Royal Bank of Canada has announced:

a domestic public offering of Non-Cumulative, 5-Year Rate Reset Preferred Shares Series BK.

Royal Bank of Canada will issue 12 million Preferred Shares Series BK priced at $25 per share to raise gross proceeds of $300 million. The bank has granted the Underwriters an option, exercisable in whole or in part, to purchase up to an additional 2 million Preferred Shares Series BK at the same offering price.

The Preferred Shares Series BK will yield 5.50 per cent annually, payable quarterly, as and when declared by the Board of Directors of Royal Bank of Canada, for the initial period ending May 24, 2021. Thereafter, the dividend rate will reset every five years at a rate equal to 4.53 per cent over the 5-year Government of Canada bond yield.

Subject to regulatory approval, on or after May 24, 2021, the bank may redeem the Preferred Shares Series BK in whole or in part at par. Holders of Preferred Shares Series BK will, subject to certain conditions, have the right to convert all or any part of their shares to Non-Cumulative Floating Rate Preferred Shares Series BL on May 24, 2021 and on May 24 every five years thereafter.

Holders of the Preferred Shares Series BL will be entitled to receive a non-cumulative quarterly floating dividend, as and when declared by the Board of Directors of Royal Bank of Canada, at a rate equal to the 3-month Government of Canada Treasury Bill yield plus 4.53 per cent. Holders of Preferred Shares Series BL will, subject to certain conditions, have the right to convert all or any part of their shares to Preferred Shares Series BK on May 24, 2026 and on May 24 every five years thereafter.

The offering will be underwritten by a syndicate led by RBC Capital Markets. The expected closing date is December 16, 2015.

We routinely undertake funding transactions to maintain strong capital ratios and a cost effective capital structure. Net proceeds from this transaction will be used for general business purposes.

They later announced:

that as a result of strong investor demand for its previously announced domestic public offering of Non-Cumulative, 5-Year Rate Reset Preferred Shares Series BK, the size of the offering has been increased to 27 million shares. The gross proceeds of the offering will now be $675 million. The bank has granted the Underwriters an option, exercisable in whole or in part, to purchase up to an additional 2 million Preferred Shares Series BK at the same offering price. The offering will be underwritten by a syndicate led by RBC Capital Markets. The expected closing date is December 16, 2015.

We routinely undertake funding transactions to maintain strong capital ratios and a cost effective capital structure. Net proceeds from this transaction will be used for general business purposes.

$675-million! That’s a monster issue!

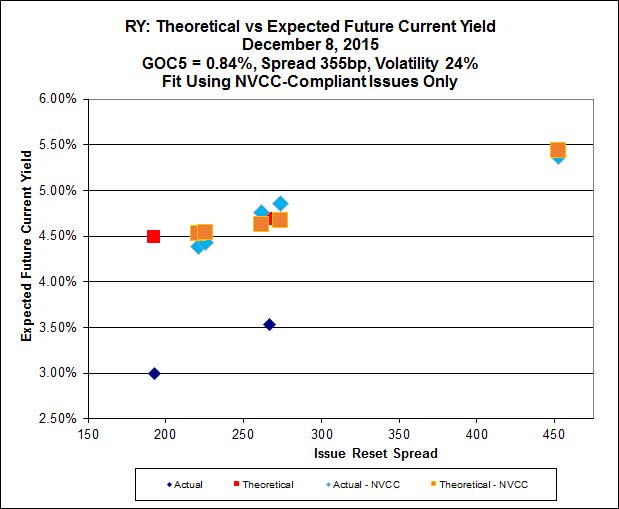

Implied Volatility analysis reveals that this issue – contrary to most new issues – is attractively priced, with a good concession to the market. Although the four extant NVCC-compliant issues appear to form a steeper curve without the influence of the new issue than with it, the Implied Volatility with the new issue included in the analysis is still a very high 24%. I consider this value to be ridiculously high; hence I expect a flattening of the curve; hence I consider the new issue more likely to outperform its peers than otherwise.

Click for Big

Update: Assiduous Reader prefQC reminds me in the comments that I neglected to discuss the lack of a floor rate on future resets of the issue.

The question of whether banks could issue NVCC-compliant preferred shares with a floor on future resets was first discussed when the feature first appeared, in the post New Issue: CU FixedReset, 4.50%+369M450, with a little information coming later in the comments to New Issue (Private): BMO FixedReset (?) 5.85%+???.

There is no authoritative new information available – but I will infer from the absence of a reset floor from this issue and from the New Issue: BNS FixedReset 5.50%+451 that was also announced today that the feature has been disallowed by OSFI. So, whatever one might think of my reasoning, I came up with the wrong answer.

As is always the case, OSFI’s traditions of secrecy, contempt for investors and general incompetence are well summed up in the fact that they have published no commentary on this issue.

Update, 2015-12-10: I’ve heard a whisper from the street that OSFI said ‘no’ to a minimum reset.

Update, 2015-12-18: Assiduous Reader prefobsessed alerted me to a Barry Critchley column titled Banks have to pay up if they want to issue preferred shares: Royal and BNS offer 5.50% in which he makes a passing, but unsupported assertion regarding OSFI’s views on floor rates for NVCC-compliant issues:

Other pref share issuers also face a similar environment: if they want to raise capital in this form they have to pay up. Last week, Brookfield Infrastructure Partners raised $125 million at a coupon of 5.50 per cent. But other issuers have more flexibility than the banks: they can include a so-called floor coupon, which means that the new rate in five years will at least be equal to the current coupon. The bank’s regulator OSFI has ruled that option out for the banks, at least for the time being.

So has the guaranteed minimum reset feature already become just a “passing fad” in the preferred market?

Thanks for reminding me! I think there will still be lots of minimum reset features, but not from banks. I’ve updated to post to address the absence of the feature from this issue.

I’m curious how you would time a trade in either one of these offerings given that the RBC rate reset is issued on the same day as the US Federal Reserve will presumably raise interest rates and the Scotia offering issues the day after.

If US rates go up what do you predict will be the impact on the price of both of these offerings?

What!!! +453 bps when their prior issues RY.PR. J and RY.PR.M only reset at +274 and +262 bps??? In other words, what was issued less than a year ago at $25 will soon only be worth $17??? It does not help building confidence in the Canadian pref market.

But…

What was issued a year ago at +274 and 262 bps may be around for longer than the new one at +453. It’s easy enough to concoct a scenario for the old one to be the superior alternative, even without considering the potential for capital appreciation.

… Well if you don’t consider the potential capital appreciation, the fact of the matter is then that +453 from the same issuer is better than +262/+274. Yes, the former is more likely to be bought back (and I believe it will) in 2020. This makes it a “quasi retractible” making it even more valuable in the eyes of Mr. Market who is scared by perpuitity. More significantly, these new issues (and the huge size of the RY one) show that your own reputable issuer who sold you something at $25 less than a year ago may destroy the value of what you had just bought from him. GOC 5 years did not increase in the meantime, it went lower! This means that the earlier formulas were flawed. If RY and TD banks feltl the need of a spread of +453 bps (I assume TD’s at +451bps for the same end result is just the result of a different closing date) to raise capital, how much do you think will be needed by the lower rated issuers (see the hit the resetable with minimum rates also took since those issues).

If indeed the OSFI has nixed the floor rate, as James surmises, then the “M” issues will definitely be redeemed at the next call date. (Otherwise the issuers would be in violation…)

I’m curious how you would time a trade in either one of these offerings given that the RBC rate reset is issued on the same day as the US Federal Reserve will presumably raise interest rates and the Scotia offering issues the day after.

I would execute a trade if I held something I considered significantly more expensive; if I didn’t hold such an investment, I wouldn’t trade. I would not play guessing games about the reaction of the market to the Fed rate announcement.

+453 bps when their prior issues RY.PR. J and RY.PR.M only reset at +274 and +262 bps??? In other words, what was issued less than a year ago at $25 will soon only be worth $17???

To be fair, it’s not the issuer’s fault. It’s simply that the market is demanding a higher spread over GOC-5 than it used to.

What was issued a year ago at +274 and 262 bps may be around for longer than the new one at +453. It’s easy enough to concoct a scenario for the old one to be the superior alternative, even without considering the potential for capital appreciation.

Quite right, although from the Implied Volatility analysis I conclude that the new issue is relatively cheap. Of course, if you take a view on spreads (e.g., that new issue spreads will decline from the current +453), then the Implied Volatility analysis does not apply..

More significantly, these new issues (and the huge size of the RY one) show that your own reputable issuer who sold you something at $25 less than a year ago may destroy the value of what you had just bought from him.

The issuer didn’t hurt the value – the market did. I’m sure that the bank would have been very happy to pay less for their capital requirements, but in this environment it is simply not possible.

If RY and TD banks feltl the need of a spread of +453 bps (I assume TD’s at +451bps for the same end result is just the result of a different closing date) to raise capital, how much do you think will be needed by the lower rated issuers (see the hit the resetable with minimum rates also took since those issues).

Well, that’s the $64 question, isn’t it? How much of the increase is due to the overall market movement; how much is due to a difference in perception of the credit quality of the banks; and how will the market movement affecting investment-grade issuers affect lesser issuers? Place yer bets, gents, place yer bets!

If indeed the OSFI has nixed the floor rate, as James surmises, then the “M” issues will definitely be redeemed at the next call date. (Otherwise the issuers would be in violation…)

None of the issues with a floor have been issued by OSFI-regulated entities.