Assiduous Reader IR brought to my attention recently a fascinating article titled Six Strange Things That Have Been Happening in Financial Markets:

Interesting things have certainly been happening in the underpinnings of global markets—things that either run counter to long-standing financial logic, or represent an unusual dislocation in the “normal” state of market affairs, or were once rare occurrences but have been happening with increasing frequency.

…

1. Negative swap spreads

…

2. Fractured repo rates

…

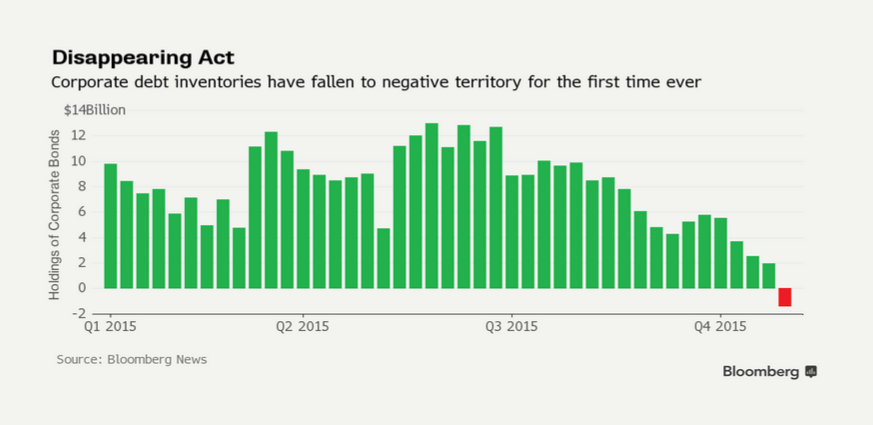

3. Corporate bond inventories below zero

Click for BigAnalysts at Goldman Sachs made waves this week when they highlighted the fact that inventories of some corporate bonds held by big dealer-banks had gone negative for the first time since the Federal Reserve began collecting such data. That means big banks are now net short corporate bonds with a maturity greater than 12 months equivalent to $1.4 billion, bucking the longer-term trend of net positive positions.

The record-breaking event revived a flurry of concerns about so-called liquidity, or ease of trading, in the $8.1 trillion corporate bond market. Similar to the repo market, a confluence of new rules is said to have made it more difficult for banks to hold corporate bonds on their balance sheets. At the same time, years of low interest rates have encouraged investors to herd into corporate bonds and hold onto them tightly.

…

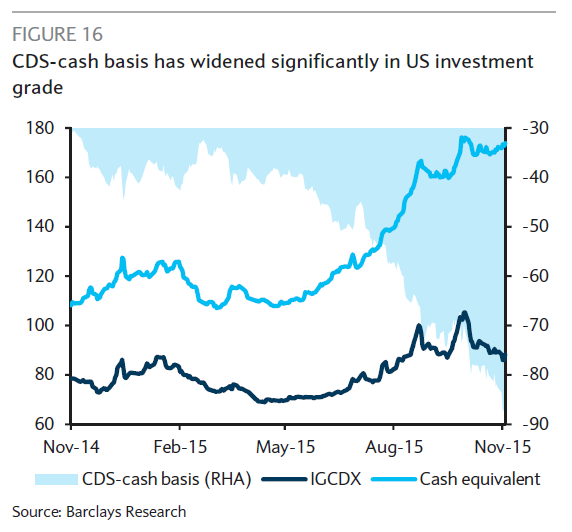

Synthetic credit is trading tighter than cash credit

Click for Big…

Above is the so-called basis between the CDX IG, an index that includes CDS tied to U.S. investment-grade companies, and the underlying cash bonds. The basis has been persistently wide and negative in recent years, as spreads on the CDX index trade at tighter levels than cash.“In exchange for the substantial liquidity of derivative indices, investors are often giving up spread right now, as most indices trade at a negative basis versus the comparable cash market,” Barclays’ Bradley Rogoff wrote in research published today. “The negative basis right now is near the largest we have witnessed at a time when there was not a funding crisis.”

Investors may be ogling such synthetic tools not just because of their purported liquidity benefits but also because of funding benefits, a similar dynamic to the one currently pushing swap spreads into negative territory.

…

Market moves that aren’t supposed to happen keep happening

…

The number of assets registering large moves—four or more standard deviations away from their normal trading range—has been increasing. Such moves would normally be expected to happen once every 62 years.While Martin blamed much of the confusion on unexpected decisions by central banks—such as the Swiss National Bank’s surprise decision to scrap its long-standing currency cap—there have been sharp market moves with seemingly little reasons behind them. Perhaps the best-known example is Oct. 15, 2014, when the yield on the 10-year U.S. Treasury briefly plunged 33 basis points—a seven standard-deviation move that should happen once every 1.6 billion years, based on a normal distribution of probabilities.

…

Volatility is itself more volatile

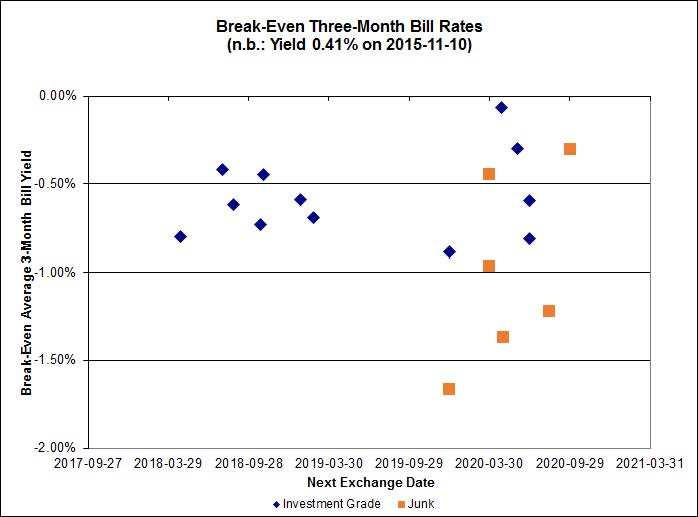

Negative swap spreads were discussed on November 5.

The CDS Basis was discussed in the post BIS Releases March 2009 Quarterly Review, where the wide spread was considered to suggest “that arbitrage activities that would usually tend to compress the price differential continued to be constrained by elevated capital and financing costs for leveraged investors.” I consider this to have the potential for severely adverse effects on the economy due to “debt decoupling”, discussed in the post Credit Default Swaps: Links to Primers, notably a paper by Hu and Black titled Debt, Equity, and Hybrid Decoupling: Governance and Systemic Risk Implications:

There are also several sources of qualitative evidence. One is the recent tendency for credit default swap contracts to require the protection buyer, if it is also a creditor, to act in the interests of other creditors. This suggests concern that the protection buyer might not otherwise do so. How this obligation can be enforced, however, without disclosure of either votes or hedges, is anyone’s guess. We have also heard from bankruptcy judges that they sometimes see odd behavior in their courtrooms, which empty crediting might explain. For example, one judge described a case in which a junior creditor complained that the firm’s value was too high, even though a lower value would hurt the class of debt the creditor ostensibly held.

Also hinted at yesterday was the latest twist in the Silver Bullion Trust / Sprott battle:

Sprott has amended the Offer by attempting to unilaterally expand the scope of the powers of attorney granted to it by those Unitholders that tender to the Offer. The amendments purport to give Sprott the authority to replace the independent Trustees of SBT, insert their own conflicted Trustees and force completion of their inadequate Offer, despite their continued failure to attract sufficient Unitholder support for doing so by legitimate means.

SBT believes that Sprott’s attempt to unilaterally amend the powers of attorney is invalid and that any actions that Sprott would purport to take pursuant to them would be invalid. SBT also believes that Sprott’s actions are contrary to the take-over bid and proxy solicitation rules and the public interest. SBT has commenced an application before the Ontario Securities Commission to contest the amendments and other aspects of the Offer and has sought an order from the Ontario Securities Commission cease trading the Offer.

SBT is of the view that the use of the powers of attorney by Sprott to replace its independent Trustees when the conditions to the Offer have not been met is not a purpose for which the powers of attorney were solicited, and a clear violation of law. Sprott’s plan to change the terms of the powers of attorney granted by certain SBT Unitholders – without consulting Unitholders or complying with securities laws – is nothing more than an illegitimate tactic to ignore the will of Unitholders and replace SBT’s independent Trustees with insiders of Sprott, all of whom are clearly and obviously conflicted. Further, Sprott had previously represented to Unitholders and the Ontario Superior Court of Justice that it would use the powers of attorney granted in connection with the Offer for the purpose of carrying out the mechanics required to complete the Offer, only if they achieved the minimum acceptance of 66⅔% of SBT Units.

This is great entertainment – but I’m glad I’m not the one paying the lawyers!

It was a poor day for the Canadian preferred share market, with PerpetualDiscounts off 2bp, FixedResets losing 56bp and DeemedRetractibles down 5bp. BAM issues were notable in the bad part of the Performance Highlights table. Volume was average. What a week it has been – but at least we’re not alone.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

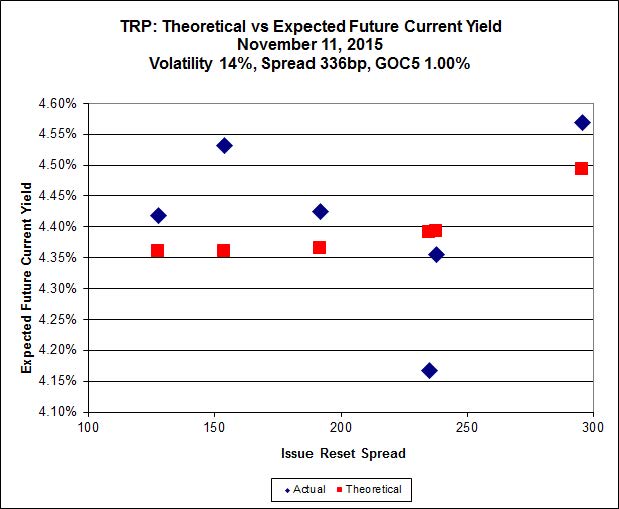

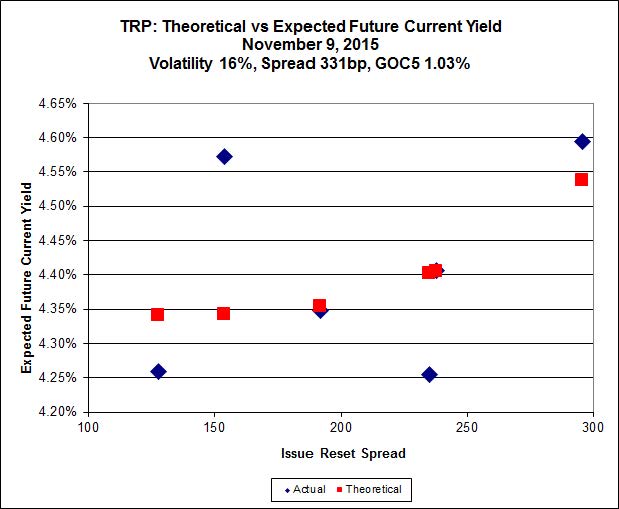

Here’s TRP:

Click for Big

There is a major increase in implied volatility today. It’s almost as if the issues with the lowest spreads have a ‘floor price’ – which is not to say that they don’t go down, but they seem to outperform on lousy days.

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 18.94 to be $0.68 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $0.24 cheap at its bid price of 13.90.

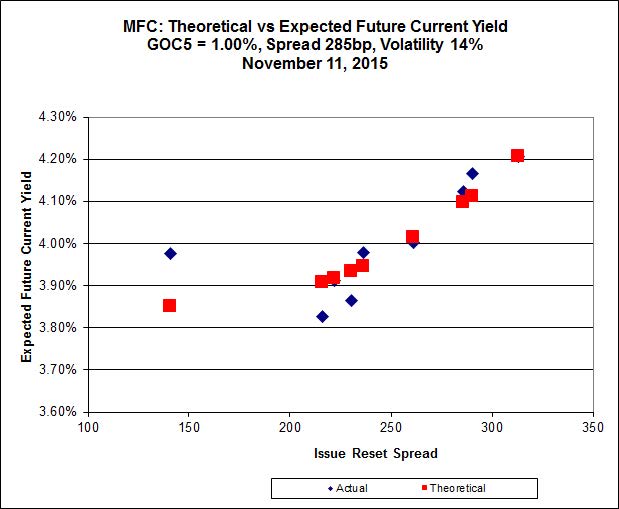

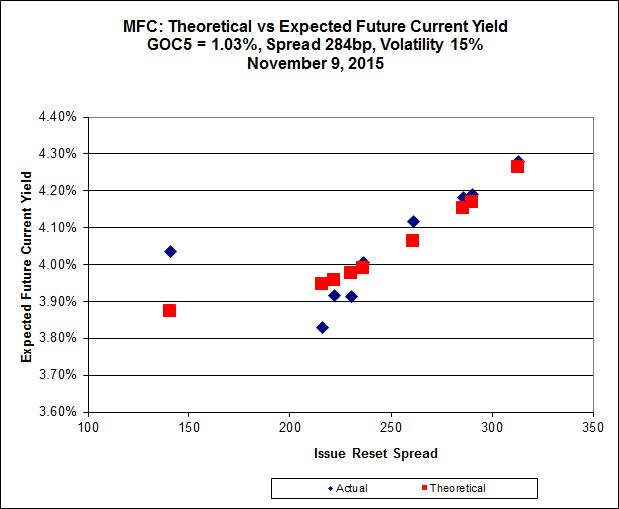

Click for Big

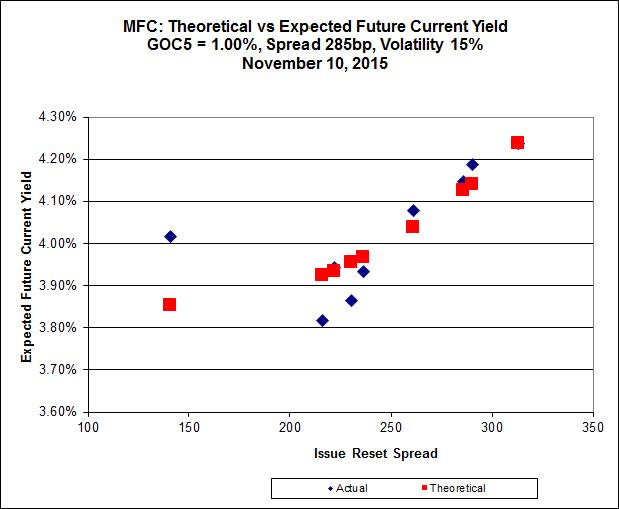

Most expensive is MFC.PR.N, resetting at +230bp on 2020-3-19, bid at 20.98 to be 0.55 rich, while MFC.PR.F resetting at +141bp on 2016-6-19, is bid at 14.45 to be 0.69 cheap.

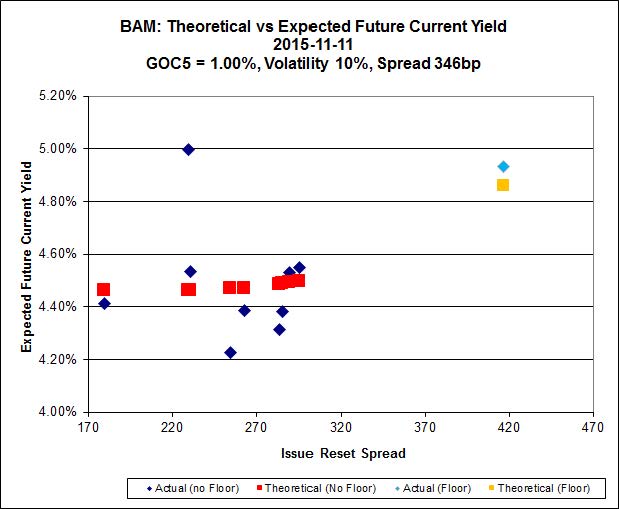

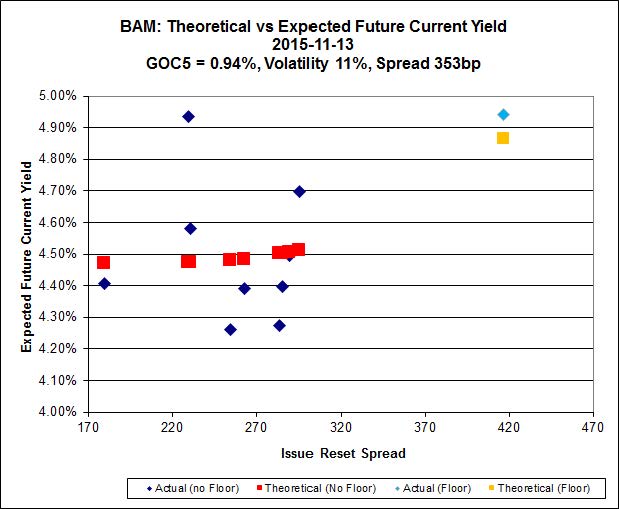

Click for Big

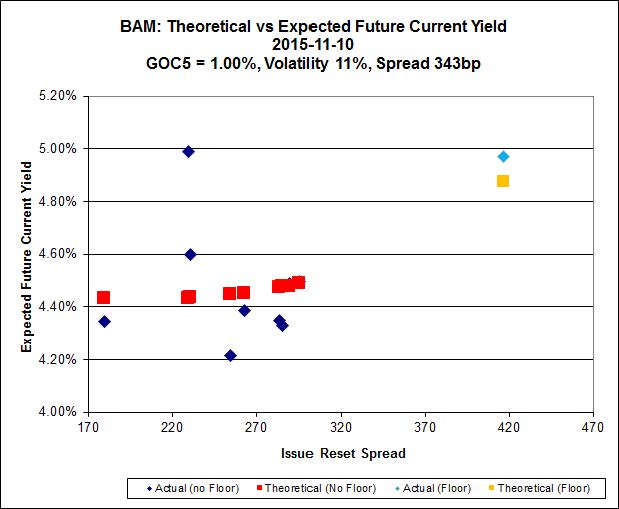

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 16.41 to be $1.70 cheap. BAM.PF.G, resetting at +284bp on 2020-6-30 is bid at 22.11 and appears to be $1.12 rich.

Click for Big

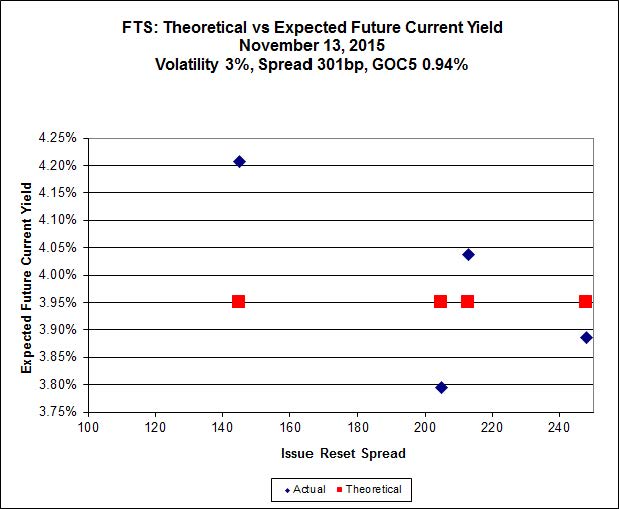

FTS.PR.K, with a spread of +205bp, and bid at 19.70, looks $0.78 expensive and resets 2019-3-1. FTS.PR.H, with a spread of +145bp and resetting 2020-6-1, is bid at 14.20 and is $0.93 cheap.

Click for Big

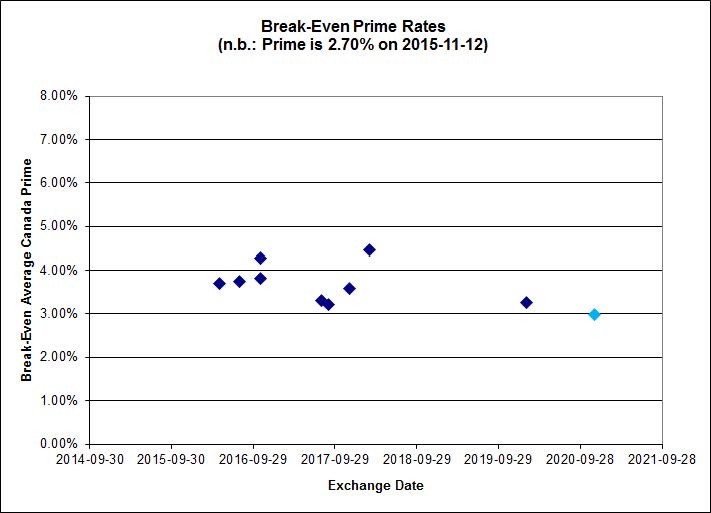

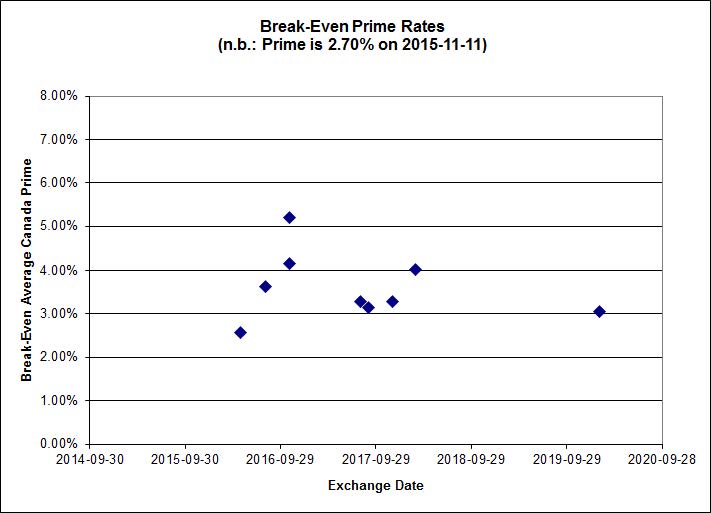

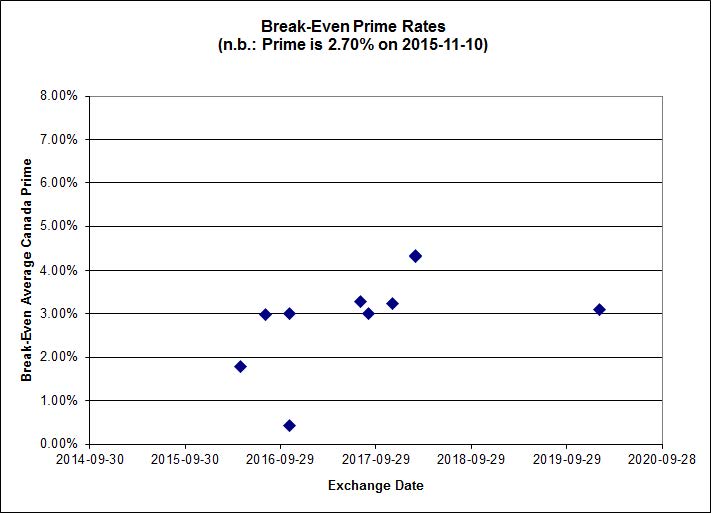

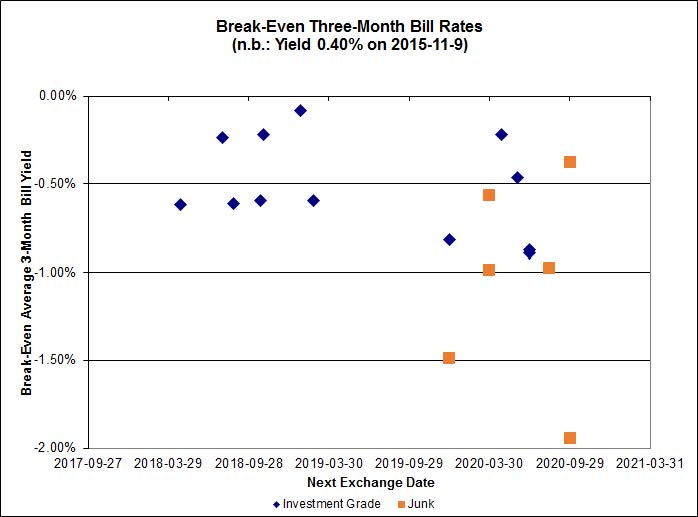

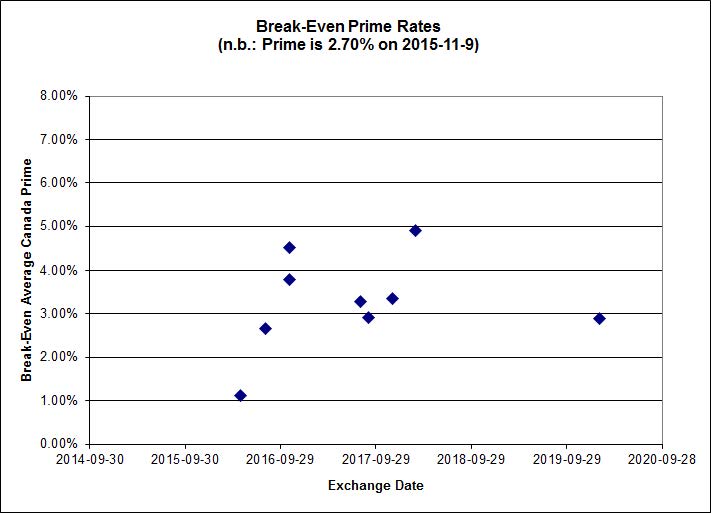

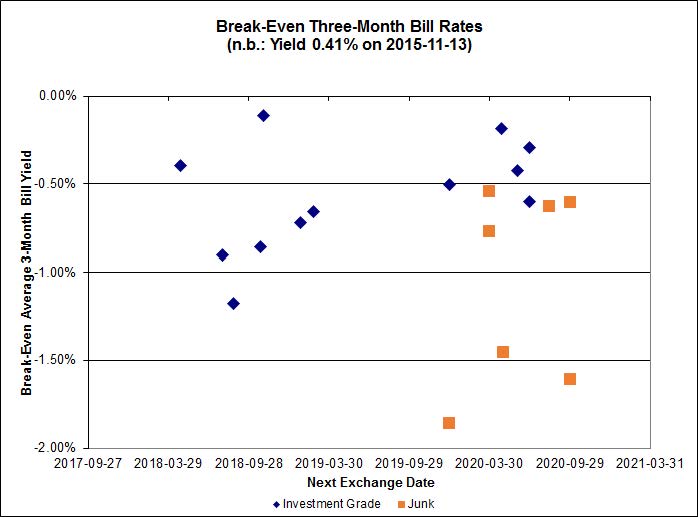

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.57%, with one outlier above 0.00%. There are two junk outliers above 0.00% and one below -2.00%.

Click for Big

The light blue point is an estimate for the potential BCE.PR.R / BCE.PF.Q pair, the latter of which is not trading. Its price has been set to the average defined by the other BCE Ratchet Rate preferreds.

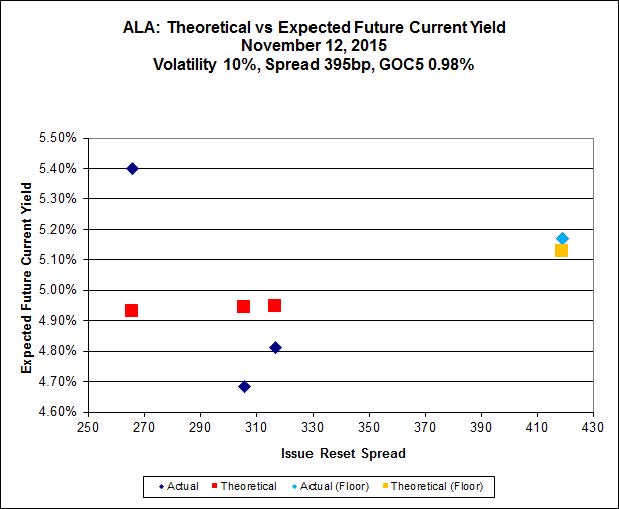

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 4.27 % | 5.12 % | 31,167 | 17.69 | 1 | 0.0000 % | 1,819.2 |

| FixedFloater | 6.27 % | 5.51 % | 28,644 | 16.91 | 1 | -3.5646 % | 3,112.2 |

| Floater | 3.87 % | 3.89 % | 69,597 | 17.62 | 3 | 0.1915 % | 2,040.6 |

| OpRet | 4.84 % | 4.54 % | 33,557 | 0.77 | 1 | 0.0000 % | 2,718.6 |

| SplitShare | 4.74 % | 5.71 % | 140,624 | 4.37 | 5 | -0.2039 % | 3,206.4 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.2039 % | 2,501.7 |

| Perpetual-Premium | 5.82 % | 4.37 % | 72,269 | 0.08 | 6 | -0.0199 % | 2,497.9 |

| Perpetual-Discount | 5.53 % | 5.61 % | 84,446 | 14.46 | 33 | -0.0158 % | 2,585.9 |

| FixedReset | 4.83 % | 4.40 % | 223,365 | 15.46 | 76 | -0.5566 % | 2,115.1 |

| Deemed-Retractible | 5.18 % | 5.19 % | 110,584 | 5.41 | 34 | -0.0530 % | 2,581.0 |

| FloatingReset | 2.59 % | 3.86 % | 53,963 | 5.78 | 10 | -0.3009 % | 2,181.0 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BAM.PR.T | FixedReset | -4.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-13 Maturity Price : 17.74 Evaluated at bid price : 17.74 Bid-YTW : 4.81 % |

| BAM.PR.X | FixedReset | -3.96 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-13 Maturity Price : 15.54 Evaluated at bid price : 15.54 Bid-YTW : 4.75 % |

| BAM.PR.G | FixedFloater | -3.56 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-13 Maturity Price : 25.00 Evaluated at bid price : 15.15 Bid-YTW : 5.51 % |

| ELF.PR.G | Perpetual-Discount | -3.52 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-13 Maturity Price : 20.57 Evaluated at bid price : 20.57 Bid-YTW : 5.84 % |

| BAM.PR.Z | FixedReset | -2.81 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-13 Maturity Price : 20.76 Evaluated at bid price : 20.76 Bid-YTW : 4.91 % |

| BIP.PR.A | FixedReset | -2.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-13 Maturity Price : 21.50 Evaluated at bid price : 21.50 Bid-YTW : 5.31 % |

| TRP.PR.E | FixedReset | -2.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-13 Maturity Price : 18.94 Evaluated at bid price : 18.94 Bid-YTW : 4.65 % |

| MFC.PR.K | FixedReset | -2.20 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.59 Bid-YTW : 6.68 % |

| TRP.PR.D | FixedReset | -2.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-13 Maturity Price : 18.30 Evaluated at bid price : 18.30 Bid-YTW : 4.75 % |

| SLF.PR.J | FloatingReset | -2.04 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.45 Bid-YTW : 9.50 % |

| HSE.PR.E | FixedReset | -2.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-13 Maturity Price : 21.97 Evaluated at bid price : 22.45 Bid-YTW : 5.06 % |

| RY.PR.Z | FixedReset | -1.93 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-13 Maturity Price : 19.85 Evaluated at bid price : 19.85 Bid-YTW : 4.17 % |

| FTS.PR.K | FixedReset | -1.75 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-13 Maturity Price : 19.70 Evaluated at bid price : 19.70 Bid-YTW : 4.09 % |

| MFC.PR.F | FixedReset | -1.70 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.45 Bid-YTW : 9.60 % |

| CU.PR.C | FixedReset | -1.60 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-13 Maturity Price : 20.91 Evaluated at bid price : 20.91 Bid-YTW : 4.06 % |

| RY.PR.H | FixedReset | -1.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-13 Maturity Price : 19.87 Evaluated at bid price : 19.87 Bid-YTW : 4.21 % |

| MFC.PR.H | FixedReset | -1.28 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.89 Bid-YTW : 4.87 % |

| BNS.PR.D | FloatingReset | -1.22 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.50 Bid-YTW : 5.62 % |

| MFC.PR.I | FixedReset | -1.20 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.12 Bid-YTW : 5.08 % |

| CM.PR.Q | FixedReset | -1.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-13 Maturity Price : 22.18 Evaluated at bid price : 22.80 Bid-YTW : 4.04 % |

| MFC.PR.G | FixedReset | -1.17 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.82 Bid-YTW : 5.23 % |

| BAM.PF.B | FixedReset | -1.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-13 Maturity Price : 20.32 Evaluated at bid price : 20.32 Bid-YTW : 4.61 % |

| NA.PR.W | FixedReset | -1.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-13 Maturity Price : 19.45 Evaluated at bid price : 19.45 Bid-YTW : 4.32 % |

| FTS.PR.H | FixedReset | -1.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-13 Maturity Price : 14.20 Evaluated at bid price : 14.20 Bid-YTW : 4.33 % |

| BAM.PF.F | FixedReset | -1.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-13 Maturity Price : 21.32 Evaluated at bid price : 21.61 Bid-YTW : 4.61 % |

| RY.PR.M | FixedReset | -1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-13 Maturity Price : 21.52 Evaluated at bid price : 21.52 Bid-YTW : 4.16 % |

| TD.PF.C | FixedReset | -1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-13 Maturity Price : 19.65 Evaluated at bid price : 19.65 Bid-YTW : 4.24 % |

| RY.PR.N | Perpetual-Discount | -1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-13 Maturity Price : 23.00 Evaluated at bid price : 23.40 Bid-YTW : 5.23 % |

| TD.PF.A | FixedReset | -1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-13 Maturity Price : 19.87 Evaluated at bid price : 19.87 Bid-YTW : 4.22 % |

| SLF.PR.H | FixedReset | 1.82 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.99 Bid-YTW : 6.84 % |

| FTS.PR.J | Perpetual-Discount | 4.99 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-13 Maturity Price : 21.75 Evaluated at bid price : 22.08 Bid-YTW : 5.47 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| RY.PR.B | Deemed-Retractible | 127,633 | Nesbitt crossed 64,800 at 24.95. Desjardins crossed 50,000 at the same price. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.92 Bid-YTW : 4.76 % |

| MFC.PR.I | FixedReset | 104,994 | Desjardins crossed blocks of 43,300 and 25,000, both at 23.47. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.12 Bid-YTW : 5.08 % |

| NA.PR.S | FixedReset | 55,987 | TD crossed 25,000 at 20.00. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-13 Maturity Price : 20.05 Evaluated at bid price : 20.05 Bid-YTW : 4.36 % |

| BMO.PR.S | FixedReset | 48,972 | Scotia crossed 30,000 at 20.25. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-13 Maturity Price : 20.05 Evaluated at bid price : 20.05 Bid-YTW : 4.26 % |

| RY.PR.Z | FixedReset | 47,041 | Scotia crossed 28,600 at 20.23. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-13 Maturity Price : 19.85 Evaluated at bid price : 19.85 Bid-YTW : 4.17 % |

| BAM.PF.H | FixedReset | 30,706 | YTW SCENARIO Maturity Type : Call Maturity Date : 2020-12-31 Maturity Price : 25.00 Evaluated at bid price : 25.85 Bid-YTW : 4.40 % |

| There were 34 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| ELF.PR.G | Perpetual-Discount | Quote: 20.57 – 21.47 Spot Rate : 0.9000 Average : 0.5444 YTW SCENARIO |

| MFC.PR.K | FixedReset | Quote: 19.59 – 20.13 Spot Rate : 0.5400 Average : 0.3679 YTW SCENARIO |

| BAM.PR.T | FixedReset | Quote: 17.74 – 18.30 Spot Rate : 0.5600 Average : 0.3910 YTW SCENARIO |

| GWO.PR.S | Deemed-Retractible | Quote: 24.21 – 24.75 Spot Rate : 0.5400 Average : 0.3960 YTW SCENARIO |

| TRP.PR.F | FloatingReset | Quote: 14.52 – 15.00 Spot Rate : 0.4800 Average : 0.3492 YTW SCENARIO |

| RY.PR.M | FixedReset | Quote: 21.52 – 21.90 Spot Rate : 0.3800 Average : 0.2650 YTW SCENARIO |