Top news of the day was the BoC Rate Announcement:

The Bank of Canada today announced that it is maintaining its target for the overnight rate at 1/2 per cent. The Bank Rate is correspondingly 3/4 per cent and the deposit rate is 1/4 per cent.

Inflation has evolved in line with the outlook in the Bank’s July Monetary Policy Report (MPR). Total CPI inflation remains near the bottom of the Bank’s target range, owing to declines in consumer energy prices. Core inflation is close to 2 per cent as the transitory effects of the past depreciation of the Canadian dollar are roughly offsetting disinflationary pressures from economic slack, which has increased this year. The Bank judges that the underlying trend in inflation continues to be about 1.5 to 1.7 per cent.

…

The Bank projects real GDP will grow by just over 1 per cent in 2015 before firming to about 2 per cent in 2016 and 2 1/2 per cent in 2017. The complex economic adjustments to the decline in Canada’s terms of trade will continue to play out over the projection horizon. The weaker profile for business investment suggests that, in the near term, growth in potential output is more likely to be in the lower part of the Bank’s range of estimates. Given this judgment about potential output, the Canadian economy can be expected to return to full capacity, and inflation sustainably to target, around mid-2017.

So now it’s a return to full capacity ‘around mid-2017’. In the July announcement it was ‘the first half of 2017.’ We are approaching normalcy asymptotically.

I mentioned the ‘welfare wall’ on October 14; this is the ridiculously high effective marginal tax rate on low income earners due to clawback of benefits when they’re imprudent enough to get a slightly better job or work slightly more hours. This came to mind when I read about a pending wave of closures of slum housing:

There are currently about 1.34 million units of affordable housing created by a HUD program known as Section 8 project-based rental assistance, according to a blog post published on Wednesday by Poethig and her Urban Institute colleague Reed Jordan. More than 30 percent of those units are kept affordable by contracts that are set to expire by the end of 2017.

…

Under Housing and Urban Development’s system, tenants who meet income requirements pay 30 percent of their income in rent, and HUD pays the landlord a subsidy on top of that rent. The average subsidy was $665 a month (PDF) in 2011, according to the National Low Income Housing Coalition. New York, where 33 percent of units are set to expire by 2017, has more than 123,000 units in the program; Dallas, where 47 percent of units are at risk, has about 8,800.

…

The system for preserving affordable units varies from place to place. State law gives cities in Massachusetts the right of first refusal when property owners want to let a HUD contract expire, and a number of nonprofit groups and a state-affiliated agency are devoted to preserving it. In 2013, a nonprofit called Preservation of Affordable Housing paid $234 million for about 850 apartments in Boston, Cape Cod, and elsewhere in the state to prevent the units form being converted to market rate. Washington, Chicago, and other cities require landlords to notify tenants in advance of conversions and, in some cases, give them the opportunity to buy the apartment.

So basically, given that ‘tenants … pay 30% of their income in rent’ means that the housing benefit alone is worth a 30% marginal tax rate! Overtime? A new job at $1/hour more? Are you crazy?

It’s a little difficult to put numbers on the Boston project! According to a story in the Boston Globe, basically all of the 234-million is government money, either directly or through shifting the subsidy to tax credits:

Low-income residents joined government officials and investors Thursday to celebrate the renovation of six apartment buildings, a project that totaled nearly $234 million and is being touted as the state’s largest affordable housing improvement effort.

…

They were all renovated with the help of a $168 million loan from MassHousing, the state’s affordable housing bank, almost $66 million in private investments that came from $8.9 million in tax credits provided by the Massachusetts Department of Housing and Community Development tax credits

I think the touted Preservation of Affordable Housing is just another government boondoggle, but it’s hard to say. They don’t publish their financials and their news page doesn’t provide any hints of their financing. Their news release regarding the Boston project shows the usual grab-bag of government hand-outs:

The financing package includes:

MassHousing: $35.8 million construction and permanent loan and a $9.3 million bridge loan

Mass Housing Investment Corp: $12.3 million federal low-income housing tax credit investment

Two loans from the City of Cambridge /Cambridge Affordable Housing Trust: $1,852,286 and $2.4 million for a total City/Trust contribution of $4,252,286

CEDAC: bridge loan of $3,700,000

I have sent them the following eMail:

Sirs,

I am curious regarding the incentive your beneficiaries have to improve their financial situation.

Has your organization done – or are you aware of – any research into the Effective Marginal Tax Rate (EMTR) faced by occupants of your subsidized units? By EMTR, I mean the impact of both direct taxation and reduction of benefits on additional income that could be earned by these clients.

Sincerely,

In an announcement sure to cause a fit of giggles, DBRS Confirms Advantaged Preferred Share Trust Units Stability Rating of STA-2 (middle). Stop snickering, Stability Ratings are supposed to reflect “the fund’s ability to generate sufficient cash to pay out a stable level of distributions on a per-unit basis over the longer term.” Good for snickers in the DBRS rating confirmation is the phrase:

The credit quality of the Portfolio remains strong: approximately 78% of the portfolio shares are rated at Pfd-3 (high) or higher.

Rather an unusual cut-off, wouldn’t you say? But … “Pfd-3(high)” allows them to include Enbridge. But heads will nod in agreement with:

As of Oct 14, 2015 the Trust has seen a 24% decline in Portfolio value compared to June 30, 2015 values. Such a decline is mainly explained by the negative investor sentiment regarding the overall preferred share market that translates into vast selling of preferred shares causing the supply exceeding the demand. The fund rating methodology does not directly address the potential price volatility of the Portfolio.

Until, of course, those wisely nodding heads realize that it doesn’t actually say anything. Some might wonder if this comment is the whole point of the confirmation, desperately asked for by the fund sponsors! “Please, give us something we can say to all our angry clients!”

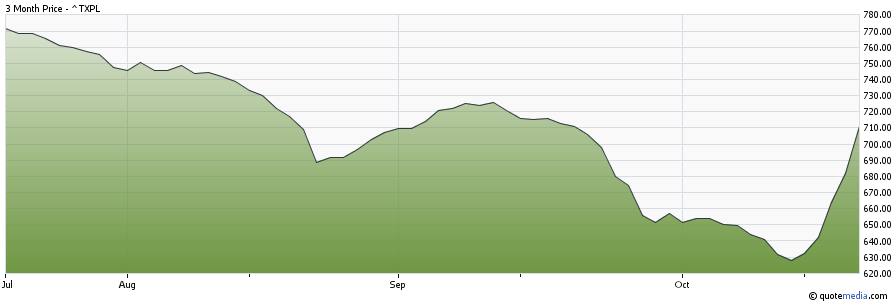

Canadian preferred share investors have a new ride!

Click for Big

It was another incredibly strong day for the Canadian preferred share market, with PerpetualDiscounts up 53bp, FixedResets winning an amazing 306bp and DeemedRetractibles gaining a mere 48bp. No less than fourteen issues, all FixedResets, gained over 5% on the day (bid/bid); this is a rather fun statistic, too bad I don’t get to use it more often! Volume was very extremely high.

Still, let’s keep things in perspective and remember that the TXPL (price index) is still only back to where it was in mid-August. 15Q3 was a really, really, lousy quarter. On a total return basis, performance for TXPL is below zero with a start-date of August 19. So while I’m pleased to see these impressive gains, we’ll need another few weeks of them before we can call it a good year!

Click for Big

PerpetualDiscounts now yield 5.76%, equivalent to 7.49% interest at the standard equivalency factor of 1.3x. Long corporates now yield about 4.3%, so the pre-tax interest-equivalent spread (in this context, the “Seniority Spread”) is now about 320bp, a sharp reduction from the ludicrous 340bp reported October 14.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

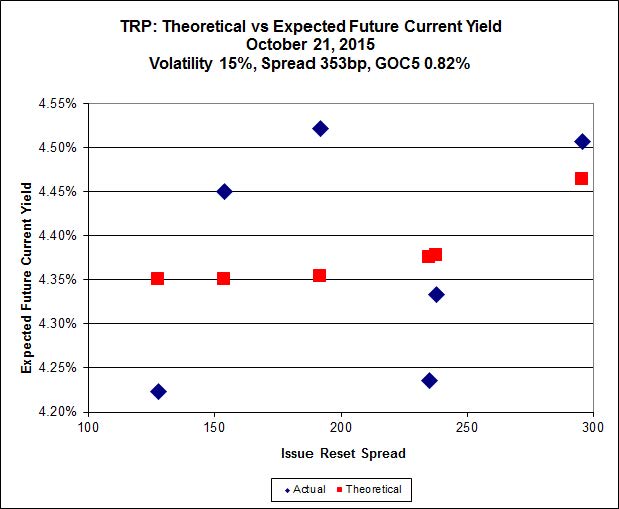

Here’s TRP:

Click for Big

Implied Volatility remained constant today, above what I consider reasonable.

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 18.71 to be $0.60 rich, while TRP.PR.A, resetting 2019-12-31 at +192, is $0.58 cheap at its bid price of 15.15.

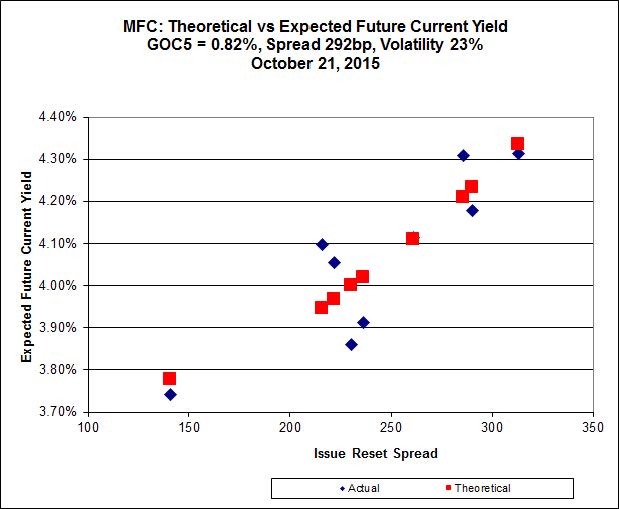

Click for Big

Implied Volatility declined slightly for the MFC series today.

Most expensive is MFC.PR.N, resetting at +230bp on 2020-3-19, bid at 14.90 to be 0.71 rich, while MFC.PR.L resetting at +216bp on 2019-6-19, is bid at 18.18 to be 0.70 cheap.

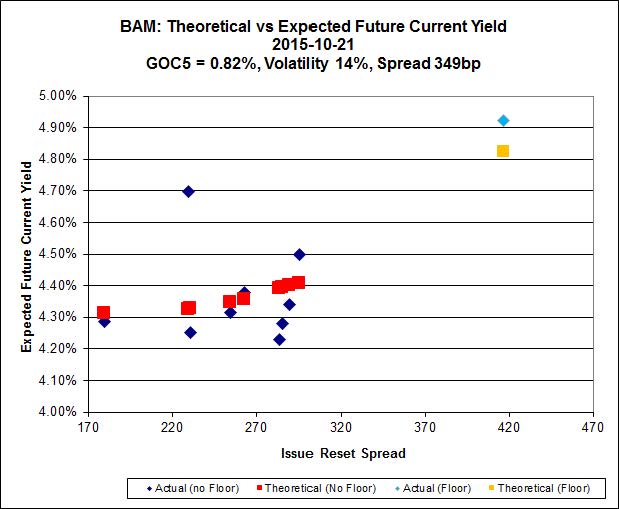

Click for Big

The fit on the BAM issues continues to be poor. Implied Volatility increased a little today, but this is a figure that’s very highly dependent on the performance of the high-spread issue BAM.PF.H.

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 16.60 to be $0.90 cheap. BAM.PF.G, resetting at +284bp on 2020-6-30 is bid at 21.63 and appears to be $0.69 rich.

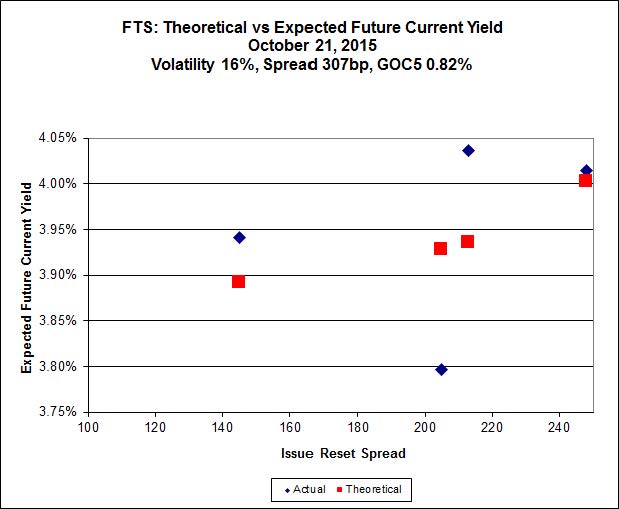

Click for Big

Implied Volatility declined again today but remains high.

FTS.PR.K, with a spread of +205bp, and bid at 18.90, looks $0.63 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 18.27 and is $0.47 cheap.

Click for Big

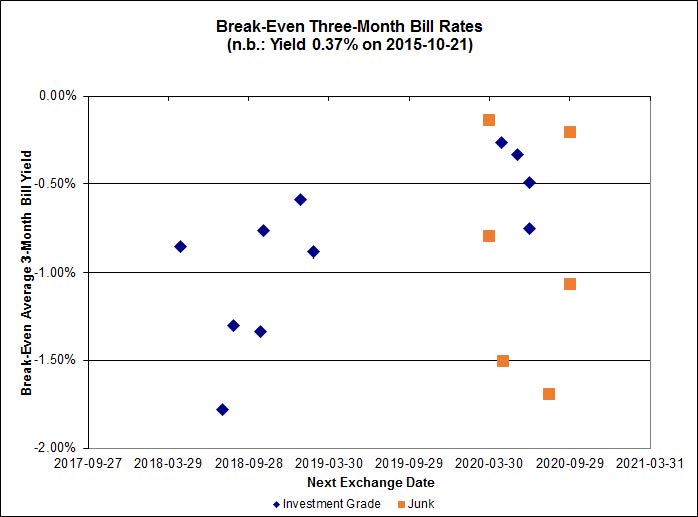

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.87%, with one outlier above 0.00%. The distribution is bimodal, with bank NVCC non-compliant pairs averaging -1.07% and other issues averaging -0.31%. There are two junk outliers above 0.00% and two below -2.00%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 2.3096 % | 1,717.8 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 2.3096 % | 3,003.5 |

| Floater | 4.32 % | 4.38 % | 62,145 | 16.66 | 3 | 2.3096 % | 1,826.1 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0162 % | 2,757.8 |

| SplitShare | 4.35 % | 5.17 % | 78,063 | 2.97 | 5 | 0.0162 % | 3,232.0 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0162 % | 2,521.7 |

| Perpetual-Premium | 5.88 % | 5.83 % | 68,250 | 14.02 | 5 | 0.3135 % | 2,476.4 |

| Perpetual-Discount | 5.67 % | 5.76 % | 80,237 | 14.25 | 33 | 0.5261 % | 2,512.2 |

| FixedReset | 4.94 % | 4.46 % | 205,668 | 15.90 | 76 | 3.0619 % | 2,062.6 |

| Deemed-Retractible | 5.22 % | 5.17 % | 105,739 | 5.44 | 33 | 0.4826 % | 2,554.1 |

| FloatingReset | 2.51 % | 4.02 % | 68,838 | 5.82 | 9 | 1.7865 % | 2,149.9 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| W.PR.J | Perpetual-Discount | -1.96 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 22.78 Evaluated at bid price : 23.06 Bid-YTW : 6.11 % |

| FTS.PR.F | Perpetual-Discount | -1.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 21.44 Evaluated at bid price : 21.70 Bid-YTW : 5.72 % |

| MFC.PR.F | FixedReset | 1.02 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.90 Bid-YTW : 8.97 % |

| TD.PF.F | Perpetual-Discount | 1.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 22.39 Evaluated at bid price : 22.69 Bid-YTW : 5.41 % |

| RY.PR.P | Perpetual-Discount | 1.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 23.85 Evaluated at bid price : 24.19 Bid-YTW : 5.46 % |

| FTS.PR.H | FixedReset | 1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 14.40 Evaluated at bid price : 14.40 Bid-YTW : 4.10 % |

| GWO.PR.H | Deemed-Retractible | 1.10 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.15 Bid-YTW : 6.59 % |

| PWF.PR.S | Perpetual-Discount | 1.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 21.31 Evaluated at bid price : 21.60 Bid-YTW : 5.57 % |

| RY.PR.N | Perpetual-Discount | 1.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 22.66 Evaluated at bid price : 23.00 Bid-YTW : 5.48 % |

| W.PR.H | Perpetual-Discount | 1.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 22.80 Evaluated at bid price : 23.08 Bid-YTW : 5.99 % |

| GWO.PR.L | Deemed-Retractible | 1.23 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.75 Bid-YTW : 5.88 % |

| BNS.PR.B | FloatingReset | 1.23 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.22 Bid-YTW : 4.02 % |

| MFC.PR.B | Deemed-Retractible | 1.23 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.37 Bid-YTW : 6.89 % |

| BNS.PR.Q | FixedReset | 1.24 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.42 Bid-YTW : 3.48 % |

| SLF.PR.E | Deemed-Retractible | 1.27 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.76 Bid-YTW : 7.10 % |

| PWF.PR.E | Perpetual-Discount | 1.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 23.68 Evaluated at bid price : 23.95 Bid-YTW : 5.76 % |

| GWO.PR.Q | Deemed-Retractible | 1.28 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.00 Bid-YTW : 6.39 % |

| RY.PR.L | FixedReset | 1.34 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.03 Bid-YTW : 4.04 % |

| CU.PR.H | Perpetual-Discount | 1.36 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 22.79 Evaluated at bid price : 23.16 Bid-YTW : 5.77 % |

| BNS.PR.P | FixedReset | 1.38 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.30 Bid-YTW : 3.58 % |

| TD.PR.T | FloatingReset | 1.41 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.25 Bid-YTW : 3.89 % |

| RY.PR.W | Perpetual-Discount | 1.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 22.46 Evaluated at bid price : 22.72 Bid-YTW : 5.47 % |

| MFC.PR.C | Deemed-Retractible | 1.52 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.65 Bid-YTW : 7.20 % |

| BMO.PR.M | FixedReset | 1.53 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.57 Bid-YTW : 3.31 % |

| IFC.PR.C | FixedReset | 1.59 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.81 Bid-YTW : 6.66 % |

| SLF.PR.A | Deemed-Retractible | 1.67 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.91 Bid-YTW : 6.63 % |

| HSE.PR.G | FixedReset | 1.71 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 22.71 Evaluated at bid price : 23.80 Bid-YTW : 4.61 % |

| SLF.PR.B | Deemed-Retractible | 1.76 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.00 Bid-YTW : 6.63 % |

| BNS.PR.A | FloatingReset | 1.77 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.05 Bid-YTW : 3.74 % |

| BAM.PF.D | Perpetual-Discount | 1.85 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 20.97 Evaluated at bid price : 20.97 Bid-YTW : 5.91 % |

| TRP.PR.B | FixedReset | 1.89 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 12.43 Evaluated at bid price : 12.43 Bid-YTW : 4.30 % |

| HSE.PR.A | FixedReset | 2.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 14.09 Evaluated at bid price : 14.09 Bid-YTW : 4.69 % |

| CM.PR.Q | FixedReset | 2.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 21.50 Evaluated at bid price : 21.50 Bid-YTW : 4.22 % |

| BMO.PR.S | FixedReset | 2.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 19.57 Evaluated at bid price : 19.57 Bid-YTW : 4.31 % |

| TD.PR.Z | FloatingReset | 2.37 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.00 Bid-YTW : 4.17 % |

| BMO.PR.Z | Perpetual-Discount | 2.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 23.25 Evaluated at bid price : 23.55 Bid-YTW : 5.41 % |

| MFC.PR.K | FixedReset | 2.40 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.74 Bid-YTW : 7.14 % |

| BAM.PR.Z | FixedReset | 2.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 21.00 Evaluated at bid price : 21.00 Bid-YTW : 4.72 % |

| VNR.PR.A | FixedReset | 2.45 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 20.92 Evaluated at bid price : 20.92 Bid-YTW : 4.46 % |

| TRP.PR.D | FixedReset | 2.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 18.46 Evaluated at bid price : 18.46 Bid-YTW : 4.57 % |

| TRP.PR.G | FixedReset | 2.54 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 20.97 Evaluated at bid price : 20.97 Bid-YTW : 4.59 % |

| BAM.PR.B | Floater | 2.56 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 11.20 Evaluated at bid price : 11.20 Bid-YTW : 4.25 % |

| BMO.PR.R | FloatingReset | 2.59 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.60 Bid-YTW : 3.76 % |

| TD.PR.S | FixedReset | 2.64 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.50 Bid-YTW : 3.21 % |

| HSE.PR.E | FixedReset | 2.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 22.63 Evaluated at bid price : 23.61 Bid-YTW : 4.67 % |

| BNS.PR.D | FloatingReset | 2.72 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.90 Bid-YTW : 6.05 % |

| SLF.PR.I | FixedReset | 2.73 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.34 Bid-YTW : 6.44 % |

| PWF.PR.T | FixedReset | 2.82 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 21.52 Evaluated at bid price : 21.90 Bid-YTW : 3.82 % |

| RY.PR.M | FixedReset | 2.82 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 20.06 Evaluated at bid price : 20.06 Bid-YTW : 4.42 % |

| CM.PR.O | FixedReset | 2.84 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 19.20 Evaluated at bid price : 19.20 Bid-YTW : 4.32 % |

| TD.PF.A | FixedReset | 2.97 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 19.05 Evaluated at bid price : 19.05 Bid-YTW : 4.27 % |

| BMO.PR.W | FixedReset | 3.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 18.60 Evaluated at bid price : 18.60 Bid-YTW : 4.39 % |

| BNS.PR.Y | FixedReset | 3.14 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.01 Bid-YTW : 5.64 % |

| NA.PR.Q | FixedReset | 3.25 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.75 Bid-YTW : 3.59 % |

| FTS.PR.M | FixedReset | 3.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 20.55 Evaluated at bid price : 20.55 Bid-YTW : 4.29 % |

| PWF.PR.P | FixedReset | 3.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 15.00 Evaluated at bid price : 15.00 Bid-YTW : 4.08 % |

| RY.PR.I | FixedReset | 3.40 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.35 Bid-YTW : 3.76 % |

| RY.PR.J | FixedReset | 3.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 20.63 Evaluated at bid price : 20.63 Bid-YTW : 4.40 % |

| TD.PF.B | FixedReset | 3.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 19.08 Evaluated at bid price : 19.08 Bid-YTW : 4.26 % |

| BAM.PR.C | Floater | 3.52 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 10.88 Evaluated at bid price : 10.88 Bid-YTW : 4.38 % |

| MFC.PR.H | FixedReset | 3.53 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.89 Bid-YTW : 5.31 % |

| NA.PR.W | FixedReset | 3.54 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 19.00 Evaluated at bid price : 19.00 Bid-YTW : 4.30 % |

| TRP.PR.F | FloatingReset | 3.56 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 14.24 Evaluated at bid price : 14.24 Bid-YTW : 4.05 % |

| RY.PR.Z | FixedReset | 3.70 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 19.34 Evaluated at bid price : 19.34 Bid-YTW : 4.23 % |

| BAM.PR.R | FixedReset | 3.75 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 16.60 Evaluated at bid price : 16.60 Bid-YTW : 4.87 % |

| BMO.PR.T | FixedReset | 3.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 19.00 Evaluated at bid price : 19.00 Bid-YTW : 4.33 % |

| BAM.PF.E | FixedReset | 3.83 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 19.52 Evaluated at bid price : 19.52 Bid-YTW : 4.70 % |

| RY.PR.H | FixedReset | 3.85 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 19.14 Evaluated at bid price : 19.14 Bid-YTW : 4.32 % |

| CM.PR.P | FixedReset | 4.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 18.99 Evaluated at bid price : 18.99 Bid-YTW : 4.27 % |

| BMO.PR.Y | FixedReset | 4.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 21.54 Evaluated at bid price : 21.86 Bid-YTW : 4.22 % |

| MFC.PR.G | FixedReset | 4.12 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.26 Bid-YTW : 5.41 % |

| BAM.PF.G | FixedReset | 4.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 21.34 Evaluated at bid price : 21.63 Bid-YTW : 4.50 % |

| BNS.PR.Z | FixedReset | 4.68 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.15 Bid-YTW : 6.06 % |

| BMO.PR.Q | FixedReset | 4.74 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.00 Bid-YTW : 5.41 % |

| TD.PF.C | FixedReset | 4.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 18.90 Evaluated at bid price : 18.90 Bid-YTW : 4.28 % |

| IAG.PR.G | FixedReset | 4.96 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.80 Bid-YTW : 5.66 % |

| MFC.PR.J | FixedReset | 4.99 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.84 Bid-YTW : 6.05 % |

| TD.PF.E | FixedReset | 5.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 21.32 Evaluated at bid price : 21.60 Bid-YTW : 4.28 % |

| BAM.PF.B | FixedReset | 5.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 19.70 Evaluated at bid price : 19.70 Bid-YTW : 4.62 % |

| TRP.PR.C | FixedReset | 5.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 13.26 Evaluated at bid price : 13.26 Bid-YTW : 4.50 % |

| MFC.PR.M | FixedReset | 5.28 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.32 Bid-YTW : 6.32 % |

| BAM.PF.F | FixedReset | 5.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 21.50 Evaluated at bid price : 21.50 Bid-YTW : 4.53 % |

| BIP.PR.A | FixedReset | 5.56 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 21.54 Evaluated at bid price : 21.85 Bid-YTW : 5.09 % |

| BAM.PF.A | FixedReset | 5.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 21.42 Evaluated at bid price : 21.42 Bid-YTW : 4.54 % |

| BAM.PR.X | FixedReset | 6.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 15.28 Evaluated at bid price : 15.28 Bid-YTW : 4.64 % |

| FTS.PR.G | FixedReset | 6.47 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 18.27 Evaluated at bid price : 18.27 Bid-YTW : 4.30 % |

| NA.PR.S | FixedReset | 6.74 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 19.80 Evaluated at bid price : 19.80 Bid-YTW : 4.28 % |

| BAM.PR.T | FixedReset | 7.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 18.40 Evaluated at bid price : 18.40 Bid-YTW : 4.47 % |

| MFC.PR.N | FixedReset | 7.21 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.21 Bid-YTW : 6.32 % |

| CU.PR.C | FixedReset | 7.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 21.50 Evaluated at bid price : 21.50 Bid-YTW : 3.88 % |

| FTS.PR.K | FixedReset | 7.75 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 18.90 Evaluated at bid price : 18.90 Bid-YTW : 4.13 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| TRP.PR.D | FixedReset | 236,463 | Desjardins crossed blocks of 97,000 and 104,300, both at 18.40. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 18.46 Evaluated at bid price : 18.46 Bid-YTW : 4.57 % |

| MFC.PR.J | FixedReset | 88,995 | Scotia crossed 28500 at 19.90 and 40,000 at 20.00. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.84 Bid-YTW : 6.05 % |

| MFC.PR.M | FixedReset | 81,090 | Scotia crossed 10,100 at 19.52 and 32,900 at 21.00. That’s one helluva difference in block prices! YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.32 Bid-YTW : 6.32 % |

| MFC.PR.N | FixedReset | 66,655 | Scotia crossed 12,400 at 19.15. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.21 Bid-YTW : 6.32 % |

| TD.PF.E | FixedReset | 65,700 | Scotia sold 13,800 to TD at 21.20 and bought 10,000 from RBC at 21.45. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 21.32 Evaluated at bid price : 21.60 Bid-YTW : 4.28 % |

| PWF.PR.P | FixedReset | 54,021 | Nesbitt crossed 30,000 at 15.27. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-21 Maturity Price : 15.00 Evaluated at bid price : 15.00 Bid-YTW : 4.08 % |

| There were 72 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| TRP.PR.G | FixedReset | Quote: 20.97 – 22.39 Spot Rate : 1.4200 Average : 0.7902 YTW SCENARIO |

| MFC.PR.L | FixedReset | Quote: 18.18 – 19.45 Spot Rate : 1.2700 Average : 0.8489 YTW SCENARIO |

| CM.PR.O | FixedReset | Quote: 19.20 – 20.27 Spot Rate : 1.0700 Average : 0.6604 YTW SCENARIO |

| MFC.PR.H | FixedReset | Quote: 22.89 – 23.99 Spot Rate : 1.1000 Average : 0.6960 YTW SCENARIO |

| CM.PR.P | FixedReset | Quote: 18.99 – 20.00 Spot Rate : 1.0100 Average : 0.6529 YTW SCENARIO |

| MFC.PR.I | FixedReset | Quote: 21.35 – 22.10 Spot Rate : 0.7500 Average : 0.4121 YTW SCENARIO |

Question : IF a pref is sold one day prior to the dividend date, and bought back the next day on the dividend date, and given the settlements of 3 days respectively, would I get a dividend in either case ? If I don’t get one for either scenario, does the person on the opposite side of either transaction get one ?

Thank you in advance..

What’s a dividend date?

This link will address your questions. http://www.investopedia.com/university/introduction-to-dividends/dividend-dates.asp

I like my publication better: Dividends and Ex-Dates.

But yes, I agree with gsp, it is unclear which dividend date is meant.

It was a RY pref

Sold oct 21 settles oct 26

Bought back oct 22 settles oct 27

I’m presuming I don’t get the dividend, but a) does the person who bought my shares on oct 21 get it ? B) does the person selling on oct 22 lose theirs ?

Thanks again.

The ex-dividend date for RY preferreds was October 22.

When you sold it on October 21, you sold it prior to the ex-date, so you don’t get the dividend.

When you bought it on October 22, you bought it on or after the ex-date, so you don’t get the dividend.

Thanks, I had thought both answers were the case, that said, a) does the person who bought my shares on oct. 21 get the dividend ? B) does the person who sold to me oct. 22 lose their dividend ?

Perhaps what I’m asking and trying to phrase this correctly, what happens to the dividends during the settlement period of 3 business days. Someone told me that a buyer of any stock with dividends has to have it settle a day prior to the dividend date.

Thanks again, sorry if I’m clogging up the board here…

Like most things, there’s no free lunch. There is nothing special about the settlement period. As an investor, the ex dividend date is what you need to pay attention to (Oct 22 in this case).

Starting on Oct 22, RY trades with no dividend. Consequently, the buyer on Oct 21 gets the div and the seller does not. Starting on Oct 22, there is no dividend for either buyers or sellers (except of course the dividend that will be paid in 3 months time).

First off, I think you should read my article on dividend dates. That should clear up your uncertainty.

You should realize that the company does not actually declare the ex-Dividend date (and, in fact, they will be breaking the rules of the Exchange if they do). The company declares only the Record Date and the Payment Date.

The Record Date for the RY preferreds is October 26, which is Monday. What that means is that whoever actually owns the shares at the Close of Business on October 26 gets the dividend

The ex-dividend date is determined and publicized by the Exchange. They determine the first date on which a purchaser will not actually own the shares at 5pm on the date the trade settles. In this case, it was October 22, because a trade executed for normal settlement on October 22 will settle on October 27, which is after the Record Date.

Sometimes, relatively rarely and basically never for retail, you can trade for special settlement – one day settlement or fifteen, or any other period you agree with the buyer. Then, of course, the ex-dividend date calculated by the Exchange is irrelevant because it is calculated for normal settlement.

During the settlement period, the seller has contracted to sell the shares, but the shares have not actually changed hands and the buyer has not yet paid for them. Ownership remains with the seller until the trade actually settles.

Think of it like selling a house: you sell your house on January 20 with a Closing Date of March 31. You don’t get any actual cash until March 31, because until March 31 you still own the house. If the house burns to the ground on March 20, you’re on the hook – you will have to go to the buyer and tell him ‘Look … you know that thing I agreed to sell you on March 31 … um … I can’t actually deliver it’.

You might find it of interest to know that – in the old days, anyway – all the major brokers had a unit in their Operations Department called “Dividend Claims”, which had the purpose of tracking down and claiming dividends to which the brokerage was entitled, but did not actually receive.

Say, for instance Merrill Lynch buys (on behalf of a customer) 1,000 shares of XYZ the day before the ex-dividend date (and therefore ML’s customer is entitled to the dividend). Three days later, which happens to be the Record Date, the trade settles: TD sends over certificates for 1,000 shares and gets the money in exchange.

But, sadly, these certificates are registered to TD, and at the end of the day they still haven’t been transferred to ML’s ownership, because this takes a week (and they’ll probably be left in TD’s name anyway, because transfer is expensive).

Therefore, when the company (or its Transfer Agent) does its calculations to determine who owns the shares at 5pm, it sees that the shares are registered to TD and therefore sends the cheque to TD.

TD cashes the cheque, of course, but recognizes that it wasn’t actually entitled to this dividend, so it records a deposit to its claims account. Merrill, when it goes through its figures, realizes that it paid a dividend on the 1,000 shares to its customer (who was entitled to it) but hasn’t yet received anything from the company.

So the Claims unit of Merrill has to figure out who the dividend went to. After examining their records and microfiched photographs of all the settlements for that stock, they determine that it is TD who owes them the money. So they send a dividend claim to TD and TD sends them the money.

This could get pretty hairy, as I’m sure you can see, what with ML having intermediary ownership to 20-million shares of Imperial Oil on behalf of 20,000 customers, with certificates whizzing in and out every day … but it’s simpler nowadays that electronic ownership through CDS (or equivalent clearing-houses in other countries) has become pervasive.