So the Canadian jobs number wasn’t as bad as expected, because we’re all working for the government:

Canadian employment fell by 6,400 in June on the biggest decline in part-time work in more than four years, sustaining the view the economy is losing steam and may require another jolt of stimulus from the central bank.

The unemployment rate remained at 6.8 percent for a fifth month, Statistics Canada said Friday in Ottawa. Part-time work fell 71,200, exceeding the 64,800 gain in full-time work. Quebec posted a decline of 33,300, the most since May 2005.

…

Private companies cut 26,300 workers, tempering gains in public-sector employment, which rose by 42,200.

Meanwhile, Yellen continues to expect a Fed hike:

Federal Reserve Chair Janet Yellen, speaking after weeks of financial-market turmoil over China and Greece, maintained her call for an interest-rate increase this year as the U.S. economy improves.

“I expect that it will be appropriate at some point later this year to take the first step to raise the federal funds rate and thus begin normalizing monetary policy,” Yellen said in her first public remarks since the June meeting of the Federal Open Market Committee.

Yellen added a note of caution, saying that “the course of the economy and inflation remains highly uncertain, and unanticipated developments could delay or accelerate this first step.” In her only mention of Greece in a 14-page speech delivered Friday in Cleveland, she identified that nation’s debt crisis as one cause of uncertainty.

And worrying about Greece is, like, getting old, you know?

Stock investors got jolted in a zigzag week, with plunges around the world giving way to the biggest rallies in at least three years for China and Europe.

Spurred by optimism on Greece, the Stoxx Europe 600 Index climbed 4.3 percent on Thursday and Friday, erasing earlier losses with the biggest two-day advance since 2011. The Shanghai Stock Exchange Composite Index jumped 11 percent in two sessions, the most in almost seven years, while the Standard & Poor’s 500 Index added 1.2 percent Friday to wipe out a weekly decline.

It was a mixed day for the Canadian preferred share market, with PerpetualDiscounts off 19bp, FixedResets gaining 45bp and DeemedRetractibles down 21bp. Floaters bounced back from yesterday‘s downdraft. The Performance Highlights table is again very lengthy, but skewed towards positive returns this time. Volume was extremely high.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

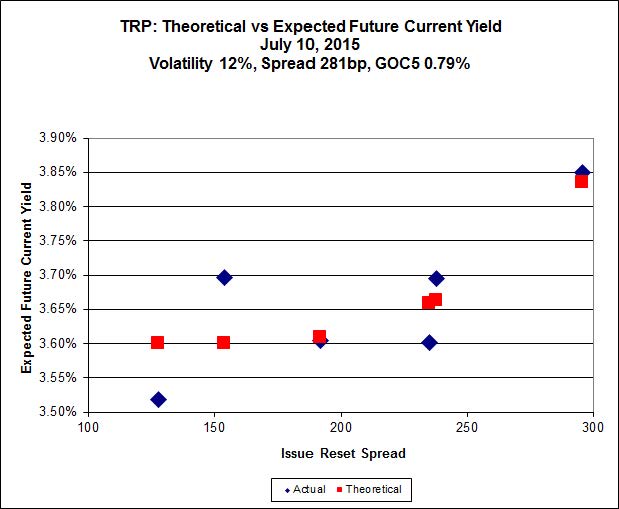

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 21.80 to be $0.35 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $0.42 cheap at its bid price of 15.76.

Click for Big

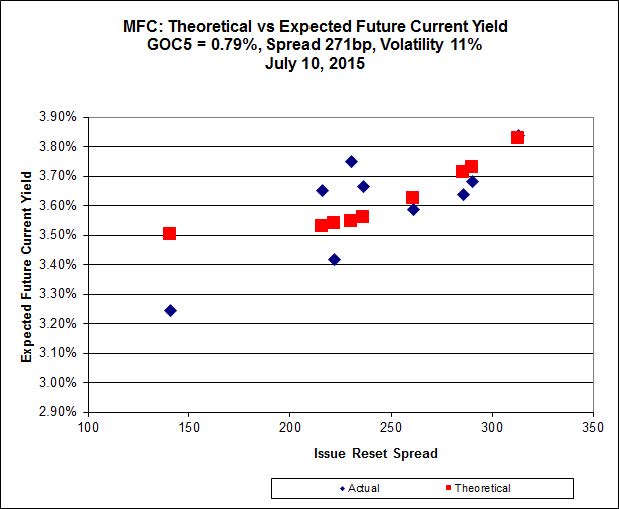

The fit is horrible today, and Implied Volatility has dropped precipitously.

Most expensive is MFC.PR.F, resetting at +141bp on 2016-6-19, bid at 16.96 to be $1.25 rich, while MFC.PR.N, resetting at +230bp on 2020-3-19, and which has a very low bid that does not seem reflective of market conditions (see the Performance Highlights Table) is bid at 20.61 to be $1.17 cheap.

Click for Big

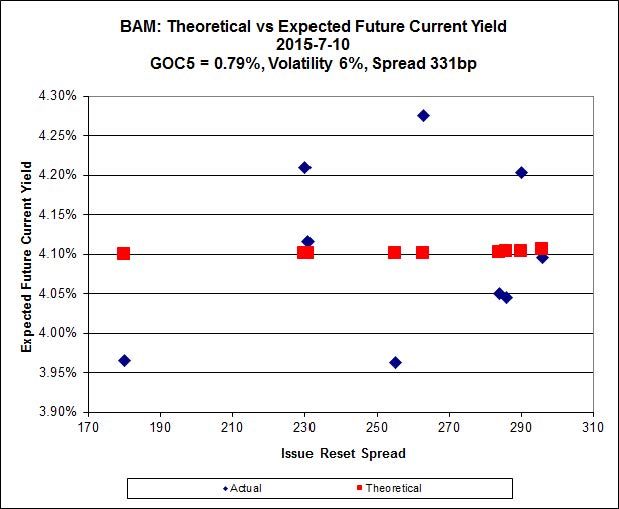

The cheapest issue relative to its peers is BAM.PF.B, resetting at +263bp on 2019-3-31, bid at 20.00 to be $0.85 cheap. BAM.PF.E, resetting at +255bp on 2020-3-31 is bid at 21.07 and appears to be $0.70 rich.

Click for Big

FTS.PR.K, with a spread of +205bp, and bid at 21.50, looks $0.35 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 21.31 and is $0.33 cheap.

The calculated level of implied volatility declined today, but is still higher than I would expect; reversion to a lower level will imply underperformance of the lower-spread issues.

Click for Big

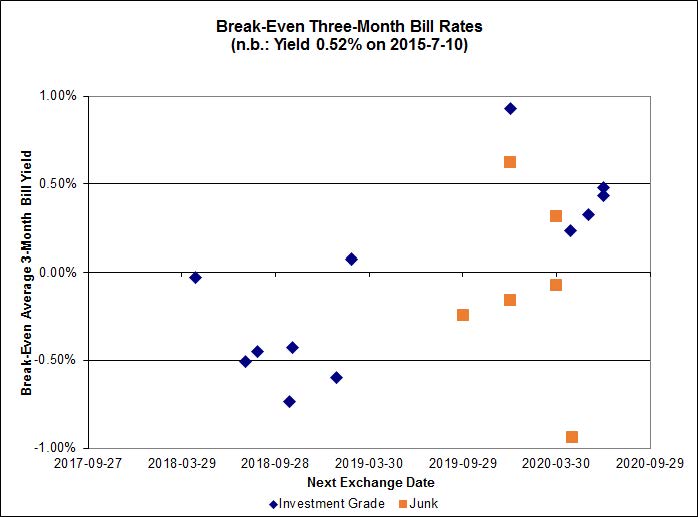

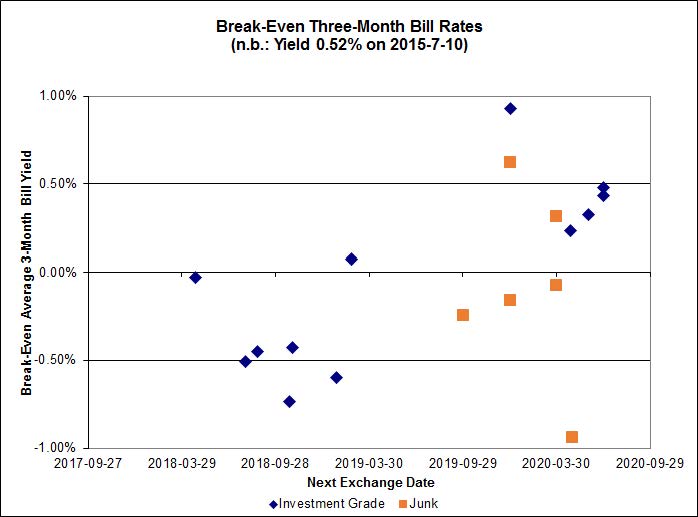

The change of scale on the chart means there are no outliers today!

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.02% (which seems a little extreme!).

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 8.4697 % | 2,127.8 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 8.4697 % | 3,720.4 |

| Floater | 3.64 % | 3.69 % | 61,973 | 18.12 | 3 | 8.4697 % | 2,262.0 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.2422 % | 2,754.0 |

| SplitShare | 4.62 % | 4.98 % | 69,071 | 3.21 | 3 | -0.2422 % | 3,227.5 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.2422 % | 2,518.2 |

| Perpetual-Premium | 5.52 % | 3.76 % | 65,814 | 0.47 | 13 | -0.0396 % | 2,512.4 |

| Perpetual-Discount | 5.43 % | 5.38 % | 93,279 | 14.77 | 21 | -0.1940 % | 2,637.8 |

| FixedReset | 4.68 % | 3.81 % | 223,542 | 15.93 | 88 | 0.4534 % | 2,248.5 |

| Deemed-Retractible | 5.03 % | 3.76 % | 111,462 | 0.61 | 34 | -0.2139 % | 2,617.4 |

| FloatingReset | 2.52 % | 3.18 % | 54,283 | 6.07 | 10 | 0.1226 % | 2,281.0 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| MFC.PR.N | FixedReset | -5.24 % | This looks like an effect of a very thin market and shoddy market-making. There are seventeen trades timestamped 3:59, sixteen of which are for 100 shares and one of which was for 30 shares. The selling brokers were Scotia and Anonymous; the selling might have come from either a retail stockbroker who’s not very good at his job or a price-insensitive algorithm. These trades were done in a range of 20.98-21.80; 20.98 was the low for the day. The day’s VWAP, on volume of 14,458 shares, was 21.769583. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.61 Bid-YTW : 5.97 % |

| MFC.PR.L | FixedReset | -3.85 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.21 Bid-YTW : 6.13 % |

| ELF.PR.G | Perpetual-Discount | -2.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-10 Maturity Price : 21.50 Evaluated at bid price : 21.50 Bid-YTW : 5.55 % |

| MFC.PR.C | Deemed-Retractible | -2.48 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.00 Bid-YTW : 6.26 % |

| ENB.PR.J | FixedReset | -2.36 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-10 Maturity Price : 17.82 Evaluated at bid price : 17.82 Bid-YTW : 5.10 % |

| HSE.PR.C | FixedReset | -2.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-10 Maturity Price : 21.74 Evaluated at bid price : 22.11 Bid-YTW : 4.61 % |

| POW.PR.D | Perpetual-Discount | -1.98 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-10 Maturity Price : 23.04 Evaluated at bid price : 23.31 Bid-YTW : 5.38 % |

| SLF.PR.C | Deemed-Retractible | -1.61 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.94 Bid-YTW : 6.22 % |

| HSE.PR.G | FixedReset | -1.57 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-10 Maturity Price : 22.67 Evaluated at bid price : 23.77 Bid-YTW : 4.59 % |

| SLF.PR.B | Deemed-Retractible | -1.44 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.19 Bid-YTW : 5.85 % |

| ENB.PR.D | FixedReset | -1.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-10 Maturity Price : 16.31 Evaluated at bid price : 16.31 Bid-YTW : 5.12 % |

| ENB.PR.B | FixedReset | -1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-10 Maturity Price : 16.18 Evaluated at bid price : 16.18 Bid-YTW : 5.15 % |

| ENB.PR.F | FixedReset | -1.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-10 Maturity Price : 16.55 Evaluated at bid price : 16.55 Bid-YTW : 5.25 % |

| BAM.PF.F | FixedReset | -1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-10 Maturity Price : 22.06 Evaluated at bid price : 22.56 Bid-YTW : 4.25 % |

| BNS.PR.D | FloatingReset | -1.04 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.83 Bid-YTW : 3.65 % |

| PWF.PR.E | Perpetual-Premium | -1.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-10 Maturity Price : 24.46 Evaluated at bid price : 24.70 Bid-YTW : 5.57 % |

| NA.PR.S | FixedReset | 1.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-10 Maturity Price : 21.84 Evaluated at bid price : 22.20 Bid-YTW : 3.76 % |

| TRP.PR.B | FixedReset | 1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-10 Maturity Price : 14.71 Evaluated at bid price : 14.71 Bid-YTW : 3.58 % |

| TD.PF.B | FixedReset | 1.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-10 Maturity Price : 21.43 Evaluated at bid price : 21.43 Bid-YTW : 3.75 % |

| FTS.PR.H | FixedReset | 1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-10 Maturity Price : 17.00 Evaluated at bid price : 17.00 Bid-YTW : 3.43 % |

| ENB.PF.C | FixedReset | 1.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-10 Maturity Price : 18.40 Evaluated at bid price : 18.40 Bid-YTW : 5.08 % |

| ENB.PR.P | FixedReset | 1.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-10 Maturity Price : 17.15 Evaluated at bid price : 17.15 Bid-YTW : 5.09 % |

| MFC.PR.G | FixedReset | 1.21 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.05 Bid-YTW : 3.83 % |

| HSE.PR.A | FixedReset | 1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-10 Maturity Price : 15.74 Evaluated at bid price : 15.74 Bid-YTW : 4.18 % |

| FTS.PR.K | FixedReset | 1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-10 Maturity Price : 21.50 Evaluated at bid price : 21.50 Bid-YTW : 3.59 % |

| MFC.PR.J | FixedReset | 1.28 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.70 Bid-YTW : 4.31 % |

| TRP.PR.E | FixedReset | 1.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-10 Maturity Price : 21.52 Evaluated at bid price : 21.80 Bid-YTW : 3.86 % |

| TRP.PR.C | FixedReset | 1.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-10 Maturity Price : 15.76 Evaluated at bid price : 15.76 Bid-YTW : 3.77 % |

| BMO.PR.S | FixedReset | 1.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-10 Maturity Price : 21.85 Evaluated at bid price : 22.22 Bid-YTW : 3.72 % |

| ENB.PR.Y | FixedReset | 1.51 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-10 Maturity Price : 16.85 Evaluated at bid price : 16.85 Bid-YTW : 5.07 % |

| IAG.PR.G | FixedReset | 1.60 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.69 Bid-YTW : 3.98 % |

| BAM.PR.R | FixedReset | 1.66 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-10 Maturity Price : 18.35 Evaluated at bid price : 18.35 Bid-YTW : 4.39 % |

| SLF.PR.I | FixedReset | 1.66 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.43 Bid-YTW : 3.99 % |

| PWF.PR.T | FixedReset | 1.79 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-10 Maturity Price : 23.11 Evaluated at bid price : 24.50 Bid-YTW : 3.30 % |

| RY.PR.J | FixedReset | 1.86 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-10 Maturity Price : 23.03 Evaluated at bid price : 24.60 Bid-YTW : 3.53 % |

| TD.PF.E | FixedReset | 2.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-10 Maturity Price : 23.00 Evaluated at bid price : 24.60 Bid-YTW : 3.62 % |

| VNR.PR.A | FixedReset | 2.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-10 Maturity Price : 22.23 Evaluated at bid price : 22.55 Bid-YTW : 4.09 % |

| TRP.PR.F | FloatingReset | 2.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-10 Maturity Price : 18.41 Evaluated at bid price : 18.41 Bid-YTW : 3.33 % |

| CM.PR.Q | FixedReset | 2.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-10 Maturity Price : 23.07 Evaluated at bid price : 24.76 Bid-YTW : 3.50 % |

| BNS.PR.Z | FixedReset | 2.48 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.16 Bid-YTW : 3.58 % |

| RY.PR.Z | FixedReset | 2.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-10 Maturity Price : 21.86 Evaluated at bid price : 22.23 Bid-YTW : 3.61 % |

| TD.PF.A | FixedReset | 2.62 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-10 Maturity Price : 21.28 Evaluated at bid price : 21.55 Bid-YTW : 3.72 % |

| RY.PR.H | FixedReset | 2.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-10 Maturity Price : 21.56 Evaluated at bid price : 21.84 Bid-YTW : 3.72 % |

| PWF.PR.P | FixedReset | 2.98 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-10 Maturity Price : 17.64 Evaluated at bid price : 17.64 Bid-YTW : 3.45 % |

| FTS.PR.M | FixedReset | 4.87 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-10 Maturity Price : 22.58 Evaluated at bid price : 23.49 Bid-YTW : 3.65 % |

| MFC.PR.K | FixedReset | 7.41 % | Down 4.65% yesterday. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.02 Bid-YTW : 4.93 % |

| BAM.PR.K | Floater | 7.61 % | Down 6.59% yesterday. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-10 Maturity Price : 13.57 Evaluated at bid price : 13.57 Bid-YTW : 3.70 % |

| BAM.PR.C | Floater | 8.80 % | Down 7.06% yesterday. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-10 Maturity Price : 13.60 Evaluated at bid price : 13.60 Bid-YTW : 3.69 % |

| BAM.PR.B | Floater | 8.99 % | Down 7.25% yesterday. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-10 Maturity Price : 13.94 Evaluated at bid price : 13.94 Bid-YTW : 3.60 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BNS.PR.B | FloatingReset | 76,565 | Scotia crossed 15,300 at 23.20; TD crossed 50,000 at the same price. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.22 Bid-YTW : 3.35 % |

| TRP.PR.B | FixedReset | 74,510 | Nesbitt crossed 48,600 at 14.70. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-10 Maturity Price : 14.71 Evaluated at bid price : 14.71 Bid-YTW : 3.58 % |

| BNS.PR.Z | FixedReset | 73,624 | Nesbitt crossed 49,900 at 22.65. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.16 Bid-YTW : 3.58 % |

| TD.PR.Y | FixedReset | 63,240 | Nesbitt crossed 10,000 at 25.15; RBC crossed 50,000 at 25.16. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.04 Bid-YTW : 2.99 % |

| SLF.PR.I | FixedReset | 59,366 | TD crossed 50,000 at 24.45. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.43 Bid-YTW : 3.99 % |

| MFC.PR.L | FixedReset | 57,388 | RBC crossed 50,000 at 21.24. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.21 Bid-YTW : 6.13 % |

| There were 60 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| MFC.PR.M | FixedReset | Quote: 21.50 – 23.00 Spot Rate : 1.5000 Average : 0.8798 YTW SCENARIO |

| MFC.PR.L | FixedReset | Quote: 20.21 – 21.70 Spot Rate : 1.4900 Average : 0.8853 YTW SCENARIO |

| MFC.PR.N | FixedReset | Quote: 20.61 – 21.85 Spot Rate : 1.2400 Average : 0.7370 YTW SCENARIO |

| IFC.PR.C | FixedReset | Quote: 21.90 – 22.80 Spot Rate : 0.9000 Average : 0.5474 YTW SCENARIO |

| ENB.PR.T | FixedReset | Quote: 17.17 – 17.99 Spot Rate : 0.8200 Average : 0.5026 YTW SCENARIO |

| HSE.PR.C | FixedReset | Quote: 22.11 – 22.84 Spot Rate : 0.7300 Average : 0.4434 YTW SCENARIO |