Canadian Utilities Limited has announced (emphasis added):

it has entered into an agreement with a syndicate of underwriters co-led by BMO Capital Markets and RBC Capital Markets, and including TD Securities Inc., Scotiabank, CIBC, Canaccord Genuity Corp., and GMP Securities L.P. The underwriters have agreed to buy 4,000,000 4.50% Cumulative Redeemable Second Preferred Shares Series FF at a price of $25.00 per share for aggregate gross proceeds of $100,000,000. The proceeds will be used for capital expenditures, to repay indebtedness and for other general corporate purposes.

Canadian Utilities Limited has granted the underwriters an option to purchase at the offering price an additional 2,000,000 Series FF Preferred Shares exercisable in whole or in part at any time up to 7:00 AM (Calgary time) on the date that is two business days prior to closing. Should the option be fully exercised, the total gross proceeds of the Series FF Preferred Share offering will be $150,000,000.

The Series FF Preferred Shares will be issued to the public at a price of $25.00 per share and holders will be entitled to receive fixed cumulative preferential cash dividends, payable quarterly for an initial period of five years, as and when declared by the Board of Directors of the Company at an annual rate of $1.125 per share, to yield 4.50% annually.

Thereafter, the dividend rate will reset every five years to the then current 5-Year Government of Canada Bond yield plus 3.69%, and in any event, no less than 4.50%. On December 1, 2020, and on December 1 of every fifth year thereafter, the Company may redeem the Series FF Preferred Shares in whole or in part at par.

Holders may elect to convert any or all of their Series FF Preferred Shares into an equal number of Cumulative Redeemable Second Preferred Shares Series GG on December 1, 2020, and on December 1 of every fifth year thereafter. Holders of the Series GG Preferred Shares will be entitled to receive quarterly floating rate cumulative preferential cash dividends, as and when declared by the Board of Directors of the Company, equal to the then current 3-month Government of Canada Treasury Bill yield plus 3.69%. On December 1, 2025, and on December 1, of every fifth year thereafter, the Company may redeem the Series GG Preferred Shares in whole or in part at par. On any other date, the Company may redeem the Series GG Preferred Shares in whole or in part by the payment of $25.50 for each share to be redeemed.

The offering is being made only in the provinces of Canada by means of a prospectus supplement and the closing date of the issue is expected to be on or about September 24, 2015.

Assiduous Readers with sharp eyes will have noticed the bolding and murmured to themselves ‘oh, a minimum rate on reset guarantee! So that’s what the “M450” in the headline of this post means! It wasn’t a typo! Gee, I wish I hadn’t sent that vituperative eMail!’

The minimum rate guarantee seems to have been very popular, since later in the day they announced:

that as a result of strong investor demand for its previously announced offering of Cumulative Redeemable Second Preferred Shares Series FF, the size of the offering has been increased to 10,000,000 shares. The aggregate gross proceeds will now be $250,000,000.

It’s an interesting idea and I’m sure that investors will be demanding this feature for some time to come (images of stolen horses and barn doors come to mind!). But will the banks and insurers issue them? We can take a refreshing look at the Capital Adequacy Guidelines, Chapter 2, “Definition of Capital” for some hints … I don’t see anything that would stop them.

Item 2.1.2.1(11)(4) states:

Is perpetual, i.e. there is no maturity date and there are no step-ups [Footnote 14] or other incentives to redeem [Footnote 15].

Footnote 14 reads: A step-up is defined as a call option combined with a pre-set increase in the initial credit spread of the instrument at a future date over the initial dividend (or distribution) rate after taking into account any swap spread between the original reference index and the new reference index. Conversion from a fixed rate to a floating rate (or vice versa) in combination with a call option without any increase in credit spread would not constitute a step-up.

Footnote 15 reads: Other incentives to redeem include a call option combined with a requirement or an investor option to convert the instrument into common shares if the call is not exercised.

So I don’t think there’s a problem there – OSFI is worried about issuance of 2% century-wink-wink-nudge-nudge bonds that step up to 25% on the first call date, thereby giving the issuer a certain incentive to redeem. But that’s not the case here; there is a floor, but it will not necessarily be applied.

The other rule I thought of that might throw a monkey-wrench into bank issuance was item 2.1.2.1(11)(9):

The instrument cannot have a credit sensitive dividend feature, that is a dividend/coupon that is reset periodically based in whole or in part on the institution or organization’s credit standing [Footnote 18]

Footnote 18 reads: Institutions may use a broad index as a reference rate in which the issuing institution is a reference entity, however, the reference rate should not exhibit significant correlation with the institution’s credit standing. If an institution plans to issue capital instruments where the margin is linked to a broad index in which the institution is a reference entity, the institution should ensure that the dividend/coupon is not credit-sensitive. [BCBS FAQs #12, p.5]

So, while it was worth checking, that particular rule is very specific that increases in spread based on credit quality is prohibited, but increases in spread based on interest rates seems to be OK.

So I think this minimum rate guarantee structure will be permissible for banks. But I’m neither OSFI nor an underwriter nor a bank treasury analyst!

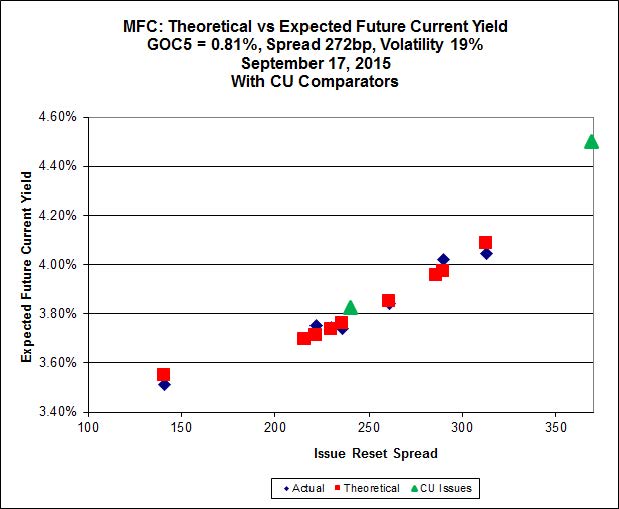

Update, 2015-9-17: This chart compares the CU issues to extant MFC issues. See the comments for discussion.

Click for Big

… And how will you call this new beast: the “minimum return resetable”? Unless you tell me resetting at +369 bps is historically logic for this credit quality (It looks to me as a generous rate reset), this issue should not long lived and redeemed in five years. I also note that the Floater against which this floater can be exchanged for every five years does not seem to have the minimum protection the originating issue has. Cheers!

I am surprised that its older cousin fixed-reset CU.PR.C, which has a yield of about 3.9%, has not dropped more in price since yesterday’s announcement. What am I missing?

(It looks to me as a generous rate reset), this issue should not long lived and redeemed in five years.

I agree – 369bp is a very high spread for a good credit like CU.

I also note that the Floater against which this floater can be exchanged for every five years does not seem to have the minimum protection the originating issue has.

Yes, that part’s very odd.

I am surprised that its older cousin fixed-reset CU.PR.C, which has a yield of about 3.9%, has not dropped more in price since yesterday’s announcement

It’s basically in line with MFC. Observe that CU.PR.C has an Issue Reset Spread of 240bp, a Yield-To-Worst of about 3.90% and an Expected Future Current Yield of 3.83% at today’s price of 20.97, while the new issue figures are 369bp, 4.40% YTW and 4.50% EFCY when priced at par. These points are plotted on the chart I’ve just added to the main post, and are within ballpark of where you would expect them to be if these were MFC issues.

Of course, as I’ve pointed out before, the Implied Volatility for the MFC series is much higher than one would expect for truly perpetual issues, although much lower than one would expect if the issues were considered retractible. If Implied Volatility were to decline to levels I consider more reasonable for unregulated (and NVCC-compliant) issues, then this would involve a relative increase in the EFCY for CU.PR.C and therefore a relative decrease in price.

It will also be noted that the above argument implicitly assigns a value of zero to the rate floor attribute. I don’t think the floor is worth much in the current environment, but it should be worth something!

Thanks James for the detailed response. Now I’ll need to put on my “thinking cap” in order to fully digest it…

[…] is a FixedReset, 4.50%+369M450, that commenced trading 2015-9-24 after being announced 2015-9-14. The issue reset to its minimum rate of 4.50% (unchanged) effective 2020-12-1 and there was no […]