Well, here’s another nail in Keystone’s coffin:

Ending years of declining to take a side on the issue because of her role in the Obama administration, Hillary Clinton on Tuesday announced her opposition to the construction of the Keystone XL oil pipeline.

“I don’t think we need to have a pipeline bringing very dirty oil, exploiting the tar sands in western Canada, across our border,” she told the Des Moines Register’s editorial board.

At a town hall in Des Moines beforehand, she expressed an eagerness to end the debate over Keystone, which had become a “distraction” from the broader fight against climate change. “I don’t think it’s in the best interest of what we need to do to combat climate change, ” she said in response to a question from a Drake University student.

Power Corporation, proud issuer of myriad preferred shares issues, has been confirmed at Pfd-2(high) by DBRS:

DBRS Limited (DBRS) has today confirmed the Senior Debt as well as the Non-Cumulative First Preferred Shares and Cumulative Redeemable First Preferred Shares, 1986 Series ratings of Power Corporation of Canada (POW or the Company) at A (high) and Pfd-2 (high), respectively. The trend on the ratings remains Stable. The credit strength of POW is directly tied to its 65.6% equity interest in Power Financial Corporation (PWF), which represents a substantial majority of the Company’s earnings and cash flow as well as the vast majority of the Company’s estimated net asset value. The Senior Debt rating of the Company is A (high) or one notch below the AA (low) rating on the Senior Debentures of PWF, reflecting the structural subordination of the holding company’s obligations.

Should PWF be upgraded, then POW could also benefit. Conversely, a shift in the Company’s risk profile resulting from a major divestiture or acquisition, a material increase in financial leverage or increased adoption of double leverage, deteriorating earnings and prolonged distress at the major operating subsidiaries, a downgrade of the rating of Great-West Lifeco Inc. (GWO) or PWF, or evidence of governance and control difficulties could have negative rating implications.

Similarly, Power Financial Corporation, issuer of myriad preferred share issues of its own, was confirmed at Pfd-1(low) by DBRS:

DBRS Limited (DBRS) has today confirmed the Issuer Rating and Senior Debentures rating of Power Financial Corporation (PWF or the Company) at AA (low), along with the Non-Cumulative First Preferred Shares and Cumulative First Preferred Shares (Series A) ratings at Pfd-1 (low). All trends remain Stable. The Company’s ratings are largely derived from its controlling interests in two of Canada’s leading financial service providers: Great-West Lifeco Inc. (GWO; Senior Debt rated AA (low) by DBRS), one of the three largest life insurance concerns in Canada, and IGM Financial Inc. (IGM; Senior Debt rated A (high) by DBRS), one of the largest mutual fund complexes in Canada as measured by long-term assets under management (AUM).

These two interests, accounting for more than 90% of the Company’s earnings, dividends and asset value, are a source of stable recurring earnings and cash flow. Under the strategic leadership of the Company, both GWO and IGM have become increasingly diversified as they have grown, both organically and by acquisition. The Company has correspondingly increased its exposure to the wealth management business in all of its chosen geographies. Both of these subsidiaries in turn benefit from the Company’s hands-on governance and risk-averse culture.

PWF’s ratings currently reflect the ratings of its most highly rated subsidiary, GWO. Should GWO be upgraded, PWF could also benefit. Conversely, a material increase in unconsolidated financial leverage giving rise to deterioration in coverage ratios; any deterioration in the creditworthiness of a major operating subsidiary, particularly a downgrade of the rating of GWO; a shift in the Company’s risk profile resulting from a major divestiture or acquisition; or evidence of governance and control difficulties could have negative rating implications.

It was a poor day for the Canadian preferred share market, with PerpetualDiscounts down 27bp, FixedResets losing 57bp and DeemedRetractibles off 10bp. The Performance Highlights table is very long, dominated by losing FixedResets, with only one winner amongst the carnage. Volume was slightly below average.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

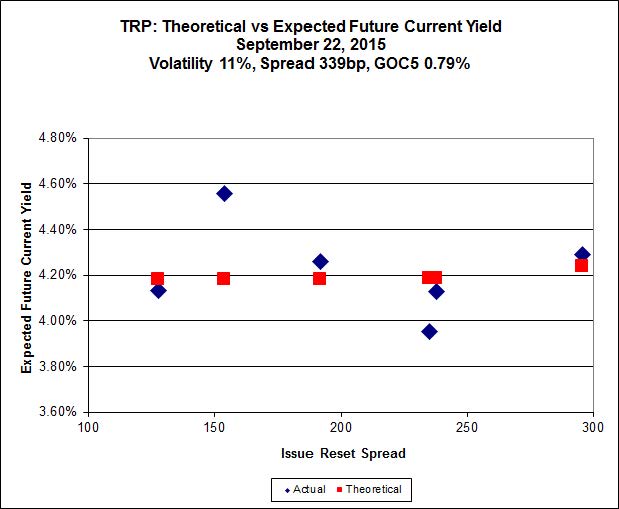

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 19.85 to be $1.10 rich, while TRP.PR.C, resetting 2016-1-30 at +164, is $1.16 cheap at its bid price of 12.78.

Click for Big

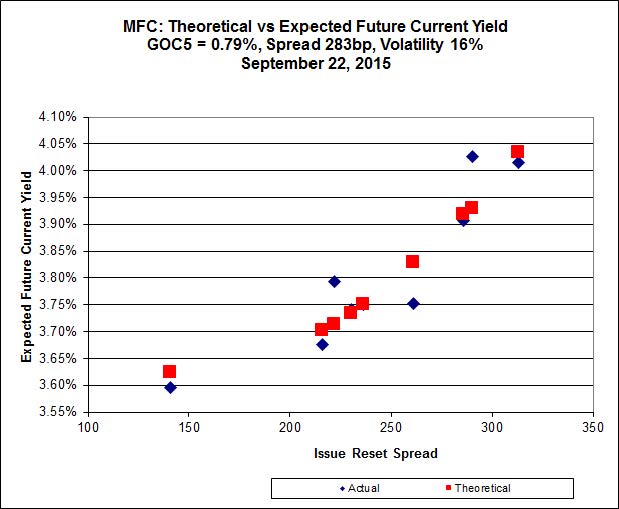

Another good fit today for MFC, with Implied Volatility falling significantly today.

Most expensive is MFC.PR.J, resetting at +261bp on 2018-3-19, bid at 22.65 to be 0.45 rich, while MFC.PR.G, resetting at +290bp on 2016-12-19, is bid at 22.91 to be 0.57 cheap.

Click for Big

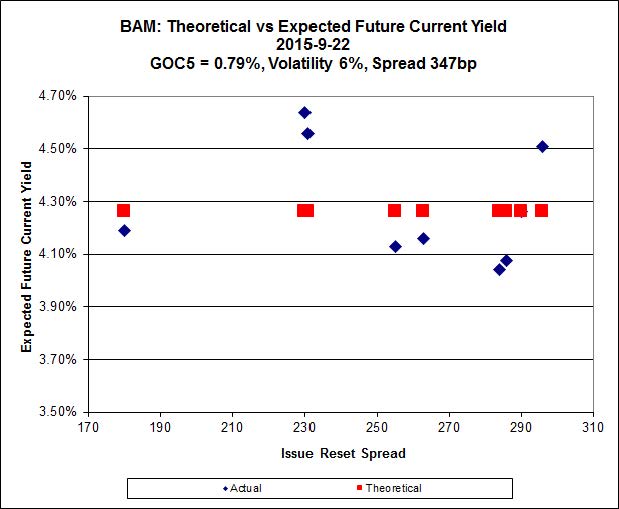

The fit on the BAM issues continues to be horrible.

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 16.70 to be $1.47 cheap. BAM.PF.G, resetting at +284bp on 2020-6-30 is bid at 22.45 and appears to be $1.15 rich.

Click for Big

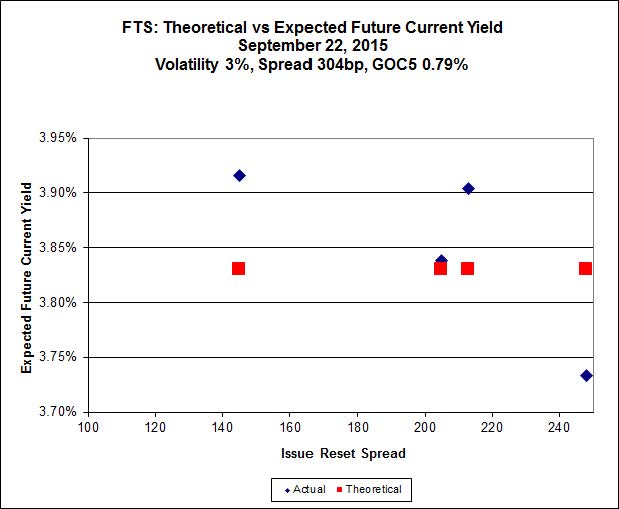

FTS.PR.M, with a spread of +248bp, and bid at 21.90, looks $0.56 expensive and resets 2019-12-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 18.70 and is $0.36 cheap.

Click for Big

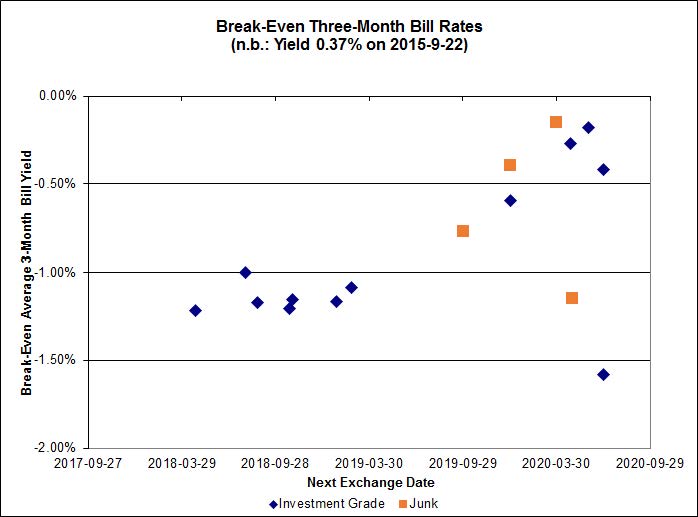

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.92%, with no outliers. The distribution’s bimodality has returned, with bank NVCC non-compliant pairs averaging -1.14% and other issues averaging -0.61%. There are two junk outliers above 0.00%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0636 % | 1,648.1 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0636 % | 2,881.6 |

| Floater | 4.51 % | 4.52 % | 60,202 | 16.38 | 3 | 0.0636 % | 1,752.0 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0742 % | 2,769.8 |

| SplitShare | 4.48 % | 4.83 % | 62,815 | 3.05 | 4 | 0.0742 % | 3,246.1 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0742 % | 2,532.7 |

| Perpetual-Premium | 5.72 % | 0.80 % | 57,832 | 0.08 | 8 | 0.0901 % | 2,498.4 |

| Perpetual-Discount | 5.47 % | 5.57 % | 66,407 | 14.52 | 30 | -0.2677 % | 2,593.5 |

| FixedReset | 4.78 % | 4.27 % | 178,259 | 15.80 | 74 | -0.5695 % | 2,130.0 |

| Deemed-Retractible | 5.16 % | 4.54 % | 92,174 | 5.48 | 33 | -0.0997 % | 2,576.3 |

| FloatingReset | 2.52 % | 4.03 % | 51,264 | 5.88 | 9 | -1.0569 % | 2,125.6 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| SLF.PR.J | FloatingReset | -3.77 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 12.75 Bid-YTW : 9.95 % |

| TRP.PR.F | FloatingReset | -3.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-22 Maturity Price : 14.20 Evaluated at bid price : 14.20 Bid-YTW : 4.03 % |

| TRP.PR.A | FixedReset | -3.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-22 Maturity Price : 15.90 Evaluated at bid price : 15.90 Bid-YTW : 4.51 % |

| GWO.PR.S | Deemed-Retractible | -2.80 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.60 Bid-YTW : 6.07 % |

| FTS.PR.H | FixedReset | -2.72 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-22 Maturity Price : 14.30 Evaluated at bid price : 14.30 Bid-YTW : 4.08 % |

| BMO.PR.T | FixedReset | -2.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-22 Maturity Price : 20.55 Evaluated at bid price : 20.55 Bid-YTW : 3.95 % |

| IFC.PR.A | FixedReset | -2.26 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.00 Bid-YTW : 8.83 % |

| BNS.PR.D | FloatingReset | -2.17 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.86 Bid-YTW : 5.21 % |

| BAM.PF.D | Perpetual-Discount | -2.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-22 Maturity Price : 21.26 Evaluated at bid price : 21.54 Bid-YTW : 5.70 % |

| BAM.PR.N | Perpetual-Discount | -1.96 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-22 Maturity Price : 21.00 Evaluated at bid price : 21.00 Bid-YTW : 5.69 % |

| CM.PR.P | FixedReset | -1.90 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-22 Maturity Price : 20.60 Evaluated at bid price : 20.60 Bid-YTW : 3.95 % |

| FTS.PR.K | FixedReset | -1.86 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-22 Maturity Price : 18.50 Evaluated at bid price : 18.50 Bid-YTW : 4.17 % |

| MFC.PR.K | FixedReset | -1.73 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.84 Bid-YTW : 6.29 % |

| TRP.PR.C | FixedReset | -1.69 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-22 Maturity Price : 12.78 Evaluated at bid price : 12.78 Bid-YTW : 4.74 % |

| VNR.PR.A | FixedReset | -1.69 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-22 Maturity Price : 19.81 Evaluated at bid price : 19.81 Bid-YTW : 4.76 % |

| BNS.PR.Z | FixedReset | -1.68 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.09 Bid-YTW : 5.35 % |

| CM.PR.O | FixedReset | -1.66 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-22 Maturity Price : 21.36 Evaluated at bid price : 21.36 Bid-YTW : 3.90 % |

| GWO.PR.N | FixedReset | -1.57 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.45 Bid-YTW : 8.95 % |

| BNS.PR.C | FloatingReset | -1.52 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.01 Bid-YTW : 4.42 % |

| BNS.PR.Y | FixedReset | -1.41 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.00 Bid-YTW : 4.83 % |

| SLF.PR.I | FixedReset | -1.36 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.06 Bid-YTW : 5.89 % |

| HSE.PR.A | FixedReset | -1.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-22 Maturity Price : 13.55 Evaluated at bid price : 13.55 Bid-YTW : 4.83 % |

| BAM.PR.T | FixedReset | -1.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-22 Maturity Price : 17.00 Evaluated at bid price : 17.00 Bid-YTW : 4.80 % |

| TD.PF.E | FixedReset | -1.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-22 Maturity Price : 22.78 Evaluated at bid price : 24.02 Bid-YTW : 3.79 % |

| POW.PR.B | Perpetual-Discount | -1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-22 Maturity Price : 23.58 Evaluated at bid price : 23.85 Bid-YTW : 5.61 % |

| FTS.PR.M | FixedReset | -1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-22 Maturity Price : 21.60 Evaluated at bid price : 21.90 Bid-YTW : 3.96 % |

| BNS.PR.A | FloatingReset | -1.12 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.90 Bid-YTW : 3.91 % |

| TD.PF.C | FixedReset | -1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-22 Maturity Price : 21.00 Evaluated at bid price : 21.00 Bid-YTW : 3.87 % |

| BIP.PR.A | FixedReset | -1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-22 Maturity Price : 21.48 Evaluated at bid price : 21.77 Bid-YTW : 5.06 % |

| TD.PF.A | FixedReset | -1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-22 Maturity Price : 21.11 Evaluated at bid price : 21.11 Bid-YTW : 3.87 % |

| TRP.PR.B | FixedReset | -1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-22 Maturity Price : 12.53 Evaluated at bid price : 12.53 Bid-YTW : 4.22 % |

| IAG.PR.G | FixedReset | 1.08 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.54 Bid-YTW : 5.14 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BSC.PR.C | SplitShare | 65,570 | New issue settled today. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2020-09-22 Maturity Price : 19.71 Evaluated at bid price : 19.69 Bid-YTW : 4.04 % |

| TRP.PR.E | FixedReset | 50,191 | RBC bought 10,000 from TD at 20.00. Desjardins crossed 14,700 at 19.85. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-22 Maturity Price : 19.85 Evaluated at bid price : 19.85 Bid-YTW : 4.34 % |

| NA.PR.S | FixedReset | 42,908 | TD crossed 29,100 at 21.70. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-22 Maturity Price : 21.31 Evaluated at bid price : 21.60 Bid-YTW : 3.92 % |

| FTS.PR.K | FixedReset | 40,000 | Nesbitt crossed 30,900 at 18.60. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-22 Maturity Price : 18.50 Evaluated at bid price : 18.50 Bid-YTW : 4.17 % |

| FTS.PR.F | Perpetual-Discount | 33,050 | RBC crossed 19,800 at 22.52. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-22 Maturity Price : 22.23 Evaluated at bid price : 22.50 Bid-YTW : 5.49 % |

| BNS.PR.P | FixedReset | 31,300 | RBC crossed 25,000 at 24.47. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.40 Bid-YTW : 3.59 % |

| There were 27 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| RY.PR.Z | FixedReset | Quote: 21.10 – 21.82 Spot Rate : 0.7200 Average : 0.4419 YTW SCENARIO |

| MFC.PR.G | FixedReset | Quote: 22.91 – 23.51 Spot Rate : 0.6000 Average : 0.3788 YTW SCENARIO |

| BAM.PF.D | Perpetual-Discount | Quote: 21.54 – 22.05 Spot Rate : 0.5100 Average : 0.3289 YTW SCENARIO |

| TD.PR.Z | FloatingReset | Quote: 22.43 – 22.98 Spot Rate : 0.5500 Average : 0.3939 YTW SCENARIO |

| BMO.PR.T | FixedReset | Quote: 20.55 – 21.05 Spot Rate : 0.5000 Average : 0.3618 YTW SCENARIO |

| BAM.PR.N | Perpetual-Discount | Quote: 21.00 – 21.40 Spot Rate : 0.4000 Average : 0.2829 YTW SCENARIO |