So, are the oil sands now a white elephant?

The last place oil producers want to be when prices plummet to profit-demolishing lows is midstream on a billion-dollar project in one of the costliest parts of the planet to extract crude.

Yet that’s exactly where half a dozen oil sands operators from Suncor Energy Inc. to Brion Energy Corp. find themselves with prices for Canadian oil now hovering around $30 a barrel. While all around them projects have been postponed or canceled, their investments were judged too far along when the oil game suddenly moved from offense to defense.

These projects will add at least another 500,000 barrels a day — roughly a 25 percent increase from Alberta — to an oversupplied North American market by 2017.

…

A general rule of thumb says new plants require a West Texas Intermediate price of $80 a barrel to break even. Western Canada Select, a blend of heavy Alberta crude, is currently selling at a discount of about $14 a barrel to the WTI benchmark, which closed at $46.75 Thursday in New York.

…

Returns on capital invested by Canada’s largest oil-sands producers reached 20 percent at some points over the past five years, according to data compiled by Bloomberg. That figure is now closer to zero or negative for companies such as Athabasca Oil Co. and Cenovus.

There are two things you can sell in this world: entertainment and things. Don’t sell things:

In most AT&T, Sprint, or T-Mobile stores, it takes a while to find the ZTE phones, buried in the back, past the latest from Apple and Samsung. But they’re there. In AT&T stores it’s the ZTE Maven, which has a screen, speakers, and a processor with capabilities somewhere between the iPhone 5 and 6. As Tony Greco, ZTE’s head of U.S. retail marketing, puts it, “These were state-of-the-art features two years ago.” The Maven’s draw, really, is price. Without any subsidies from a wireless carrier, the phone costs just $60. And it’s not even one of the company’s cheaper models.

…

ZTE is quietly becoming a force in the U.S. by selling good enough phones at low prices—smaller prepaid smartphones for $30, basic phones with QWERTY keyboards for about the same, and so on. The Chinese company’s products are among the cheap phones of choice at three of the big four U.S. carriers. (Verizon doesn’t carry them.) ZTE claimed about 8 percent of America’s smartphone market in the second quarter of this year, says researcher IDC, up from 4.2 percent in the first quarter of 2014. That ranks the company fourth among smartphone makers overall, behind Apple, Samsung, and LG. “We came from nowhere, and now we are a solid force,” says Lixin Cheng, head of ZTE’s U.S. operations.

So the question of the day is: if you pay quintuple price, can you really say you’ve bought a “smart” ‘phone?

Thanks to a new thesaurus, I now have many more words to describe the preferred share market:

Let’s let Rajna Gibson Brandon and Christopher Hemmens from the University of Geneva and the University of St. Gallen’s Mathieu Trepanier explain:

“We find that market irrationality has a signicantly negative effect on subsequent stock market returns — proxied by the S&P 500 and the Dow Jones Industrial Average — and exacerbates stock market volatility,” they write in a new research paper. “The full impact takes time to manifest with small downturns at first culminating in a significant negative impact after three days followed by a weak reversal almost a week later.”

By “market irrationality” they are referring specifically to the types of words appearing in the financial press that, to use some fancy words, may prove to be parlous augers for stock prices. They list 141 words, but some of the favorites around here are “bonkers,” “barbarous,” “berserk,” “daft,” “perverse” and “psycho.” (Yes, a lot of words beginning with “b,” the Greek equivalent of which is “beta.”)

Brompton Split Banc Corp., proud issuer of SBC.PR.A was confirmed at Pfd-3(high) by DBRS:

The main form of credit enhancement available to the Preferred Shares is a buffer of downside protection. Downside protection corresponds to the percentage decline in market value of the Portfolio that must be experienced before the Preferred Shares would be in a loss position. The amount of downside protection available to the Preferred Shares as of August 6, 2015, is 55.8%.

In the past year, the performance of the Company has been stable. Current dividend coverage is 1.65 times. Quarterly Preferred Share and monthly Capital Share distributions have remained unchanged since 2013. Other key rating considerations include the credit quality, volatility and diversification of the Portfolio as well as changes in the dividend policies of the underlying companies in the Portfolio.

Based on the aforementioned considerations and performance metrics, DBRS confirms the Pfd-3 (high) rating of the Preferred Shares issued by Brompton Split Banc Corp.

Canadian Banc Corp., proud issuer of BK.PR.A, was confirmed at Pfd-3(high) by DBRS:

The main form of credit enhancement available to the Preferred Shares is a buffer of downside protection. The amount of downside protection available to the Preferred Shares as of August 26, 2015, is 53.4%. The Preferred Share dividend coverage ratio is approximately 1.18 times.

Although the credit quality of the underlying assets of the Portfolio is strong, the Portfolio is concentrated in the financial services industry. As a result, its value has recently seen a slight deterioration due to the weak performance of common shares of the six Canadian Banks since the beginning of 2015. The floating nature of dividend distributions to Preferred Shares and Class A Shares, although mitigated by predetermined ranges of dividend yields, may potentially increase the volatility of the protection available to holders of the Preferred Shares in a high interest rate environment.

Based on these considerations and aforementioned performance metrics, DBRS confirms the Pfd-3 (high) rating of the Canadian Banc Corp. Preferred Shares.

It was another fine day for the Canadian preferred share market, with PerpetualDiscounts gaining 12bp, FixedResets winning 45bp and DeemedRetractibles up 16bp. The Performance Highlights table is notable for having very few losers today. Volume was very low.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

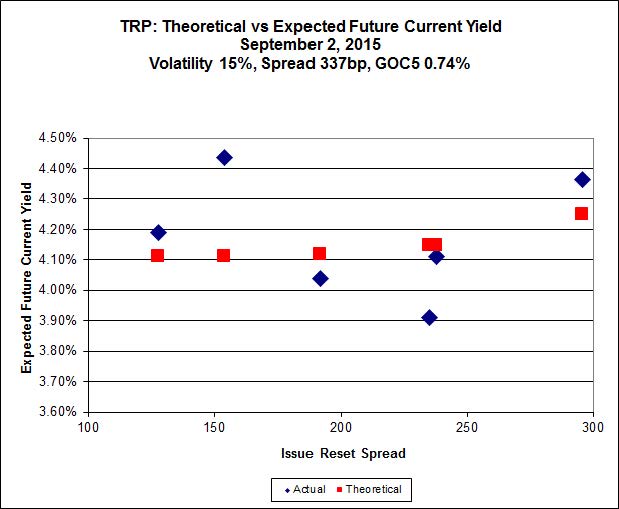

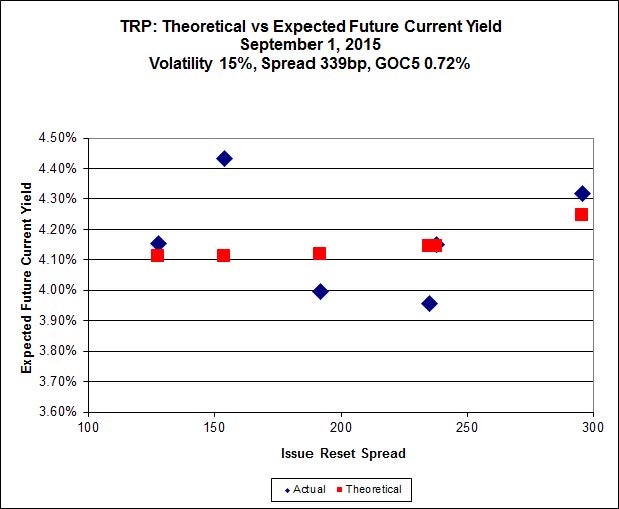

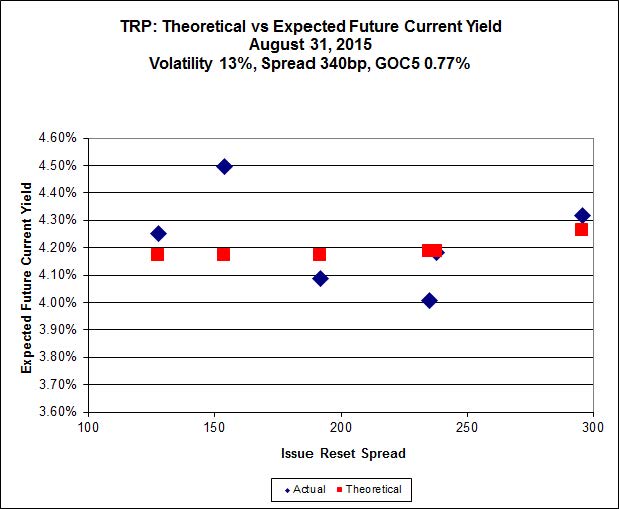

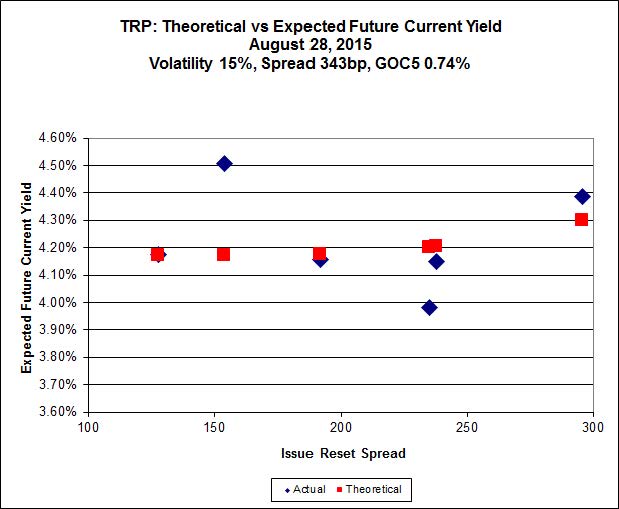

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 19.67 to be $0.93 rich, while TRP.PR.C, resetting 2016-1-30 at +164, is $0.83 cheap at its bid price of 13.10.

Click for Big

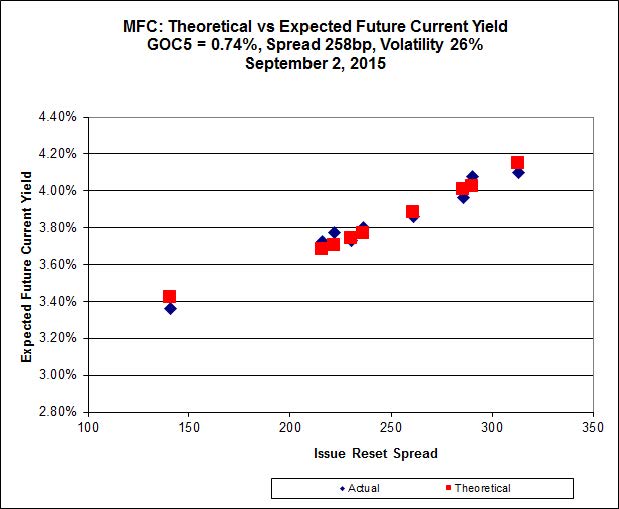

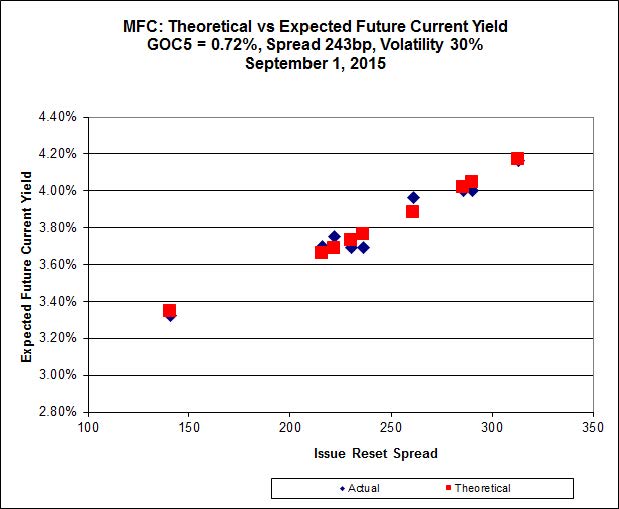

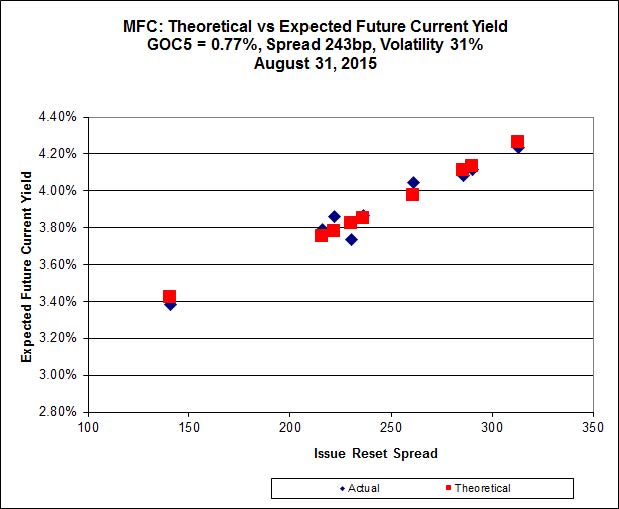

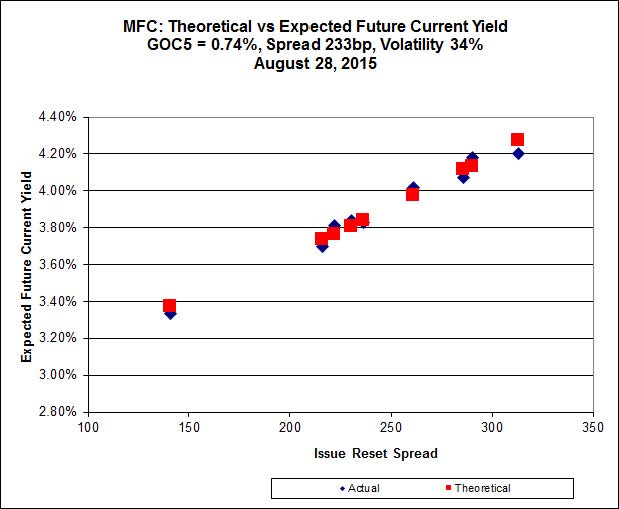

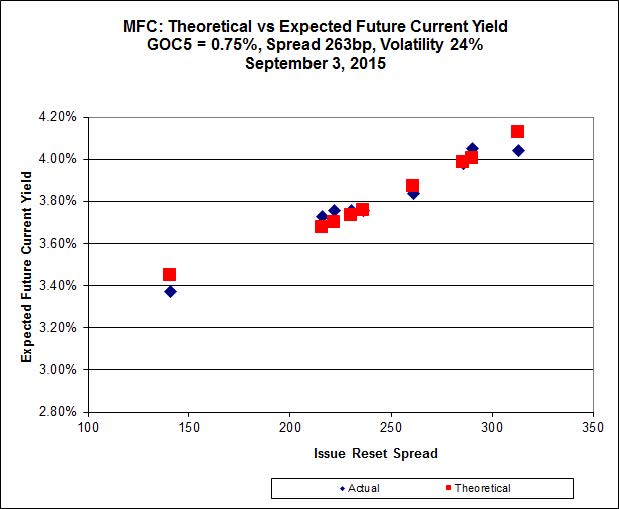

Another good fit today for MFC, with Implied Volatility dropping a bit again today.

Most expensive is MFC.PR.H, resetting at +313bp on 2017-3-19, bid at 24.00 to be 0.30 rich, while MFC.PR.K, resetting at +222bp on 2018-9-19, is bid at 19.77 to be 0.31 cheap.

Click for Big

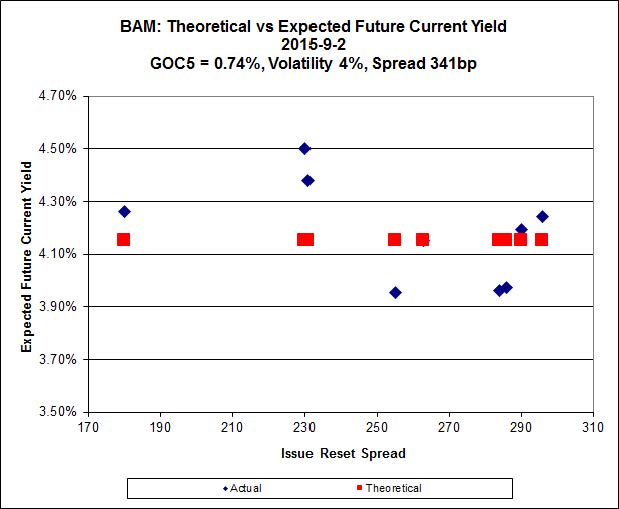

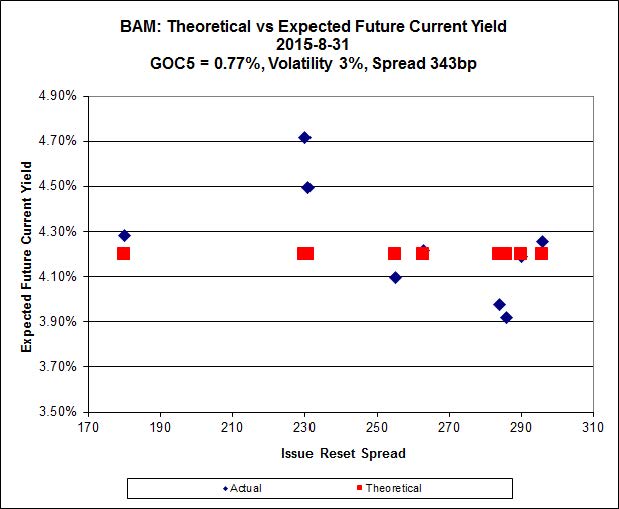

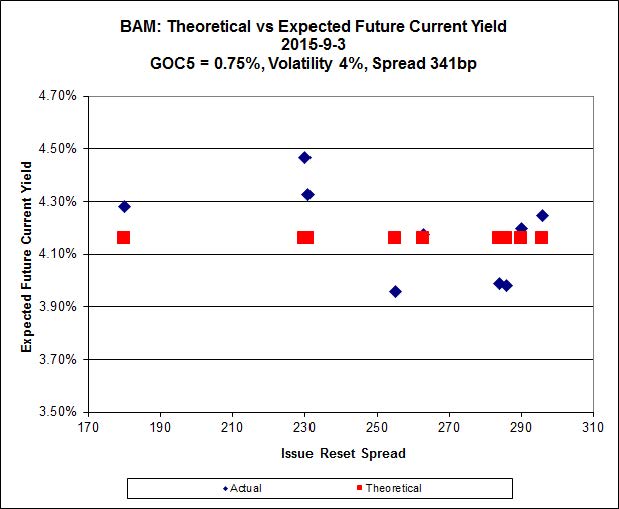

The fit on the BAM issues continues to be horrible.

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 17.07 to be $1.26 cheap. BAM.PF.E, resetting at +255bp on 2020-3-31 is bid at 20..85 and appears to be $1.02 rich.

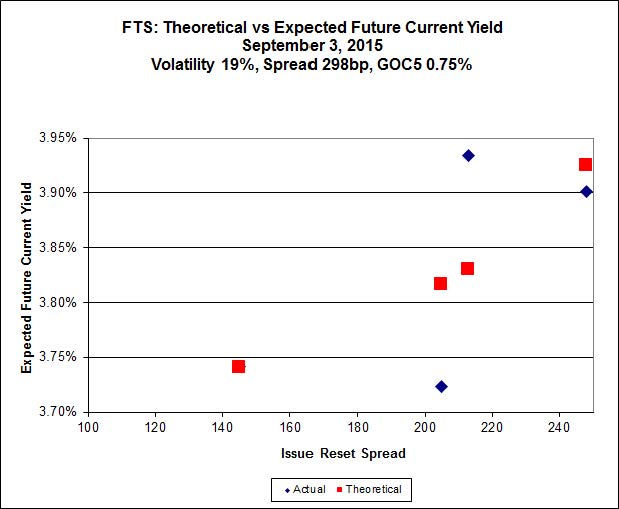

Click for Big

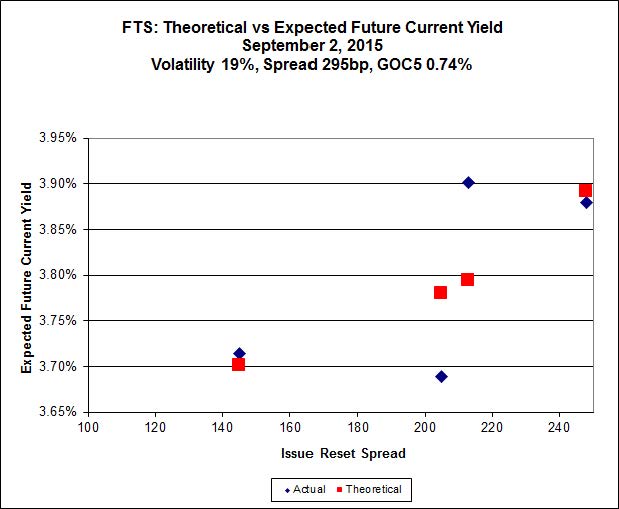

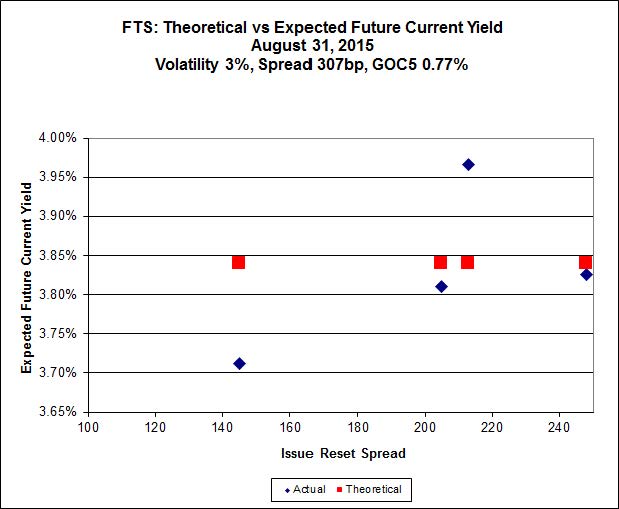

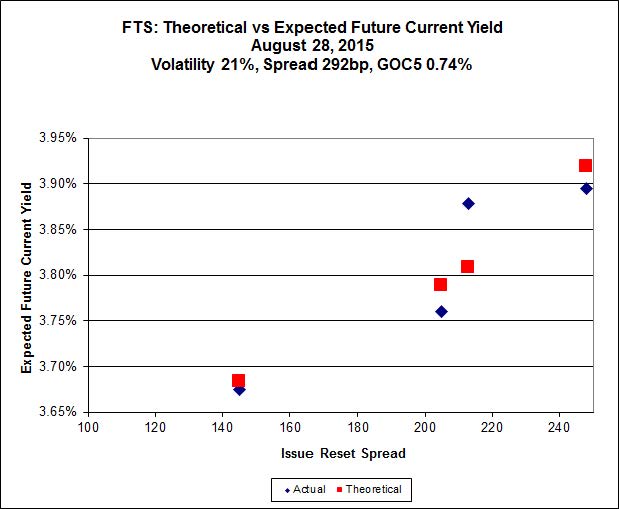

FTS.PR.K, with a spread of +205bp, and bid at 18.80, looks $0.46 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 18.30 and is $0.50 cheap.

Click for Big

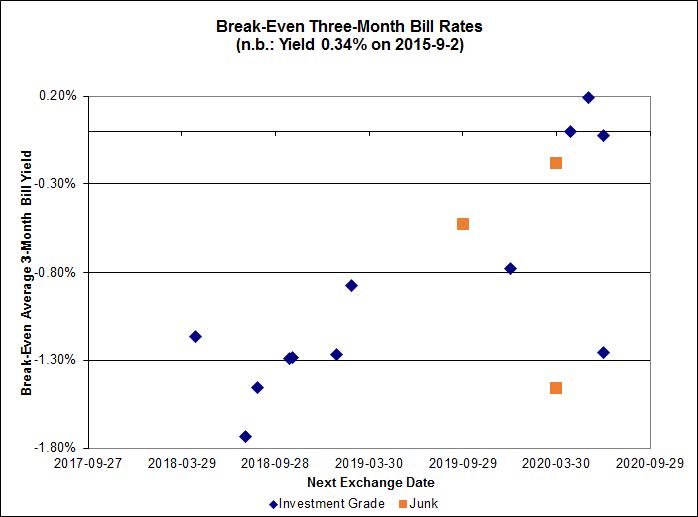

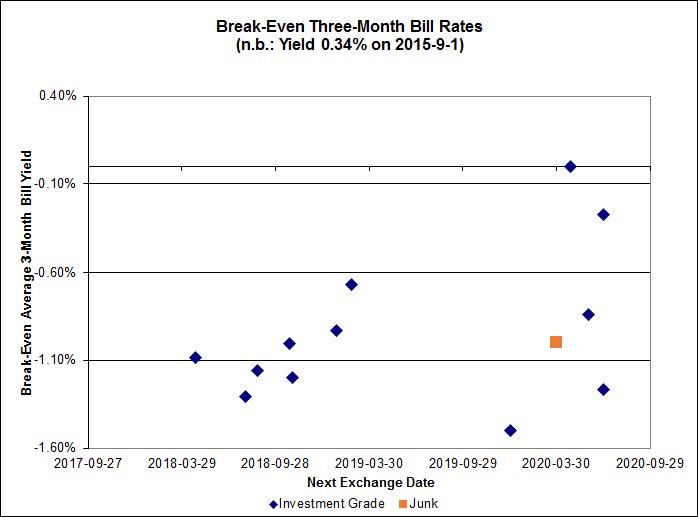

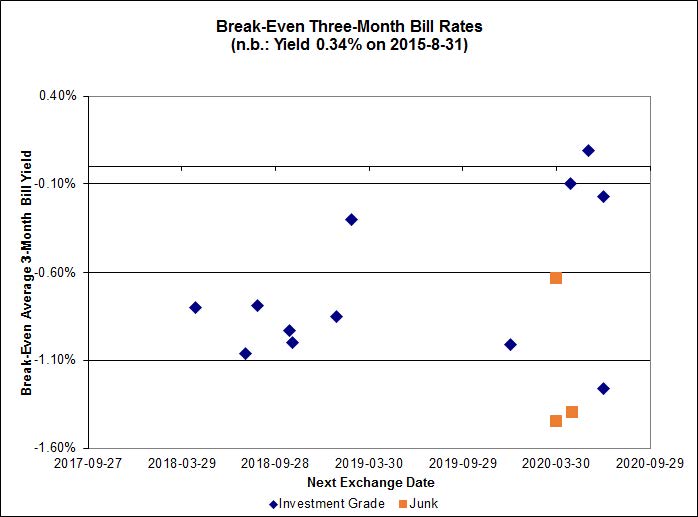

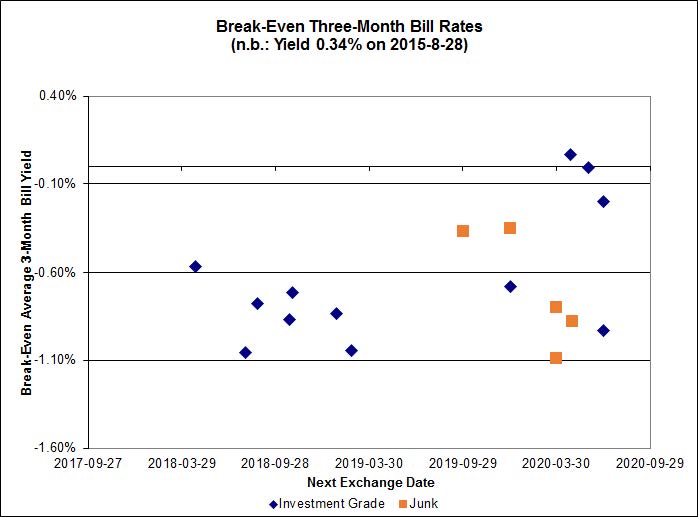

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.94%, with no outliers. Note that the distribution is bimodal, with NVCC non-compliant bank issues averaging -1.25% and the unregulated issues averaging -0.51%. There is one junk outlier below -1.80% and one above +0.20%.

Click for Big

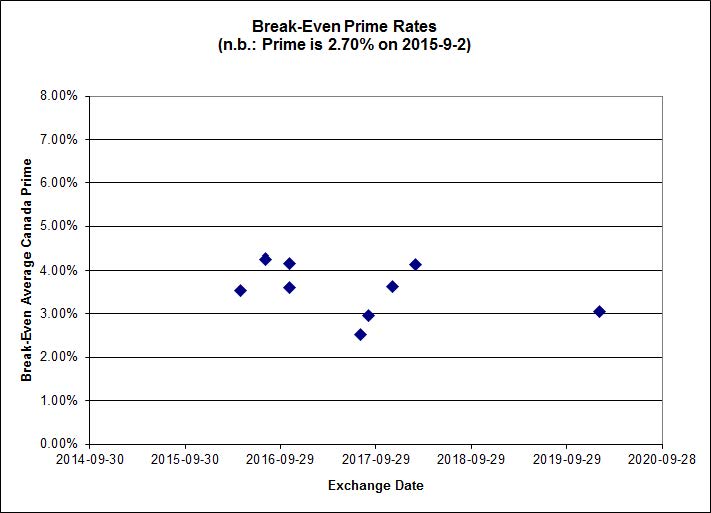

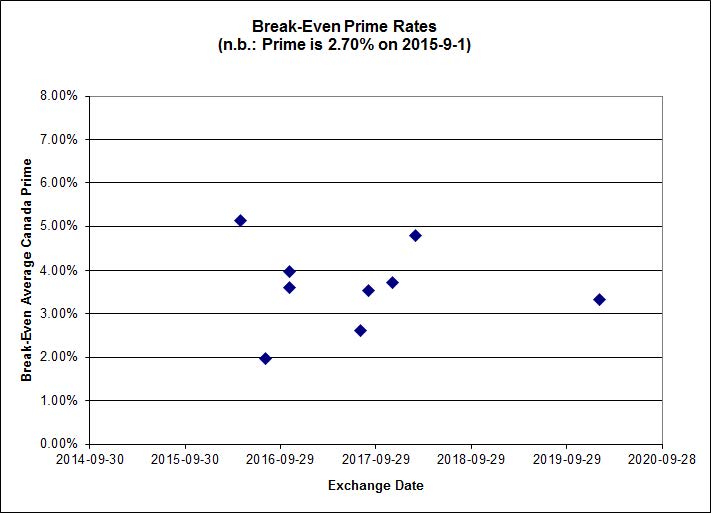

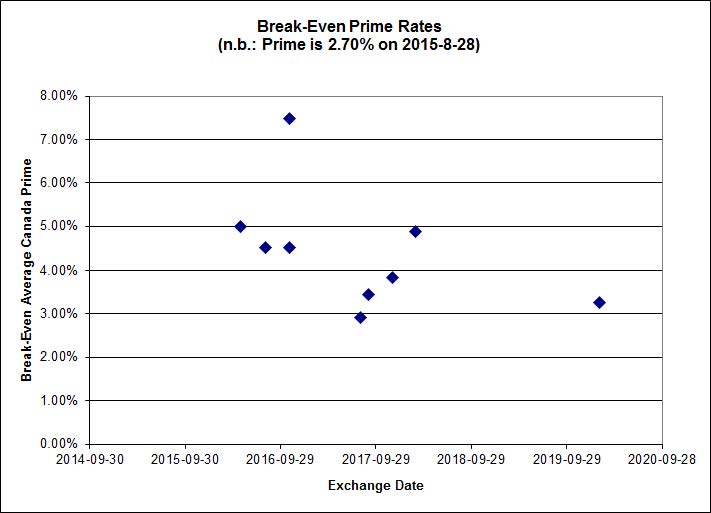

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.2490 % | 1,658.9 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.2490 % | 2,900.5 |

| Floater | 4.42 % | 4.50 % | 56,166 | 16.34 | 3 | -0.2490 % | 1,763.5 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1221 % | 2,774.2 |

| SplitShare | 4.64 % | 4.87 % | 66,031 | 3.10 | 3 | 0.1221 % | 3,251.2 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1221 % | 2,536.7 |

| Perpetual-Premium | 5.72 % | 5.42 % | 59,641 | 2.01 | 8 | 0.0594 % | 2,490.1 |

| Perpetual-Discount | 5.46 % | 5.52 % | 75,759 | 14.63 | 30 | 0.1244 % | 2,589.0 |

| FixedReset | 4.73 % | 4.20 % | 178,014 | 16.09 | 74 | 0.4543 % | 2,150.1 |

| Deemed-Retractible | 5.15 % | 5.08 % | 102,708 | 5.52 | 33 | 0.1619 % | 2,576.5 |

| FloatingReset | 2.43 % | 3.80 % | 49,700 | 5.95 | 9 | -0.0216 % | 2,173.7 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| TRP.PR.F | FloatingReset | -2.81 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-03 Maturity Price : 14.16 Evaluated at bid price : 14.16 Bid-YTW : 3.98 % |

| SLF.PR.H | FixedReset | -1.82 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.85 Bid-YTW : 6.55 % |

| FTS.PR.F | Perpetual-Discount | -1.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-03 Maturity Price : 22.07 Evaluated at bid price : 22.30 Bid-YTW : 5.52 % |

| SLF.PR.C | Deemed-Retractible | 1.01 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.06 Bid-YTW : 6.73 % |

| TD.PF.E | FixedReset | 1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-03 Maturity Price : 22.95 Evaluated at bid price : 24.45 Bid-YTW : 3.63 % |

| BAM.PR.R | FixedReset | 1.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-03 Maturity Price : 17.07 Evaluated at bid price : 17.07 Bid-YTW : 4.68 % |

| CM.PR.Q | FixedReset | 1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-03 Maturity Price : 22.45 Evaluated at bid price : 23.30 Bid-YTW : 3.77 % |

| BAM.PF.C | Perpetual-Discount | 1.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-03 Maturity Price : 21.20 Evaluated at bid price : 21.20 Bid-YTW : 5.83 % |

| BMO.PR.Y | FixedReset | 1.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-03 Maturity Price : 22.62 Evaluated at bid price : 23.65 Bid-YTW : 3.72 % |

| SLF.PR.D | Deemed-Retractible | 1.31 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.90 Bid-YTW : 6.83 % |

| TRP.PR.B | FixedReset | 1.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-03 Maturity Price : 12.21 Evaluated at bid price : 12.21 Bid-YTW : 4.19 % |

| BAM.PR.M | Perpetual-Discount | 1.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-03 Maturity Price : 21.00 Evaluated at bid price : 21.00 Bid-YTW : 5.77 % |

| NA.PR.S | FixedReset | 1.42 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-03 Maturity Price : 21.45 Evaluated at bid price : 21.45 Bid-YTW : 3.89 % |

| TRP.PR.G | FixedReset | 1.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-03 Maturity Price : 21.50 Evaluated at bid price : 21.50 Bid-YTW : 4.35 % |

| MFC.PR.M | FixedReset | 1.47 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.70 Bid-YTW : 5.91 % |

| BAM.PR.T | FixedReset | 1.55 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-03 Maturity Price : 17.68 Evaluated at bid price : 17.68 Bid-YTW : 4.59 % |

| HSE.PR.C | FixedReset | 1.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-03 Maturity Price : 21.15 Evaluated at bid price : 21.15 Bid-YTW : 4.75 % |

| MFC.PR.H | FixedReset | 1.69 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.00 Bid-YTW : 4.51 % |

| TD.PR.T | FloatingReset | 1.79 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.70 Bid-YTW : 3.53 % |

| TRP.PR.C | FixedReset | 1.95 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-03 Maturity Price : 13.10 Evaluated at bid price : 13.10 Bid-YTW : 4.45 % |

| BAM.PF.D | Perpetual-Discount | 2.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-03 Maturity Price : 21.31 Evaluated at bid price : 21.60 Bid-YTW : 5.76 % |

| HSE.PR.E | FixedReset | 2.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-03 Maturity Price : 21.76 Evaluated at bid price : 22.15 Bid-YTW : 4.89 % |

| NA.PR.W | FixedReset | 2.61 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-03 Maturity Price : 20.80 Evaluated at bid price : 20.80 Bid-YTW : 3.85 % |

| BMO.PR.W | FixedReset | 2.93 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-03 Maturity Price : 21.10 Evaluated at bid price : 21.10 Bid-YTW : 3.72 % |

| PWF.PR.P | FixedReset | 3.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-03 Maturity Price : 16.00 Evaluated at bid price : 16.00 Bid-YTW : 3.73 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| MFC.PR.K | FixedReset | 99,506 | RBC crossed blocks of 47,200 and 30,000, both at 19.95. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.77 Bid-YTW : 6.24 % |

| RY.PR.Z | FixedReset | 72,000 | RBC crossed 50,000 at 21.60. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-03 Maturity Price : 21.28 Evaluated at bid price : 21.56 Bid-YTW : 3.63 % |

| BNS.PR.O | Deemed-Retractible | 69,410 | RBC sold 12,200 to anonymous at 25.62; 10,000 to TD at 25.62, and another 20,000 to TD at 25.60. YTW SCENARIO Maturity Type : Call Maturity Date : 2016-04-27 Maturity Price : 25.25 Evaluated at bid price : 25.60 Bid-YTW : 4.14 % |

| IAG.PR.G | FixedReset | 55,881 | RBC crossed 50,000 at 23.95. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.78 Bid-YTW : 4.34 % |

| BAM.PF.B | FixedReset | 42,250 | Desjardins crossed 36,800 at 20.30. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-03 Maturity Price : 20.24 Evaluated at bid price : 20.24 Bid-YTW : 4.44 % |

| MFC.PR.G | FixedReset | 34,467 | RBC crossed 30,000 at 22.70. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.53 Bid-YTW : 5.07 % |

| There were 18 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| RY.PR.M | FixedReset | Quote: 22.72 – 24.00 Spot Rate : 1.2800 Average : 1.0892 YTW SCENARIO |

| RY.PR.H | FixedReset | Quote: 21.55 – 22.25 Spot Rate : 0.7000 Average : 0.5119 YTW SCENARIO |

| TRP.PR.F | FloatingReset | Quote: 14.16 – 15.14 Spot Rate : 0.9800 Average : 0.8062 YTW SCENARIO |

| FTS.PR.F | Perpetual-Discount | Quote: 22.30 – 22.85 Spot Rate : 0.5500 Average : 0.3983 YTW SCENARIO |

| HSE.PR.G | FixedReset | Quote: 22.31 – 22.90 Spot Rate : 0.5900 Average : 0.4392 YTW SCENARIO |

| VNR.PR.A | FixedReset | Quote: 19.80 – 20.37 Spot Rate : 0.5700 Average : 0.4658 YTW SCENARIO |