Greek bank depositors not only have to deal with the potential for bank failure should Greece exit the Euro, but I’m sure they’re also worried about a punitive tax on deposits in good banks. So they’ve found another option:

Click for Big

It nice to see a supervisor fired for poor supervision:

Citigroup Inc. fired a trader on Friday for allegedly mismarking an inflation-options book and dismissed his boss for lax oversight, according to a person familiar with the matter.

Carl Bonde lost his job in New York after the bank determined he’d inflated the value of his trading positions by less than $30 million, the person said. Keith Price, head of U.S. inflation trading, was dismissed for his failure to supervise Bonde, said the person, who asked not to be identified discussing a personnel matter.

How ’bout them equities, eh?

Global stocks powered to their best weekly rally in nearly two years, sending two of the biggest equity benchmarks to the brink of records, on speculation the U.S. Federal Reserve will leave interest rates at zero past mid-year while European policy makers press stimulus.

The MSCI All-Country World Index surged 3.2 percent for the five days, pushing the Nasdaq Composite Index to within 7 points of wiping out all its losses since the Internet bubble. The Stoxx Europe 600 Index soared 1.9 percent to close 0.4 percent from its March 2000 high.

…

Other benchmark indexes also gained during the week. The Standard & Poor’s 500 Index rose 2.7 percent to 2,108.10 in the five days, 0.4 percent away from a record. In London, the FTSE 100 Index hit a fresh record, climbing above 7,000 for the first time. The Russell 2000 Index gained 2.8 percent to an all-time high.

Capital Power Corporation, proud issuer of CPX.PR.A, CPX.PR.C and CPX.PR.E, has been confirmed at Pfd-3(low) by DBRS:

DBRS Limited (DBRS) has today confirmed the rating of the Preferred Shares of Capital Power Corporation (CPC or the Company) at Pfd-3 (low) with a Stable trend. CPC’s Preferred Shares rating is based on the credit quality of its subsidiary, Capital Power L.P. (CPLP; rated BBB). Please see the CPLP rating report dated March 20, 2015, for more information on the credit quality of CPLP. The one-notch differential in the ratings of CPC and CPLP reflects the structural subordination at CPC.

…

CPC’s financial risk profile is based on its deconsolidated credit metrics. As CPC has no bonds/debentures issued at the parent level and is not expected to issue any debt in the foreseeable future, its adjusted leverage primarily consists of its preferred shares outstanding, which are treated as debt by DBRS. In the adjusted debt-to-capital calculation, the amount of preferred shares over the 20% preferred shares-to-equity threshold (defined as the percentage of preferred shares outstanding divided by total equity, excluding preferreds and minority interest) is treated as debt by DBRS. In 2014, CPC had $464 million of preferred shares outstanding, of which $67 million was treated as debt. As such, CPC’s unconsolidated debt-to-capital ratio was approximately 3% in 2014, which remains supportive of the current rating category. In addition, the unconsolidated fixed charge coverage ratio is expected to remain high at around five times.

It was a good day for the Canadian preferred share market, with PerpetualDiscounts winning 78bp, FixedResets up 10bp and DeemedRetractibles gaining 2bp. The Performance Highlights table has a good length, capped by winning PerpetualDiscounts. Volume was extremely high.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

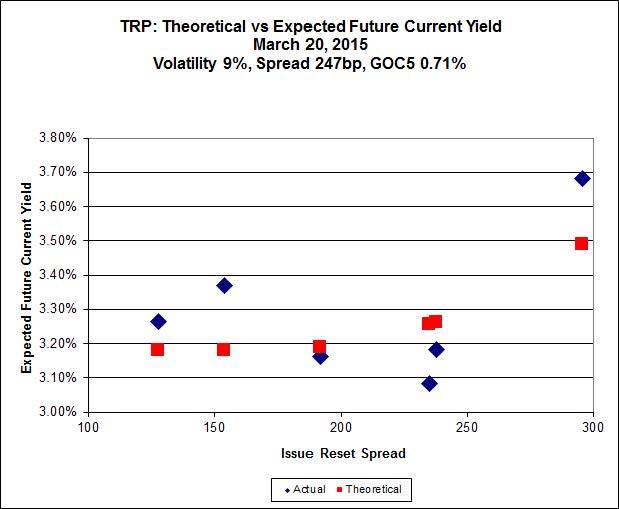

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 24.81 to be $1.31 rich, while TRP.PR.G, resetting 2020-11-30 at +296, is $1.37 cheap at its bid price of 24.92.

Click for Big

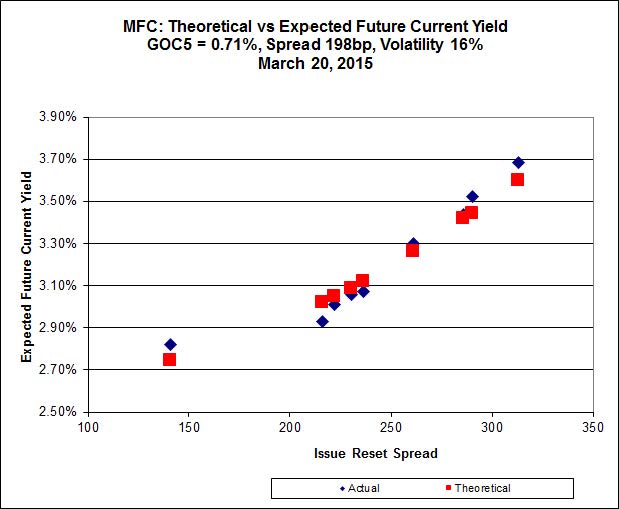

Another excellent fit, but the numbers are perplexing. Implied Volatility for MFC continues to be a conundrum, although it declined substantially today. It is still too high if we consider that NVCC rules will never apply to these issues; it is still too low if we consider them to be NVCC non-compliant issues (and therefore with Deemed Maturities in the call schedule).

Most expensive is MFC.PR.L, resetting at +216 on 2019-6-19, bid at 24.48 to be $0.72 rich, while MFC.PR.H, resetting at +313bp on 2017-3-19, is bid at 26.05 to be $0.63 cheap.

Click for Big

The fit on this series is actually quite reasonable – it’s the scale that makes it look so weird.

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 21.53 to be $0.56 cheap. BAM.PF.E, resetting at +255bp 2020-3-31 is bid at 24.51 and appears to be $0.93 rich

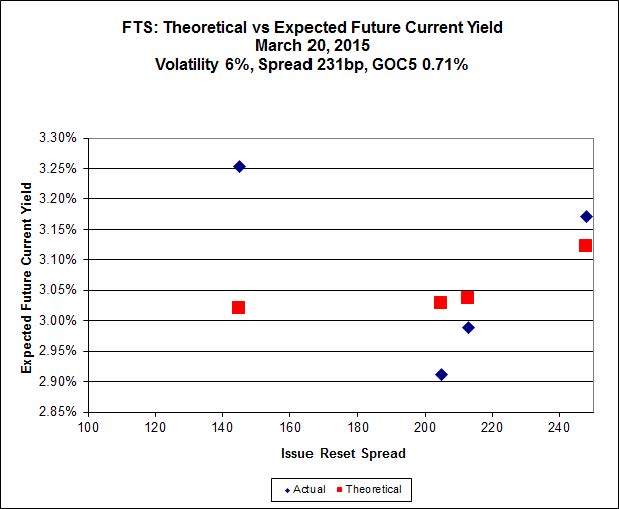

Click for Big

This is just weird because the middle is expensive and the ends are cheap but anyway … FTS.PR.H, with a spread of +145bp, and bid at 16.60, looks $1.28 cheap and resets 2015-6-1. FTS.PR.K, with a spread of +205bp and resetting 2019-3-1, is bid at 23.70 and is $0.92 rich.

Click for Big

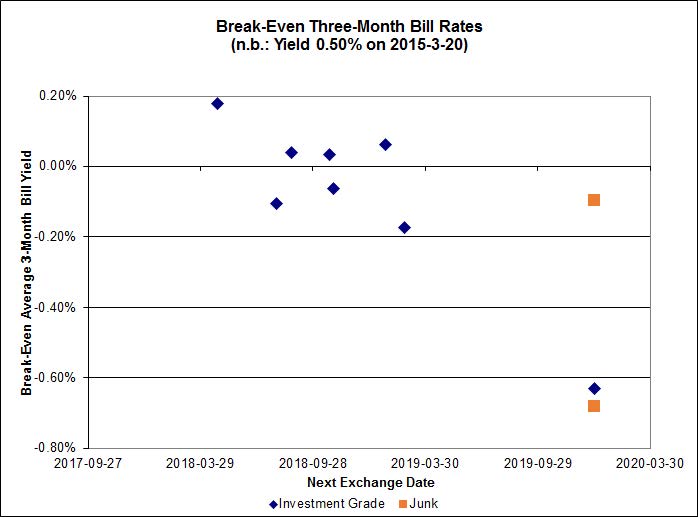

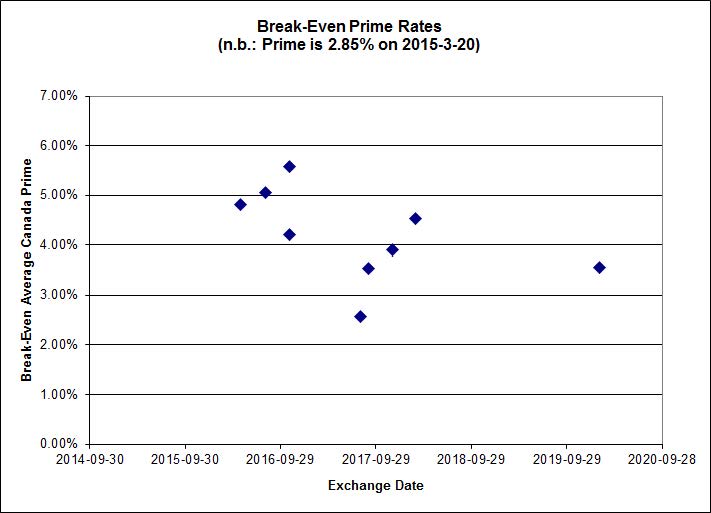

Investment-grade pairs predict an average over the next five years of about 0.00% – except for one outlier, TRP.PR.A / TRP.PR.F, which has a break-even of -0.63%. The DC.PR.B / DC.PR.D pair has gone from the extreme to the ludicrous and now predicts an average bill rate over the next 4 3/4 years of -2.36%

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -3.1190 % | 2,282.9 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -3.1190 % | 3,991.5 |

| Floater | 3.32 % | 3.21 % | 63,097 | 19.21 | 3 | -3.1190 % | 2,426.9 |

| OpRet | 4.07 % | 0.93 % | 105,377 | 0.25 | 1 | -0.0397 % | 2,765.8 |

| SplitShare | 4.46 % | 4.31 % | 57,630 | 4.43 | 5 | -0.1429 % | 3,216.8 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0397 % | 2,529.1 |

| Perpetual-Premium | 5.29 % | 1.26 % | 57,461 | 0.09 | 25 | 0.0516 % | 2,522.3 |

| Perpetual-Discount | 4.96 % | 5.02 % | 172,159 | 15.24 | 9 | 0.7483 % | 2,822.9 |

| FixedReset | 4.38 % | 3.42 % | 241,019 | 16.83 | 85 | 0.0976 % | 2,432.4 |

| Deemed-Retractible | 4.90 % | -1.43 % | 112,770 | 0.11 | 37 | 0.0171 % | 2,659.5 |

| FloatingReset | 2.49 % | 2.90 % | 86,537 | 6.31 | 8 | -0.0748 % | 2,333.7 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BAM.PR.K | Floater | -9.54 % | A nonsensical closing bid, courtesy of those hard-working bank employees at the Toronto Stock Exchange. The issue traded 4,040 shares in a range of 15.41-72. As with the same issue on March 10, it is not clear whether this is due to inadequate Toronto Stock Exchange reporting or inadequate Toronto Stock Exchange supervision of market-makers. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-20 Maturity Price : 14.03 Evaluated at bid price : 14.03 Bid-YTW : 3.55 % |

| ENB.PR.Y | FixedReset | -1.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-20 Maturity Price : 20.15 Evaluated at bid price : 20.15 Bid-YTW : 4.14 % |

| TRP.PR.F | FloatingReset | -1.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-20 Maturity Price : 18.80 Evaluated at bid price : 18.80 Bid-YTW : 3.25 % |

| SLF.PR.H | FixedReset | -1.28 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.36 Bid-YTW : 4.39 % |

| CGI.PR.D | SplitShare | -1.21 % | YTW SCENARIO Maturity Type : Soft Maturity Maturity Date : 2023-06-14 Maturity Price : 25.00 Evaluated at bid price : 25.30 Bid-YTW : 3.60 % |

| BNS.PR.Z | FixedReset | 1.03 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.55 Bid-YTW : 3.33 % |

| IAG.PR.G | FixedReset | 1.10 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2017-06-30 Maturity Price : 25.00 Evaluated at bid price : 25.69 Bid-YTW : 2.99 % |

| BAM.PR.R | FixedReset | 1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-20 Maturity Price : 21.53 Evaluated at bid price : 21.53 Bid-YTW : 3.69 % |

| MFC.PR.L | FixedReset | 1.16 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.48 Bid-YTW : 3.62 % |

| CIU.PR.C | FixedReset | 1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-20 Maturity Price : 16.86 Evaluated at bid price : 16.86 Bid-YTW : 3.25 % |

| BAM.PR.N | Perpetual-Discount | 1.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-20 Maturity Price : 22.70 Evaluated at bid price : 23.04 Bid-YTW : 5.15 % |

| BAM.PF.C | Perpetual-Discount | 1.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-20 Maturity Price : 23.12 Evaluated at bid price : 23.45 Bid-YTW : 5.17 % |

| CU.PR.F | Perpetual-Discount | 1.61 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-20 Maturity Price : 23.63 Evaluated at bid price : 24.00 Bid-YTW : 4.71 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| RY.PR.M | FixedReset | 276,913 | Recent inventory blow-out. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-20 Maturity Price : 22.99 Evaluated at bid price : 24.61 Bid-YTW : 3.36 % |

| POW.PR.D | Perpetual-Premium | 230,738 | Nesbitt crossed blocks of 50,000 shares, 110,600 and 60,000, all at 25.25. YTW SCENARIO Maturity Type : Call Maturity Date : 2015-04-19 Maturity Price : 25.00 Evaluated at bid price : 25.30 Bid-YTW : 1.26 % |

| IAG.PR.G | FixedReset | 167,264 | Nesbitt crossed 160,600 at 25.60. YTW SCENARIO Maturity Type : Call Maturity Date : 2017-06-30 Maturity Price : 25.00 Evaluated at bid price : 25.69 Bid-YTW : 2.99 % |

| NA.PR.S | FixedReset | 162,676 | TD crossed 125,000 at 25.40. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-20 Maturity Price : 23.34 Evaluated at bid price : 25.32 Bid-YTW : 3.15 % |

| RY.PR.J | FixedReset | 157,750 | RBC crossed 69,800 at 24.99 and 16,000 at 25.00. RBC bought blocks of 17,700 and 19,900 from Nesbitt at 24.99. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-20 Maturity Price : 23.14 Evaluated at bid price : 24.97 Bid-YTW : 3.40 % |

| ENB.PR.N | FixedReset | 146,462 | RBC crossed 139,000 at 21.00. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-20 Maturity Price : 21.00 Evaluated at bid price : 21.00 Bid-YTW : 4.20 % |

| BMO.PR.S | FixedReset | 142,232 | Nesbitt crossed 48,300 at 25.06. RBC crossed 52,800 at 25.06 and 25,000 at 25.12. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-20 Maturity Price : 23.30 Evaluated at bid price : 25.20 Bid-YTW : 3.08 % |

| RY.PR.E | Deemed-Retractible | 137,605 | Nesbitt crossed blocks of 65,100 and 70,000, both at 25.55. YTW SCENARIO Maturity Type : Call Maturity Date : 2015-04-19 Maturity Price : 25.25 Evaluated at bid price : 25.57 Bid-YTW : -7.21 % |

| ENB.PR.D | FixedReset | 105,044 | RBC crossed blocks of 35,000 and 51,400 at 19.54. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-20 Maturity Price : 19.40 Evaluated at bid price : 19.40 Bid-YTW : 4.21 % |

| CM.PR.Q | FixedReset | 102,874 | RBC crossed 35,500 at 24.87. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-20 Maturity Price : 23.09 Evaluated at bid price : 24.86 Bid-YTW : 3.45 % |

| ENB.PR.F | FixedReset | 102,498 | Nesbitt sold 18,500 to RBC at 20.00 and crossed 42,900 at the same price. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-20 Maturity Price : 19.92 Evaluated at bid price : 19.92 Bid-YTW : 4.26 % |

| BMO.PR.T | FixedReset | 101,392 | TD crossed 50,000 and 45,000 at 24.95. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-20 Maturity Price : 23.10 Evaluated at bid price : 24.71 Bid-YTW : 3.09 % |

| There were 49 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| BAM.PR.K | Floater | Quote: 14.03 – 15.89 Spot Rate : 1.8600 Average : 1.1308 YTW SCENARIO |

| CGI.PR.D | SplitShare | Quote: 25.30 – 25.80 Spot Rate : 0.5000 Average : 0.3579 YTW SCENARIO |

| TD.PR.Z | FloatingReset | Quote: 23.85 – 24.26 Spot Rate : 0.4100 Average : 0.2781 YTW SCENARIO |

| MFC.PR.K | FixedReset | Quote: 24.32 – 24.80 Spot Rate : 0.4800 Average : 0.3627 YTW SCENARIO |

| BMO.PR.R | FloatingReset | Quote: 23.90 – 24.20 Spot Rate : 0.3000 Average : 0.2021 YTW SCENARIO |

| ENB.PR.T | FixedReset | Quote: 20.48 – 20.79 Spot Rate : 0.3100 Average : 0.2233 YTW SCENARIO |