Canada’s currency weakened past C$1.30 per U.S. dollar for the first time since 2009 amid speculation the nation’s central bank will cut interest rates again to fight the economic damage from lower oil prices.

The loonie, as the Canadian dollar is known for the image of the aquatic bird on the C$1 coin, fell to as weak as C$1.3008. It traded at C$1.2965 at 9:26 a.m. in Toronto, and is poised to decline for a fourth week.

…

Monetary easing in Canada contrasts with the U.S. Federal Reserve, which is contemplating its first interest-rate increase in almost a decade.“For the Canadian dollar, the policy-divergence theme got a strong boost with the Bank of Canada cutting rates, while leaving the door open to more,” Matt Derr, a foreign-exchange strategist at Credit Suisse Group AG in New York, said by e-mail. Declining crude prices may put further pressure on the currency, he said.

Canada’s dollar has fallen 3.3 percent in the last three months, making it the second-worst performer among 10 developed-nation peers, according to data compiled by Bloomberg.

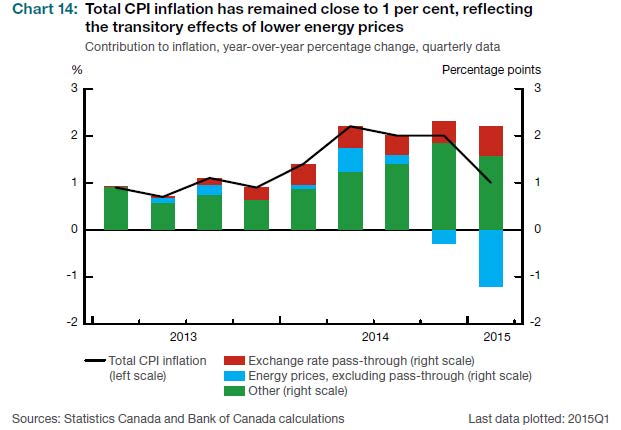

Canadian headline inflation is not an impediment to loose money:

Canada’s annual inflation rate quickened to 1 percent in June as food and shelter costs increased and energy provided less of a drag, providing no impetus for the central bank to change course on loose monetary policy.

Consumer prices accelerated from a 0.9 percent pace in May, Statistics Canada said Friday in Ottawa, as meat, dairy and bakery products and fresh fruit grew dearer.

Bank of Canada policy makers cut interest rates this week, saying a weak economy threatened to keep inflation from returning to its 2 percent target. The currency depreciated to the lowest since 2009 on speculation price gains aren’t enough to eliminate the chance of another central-bank rate cut.

…

The core rate, which excludes eight volatile products such as energy, accelerated to 2.3 percent, close to the March reading of 2.4 percent that was the fastest since 2008.Canada’s dollar dropped to C$1.3008 per U.S. dollar today. Two-year bond yields rose 1 basis point to 0.43 percent and 30-year securities fell to 2.25 percent from 2.27 percent.

The plunge in crude oil prices has driven down inflation and also triggered four straight monthly declines in output. At the same time, core prices have remained elevated on higher costs for meat and telecommunications products.

Economists surveyed by Bloomberg forecast Friday’s report would show overall inflation at 1 percent and the core rate remaining at 2.2 percent.

Energy costs fell 9 percent in June from 12 months earlier, less than May’s 11.8 percent rate of decline. Excluding energy the inflation rate slowed to 2.1 percent from 2.2 percent.

While the reported core inflation rate is above 2.0%, the July Monetary Policy Report states:

In contrast, core inflation as measured by CPIX has been slightly above 2 per cent, boosted by the pass-through effects of the past depreciation of the Canadian dollar and some sector-specific factors, which have offset the disinflationary force from slack in the economy (Chart 15). Although the impact of pass-through is difficult to gauge precisely, the Bank estimates that it is currently raising CPIX inflation by about 0.4 to 0.6 percentage points (Box 1).2 The underlying trend in inflation is assessed to be 1.5 to 1.7 per cent, a bit lower than in the April Report, consistent with material and increased slack in the Canadian economy.

Click for Big

In an interesting twist, Freddie Mac is selling structured notes:

Freddie Mac is expanding its risk-sharing efforts meant to protect taxpayers and potentially prepare the $9.4 trillion U.S. home-loan market for its future.

In a planned $300 million offering of mortgage-backed securities being managed by Credit Suisse Group AG, the government-backed company will sell $22.5 million of junior-ranking bonds without its guarantees, a person with knowledge of the deal said.

…

The bonds reflect directions that Freddie Mac and rival Fannie Mae have received from their overseer, the Federal Housing Finance Agency, to experiment with different ways of pushing their losses from homeowner defaults to bond buyers and insurers. The FHFA has also pushed them to increase the amount of the risk-sharing.

It will be interesting to see what the ultimate effect of all this is … how much will investors be willing to pay for the company guarantee when they’ve already got the first-loss protection afforded by the Junior Notes?

BCIMC has posted some good returns:

A tactical decision to shift investments into global stock markets paid off last year for British Columbia Investment Management Corp., which earned a 14.2-per-cent return for the year and boosted its total assets to $124-billion.

BCIMC reported it moved more assets into global equities during the fiscal year ended March 31, 2015, while reducing its weighting in fixed income holdings and mortgages, responding to volatility in Canadian stock markets as oil prices declined.

The fund ended the fiscal year with 49.5 per cent of its assets invested in public stock markets, up from 47.6 per cent a year earlier. BCIMC had 21.5 per cent of its holdings in fixed-income securities such as bonds, down slightly from 22 per cent last year, while 14.6 per cent of the portfolio is in real estate, a decline from 17.4 per cent at the end of fiscal 2014.

The fund said its Canadian public equity holdings earned a 7.5-per-cent return last year, while global public equities earned a far higher 23 per cent and emerging markets equities posted 21.4-per-cent gains, illustrating the value of shifting out of Canada’s volatile stock market.

…

BCIMC said investing in passive benchmarks last year would have earned a 12.6-per-cent return, so its active investment strategy added $1.4-billion in additional returns. Over the past 10 years, BCIMC earned an average 8.1-per-cent annualized return, exceeding its benchmark of 7.3 per cent.

But, we all ask, what are the cool kids doing now?:

Options on indexes made up of credit default swaps (CDS) have been a sleeper hit over the past few years.

While trading indexes comprising CDS tied to a basket of corporate names can give investors a cheap and easy way to trade corporate credit at a time when the cash market is said to be illiquid, options written on those same indexes can do one better. The options give investors the right to buy or sell CDS indexes, such as Markit’s CDX or iTraxx series.

…

In 2005, Citigroup estimated that about $2 billion worth of credit index options were trading per month, or roughly $24 billion over the course of the year. Last December, the same Citi analysts figured that about $1.4 trillion of the instruments had exchanged hands in all of 2014, compared with $573 billion worth in 2013. If correct, that would be more than a 5,000 percent jump in activity over the course of a decade.

…

The risk is that the popularity of options on CDS indexes, combined with a big move in one of the indexes, could spark a flurry of hedging activity by the big dealer-banks as they struggle to get their positions back to neutral. That in turn could end up amplifying the move in the underlying index.Here’s Barclays:

The relative growth of option volumes will likely make it increasingly more common to have option hedging (by dealers) exerting a meaningful influence on index dynamics—ie, we can expect to see the “option tail wagging the index dog” … This is particularly relevant because anecdotal evidence suggests that the majority of trades executed by investors are without delta as pure directional positions, and if anything, this proportion has been increasing over time. As such, in response to spread moves, the majority of delta-hedging will take place on the dealer side, with limited “natural” offset by investors delta-hedging in the opposite direction. Should the trend of rising relative option volumes continue, we are likely to see more cases of “pin risk” (delta-hedging of options bought by dealers making it more likely that spreads will stay around the strike) or “negative gamma” (delta-hedging of options sold by dealers, leading to amplifications of spread moves wider and tighter).

PDV.PR.A was confirmed at Pfd-3(high) by DBRS:

On July 18, 2014, DBRS upgraded the rating of the Preferred Shares to Pfd-3 (high) mainly based on a significant increase in downside protection to holders of the Preferred Shares. Over the last few months, the NAV of the Company has been declining as a result of high levels of uncertainty in the markets, resulting in a reduction in downside protection to 43% average compared with 45% a year ago. The dividend coverage ratio stands at approximately 0.7 times. Current performance metrics are still commensurate with the rating assigned, and as a result, the rating of the Preferred Shares has been confirmed at Pfd-3 (high).

After all the horror of the past six weeks-odd (not to mention the past six damn months!) the preferred share market has found a better place.

Click for Big

If this keeps up for the rest of the month, we might even break-even year-to-date!

It was a superb day for the Canadian preferred share market, with PerpetualDiscounts up 51bp, FixedResets winning an incredible 138bp and DeemedRetractibles gaining 45bp. The Performance Highlights table is … well, the Performance Highlights table is much as you’d expect, OK? Volume was very high.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

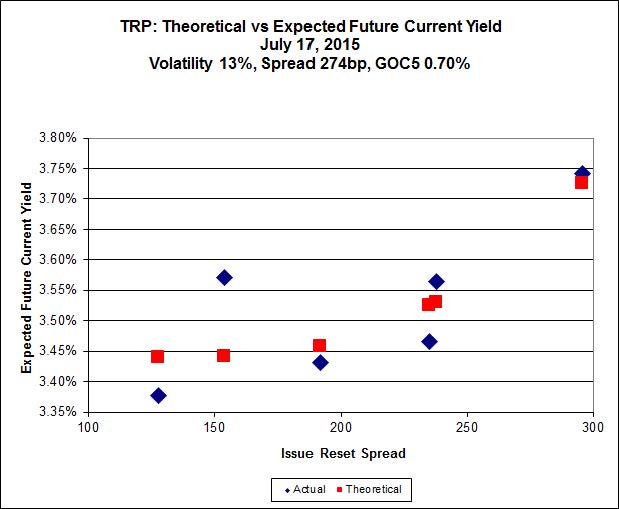

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +128, is bid at 22.00 to be $0.37 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $0.59 cheap at its bid price of 15.70.

Click for Big

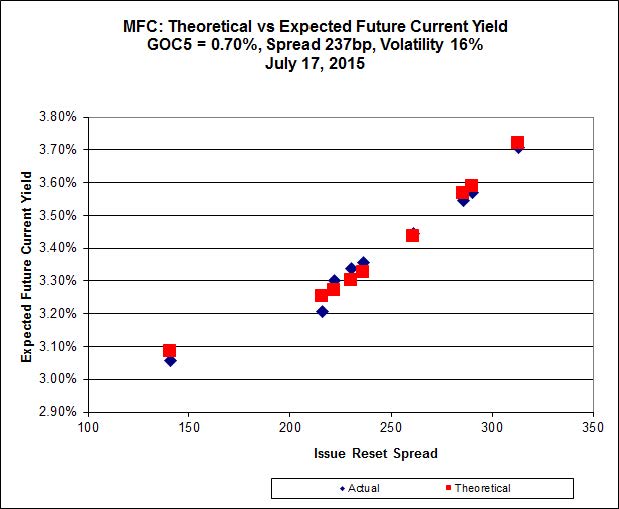

An extremely good fit today!

Most expensive is MFC.PR.L, resetting at +216bp on 2019-6-19, bid at 22.30 to be $0.31 rich, while MFC.PR.N, resetting at +230bp on 2020-3-19, is bid at 22.48 to be $0.24 cheap.

Click for Big

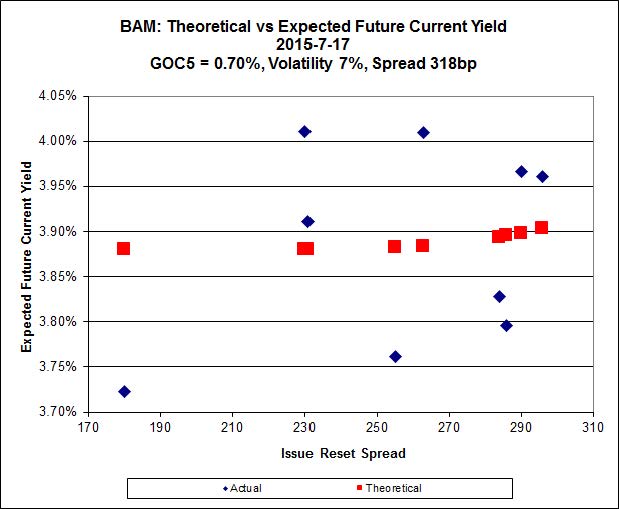

The cheapest issue relative to its peers is BAM.PF.B, resetting at +263bp on 2019-3-31, bid at 20.76 to be $0.68 cheap. BAM.PR.X, resetting at +180bp on 2017-6-30 is bid at 16.79 and appears to be $0.68 rich.

Click for Big

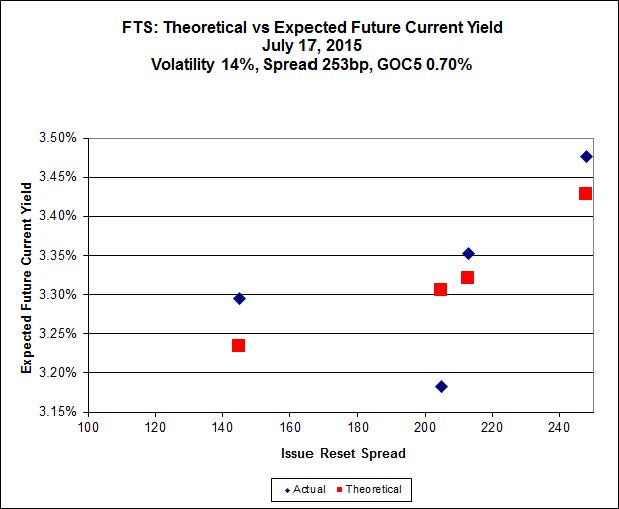

FTS.PR.K, with a spread of +205bp, and bid at 21.60, looks $0.80 expensive and resets 2019-3-1. FTS.PR.M, with a spread of +248bp and resetting 2019-12-1, is bid at 22.87 and is $0.32 cheap.

Click for Big

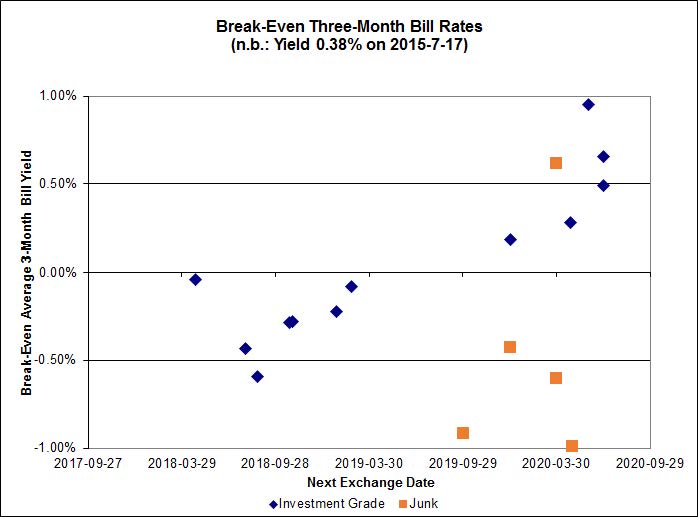

There is only one outlier; one of the junk pairs is below -1.00%.

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of 0.05% (which seems a little extreme!).

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 1.7363 % | 2,092.6 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 1.7363 % | 3,658.9 |

| Floater | 3.51 % | 3.49 % | 61,881 | 18.55 | 3 | 1.7363 % | 2,224.6 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1873 % | 2,781.5 |

| SplitShare | 4.57 % | 4.90 % | 68,000 | 3.20 | 3 | 0.1873 % | 3,259.7 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1873 % | 2,543.4 |

| Perpetual-Premium | 5.51 % | 2.95 % | 74,960 | 0.29 | 13 | 0.0487 % | 2,514.3 |

| Perpetual-Discount | 5.38 % | 5.35 % | 87,275 | 14.86 | 21 | 0.5088 % | 2,661.8 |

| FixedReset | 4.60 % | 3.78 % | 218,381 | 16.03 | 88 | 1.3821 % | 2,286.1 |

| Deemed-Retractible | 5.02 % | 4.81 % | 112,481 | 3.13 | 34 | 0.4508 % | 2,619.3 |

| FloatingReset | 2.53 % | 3.18 % | 47,513 | 6.05 | 10 | 0.6075 % | 2,277.8 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| RY.PR.J | FixedReset | -1.56 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 22.80 Evaluated at bid price : 24.02 Bid-YTW : 3.65 % |

| CU.PR.D | Perpetual-Discount | -1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 22.91 Evaluated at bid price : 23.25 Bid-YTW : 5.33 % |

| BAM.PR.C | Floater | 1.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 13.13 Evaluated at bid price : 13.13 Bid-YTW : 3.62 % |

| MFC.PR.H | FixedReset | 1.06 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2017-03-19 Maturity Price : 25.00 Evaluated at bid price : 25.84 Bid-YTW : 2.75 % |

| CU.PR.F | Perpetual-Discount | 1.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 21.89 Evaluated at bid price : 22.19 Bid-YTW : 5.12 % |

| GWO.PR.H | Deemed-Retractible | 1.11 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.78 Bid-YTW : 5.58 % |

| PWF.PR.P | FixedReset | 1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 17.05 Evaluated at bid price : 17.05 Bid-YTW : 3.58 % |

| HSE.PR.A | FixedReset | 1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 15.70 Evaluated at bid price : 15.70 Bid-YTW : 4.20 % |

| TD.PF.E | FixedReset | 1.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 23.17 Evaluated at bid price : 25.09 Bid-YTW : 3.53 % |

| BAM.PF.G | FixedReset | 1.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 22.35 Evaluated at bid price : 23.12 Bid-YTW : 4.14 % |

| ENB.PF.G | FixedReset | 1.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 19.43 Evaluated at bid price : 19.43 Bid-YTW : 4.88 % |

| HSB.PR.D | Deemed-Retractible | 1.21 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.00 Bid-YTW : 5.07 % |

| TRP.PR.A | FixedReset | 1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 19.09 Evaluated at bid price : 19.09 Bid-YTW : 3.75 % |

| SLF.PR.C | Deemed-Retractible | 1.23 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.30 Bid-YTW : 6.01 % |

| GWO.PR.N | FixedReset | 1.25 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.19 Bid-YTW : 7.49 % |

| GWO.PR.Q | Deemed-Retractible | 1.26 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.98 Bid-YTW : 5.22 % |

| SLF.PR.B | Deemed-Retractible | 1.29 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.54 Bid-YTW : 5.66 % |

| BMO.PR.T | FixedReset | 1.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 22.16 Evaluated at bid price : 22.71 Bid-YTW : 3.54 % |

| CM.PR.Q | FixedReset | 1.45 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 23.00 Evaluated at bid price : 24.55 Bid-YTW : 3.55 % |

| TD.PF.B | FixedReset | 1.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 21.89 Evaluated at bid price : 22.30 Bid-YTW : 3.57 % |

| BMO.PR.W | FixedReset | 1.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 21.90 Evaluated at bid price : 22.33 Bid-YTW : 3.58 % |

| SLF.PR.A | Deemed-Retractible | 1.60 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.55 Bid-YTW : 5.60 % |

| RY.PR.H | FixedReset | 1.62 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 22.10 Evaluated at bid price : 22.61 Bid-YTW : 3.57 % |

| BAM.PF.A | FixedReset | 1.66 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 22.22 Evaluated at bid price : 22.69 Bid-YTW : 4.22 % |

| HSE.PR.C | FixedReset | 1.73 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 21.89 Evaluated at bid price : 22.33 Bid-YTW : 4.57 % |

| BMO.PR.Q | FixedReset | 1.74 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.40 Bid-YTW : 3.49 % |

| HSB.PR.C | Deemed-Retractible | 1.76 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2015-08-16 Maturity Price : 25.00 Evaluated at bid price : 25.44 Bid-YTW : -12.85 % |

| TD.PF.C | FixedReset | 1.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 21.93 Evaluated at bid price : 22.39 Bid-YTW : 3.54 % |

| BMO.PR.S | FixedReset | 1.79 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 22.53 Evaluated at bid price : 23.32 Bid-YTW : 3.51 % |

| BAM.PR.Z | FixedReset | 1.81 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 22.57 Evaluated at bid price : 23.10 Bid-YTW : 4.22 % |

| BAM.PF.E | FixedReset | 1.89 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 21.32 Evaluated at bid price : 21.60 Bid-YTW : 4.19 % |

| ENB.PF.C | FixedReset | 1.91 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 19.21 Evaluated at bid price : 19.21 Bid-YTW : 4.86 % |

| PWF.PR.K | Perpetual-Discount | 1.91 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 23.68 Evaluated at bid price : 23.95 Bid-YTW : 5.17 % |

| BIP.PR.A | FixedReset | 2.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 21.85 Evaluated at bid price : 22.30 Bid-YTW : 4.94 % |

| BNS.PR.D | FloatingReset | 2.07 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.68 Bid-YTW : 3.77 % |

| ENB.PR.F | FixedReset | 2.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 17.56 Evaluated at bid price : 17.56 Bid-YTW : 4.94 % |

| FTS.PR.K | FixedReset | 2.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 21.31 Evaluated at bid price : 21.60 Bid-YTW : 3.55 % |

| MFC.PR.J | FixedReset | 2.21 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.02 Bid-YTW : 4.15 % |

| BAM.PR.N | Perpetual-Discount | 2.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 20.63 Evaluated at bid price : 20.63 Bid-YTW : 5.82 % |

| BAM.PR.M | Perpetual-Discount | 2.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 20.61 Evaluated at bid price : 20.61 Bid-YTW : 5.82 % |

| BAM.PF.C | Perpetual-Discount | 2.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 20.96 Evaluated at bid price : 20.96 Bid-YTW : 5.85 % |

| ENB.PF.E | FixedReset | 2.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 19.30 Evaluated at bid price : 19.30 Bid-YTW : 4.88 % |

| ENB.PR.J | FixedReset | 2.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 18.71 Evaluated at bid price : 18.71 Bid-YTW : 4.85 % |

| BNS.PR.Z | FixedReset | 2.50 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.39 Bid-YTW : 3.43 % |

| ENB.PF.A | FixedReset | 2.52 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 19.10 Evaluated at bid price : 19.10 Bid-YTW : 4.90 % |

| NA.PR.W | FixedReset | 2.54 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 21.80 Evaluated at bid price : 22.20 Bid-YTW : 3.61 % |

| MFC.PR.C | Deemed-Retractible | 2.61 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.76 Bid-YTW : 5.81 % |

| BAM.PF.F | FixedReset | 2.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 22.57 Evaluated at bid price : 23.45 Bid-YTW : 4.06 % |

| ENB.PR.H | FixedReset | 2.71 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 16.30 Evaluated at bid price : 16.30 Bid-YTW : 4.84 % |

| RY.PR.Z | FixedReset | 2.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 22.56 Evaluated at bid price : 23.37 Bid-YTW : 3.39 % |

| ENB.PR.P | FixedReset | 2.83 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 17.80 Evaluated at bid price : 17.80 Bid-YTW : 4.90 % |

| BAM.PR.R | FixedReset | 2.97 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 18.70 Evaluated at bid price : 18.70 Bid-YTW : 4.32 % |

| BAM.PF.B | FixedReset | 3.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 20.76 Evaluated at bid price : 20.76 Bid-YTW : 4.36 % |

| ENB.PR.Y | FixedReset | 3.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 17.84 Evaluated at bid price : 17.84 Bid-YTW : 4.78 % |

| BAM.PF.D | Perpetual-Discount | 3.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 21.25 Evaluated at bid price : 21.25 Bid-YTW : 5.82 % |

| BAM.PR.T | FixedReset | 3.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 19.24 Evaluated at bid price : 19.24 Bid-YTW : 4.25 % |

| BAM.PR.X | FixedReset | 3.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 16.79 Evaluated at bid price : 16.79 Bid-YTW : 4.20 % |

| TRP.PR.C | FixedReset | 3.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 15.68 Evaluated at bid price : 15.68 Bid-YTW : 3.80 % |

| CIU.PR.C | FixedReset | 3.57 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 16.26 Evaluated at bid price : 16.26 Bid-YTW : 3.46 % |

| BAM.PR.K | Floater | 3.95 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 13.70 Evaluated at bid price : 13.70 Bid-YTW : 3.47 % |

| ENB.PR.N | FixedReset | 4.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 18.39 Evaluated at bid price : 18.39 Bid-YTW : 4.90 % |

| ENB.PR.D | FixedReset | 4.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 17.13 Evaluated at bid price : 17.13 Bid-YTW : 4.88 % |

| MFC.PR.M | FixedReset | 4.35 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.80 Bid-YTW : 4.75 % |

| IFC.PR.A | FixedReset | 4.44 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.81 Bid-YTW : 6.67 % |

| MFC.PR.K | FixedReset | 4.69 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.11 Bid-YTW : 4.89 % |

| ENB.PR.B | FixedReset | 4.87 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 17.01 Evaluated at bid price : 17.01 Bid-YTW : 4.90 % |

| MFC.PR.N | FixedReset | 4.90 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.48 Bid-YTW : 4.86 % |

| TRP.PR.F | FloatingReset | 5.88 % | Reversing a good-sized chunk of yesterday‘s nonsense. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 18.00 Evaluated at bid price : 18.00 Bid-YTW : 3.41 % |

| MFC.PR.L | FixedReset | 6.70 % | Nothing wrong with this! Each of the last 25 trades were above the closing bid and the high for the day was 22.61. The VWAP on 7,504 shares was 22.18. After making the Performance Highlights Table (and not in a good way) on each of July 7, July 8, July 9 and July 10, it was about time the issue caught a break. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.30 Bid-YTW : 4.87 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| NA.PR.M | Deemed-Retractible | 220,933 | Scotia crossed 220,000 at 25.52. Nice ticket! YTW SCENARIO Maturity Type : Call Maturity Date : 2015-08-16 Maturity Price : 25.50 Evaluated at bid price : 25.50 Bid-YTW : 0.20 % |

| BNS.PR.Y | FixedReset | 150,667 | Scotia crossed 130,000 at 22.30. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.27 Bid-YTW : 3.70 % |

| SLF.PR.I | FixedReset | 70,939 | Nesbitt crossed 43,000 at 23.80. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.75 Bid-YTW : 4.36 % |

| RY.PR.F | Deemed-Retractible | 58,300 | TD crossed 55,000 at 25.41. YTW SCENARIO Maturity Type : Call Maturity Date : 2016-05-24 Maturity Price : 25.00 Evaluated at bid price : 25.41 Bid-YTW : 3.26 % |

| HSE.PR.G | FixedReset | 43,617 | Nesbitt crossed 24,700 at 23.99. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 22.76 Evaluated at bid price : 23.95 Bid-YTW : 4.56 % |

| BAM.PF.E | FixedReset | 38,016 | RBC crossed 35,000 at 21.30. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-17 Maturity Price : 21.32 Evaluated at bid price : 21.60 Bid-YTW : 4.19 % |

| There were 53 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| TRP.PR.E | FixedReset | Quote: 22.00 – 23.00 Spot Rate : 1.0000 Average : 0.6436 YTW SCENARIO |

| PWF.PR.L | Perpetual-Discount | Quote: 24.22 – 24.98 Spot Rate : 0.7600 Average : 0.4906 YTW SCENARIO |

| RY.PR.J | FixedReset | Quote: 24.02 – 24.64 Spot Rate : 0.6200 Average : 0.3973 YTW SCENARIO |

| CU.PR.D | Perpetual-Discount | Quote: 23.25 – 23.89 Spot Rate : 0.6400 Average : 0.4494 YTW SCENARIO |

| GWO.PR.S | Deemed-Retractible | Quote: 25.65 – 26.18 Spot Rate : 0.5300 Average : 0.3627 YTW SCENARIO |

| TRP.PR.D | FixedReset | Quote: 21.60 – 22.10 Spot Rate : 0.5000 Average : 0.3356 YTW SCENARIO |