Assiduous Reader B writes in and says:

I am a subscriber to your monthly newsletter but haven’t notice anything recent on this issue

My question is why would investors embrace the new issue at a yield of 4.50% while selling down the existing A issue which is now paying a yield that is a full percentage point higher.

I recognize the higher reset rate but the yield spread still seems excessive.

Thanks for your assistance

So, since he’s a customer I answered; and I said:

I will address your question in a post on prefblog.com tonight, but in the meantime can you tell me why you believe that HSE.PR.A is yielding a full percentage point higher?

… and he responded:

Thanks James for getting back to me – according to my screen on TD, HSE PR A is yielding 5.68 – the new issue is yielding 4.50% – I know there is something to be said for the extra reset pickup but the difference in current yield seems excessive

… and he included a picture:

Click for Big

OK, so his first mistake is getting advice – even advice on such a simple thing as yield – from a bank. You should never seek advice or analysis from a bank, because they’re all domeless wonderboys, with about enough brains to say “We’re big!” and not much else.

In this particular case, TD has told him that the yield on HSE.PR.A, when quoted at 19.56-59, is 5.6789%, which a little experimentation tells us, is the Current Yield Ask, that is to say, the Current Dividend, 1.1125, divided by the Ask Price of 19.59, equals 5.6789178%, where I have tacked another three decimal places on to their reported figure just to sneer at the bank and their precious four decimal places of meaningless precision.

Never Use Current Yield When Analyzing Preferreds

It isn’t even accurate when evaluating Straight Perpetuals (since the relationship between the calculation date and the next payment date is a significant source of error), and is absolutely hopeless when evaluating something that may be called (which is not important in this case) or which is expected to experience a change in dividend (which is very important in this case).

Assiduous Reader B has made the mistake of assuming that the Issue Reset Spread is of minor importance, a mere adjustment to Current Yield, but in this case the projected dividend is so different from the current dividend that he’s wrong.

HSE.PR.A is a FixedReset, 4.45%+173, that commenced trading 2011-3-18 after being announced 2011-3-10. It resets in March, 2016, and if the GOC-5 yield continues to be at its yield of 1.45%, the reset rate will be 3.18%, a 29% drop from current levels.

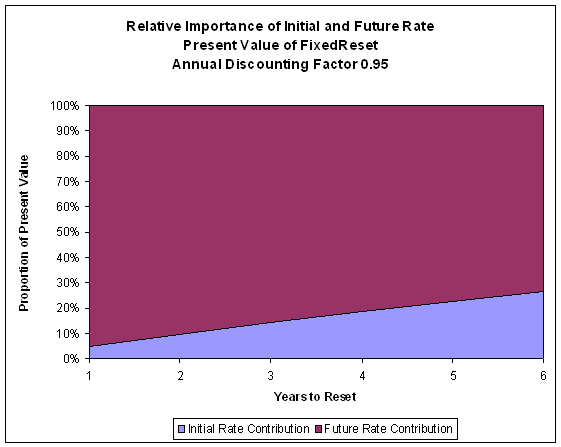

One chart I am particularly fond of illustrates the relative importance of the Current Dividend vs. the Issue Reset Spread for FixedResets that may be assumed to be perpetual (which is a pretty good bet in this case):

Click For Big

Given that HSE.PR.A resets in a little over one year, we see that the headline figure, 4.45%, contributes less than 10% of the valuation of the instrument – all the rest is entirely up to the Issue Reset Spread.

So, given that we know the importance of the Issue Reset Spread, how can we work out the all in yield of the issue in order to allow us to compare HSE.PR.A to the new issue, which is a FixedReset, 4.50%+313?

The answer is to use the Yield Calculator for Resets, which is an Excel Spreadsheet I have made available to the public, linked on the Right-Hand Navigation Panel under the heading “Calculators”. [Update: Note that this calculator has been improved since this post was written; the input of the data has been simplified. … JH 2015-8-7] It should be noticed that this is not a magic black box, nor is it particularly sophisticated. It’s simply a tool to allow a schedule of cash flows to be input into a spreadsheet easily. So to use the tool, we input our data into the yellow boxes. We’ll get the results of the calculation in the green boxes and the calculation is performed in the turquoise boxes;; we don’t touch them. Only touch the yellow boxes:

- Current Price: we’ll put in 19.59, because that’s what the bank used.

- Call Price: You can put in the call price here, but we’re not expecting the issue to be called – we expect it to remain outstanding in 25 years. So what will the price be in 25 years? There are various approaches to this, one of which is discussed in PrefLetter, but it’s reasonable to assume that in 25 years it will be priced the same as it is now, so we’ll put in 19.59. If you don’t like 19.59, put in some other number. It’s not magic. The Yield Calculation Police won’t take you away if you put in some other number. But your calculation is only as good as your assumptions, so if you calculate a very high yield by inputting some silly price – like $50.00 – as the end-price, well, your calculation is only as good as your assumptions.

- Settlement Date: Strictly speaking, we should put in the date that a trade executed today will settle (2014-12-9), but I usually use the Trade Date, on the grounds that the bank won’t even let you enter the order unless you’ve got money available RIGHT NOW to pay for it. So I’ll input 2014-12-4.

- Call Date: If it was priced at $26.00 and I was expecting it to be called, I would put in the call date. But I expect it to be around in twenty-five years (the maximum allowable in this spreadsheet) so I’ll put in 2039-12-4. Again, it’s up to you. If detailed examination of the numerological code embedded in The Gospel According To St. Mark has convinced you that it will be priced at 21.13 on 2028-7-8, go ahead and put in that call price and that date. Don’t worry about the Yield Calculation Police, I’ve paid them off.

- Quarterly Dividend: So what dividend does it pay right now, expressed as a quarterly amount? I hate using a calculator to calculate six decimal places, so I will input a tiny Excel formula “=25 * 0.0445 / 4”, that is, “equal to the par value times the annual coupon rate divided by four”.

- Cycle: This gets a little tricky, because we need to know the pay-date of each dividend. A little research tells us it’s paid on the last day of each quarter, March / June / September / December, which is cycle 3. So plug in “3”

- Pay Date: So what day of these months? It’s the last day, so plug in “31”. In the cash flow schedule, the calculated date “June 31” will be transformed to “July 1”, as you can see in the turquoise area to the right of the data input area. This is a bit of an error, but a very tiny one.

- Include First Dividend: This is quite important. As the spreadsheet tells you, the next dividend payment is December 31, based on the information you’ve input above. If you buy it today, will you earn that dividend? You’ll have to look up the ex-dividend date for the issue; in this case the ex-dividend date was 2014-11-25, which is now in the past, so you WON’T get the next dividend, so input “0”

- First Dividend Value: For most issues, the first dividend payment is for a different amount from the others, since it’s adjusted to reflect the time from the security’s issue to the pay date, rather than pay-date to pay-date. HSE.PR.A has been around for a long time, so this does not apply and we’re not even earning the next dividend anyway, so it doubly doesn’t matter. Leave this field blank.

- Reset Date: The issue resets 2016-3-31. Plug in this date

- Quarterly Dividend After Reset: This is the moment we’ve all been waiting for! We have to estimate what the dividend will be after the reset, while bearing in mind that the yield we calculate will only be as good as our estimates. It’s generally best to assume that major market yields will not change; that on the reset calculation date the 5-year GOC yield will be the same as it is today, 1.45%. But if you feel this is unreasonable, put in another number you’re more comfortable with. If you think that 1.45% is ridiculous and that GOC-5 will be 2.00% on recalculation day, use 2.00%. You have to use some kind of assumption, there’s no way around that. We will note that TD’s calculation, in using Current Yield, assumed the dividend would not change; i.e., that the dividend would reset to be equal to the 4.45% it is currently, i.e., that GOC-5 on reset calculation date will be 2.72%. Well, if that’s the number you want to use, go ahead. It’s a free country and you can assume anything you like. Just remember that the quality of your yield estimate will reflect the quality of your assumptions; and also remember that consistency is a virtue, so if two issues are resetting at the same time, you should use the same estimate for GOC-5. But I will assume a future GOC-5 rate of 1.45%, so I’ll input the Excel formula “=25 * (0.0145 + 0.0173) / 4” = par value * (sum of assumed GOC-5 rate and Issue Reset Spread [expressed annually]) divided by 4 [quarters per year]. We should also note that the spreadsheet makes no provision for changes in GOC-5, so if you feel that GOC-5 will be 2.00% on the 2016 reset calculation date, but 3.00% on the 2021 reset calculation date, you’ll have to develop your own elaboration of this spreadsheet.

And that’s the end of our input and our answer pops up in the green boxes! Current Yield, 5.68%, just as advertised by TD, but an Annualized Quarterly Yield To Call of 4.17%. That’s quite a difference! And, I will note, it is substantially less than the New Issue FixedReset, 4.50%+313. Implied Volatility Theory tells us to expect less for a deeply discounted issue compared to one at or near par value, but just how much less it should be is a whole ‘nuther issue.

And, I suggest, you should always think of this number as “4.17%, assuming an end-price of 19.59 and a constant GOC-5 of 1.45%”, just to remind yourself of the two critical assumptions you made.

So there you have it. I suggest that those interested in using this spreadsheet as an adjunct to their trading first check all the calculations – Trust But Verify! – and second, play around with it a bit. Change the assumptions of end-price and GOC-5 estimate on reset, see how sensitive the answers are to the inputs. The better you understand your data, the better an investor you’ll be.

[…] a detailed numerical example for the use of this calculator in the post What is the Yield of HSE.PR.A?. This explanation is based on the old version, but if you can’t figure out the layout […]

[…] we plug the above data into the yield calculator for resets (which is discussed here and has recently been slightly modified), we arrive at a annualized (compounded semi-annually) […]

[…] we plug the above data into the yield calculator for resets (which is discussed here and has recently been slightly modified), we arrive at a annualized (compounded semi-annually) […]

[…] we plug the above data into the yield calculator for resets (which is discussed here and has recently been slightly modified), we arrive at a annualized (compounded semi-annually) […]

[…] we plug the above data into the yield calculator for resets (which is discussed here and has recently been slightly modified), we arrive at a annualized (compounded semi-annually) […]

[…] we plug the above data into the yield calculator for resets (which is discussed here), we arrive at a quarterly annualized yield of 8.25% for RY.PR.J (this is quarterly compounded […]

[…] we plug the above data into the yield calculator for resets (which is discussed here), we arrive at a quarterly annualized yield of 7.28% for RY.PR.J (this is quarterly compounded […]