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.27 Bid-YTW : 8.01 % |

| CM.PR.O | FixedReset Disc | 1.96 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 16.62 Evaluated at bid price : 16.62 Bid-YTW : 5.39 % |

| IAF.PR.G | FixedReset Ins Non | 1.98 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2030-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.50 Bid-YTW : 7.57 % |

| MFC.PR.G | FixedReset Ins Non | 1.99 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2030-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.91 Bid-YTW : 8.10 % |

| NA.PR.W | FixedReset Disc | 2.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 15.38 Evaluated at bid price : 15.38 Bid-YTW : 5.58 % |

| BAM.PF.E | FixedReset Disc | 2.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 15.50 Evaluated at bid price : 15.50 Bid-YTW : 6.14 % |

| TD.PF.J | FixedReset Disc | 2.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 20.37 Evaluated at bid price : 20.37 Bid-YTW : 4.99 % |

| BAM.PR.Z | FixedReset Disc | 2.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 17.67 Evaluated at bid price : 17.67 Bid-YTW : 6.11 % |

| BIP.PR.F | FixedReset Disc | 2.36 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 21.35 Evaluated at bid price : 21.65 Bid-YTW : 5.89 % |

| PWF.PR.P | FixedReset Disc | 2.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 12.50 Evaluated at bid price : 12.50 Bid-YTW : 5.48 % |

| MFC.PR.N | FixedReset Ins Non | 2.44 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2030-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.51 Bid-YTW : 9.23 % |

| SLF.PR.H | FixedReset Ins Non | 2.54 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2030-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.75 Bid-YTW : 8.67 % |

| BAM.PF.F | FixedReset Disc | 2.57 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 16.77 Evaluated at bid price : 16.77 Bid-YTW : 6.09 % |

| BMO.PR.D | FixedReset Disc | 2.81 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 20.85 Evaluated at bid price : 20.85 Bid-YTW : 5.23 % |

| RY.PR.S | FixedReset Disc | 2.88 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 19.62 Evaluated at bid price : 19.62 Bid-YTW : 4.92 % |

| BAM.PR.X | FixedReset Disc | 2.89 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 12.47 Evaluated at bid price : 12.47 Bid-YTW : 5.93 % |

| EMA.PR.C | FixedReset Disc | 2.92 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 17.65 Evaluated at bid price : 17.65 Bid-YTW : 5.74 % |

| BAM.PR.R | FixedReset Disc | 3.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 14.43 Evaluated at bid price : 14.43 Bid-YTW : 5.99 % |

| CU.PR.G | Perpetual-Discount | 3.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 21.25 Evaluated at bid price : 21.25 Bid-YTW : 5.33 % |

| CM.PR.Q | FixedReset Disc | 3.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 17.78 Evaluated at bid price : 17.78 Bid-YTW : 5.57 % |

| TD.PF.I | FixedReset Disc | 3.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 21.06 Evaluated at bid price : 21.06 Bid-YTW : 5.06 % |

| BMO.PR.T | FixedReset Disc | 3.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 16.82 Evaluated at bid price : 16.82 Bid-YTW : 5.06 % |

| BAM.PF.G | FixedReset Disc | 4.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 16.96 Evaluated at bid price : 16.96 Bid-YTW : 6.03 % |

| HSE.PR.G | FixedReset Disc | 4.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 17.35 Evaluated at bid price : 17.35 Bid-YTW : 6.73 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| PWF.PR.P | FixedReset Disc | 119,008 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 12.50 Evaluated at bid price : 12.50 Bid-YTW : 5.48 % |

| TD.PF.E | FixedReset Disc | 103,300 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 18.50 Evaluated at bid price : 18.50 Bid-YTW : 5.46 % |

| MFC.PR.M | FixedReset Ins Non | 102,755 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2030-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.69 Bid-YTW : 9.14 % |

| PWF.PR.T | FixedReset Disc | 81,741 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 17.45 Evaluated at bid price : 17.45 Bid-YTW : 5.35 % |

| CM.PR.Y | FixedReset Disc | 74,397 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 22.95 Evaluated at bid price : 24.40 Bid-YTW : 5.02 % |

| TD.PF.B | FixedReset Disc | 57,789 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-09-04 Maturity Price : 17.18 Evaluated at bid price : 17.18 Bid-YTW : 5.13 % |

| There were 34 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| BAM.PR.T | FixedReset Disc | Quote: 14.12 – 14.75 Spot Rate : 0.6300 Average : 0.4685 YTW SCENARIO |

| IFC.PR.C | FixedReset Ins Non | Quote: 17.36 – 17.92 Spot Rate : 0.5600 Average : 0.4241 YTW SCENARIO |

| GWO.PR.F | Deemed-Retractible | Quote: 25.43 – 25.80 Spot Rate : 0.3700 Average : 0.2383 YTW SCENARIO |

| NA.PR.G | FixedReset Disc | Quote: 19.34 – 19.70 Spot Rate : 0.3600 Average : 0.2327 YTW SCENARIO |

| SLF.PR.J | FloatingReset | Quote: 12.51 – 12.89 Spot Rate : 0.3800 Average : 0.2765 YTW SCENARIO |

| RY.PR.H | FixedReset Disc | Quote: 17.01 – 17.33 Spot Rate : 0.3200 Average : 0.2231 YTW SCENARIO |