Canadian employment was little changed in February and the unemployment rate jumped to a five-month high as an oil shock ripples through the economy.

Nationwide employment fell by 1,000 positions, and the jobless rate rose to 6.8 percent, the highest since September, from 6.6 percent in January, Statistics Canada said Friday in Ottawa.

…

Today’s report also showed wage growth weakening and even deeper losses in the private sector.

…

Canada’s currency extended losses after the report and was down 0.7 percent to C$1.2779 against its U.S. counterpart at 9:56 a.m. in Toronto. The currency has lost 5.2 percent since the Bank of Canada cut interest rates on Jan. 21 to provide an economic buffer for the oil price shock.Jobs in the natural resource sector were down 16,900 last month. Alberta, home to the bulk of Canada’s oil production, posted a 14,000 decline in employment and its highest jobless rate since 2011, rising 0.8 percentage points to 5.3 percent. Wages in the province have stagnated since June, when crude prices began a seven-month drop to less than $50 a barrel, from more than $100.

Nationally, gains in public sector employment, which were up 24,300 in February, offset a 29,000 decline in private sector jobs.

…

By industry, the biggest decline nationally was the 19,900 positions lost in manufacturing, followed by the natural resource sector. Construction and education were the biggest gainers during the month. Average hourly wages rose 1.8 percent in February from a year earlier.

So it looks like the Conservatives won’t aim for re-election on their Economic Action Plan; it seems much wiser to stir up suspicion against and disdain for a domestic minority. I do not believe that the public sector hirings have been for secret policemen, since Bill C-51 has not yet become law and we can count on our wise masters in Ottawa to show scrupulous regard for the law.

Meanwhile, US authorities are licking their chops over another episode of regulatory extortion:

The U.S. Justice Department is seeking about $1 billion each from global banks being investigated for manipulation of currency markets, according to two people familiar with the talks.

The figure is a starting point in settlement discussions, with some banks being asked for more and some less than $1 billion. One bank that has cooperated from the beginning is expected to pay far less, one of the people said. Penalties of about $4 billion are on the table, according to one of the people, though the number could change markedly.

Banks are pushing back harder than in some previous negotiations, including those for mortgage-backed securities, and the final penalties could be lower, people close to the talks said.

…

As talks to resolve the U.S. cases advance, the Justice Department and New York’s state banking regulator have opened up a new investigation into whether banks abused a longstanding practice in the currency spot markets known as “last look.” The practice allows banks to back out of unfavorable trades at the last moment.

“Last look” refers to the feature on many platforms in which the party that is making markets gets a chance to reject a trade if it doesn’t want to complete.

It dates back to the practice in phone-to-phone trading of checking the price was still in line with the market at the end of a conversation between a dealer and client or broker, aiming to get as close to the prevailing rate as possible.

But industry figures worry that it has been used by some trading systems in recent years to systematically reject unfavourable orders or to float false orders that would never be executed to flush out the positions of other players.

Oh, OK. It’s the cool way to say “subject”.

Overall, it was another quiet, mixed day for the Canadian preferred share market, with PerpetualDiscounts off 8bp, FixedResets gaining 1bp and DeemedRetractibles up 4bp. The calm is deceptive, though, as the Performance Highlights table continues to show a lot of churn. Volume was slightly below average.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

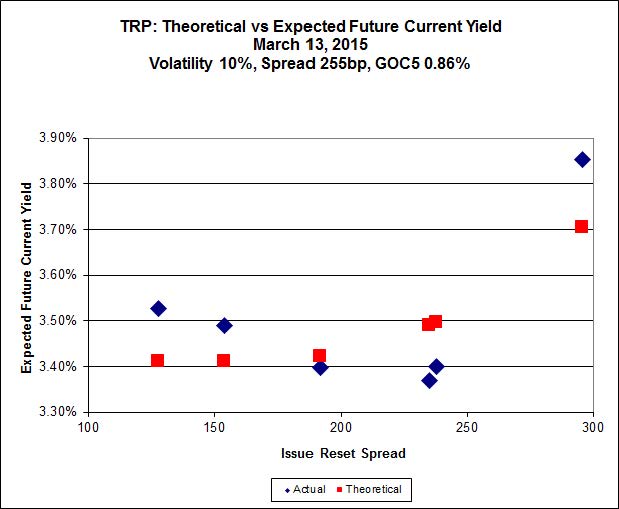

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 23.82 to be $0.82 rich, while TRP.PR.G, resetting 2020-11-30 at +296, is $1.01 cheap at its bid price of 24.78.

Click for Big

Another excellent fit, but the numbers are perplexing. Implied Volatility for MFC continues to be a conundrum, although it declined substantially today. It is still too high if we consider that NVCC rules will never apply to these issues; it is still too low if we consider them to be NVCC non-compliant issues (and therefore with Deemed Maturities in the call schedule).

Most expensive is MFC.PR.L, resetting at +216 on 2019-6-19, bid at 24.25 to be $0.58 rich, while MFC.PR.H, resetting at +313bp on 2017-3-19, is bid at 26.01 to be $0.49 cheap.

Click for Big

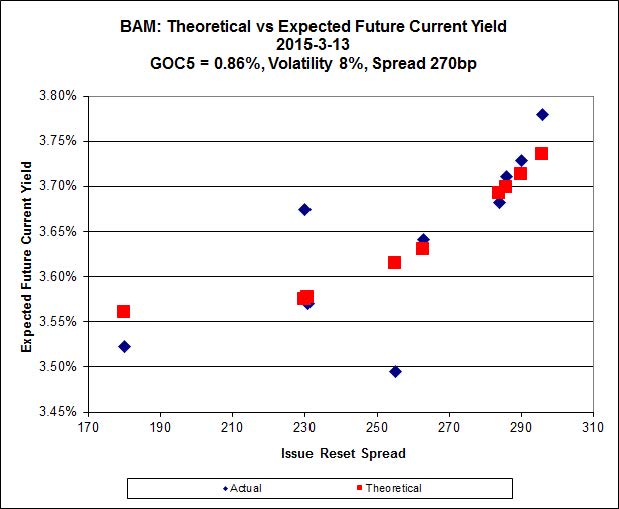

The fit on this series is actually quite reasonable – it’s the scale that makes it look so weird.

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 21.50 to be $0.60 cheap. BAM.PF.E, resetting at +255bp 2020-3-31 is bid at 24.39 and appears to be $0.80 rich.

Click for Big

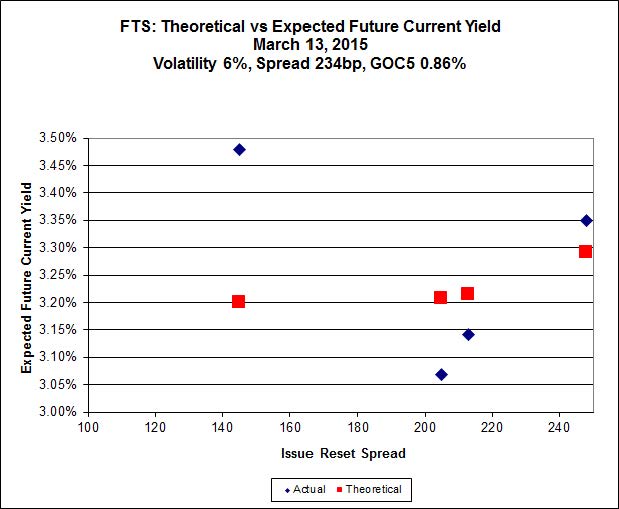

This is just weird because the middle is expensive and the ends are cheap but anyway … FTS.PR.H, with a spread of +145bp, and bid at 16.60, looks $1.45 cheap and resets 2015-6-1. FTS.PR.K, with a spread of +205bp and resetting 2019-3-1, is bid at 23.71 and is $1.03 rich.

Click for Big

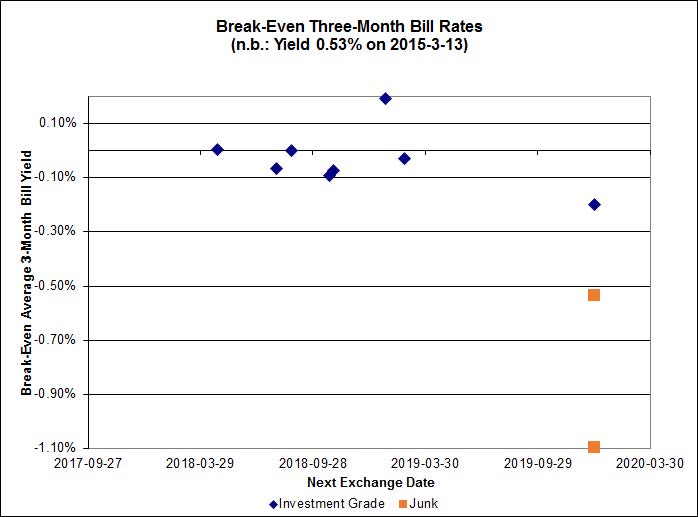

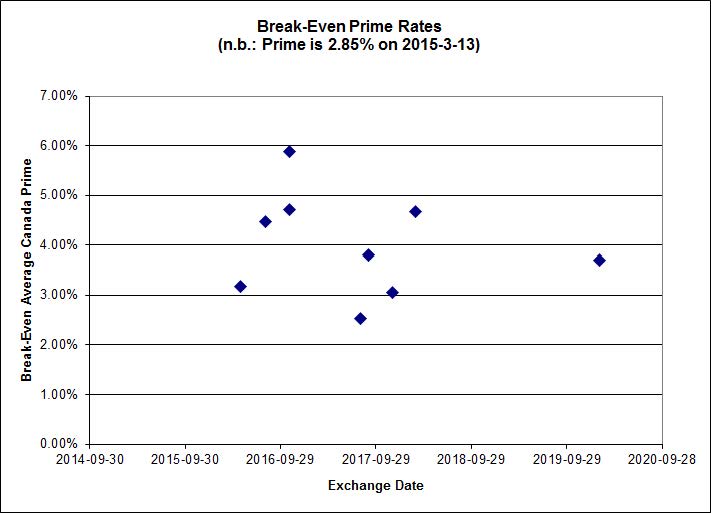

The cancellation of the previously announced deflationary environment had an immediate effect on the implied three month bill rate, with investment-grade pairs predicting an average over the next five years of between 0.00% and 0.10%

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0000 % | 2,382.2 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0000 % | 4,165.2 |

| Floater | 3.18 % | 3.18 % | 68,450 | 19.31 | 3 | 0.0000 % | 2,532.5 |

| OpRet | 4.07 % | 1.31 % | 100,250 | 0.27 | 1 | 0.0000 % | 2,762.6 |

| SplitShare | 4.48 % | 4.57 % | 53,461 | 4.44 | 5 | -0.0717 % | 3,207.1 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0000 % | 2,526.1 |

| Perpetual-Premium | 5.29 % | 0.83 % | 56,717 | 0.08 | 25 | 0.0642 % | 2,519.5 |

| Perpetual-Discount | 5.03 % | 5.01 % | 153,307 | 15.40 | 9 | -0.0800 % | 2,782.1 |

| FixedReset | 4.39 % | 3.51 % | 248,913 | 16.79 | 85 | 0.0057 % | 2,428.0 |

| Deemed-Retractible | 4.91 % | -0.77 % | 107,878 | 0.13 | 37 | 0.0427 % | 2,655.7 |

| FloatingReset | 2.49 % | 2.93 % | 80,342 | 6.33 | 8 | -0.0107 % | 2,333.6 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| HSE.PR.A | FixedReset | -2.69 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-13 Maturity Price : 17.00 Evaluated at bid price : 17.00 Bid-YTW : 3.91 % |

| CIU.PR.C | FixedReset | -2.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-13 Maturity Price : 16.49 Evaluated at bid price : 16.49 Bid-YTW : 3.49 % |

| MFC.PR.F | FixedReset | -1.52 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.45 Bid-YTW : 5.46 % |

| GWO.PR.N | FixedReset | -1.08 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.30 Bid-YTW : 5.86 % |

| MFC.PR.C | Deemed-Retractible | -1.01 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.62 Bid-YTW : 5.24 % |

| TRP.PR.F | FloatingReset | 1.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-13 Maturity Price : 18.90 Evaluated at bid price : 18.90 Bid-YTW : 3.23 % |

| BAM.PR.T | FixedReset | 1.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-13 Maturity Price : 21.73 Evaluated at bid price : 22.20 Bid-YTW : 3.66 % |

| SLF.PR.G | FixedReset | 1.49 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.40 Bid-YTW : 5.81 % |

| MFC.PR.B | Deemed-Retractible | 1.58 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.40 Bid-YTW : 4.98 % |

| BAM.PF.E | FixedReset | 2.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-13 Maturity Price : 22.94 Evaluated at bid price : 24.39 Bid-YTW : 3.62 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| RY.PR.M | FixedReset | 196,652 | New issue settled today. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-13 Maturity Price : 22.85 Evaluated at bid price : 24.25 Bid-YTW : 3.51 % |

| CM.PR.Q | FixedReset | 140,573 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-13 Maturity Price : 23.00 Evaluated at bid price : 24.61 Bid-YTW : 3.57 % |

| TD.PR.R | Deemed-Retractible | 136,308 | Called for redemption effective April 30. YTW SCENARIO Maturity Type : Call Maturity Date : 2015-04-30 Maturity Price : 25.50 Evaluated at bid price : 25.80 Bid-YTW : 1.10 % |

| HSE.PR.E | FixedReset | 86,715 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-13 Maturity Price : 23.13 Evaluated at bid price : 24.92 Bid-YTW : 4.36 % |

| SLF.PR.G | FixedReset | 71,530 | RBC crossed 57,800 at 18.50. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.40 Bid-YTW : 5.81 % |

| BIP.PR.A | FixedReset | 55,400 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-13 Maturity Price : 22.96 Evaluated at bid price : 24.50 Bid-YTW : 4.44 % |

| There were 27 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| MFC.PR.C | Deemed-Retractible | Quote: 23.62 – 24.27 Spot Rate : 0.6500 Average : 0.4416 YTW SCENARIO |

| CU.PR.C | FixedReset | Quote: 23.92 – 24.60 Spot Rate : 0.6800 Average : 0.5189 YTW SCENARIO |

| ENB.PR.T | FixedReset | Quote: 20.49 – 20.81 Spot Rate : 0.3200 Average : 0.2024 YTW SCENARIO |

| CIU.PR.C | FixedReset | Quote: 16.49 – 16.90 Spot Rate : 0.4100 Average : 0.3123 YTW SCENARIO |

| BAM.PR.N | Perpetual-Discount | Quote: 22.33 – 22.64 Spot Rate : 0.3100 Average : 0.2416 YTW SCENARIO |

| NA.PR.Q | FixedReset | Quote: 25.30 – 25.50 Spot Rate : 0.2000 Average : 0.1371 YTW SCENARIO |