Nothing happened today.

It looked for a long time as if there would be a significant pullback in the preferred share indices today, but the Forces of Goodness and Truth mounted a counterattack a little after 3:30pm that recouped a good chunk of the day’s losses:

Click for Big

TXPL closed at 706.54. You can see a tiny little sliver of green at the extreme right-hand side of the chart, showing how the index rose 3+ points in the dying seconds of the day … at 3:58pm, the index level was 702.97.

But one must remember two very important things when looking at TXPL! First, it’s a price index and therefore of highly limited informational value. All the Royal Bank issues went ex-dividend today and this caused about 5bp divergence on the day between the Total Return index and the Price Index. Additionally, TXPL is calculated on a close/close basis; while the late rally will have causes some distortion (in that the closes will be, in general, further above the bid than otherwise), there will have been even more distortion in the prior number due to yesterday‘s wild ride. In addition, TXPL is riddled with junk, which I don’t pay much attention to. What I’m trying to say is …

It was a good, albeit mixed day for the Canadian preferred share market, with PerpetualDiscounts gaining 17bp, FixedResets up 41bp and DeemedRetractibles off 27bp. The bad part of the Performance Highlights table is dominated by insurance issues; the good part is more heterogeneous. Volume was high.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

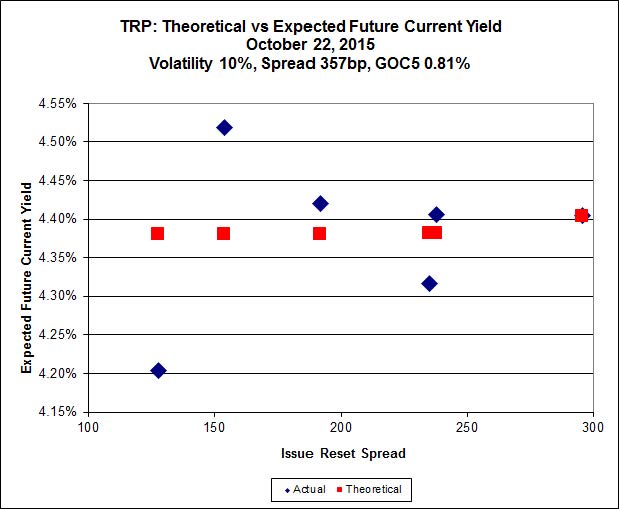

Here’s TRP:

Click for Big

Implied Volatility declined to more reasonable levels today.

TRP.PR.B, which resets 2020-6-30 at +128, is bid at 12.43 to be $0.50 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $0.41 cheap at its bid price of 13.00.

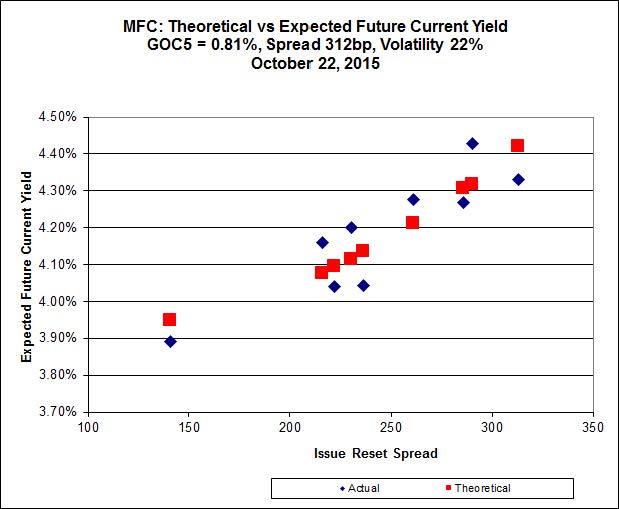

Click for Big

Implied Volatility declined slightly for the MFC series today.

Most expensive is MFC.PR.H, resetting at +313bp on 2017-3-19, bid at 22.75 to be 0.46 rich, while MFC.PR.G resetting at +290bp on 2016-12-19, is bid at 20.95 to be 0.54 cheap.

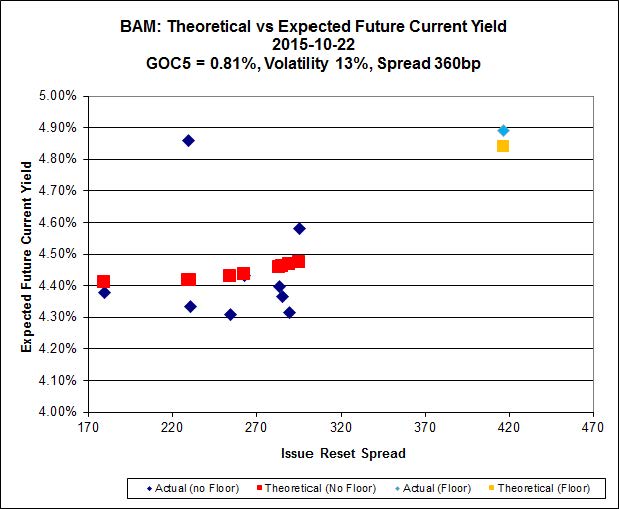

Click for Big

The fit on the BAM issues continues to be poor. Implied Volatility increased a little today, but this is a figure that’s very highly dependent on the performance of the high-spread issue BAM.PF.H.

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 16.00 to be $1.61 cheap. BAM.PF.A, resetting at +290bp on 2018-9-30 is bid at 21.50 and appears to be $0.74 rich.

Click for Big

Implied Volatility remains high.

FTS.PR.K, with a spread of +205bp, and bid at 18.95, looks $1.33 expensive and resets 2019-3-1. FTS.PR.H, with a spread of +145bp and resetting 2020-6-1, is bid at 13.50 and is $0.55 cheap.

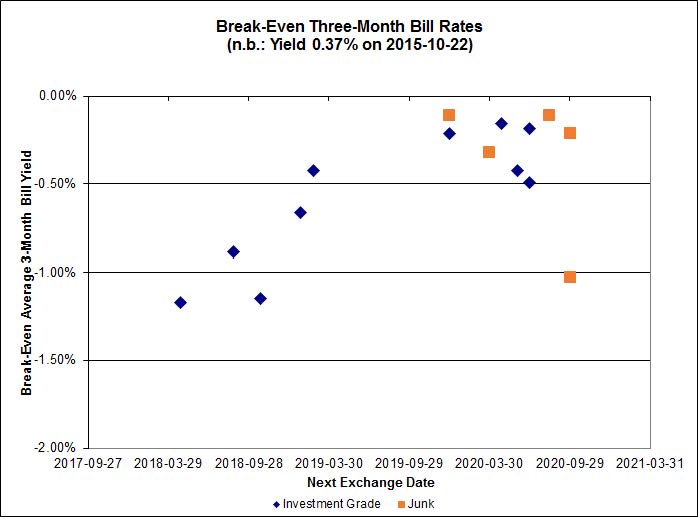

Click for Big

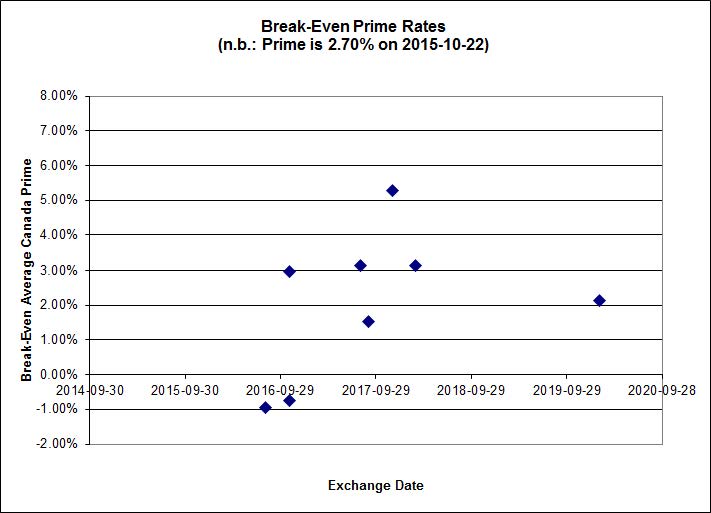

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.88%, with two outliers below -2.00%. The distribution is bimodal, with bank NVCC non-compliant pairs averaging -1.29% and other issues averaging -0.29%. There are two junk outliers above 0.00% and three below -2.00%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 1.2813 % | 1,739.8 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 1.2813 % | 3,042.0 |

| Floater | 4.27 % | 4.35 % | 61,882 | 16.71 | 3 | 1.2813 % | 1,849.5 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.2028 % | 2,752.2 |

| SplitShare | 4.36 % | 5.38 % | 77,471 | 2.96 | 5 | -0.2028 % | 3,225.4 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.2028 % | 2,516.6 |

| Perpetual-Premium | 5.88 % | 5.83 % | 67,837 | 14.02 | 5 | -0.0080 % | 2,476.2 |

| Perpetual-Discount | 5.67 % | 5.73 % | 80,908 | 14.23 | 33 | 0.1726 % | 2,516.5 |

| FixedReset | 4.93 % | 4.41 % | 204,535 | 15.87 | 76 | 0.4051 % | 2,071.0 |

| Deemed-Retractible | 5.24 % | 5.05 % | 106,388 | 5.47 | 33 | -0.2656 % | 2,547.3 |

| FloatingReset | 2.51 % | 4.06 % | 66,285 | 5.82 | 9 | -0.1871 % | 2,145.9 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| MFC.PR.F | FixedReset | -3.96 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.31 Bid-YTW : 9.51 % |

| SLF.PR.D | Deemed-Retractible | -2.28 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.11 Bid-YTW : 7.49 % |

| MFC.PR.B | Deemed-Retractible | -2.06 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.93 Bid-YTW : 7.19 % |

| IFC.PR.C | FixedReset | -1.87 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.44 Bid-YTW : 6.92 % |

| SLF.PR.C | Deemed-Retractible | -1.84 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.22 Bid-YTW : 7.42 % |

| GWO.PR.R | Deemed-Retractible | -1.78 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.55 Bid-YTW : 6.92 % |

| SLF.PR.E | Deemed-Retractible | -1.73 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.40 Bid-YTW : 7.35 % |

| BNS.PR.C | FloatingReset | -1.63 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.37 Bid-YTW : 4.09 % |

| SLF.PR.J | FloatingReset | -1.60 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.53 Bid-YTW : 9.29 % |

| NA.PR.Q | FixedReset | -1.58 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.36 Bid-YTW : 3.88 % |

| SLF.PR.B | Deemed-Retractible | -1.55 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.66 Bid-YTW : 6.85 % |

| MFC.PR.N | FixedReset | -1.48 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.91 Bid-YTW : 6.52 % |

| BAM.PF.B | FixedReset | -1.47 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-22 Maturity Price : 19.41 Evaluated at bid price : 19.41 Bid-YTW : 4.69 % |

| SLF.PR.A | Deemed-Retractible | -1.37 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.61 Bid-YTW : 6.83 % |

| GWO.PR.N | FixedReset | -1.34 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.04 Bid-YTW : 9.44 % |

| FTS.PR.M | FixedReset | -1.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-22 Maturity Price : 20.29 Evaluated at bid price : 20.29 Bid-YTW : 4.35 % |

| MFC.PR.C | Deemed-Retractible | -1.21 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.40 Bid-YTW : 7.38 % |

| SLF.PR.H | FixedReset | -1.19 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.39 Bid-YTW : 7.84 % |

| BNS.PR.R | FixedReset | -1.10 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.31 Bid-YTW : 3.82 % |

| GWO.PR.H | Deemed-Retractible | -1.04 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.92 Bid-YTW : 6.74 % |

| MFC.PR.M | FixedReset | -1.03 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.11 Bid-YTW : 6.46 % |

| PWF.PR.S | Perpetual-Discount | -1.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-22 Maturity Price : 21.38 Evaluated at bid price : 21.38 Bid-YTW : 5.64 % |

| RY.PR.H | FixedReset | 1.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-22 Maturity Price : 19.09 Evaluated at bid price : 19.09 Bid-YTW : 4.25 % |

| RY.PR.N | Perpetual-Discount | 1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-22 Maturity Price : 22.37 Evaluated at bid price : 22.66 Bid-YTW : 5.39 % |

| BMO.PR.T | FixedReset | 1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-22 Maturity Price : 19.20 Evaluated at bid price : 19.20 Bid-YTW : 4.28 % |

| FTS.PR.K | FixedReset | 1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-22 Maturity Price : 19.10 Evaluated at bid price : 19.10 Bid-YTW : 4.08 % |

| BNS.PR.O | Deemed-Retractible | 1.06 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2015-11-21 Maturity Price : 25.50 Evaluated at bid price : 25.77 Bid-YTW : -8.79 % |

| MFC.PR.I | FixedReset | 1.17 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.60 Bid-YTW : 5.86 % |

| BAM.PR.Z | FixedReset | 1.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-22 Maturity Price : 21.25 Evaluated at bid price : 21.25 Bid-YTW : 4.66 % |

| VNR.PR.A | FixedReset | 1.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-22 Maturity Price : 21.17 Evaluated at bid price : 21.17 Bid-YTW : 4.41 % |

| BMO.PR.W | FixedReset | 1.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-22 Maturity Price : 18.85 Evaluated at bid price : 18.85 Bid-YTW : 4.33 % |

| CM.PR.O | FixedReset | 1.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-22 Maturity Price : 19.47 Evaluated at bid price : 19.47 Bid-YTW : 4.26 % |

| TRP.PR.F | FloatingReset | 1.47 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-22 Maturity Price : 14.45 Evaluated at bid price : 14.45 Bid-YTW : 3.99 % |

| SLF.PR.I | FixedReset | 1.57 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.66 Bid-YTW : 6.23 % |

| GWO.PR.S | Deemed-Retractible | 1.67 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.80 Bid-YTW : 6.02 % |

| FTS.PR.F | Perpetual-Discount | 1.75 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-22 Maturity Price : 21.84 Evaluated at bid price : 22.08 Bid-YTW : 5.63 % |

| MFC.PR.K | FixedReset | 1.76 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.07 Bid-YTW : 6.91 % |

| RY.PR.O | Perpetual-Discount | 1.91 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-22 Maturity Price : 22.18 Evaluated at bid price : 22.53 Bid-YTW : 5.42 % |

| RY.PR.M | FixedReset | 1.97 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-22 Maturity Price : 20.23 Evaluated at bid price : 20.23 Bid-YTW : 4.31 % |

| BAM.PR.K | Floater | 2.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-22 Maturity Price : 10.94 Evaluated at bid price : 10.94 Bid-YTW : 4.35 % |

| TRP.PR.A | FixedReset | 2.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-22 Maturity Price : 15.50 Evaluated at bid price : 15.50 Bid-YTW : 4.68 % |

| MFC.PR.H | FixedReset | 2.36 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.43 Bid-YTW : 5.00 % |

| RY.PR.J | FixedReset | 2.54 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-22 Maturity Price : 20.93 Evaluated at bid price : 20.93 Bid-YTW : 4.27 % |

| TD.PR.Y | FixedReset | 3.11 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.54 Bid-YTW : 3.36 % |

| TRP.PR.G | FixedReset | 3.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-22 Maturity Price : 21.40 Evaluated at bid price : 21.68 Bid-YTW : 4.41 % |

| TD.PF.D | FixedReset | 3.52 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-22 Maturity Price : 21.15 Evaluated at bid price : 21.15 Bid-YTW : 4.29 % |

| MFC.PR.L | FixedReset | 4.24 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.95 Bid-YTW : 7.09 % |

| IFC.PR.A | FixedReset | 7.05 % | Sort of a little bit real. The issue traded 12,581 shares today in a range of 15.60-34 before closing at 16.40-60, 14×5. The VWAP was 15.77. There were nine small trades timestamped from 3:53 to 3:58, inclusive, all executed between 15.69 and 15.74; then a trade at 16.02 for 100 shares timestamped 3:58, then 600 at 16.30 stamped 3:59. I also see 130 shares trading over 16.00 just before 3pm. So basically, this performance was running on fumes, probably from what the market-maker was smoking instead of maintaining an orderly market. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.40 Bid-YTW : 8.60 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| CM.PR.Q | FixedReset | 62,228 | TD sold blocks of 10,000 and 14,400 to Scotia, both at 21.50; TD crossed 12,500 at 21.49. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-22 Maturity Price : 21.40 Evaluated at bid price : 21.40 Bid-YTW : 4.24 % |

| CU.PR.I | FixedReset | 50,407 | Nesbitt crossed 40,000 at 25.25. YTW SCENARIO Maturity Type : Call Maturity Date : 2020-12-01 Maturity Price : 25.00 Evaluated at bid price : 25.25 Bid-YTW : 4.38 % |

| NA.PR.S | FixedReset | 49,447 | TD crossed 11,500 at 20.03; Nesbitt crossed 15,500 at 19.86. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-22 Maturity Price : 19.88 Evaluated at bid price : 19.88 Bid-YTW : 4.27 % |

| RY.PR.L | FixedReset | 48,835 | Desjardins crossed 39,700 at 25.10. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.97 Bid-YTW : 3.89 % |

| CM.PR.P | FixedReset | 41,280 | TD crossed 17,100 at 18.99. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-22 Maturity Price : 19.00 Evaluated at bid price : 19.00 Bid-YTW : 4.26 % |

| BAM.PF.H | FixedReset | 36,561 | Recent new issue. YTW SCENARIO Maturity Type : Call Maturity Date : 2020-12-31 Maturity Price : 25.00 Evaluated at bid price : 25.50 Bid-YTW : 4.65 % |

| There were 44 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| MFC.PR.N | FixedReset | Quote: 19.91 – 20.67 Spot Rate : 0.7600 Average : 0.4888 YTW SCENARIO |

| SLF.PR.H | FixedReset | Quote: 17.39 – 18.24 Spot Rate : 0.8500 Average : 0.6227 YTW SCENARIO |

| BAM.PF.D | Perpetual-Discount | Quote: 20.77 – 21.47 Spot Rate : 0.7000 Average : 0.4786 YTW SCENARIO |

| BAM.PR.X | FixedReset | Quote: 15.27 – 15.75 Spot Rate : 0.4800 Average : 0.2807 YTW SCENARIO |

| FTS.PR.G | FixedReset | Quote: 18.35 – 18.92 Spot Rate : 0.5700 Average : 0.3890 YTW SCENARIO |

| BNS.PR.C | FloatingReset | Quote: 22.37 – 22.99 Spot Rate : 0.6200 Average : 0.4390 YTW SCENARIO |

With the recent election behind us and the possible changes to the TFSA, I’m not surprised at the past two days of activity. Volume in REITS was high, too.

I suspect banks were busy with loans to top up TFSAs.

I suspect banks were busy with loans to top up TFSAs

You could well be right, but I don’t have any good sources to confirm that suspicion.

IMHO the end of day forces of ‘Goodness and Truth’ that brought us back up from the selloff looked like hastily executed trades by an ETF MM desk to fill up their units to facilitate a late day request for a 750K CPD block (which crossed $0.16 above the closing print). Institutional buying is always nice to see.

IMHO the end of day forces of ‘Goodness and Truth’ that brought us back up from the selloff looked like hastily executed trades by an ETF MM desk to fill up their units to facilitate a late day request for a 750K CPD block (which crossed $0.16 above the closing print).

I’ve heard that elsewhere as well. Volume in CPD spiked on October 22 to 1,145,781 shares, compared to a 30-day average (as of November 5) of about maybe 200,000 shares.