There were no dissents. The move was met with cheers:

The trouble nowadays, though, is that when people refer to “lift-off”, I don’t know whether they’re talking about the Fed rate increase or the Canadian preferred share market!

The Canadian preferred share market was on fire again today, with PerpetualDiscounts up 102bp, FixedResets winning 336bp and DeemedRetractibles gaining 59bp. The Performance Highlights table is ridiculously long again, of course, with no less than fifteen issues returning more than 5.00% on the day. Volume was again very, very heavy.

PerpetualDiscounts now yield 5.86%, equivalent to 7.62% interest at the standard equivalency factor of 1.3x. Long corporates now yield a little over 4.2%, so the pre-tax interest-equivalent spread (in this context, the “Seniority Spread”) is now about 340bp, down only slightly (and perhaps spuriously) from the 345bp reported December 9

Similarly, TXPL is somewhere close to 773.32, down 3.68% on the month-to-date but 9.08% above the December 14 low.

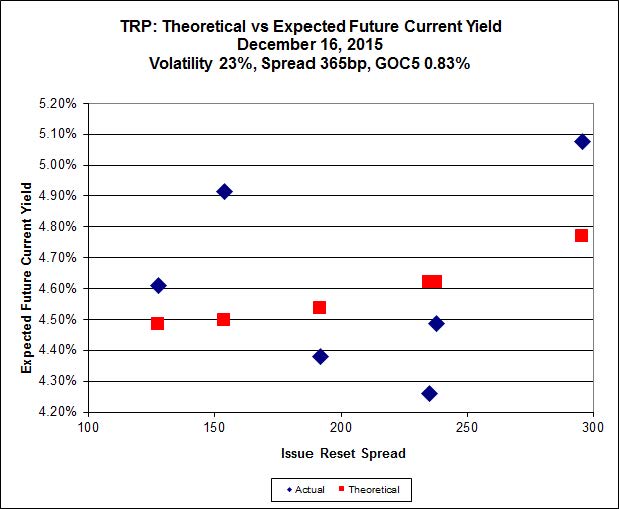

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 18.66 to be $1.45 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $1.12 cheap at its bid price of 12.06.

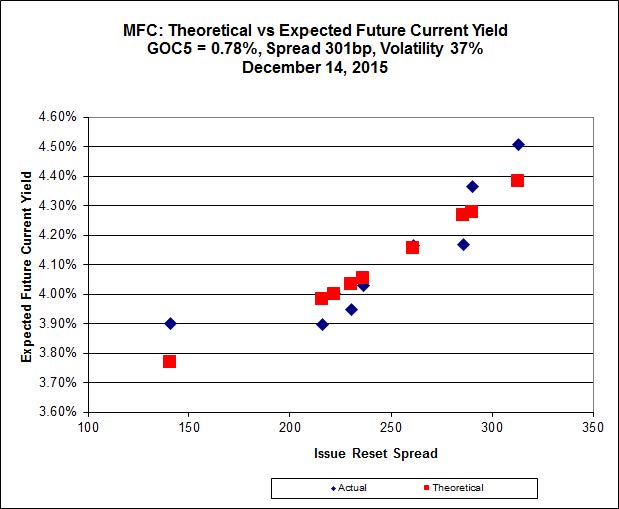

Most expensive is MFC.PR.H, resetting at +313bp on 2017-3-19, bid at 21.96 to be 0.64 cheap, while MFC.PR.I, resetting at +286bp on 2017-9-19, is bid at 22.13 to be 0.51 rich.

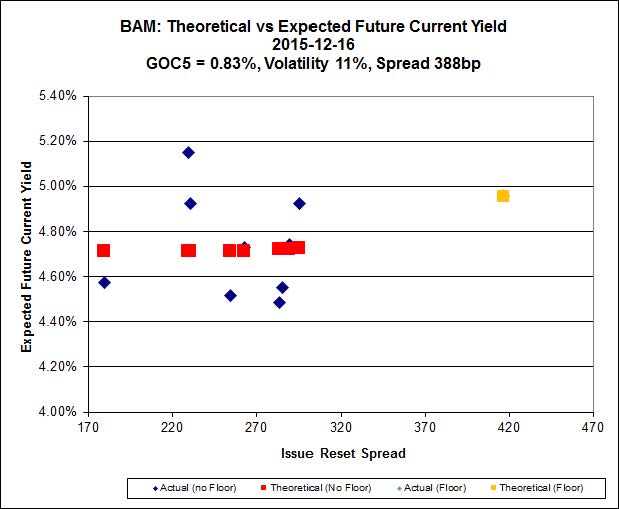

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 15.20 to be $1.41 cheap. BAM.PF.G, resetting at +284bp on 2020-6-30 is bid at 20.45 and appears to be $1.01 rich.

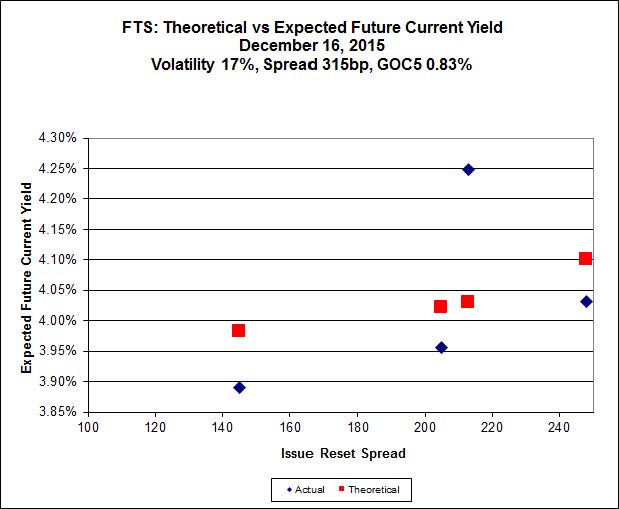

FTS.PR.M, with a spread of +248bp, and bid at 20.53, looks $0.35 expensive and resets 2019-12-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 17.42 and is $0.94 cheap.

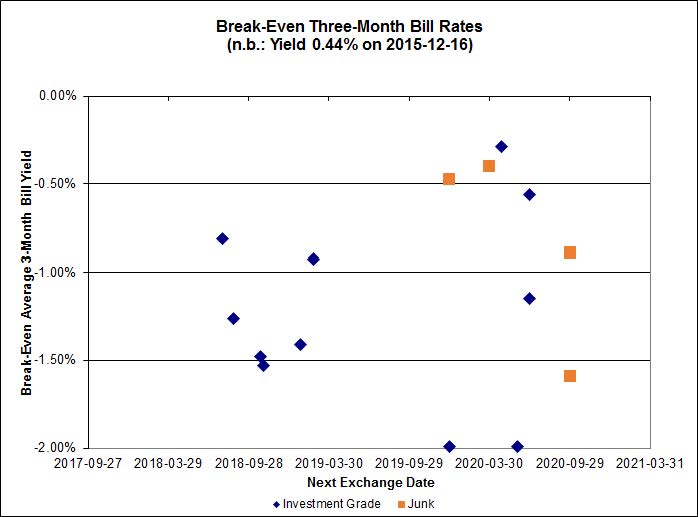

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -1.33%, with one outlier below -2.00%. There are two junk outliers below -2.00% and four above 0.00%. Note the vertical axis of this graph has been changed.

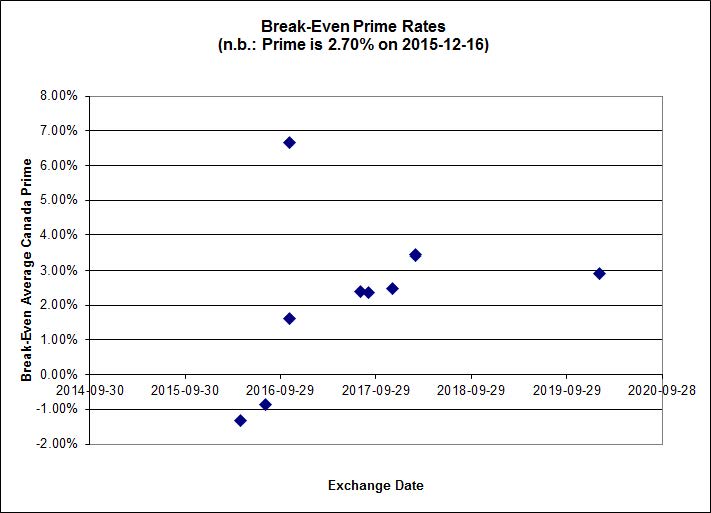

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| Performance Highlights |

| Issue |

Index |

Change |

Notes |

| PVS.PR.E |

SplitShare |

-1.98 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-10-31

Maturity Price : 25.00

Evaluated at bid price : 23.82

Bid-YTW : 6.43 % |

| BAM.PR.K |

Floater |

-1.31 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 10.52

Evaluated at bid price : 10.52

Bid-YTW : 4.49 % |

| BAM.PF.H |

FixedReset |

1.00 % |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2020-12-31

Maturity Price : 25.00

Evaluated at bid price : 25.20

Bid-YTW : 4.80 % |

| CU.PR.I |

FixedReset |

1.01 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 23.13

Evaluated at bid price : 24.90

Bid-YTW : 4.44 % |

| RY.PR.B |

Deemed-Retractible |

1.05 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 24.97

Bid-YTW : 4.80 % |

| RY.PR.D |

Deemed-Retractible |

1.06 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 24.88

Bid-YTW : 4.67 % |

| MFC.PR.C |

Deemed-Retractible |

1.10 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.31

Bid-YTW : 7.40 % |

| IFC.PR.C |

FixedReset |

1.10 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 19.26

Bid-YTW : 6.91 % |

| PWF.PR.H |

Perpetual-Premium |

1.11 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 24.43

Evaluated at bid price : 24.67

Bid-YTW : 5.91 % |

| FTS.PR.K |

FixedReset |

1.11 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 18.20

Evaluated at bid price : 18.20

Bid-YTW : 4.15 % |

| SLF.PR.C |

Deemed-Retractible |

1.14 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.32

Bid-YTW : 7.31 % |

| CU.PR.D |

Perpetual-Discount |

1.15 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 21.19

Evaluated at bid price : 21.19

Bid-YTW : 5.84 % |

| PWF.PR.L |

Perpetual-Discount |

1.15 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 21.82

Evaluated at bid price : 22.06

Bid-YTW : 5.86 % |

| POW.PR.A |

Perpetual-Discount |

1.21 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 23.99

Evaluated at bid price : 24.24

Bid-YTW : 5.87 % |

| GWO.PR.P |

Deemed-Retractible |

1.23 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 23.96

Bid-YTW : 6.01 % |

| TRP.PR.B |

FixedReset |

1.24 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 11.44

Evaluated at bid price : 11.44

Bid-YTW : 4.51 % |

| SLF.PR.D |

Deemed-Retractible |

1.25 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.21

Bid-YTW : 7.38 % |

| ELF.PR.F |

Perpetual-Discount |

1.27 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 22.06

Evaluated at bid price : 22.35

Bid-YTW : 6.03 % |

| TRP.PR.E |

FixedReset |

1.30 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 18.66

Evaluated at bid price : 18.66

Bid-YTW : 4.54 % |

| BAM.PR.B |

Floater |

1.31 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 10.84

Evaluated at bid price : 10.84

Bid-YTW : 4.36 % |

| BIP.PR.A |

FixedReset |

1.32 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 19.22

Evaluated at bid price : 19.22

Bid-YTW : 5.70 % |

| PWF.PR.F |

Perpetual-Discount |

1.35 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 22.29

Evaluated at bid price : 22.56

Bid-YTW : 5.90 % |

| PVS.PR.D |

SplitShare |

1.38 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2021-10-08

Maturity Price : 25.00

Evaluated at bid price : 22.06

Bid-YTW : 7.06 % |

| IAG.PR.A |

Deemed-Retractible |

1.38 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.55

Bid-YTW : 7.32 % |

| BAM.PR.T |

FixedReset |

1.40 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 15.95

Evaluated at bid price : 15.95

Bid-YTW : 4.96 % |

| FTS.PR.J |

Perpetual-Discount |

1.41 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 21.55

Evaluated at bid price : 21.55

Bid-YTW : 5.56 % |

| TD.PR.T |

FloatingReset |

1.51 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.25

Bid-YTW : 4.07 % |

| CU.PR.E |

Perpetual-Discount |

1.53 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 21.25

Evaluated at bid price : 21.25

Bid-YTW : 5.82 % |

| ELF.PR.G |

Perpetual-Discount |

1.54 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 20.46

Evaluated at bid price : 20.46

Bid-YTW : 5.91 % |

| CU.PR.F |

Perpetual-Discount |

1.55 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 19.70

Evaluated at bid price : 19.70

Bid-YTW : 5.77 % |

| PWF.PR.E |

Perpetual-Discount |

1.55 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 23.33

Evaluated at bid price : 23.61

Bid-YTW : 5.90 % |

| MFC.PR.B |

Deemed-Retractible |

1.56 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.88

Bid-YTW : 7.18 % |

| CM.PR.Q |

FixedReset |

1.57 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 19.40

Evaluated at bid price : 19.40

Bid-YTW : 4.64 % |

| TD.PF.A |

FixedReset |

1.57 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 18.07

Evaluated at bid price : 18.07

Bid-YTW : 4.46 % |

| CU.PR.H |

Perpetual-Discount |

1.58 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 22.15

Evaluated at bid price : 22.50

Bid-YTW : 5.87 % |

| BIP.PR.B |

FixedReset |

1.60 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 22.20

Evaluated at bid price : 22.87

Bid-YTW : 6.03 % |

| PWF.PR.K |

Perpetual-Discount |

1.64 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 21.42

Evaluated at bid price : 21.68

Bid-YTW : 5.78 % |

| CM.PR.P |

FixedReset |

1.67 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 17.03

Evaluated at bid price : 17.03

Bid-YTW : 4.72 % |

| BAM.PR.R |

FixedReset |

1.67 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 15.20

Evaluated at bid price : 15.20

Bid-YTW : 5.11 % |

| TRP.PR.H |

FloatingReset |

1.71 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 10.10

Evaluated at bid price : 10.10

Bid-YTW : 4.25 % |

| ENB.PR.A |

Perpetual-Discount |

1.72 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 22.22

Evaluated at bid price : 22.50

Bid-YTW : 6.16 % |

| TD.PR.Z |

FloatingReset |

1.75 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.15

Bid-YTW : 4.23 % |

| TRP.PR.D |

FixedReset |

1.76 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 17.88

Evaluated at bid price : 17.88

Bid-YTW : 4.67 % |

| VNR.PR.A |

FixedReset |

1.82 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 19.00

Evaluated at bid price : 19.00

Bid-YTW : 4.88 % |

| BAM.PR.Z |

FixedReset |

1.85 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 19.25

Evaluated at bid price : 19.25

Bid-YTW : 4.99 % |

| SLF.PR.J |

FloatingReset |

1.87 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 13.05

Bid-YTW : 9.93 % |

| BAM.PR.C |

Floater |

1.90 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 10.70

Evaluated at bid price : 10.70

Bid-YTW : 4.41 % |

| RY.PR.I |

FixedReset |

1.91 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 24.00

Bid-YTW : 3.93 % |

| CU.PR.G |

Perpetual-Discount |

1.91 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 19.70

Evaluated at bid price : 19.70

Bid-YTW : 5.77 % |

| BAM.PR.G |

FixedFloater |

1.94 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 25.00

Evaluated at bid price : 13.11

Bid-YTW : 6.42 % |

| CIU.PR.C |

FixedReset |

2.03 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 13.60

Evaluated at bid price : 13.60

Bid-YTW : 3.95 % |

| BNS.PR.R |

FixedReset |

2.14 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 24.33

Bid-YTW : 3.87 % |

| TD.PF.B |

FixedReset |

2.18 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 17.83

Evaluated at bid price : 17.83

Bid-YTW : 4.51 % |

| BNS.PR.C |

FloatingReset |

2.23 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.00

Bid-YTW : 4.57 % |

| PWF.PR.T |

FixedReset |

2.25 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 21.93

Evaluated at bid price : 22.25

Bid-YTW : 3.71 % |

| BNS.PR.B |

FloatingReset |

2.29 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.87

Bid-YTW : 4.48 % |

| BNS.PR.D |

FloatingReset |

2.50 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 18.45

Bid-YTW : 6.73 % |

| NA.PR.Q |

FixedReset |

2.54 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 24.62

Bid-YTW : 3.74 % |

| W.PR.J |

Perpetual-Discount |

2.56 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 22.93

Evaluated at bid price : 23.21

Bid-YTW : 6.14 % |

| W.PR.H |

Perpetual-Discount |

2.59 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 22.71

Evaluated at bid price : 23.00

Bid-YTW : 6.08 % |

| BNS.PR.Z |

FixedReset |

2.81 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 19.37

Bid-YTW : 6.86 % |

| MFC.PR.H |

FixedReset |

2.86 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.96

Bid-YTW : 5.74 % |

| RY.PR.M |

FixedReset |

2.89 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 18.86

Evaluated at bid price : 18.86

Bid-YTW : 4.59 % |

| BNS.PR.Y |

FixedReset |

2.89 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 19.55

Bid-YTW : 6.19 % |

| TRP.PR.G |

FixedReset |

2.90 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 19.86

Evaluated at bid price : 19.86

Bid-YTW : 4.74 % |

| BMO.PR.S |

FixedReset |

2.91 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 18.42

Evaluated at bid price : 18.42

Bid-YTW : 4.45 % |

| MFC.PR.F |

FixedReset |

2.94 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 14.36

Bid-YTW : 9.30 % |

| TRP.PR.C |

FixedReset |

3.08 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 12.06

Evaluated at bid price : 12.06

Bid-YTW : 4.82 % |

| NA.PR.W |

FixedReset |

3.09 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 17.02

Evaluated at bid price : 17.02

Bid-YTW : 4.76 % |

| TD.PR.S |

FixedReset |

3.12 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 23.80

Bid-YTW : 3.79 % |

| FTS.PR.H |

FixedReset |

3.17 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 14.65

Evaluated at bid price : 14.65

Bid-YTW : 3.90 % |

| MFC.PR.J |

FixedReset |

3.25 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.65

Bid-YTW : 6.07 % |

| HSE.PR.E |

FixedReset |

3.26 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 19.00

Evaluated at bid price : 19.00

Bid-YTW : 5.77 % |

| NA.PR.S |

FixedReset |

3.39 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 17.68

Evaluated at bid price : 17.68

Bid-YTW : 4.76 % |

| BMO.PR.W |

FixedReset |

3.41 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 17.60

Evaluated at bid price : 17.60

Bid-YTW : 4.51 % |

| BMO.PR.R |

FloatingReset |

3.41 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.75

Bid-YTW : 3.72 % |

| SLF.PR.G |

FixedReset |

3.45 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 15.00

Bid-YTW : 8.67 % |

| BMO.PR.M |

FixedReset |

3.49 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 24.60

Bid-YTW : 3.18 % |

| RY.PR.J |

FixedReset |

3.50 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 19.20

Evaluated at bid price : 19.20

Bid-YTW : 4.62 % |

| BAM.PF.B |

FixedReset |

3.51 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 18.29

Evaluated at bid price : 18.29

Bid-YTW : 4.84 % |

| TD.PF.C |

FixedReset |

3.57 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 18.01

Evaluated at bid price : 18.01

Bid-YTW : 4.45 % |

| TD.PF.D |

FixedReset |

3.68 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 19.99

Evaluated at bid price : 19.99

Bid-YTW : 4.50 % |

| TD.PF.E |

FixedReset |

3.74 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 20.50

Evaluated at bid price : 20.50

Bid-YTW : 4.50 % |

| BMO.PR.T |

FixedReset |

3.75 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 17.71

Evaluated at bid price : 17.71

Bid-YTW : 4.51 % |

| IFC.PR.A |

FixedReset |

3.84 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 16.24

Bid-YTW : 8.54 % |

| MFC.PR.L |

FixedReset |

3.84 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 19.18

Bid-YTW : 6.84 % |

| BNS.PR.P |

FixedReset |

3.87 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 24.68

Bid-YTW : 3.34 % |

| IAG.PR.G |

FixedReset |

3.91 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.25

Bid-YTW : 5.88 % |

| FTS.PR.I |

FloatingReset |

3.96 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 11.80

Evaluated at bid price : 11.80

Bid-YTW : 4.03 % |

| RY.PR.H |

FixedReset |

3.99 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 18.25

Evaluated at bid price : 18.25

Bid-YTW : 4.40 % |

| RY.PR.Z |

FixedReset |

4.06 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 18.21

Evaluated at bid price : 18.21

Bid-YTW : 4.36 % |

| CM.PR.O |

FixedReset |

4.07 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 17.91

Evaluated at bid price : 17.91

Bid-YTW : 4.59 % |

| MFC.PR.G |

FixedReset |

4.09 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.36

Bid-YTW : 5.84 % |

| HSE.PR.C |

FixedReset |

4.18 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 17.71

Evaluated at bid price : 17.71

Bid-YTW : 5.71 % |

| BMO.PR.Q |

FixedReset |

4.37 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.54

Bid-YTW : 5.66 % |

| MFC.PR.K |

FixedReset |

4.38 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 19.05

Bid-YTW : 6.83 % |

| BNS.PR.Q |

FixedReset |

4.43 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 24.06

Bid-YTW : 3.81 % |

| FTS.PR.M |

FixedReset |

4.64 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 20.53

Evaluated at bid price : 20.53

Bid-YTW : 4.18 % |

| TRP.PR.A |

FixedReset |

4.67 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 15.70

Evaluated at bid price : 15.70

Bid-YTW : 4.47 % |

| HSE.PR.G |

FixedReset |

4.68 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 19.00

Evaluated at bid price : 19.00

Bid-YTW : 5.76 % |

| GWO.PR.N |

FixedReset |

5.04 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 13.76

Bid-YTW : 9.56 % |

| CU.PR.C |

FixedReset |

5.05 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 18.92

Evaluated at bid price : 18.92

Bid-YTW : 4.28 % |

| MFC.PR.N |

FixedReset |

5.15 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 19.82

Bid-YTW : 6.51 % |

| MFC.PR.I |

FixedReset |

5.23 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.13

Bid-YTW : 5.41 % |

| FTS.PR.G |

FixedReset |

5.58 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 17.42

Evaluated at bid price : 17.42

Bid-YTW : 4.37 % |

| MFC.PR.M |

FixedReset |

5.60 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 19.80

Bid-YTW : 6.59 % |

| SLF.PR.I |

FixedReset |

5.71 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.35

Bid-YTW : 6.28 % |

| TD.PR.Y |

FixedReset |

5.82 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 24.37

Bid-YTW : 3.54 % |

| BAM.PF.A |

FixedReset |

6.04 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 19.67

Evaluated at bid price : 19.67

Bid-YTW : 4.82 % |

| BAM.PF.G |

FixedReset |

6.23 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 20.45

Evaluated at bid price : 20.45

Bid-YTW : 4.67 % |

| BAM.PF.F |

FixedReset |

6.63 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 20.26

Evaluated at bid price : 20.26

Bid-YTW : 4.69 % |

| SLF.PR.H |

FixedReset |

6.99 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 17.60

Bid-YTW : 7.56 % |

| BAM.PR.X |

FixedReset |

7.63 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 14.38

Evaluated at bid price : 14.38

Bid-YTW : 4.73 % |

| BAM.PF.E |

FixedReset |

7.65 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 18.71

Evaluated at bid price : 18.71

Bid-YTW : 4.76 % |

| PWF.PR.P |

FixedReset |

9.92 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-16

Maturity Price : 14.30

Evaluated at bid price : 14.30

Bid-YTW : 4.17 % |