TD.PF.E, a FixedReset, 3.70%+287, announced April 15 has settled. It will be tracked by HIMIPref™ and has been assigned to the FixedReset subindex.

The issue traded 832,925 shares today (consolidated exchanges) in a range of 24.79-93 before closing at 24.91-92.

Vital statistics are:

| TD.PF.E | FixedReset | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-04-24 Maturity Price : 23.10 Evaluated at bid price : 24.91 Bid-YTW : 3.62 % |

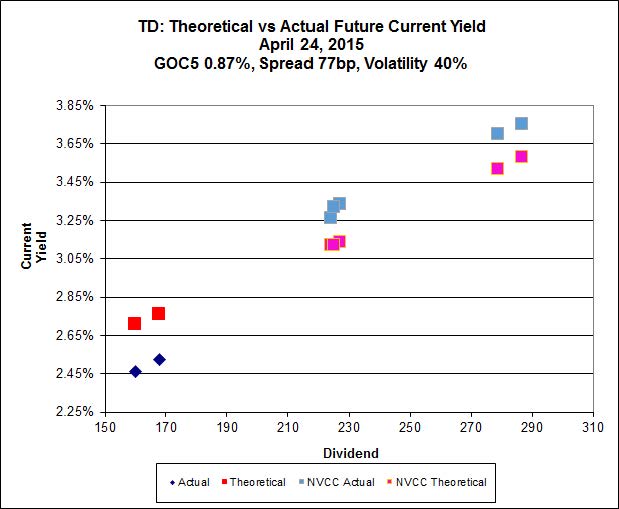

The calculation for Implied Volatility is a mess with a very poor fit, but this is due to the presence of two NVCC non-compliant issues that are, quite correctly, priced by the market using a different paradigm than the five NVCC compliant issues:

Click for Big

The fit is greatly improved when only NVCC-compliant issues are used for the calculation:

Click for Big

However, as was found at the time of announcement, it is clear that the Implied Volatility of the TD series of FixedResets is unreasonably high and that we have reason to fear severe underperformance by the lower-spread issues, should spreads increase sufficiently to give pause to those who feel that any TD issue will be near par forever, regardless of its terms.

[…] is a FixedReset, 3.70%+287, that commenced trading 2015-4-24 after being announced 2015-4-15. Notice of extension was provided on 2020-9-17. TD.PF.E will reset […]