It will be the end of an era in the Treasury market, with the last double digit coupon bond maturing:

The last Treasury bond with a coupon above 10 percent is older than some government-debt traders. It turns 30 tomorrow.

The bond was issued on Aug. 15, 1985, and is one of just five Treasury bonds left with coupons of 9 percent or higher. All of them mature in the next three years. And as the ranks of high-coupon government bonds have gotten smaller, so has the number of traders and analysts who were on Wall Street desks when high yields and worries about rising prices were the norm.

I still have fond memories of the Canada 10.25% of 2004-2-1 and the good old ‘Porsches’ … 9% March 1, 11. Nowadays, of course, that marks me as an old fogey.

Sesame Street is moving to HBO:

Sesame Workshop, the nonprofit group behind the children’s television program, has struck a five-year deal with HBO, the premium cable network, that will bring first-run episodes of “Sesame Street” exclusively to HBO and its streaming outlets starting in the fall.

The partnership, announced Thursday, will allow the financially challenged Sesame Workshop to significantly increase its production of “Sesame Street” episodes and other new programming. The group will produce 35 new “Sesame Street” episodes a year, up from the 18 it now produces. It will also create a spinoff series based on the “Sesame Street” Muppets along with another new educational series for children.

After nine months of appearing only on HBO, the shows will be available free on PBS, home to “Sesame Street” for the last 45 years.

Naturally, is some carping:

Yes, if we had the lavishly supported BBC-style system that the U.S. never had, PBS and the Corporation for Public Broadcasting might have been able to step in and feather Big Bird’s nest.

…

The Sesame Street is, practically, a good deal. But it is a deal nonetheless, over something that was once a given. It’s one more replacement of a public trust with a public-private arrangement, like a luxury developer given rights and tax breaks to build condos, in exchange for a certain percentage of affordable housing. It’s a deteriorating postal service vs. FedEx, the bus vs. Uber. Everyone still gets to visit Big Bird. Some people just have to use the poor door.

I’m happy to see the deal (and the other deal with Disney) – it helps support one of my long-term speculations, that increased globalization and technology would allow for the production of television with high production values. If you can get global revenue from a really superb show and, what’s more, make it long term global revenue then you can start to justify spending serious money on talent and production. It is, in fact, the BBC model. Sadly, we won’t see any of this money coming into Canada, or see any of our stories going out. Why produce quality, when you get the same government subsidy for garbage?

On August 11 I reported on the SEC takedown of a rather clever global hacking scheme. One of the prime suspects is:

[Vitaly] Korchevsky, 50, is one of nine people charged Tuesday by federal prosecutors and accused of being part of an alliance of hackers and traders who tapped corporate press releases before they became public and traded on the information. He was arrested at his home in Glen Mills, Pennsylvania, amid charges he helped to orchestrate a conspiracy regulators said netted $100 million.

The board of the Slavic Evangelical Baptist Church in Brookhaven, Pennsylvania, about 20 miles (32 kilometers) southwest of Philadelphia, said in a letter Thursday that Korchevsky is a “very respected and connected” member of the community who has served as senior pastor since the church was founded in 2003.

“We cannot comprehend or prevent any of these rumors and lies that have been manipulated over media channels where he has been tagged as a ’flight risk’ and simply plead to this honorable court to allow Rev. Korchevsky to get back to his family, his church and his community,” the church board members said.

Meanwhile, technology marches on – and, as usual, it is introduced with and exclusive focus on the 95% of the population that is honest, with no consideration for the other 5%:

“Keyless” car theft, which sees hackers target vulnerabilities in electronic locks and immobilizers, now accounts for 42 percent of stolen vehicles in London. BMWs and Range Rovers are particularly at-risk, police say, and can be in the hands of a technically minded criminal within 60 seconds.

Security researchers have now discovered a similar vulnerability in keyless vehicles made by several carmakers. The weakness – which affects the Radio-Frequency Identification (RFID) transponder chip used in immobilizers – was discovered in 2012, but carmakers sued the researchers to prevent them from publishing their findings.

This week the paper – by Roel Verdult and Baris Ege from Radboud University in the Netherlands and Flavio Garcia from the University of Birmingham, U.K. – is being presented at the USENIX security conference in Washington, D.C. The authors detail how the cryptography and authentication protocol used in the Megamos Crypto transponder can be targeted by malicious hackers looking to steal luxury vehicles.

…

In this case, however, researchers broke the transponder’s 96-bit cryptographic system, by listening in twice to the radio communication between the key and the transponder. This reduced the pool of potential secret key matches, and opened up the “brute force” option: running through 196,607 options of secret keys until they found the one that could start the car. It took less than half an hour.

…

The research team first took its findings to the manufacturer of the affected chip in February 2012 and then to Volkswagen in May 2013. The car-maker filed a lawsuit to block the publication of the paper – arguing that its vehicles would be placed at risk of theft – and was awarded an injunction in the U.K.’s High Court. Now, after lengthy negotiations, the paper is finally in the public domain – with just one sentence redacted.

Nice lawsuit from the carmakers. Too bad they didn’t spend the money on, you know, security. It would be interesting to read the High Court judgement and I’d poke around for it if it wasn’t PrefLetter weekend. I can see granting a six month injunction … but a permanent injunction seems counterproductive – just another opportunity for lazy Executive Vice Presidents to put off actual work.

It was a mixed day for the Canadian preferred share index, with PerpetualDiscounts gaining 16bp, FixedResets off 21bp and DeemedRetractibles up 19bp. There were no notable patterns in the Performance Highlights table. Volume was low.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

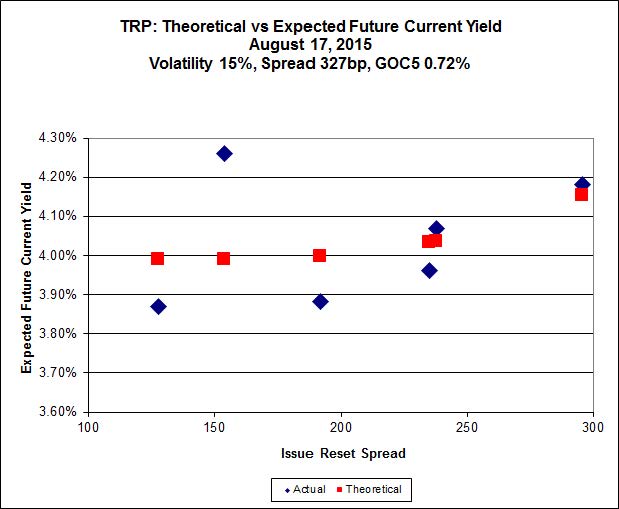

Here’s TRP:

Click for Big

Click for BigTRP.PR.B, which resets 2020-6-30 at +128, is bid at 13.16 to be $0.36 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $0.76 cheap at its bid price of 13.82.

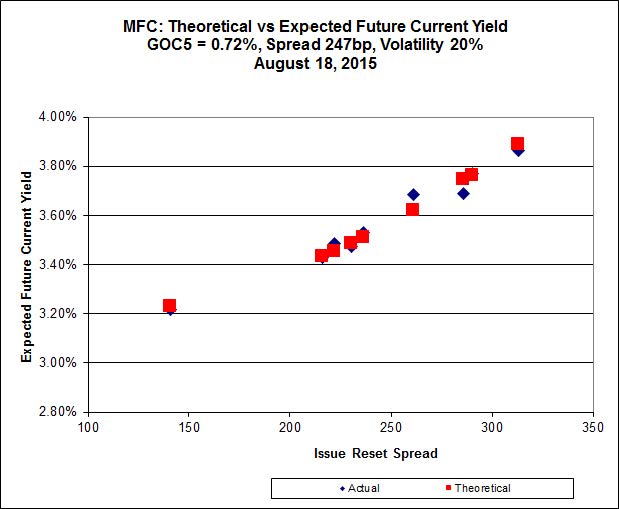

Click for Big

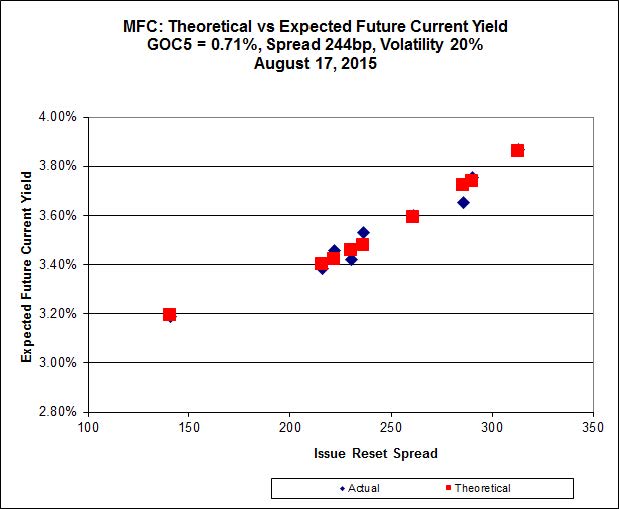

Click for BigAnother good fit today!

Most expensive is MFC.PR.I, resetting at +286bp on 2017-9-19, bid at 24.48 to be 0.29 rich, while MFC.PR.K, resetting at +222bp on 2018-9-19, is bid at 21.40 to be $0.20 cheap.

Click for Big

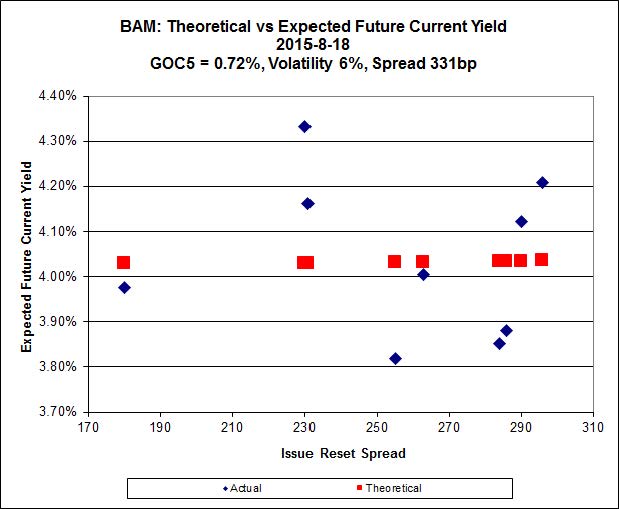

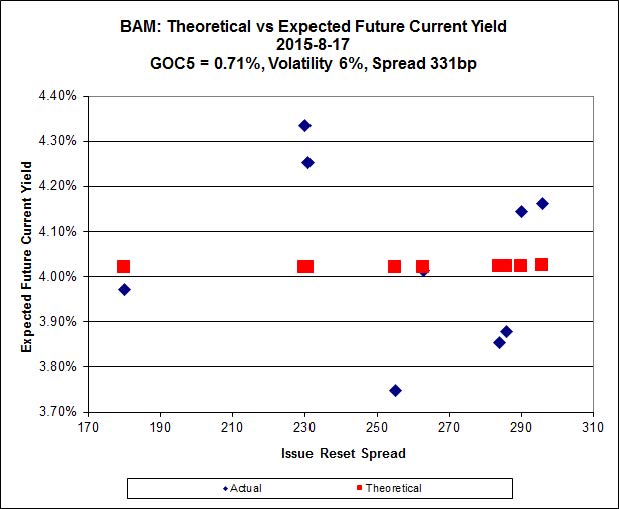

Click for BigThe fit on the BAM issues continues to be horrible.

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 17.40 to be $1.27 cheap. BAM.PF.E, resetting at +255bp on 2020-3-31 is bid at 21.70 and appears to be $1.40 rich.

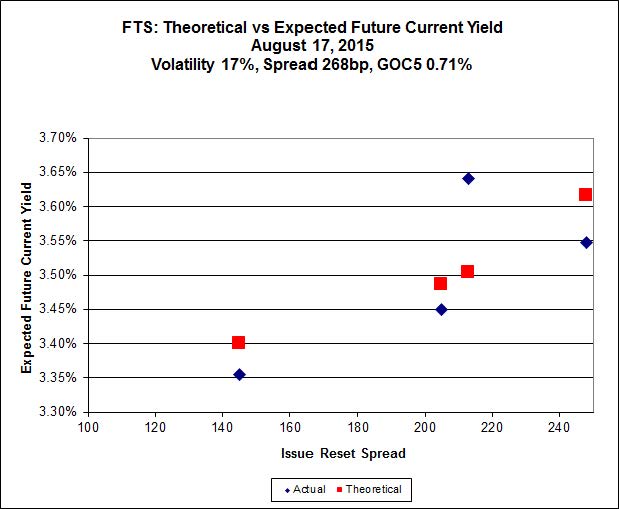

Click for Big

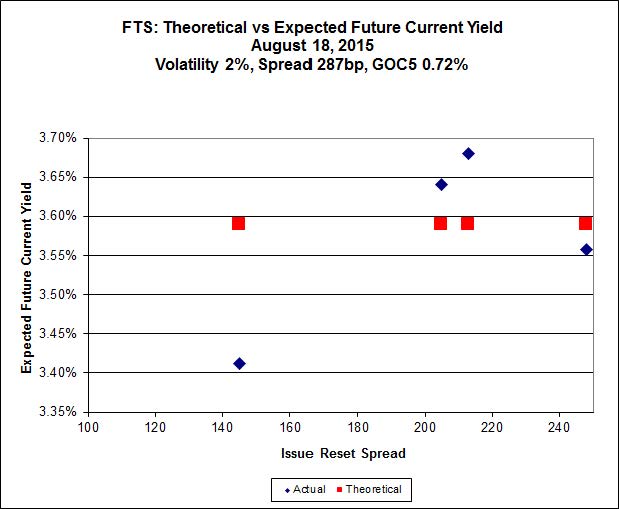

Click for BigFTS.PR.M, with a spread of +248bp, and bid at 23.04, looks $0.50 expensive and resets 2019-12-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 20.07 and is $0.63 cheap.

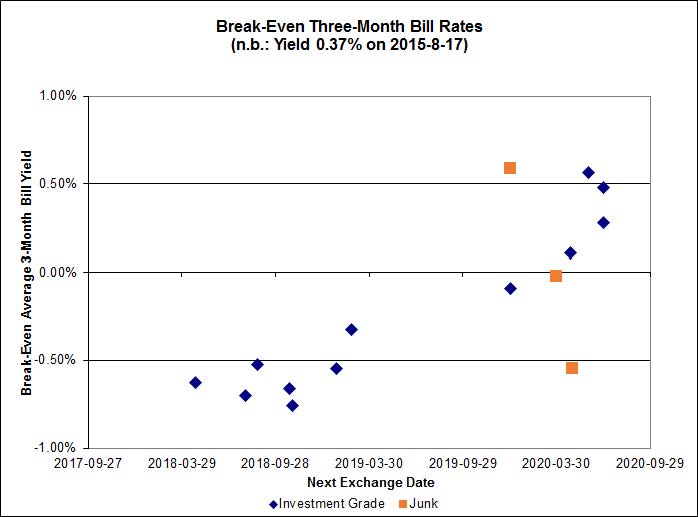

Click for Big

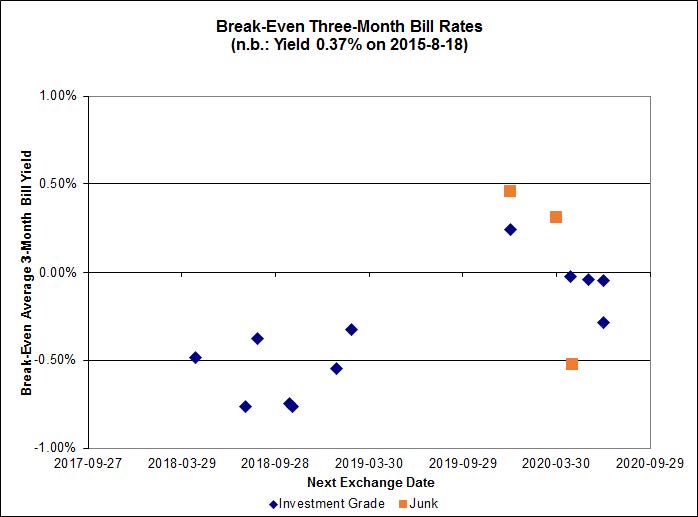

Click for BigInvestment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.32%, with no outliers. There are three junk outliers below -1.00% and one above +1.00%.

Click for Big

Click for BigShall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

HIMIPref™ Preferred Indices

These values reflect the December 2008 revision of the HIMIPref™ Indices

Values are provisional and are finalized monthly |

| Index |

Mean

Current

Yield

(at bid) |

Median

YTW |

Median

Average

Trading

Value |

Median

Mod Dur

(YTW) |

Issues |

Day’s Perf. |

Index Value |

| Ratchet |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.6057 % |

1,977.2 |

| FixedFloater |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.6057 % |

3,457.1 |

| Floater |

3.71 % |

3.78 % |

52,208 |

17.84 |

3 |

0.6057 % |

2,101.9 |

| OpRet |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

-0.0267 % |

2,777.0 |

| SplitShare |

4.58 % |

4.83 % |

55,517 |

3.12 |

3 |

-0.0267 % |

3,254.5 |

| Interest-Bearing |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

-0.0267 % |

2,539.3 |

| Perpetual-Premium |

5.72 % |

5.42 % |

60,301 |

2.06 |

9 |

-0.0353 % |

2,484.4 |

| Perpetual-Discount |

5.40 % |

5.45 % |

76,273 |

14.75 |

29 |

0.1618 % |

2,615.2 |

| FixedReset |

4.75 % |

3.87 % |

199,356 |

15.98 |

87 |

-0.2123 % |

2,221.0 |

| Deemed-Retractible |

5.10 % |

5.25 % |

98,634 |

5.44 |

34 |

0.1876 % |

2,589.4 |

| FloatingReset |

2.35 % |

3.28 % |

49,152 |

6.00 |

9 |

-0.0897 % |

2,245.8 |

| Performance Highlights |

| Issue |

Index |

Change |

Notes |

| VNR.PR.A |

FixedReset |

-3.84 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-08-14

Maturity Price : 20.02

Evaluated at bid price : 20.02

Bid-YTW : 4.38 % |

| IFC.PR.C |

FixedReset |

-3.22 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.31

Bid-YTW : 5.44 % |

| IFC.PR.A |

FixedReset |

-2.96 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 17.71

Bid-YTW : 7.32 % |

| BAM.PR.X |

FixedReset |

-2.59 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-08-14

Maturity Price : 15.80

Evaluated at bid price : 15.80

Bid-YTW : 4.12 % |

| BAM.PR.R |

FixedReset |

-1.69 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-08-14

Maturity Price : 17.40

Evaluated at bid price : 17.40

Bid-YTW : 4.32 % |

| MFC.PR.F |

FixedReset |

-1.68 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 16.60

Bid-YTW : 7.05 % |

| BAM.PR.M |

Perpetual-Discount |

-1.50 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-08-14

Maturity Price : 21.03

Evaluated at bid price : 21.03

Bid-YTW : 5.73 % |

| FTS.PR.M |

FixedReset |

-1.33 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-08-14

Maturity Price : 22.34

Evaluated at bid price : 23.04

Bid-YTW : 3.53 % |

| FTS.PR.K |

FixedReset |

-1.32 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-08-14

Maturity Price : 20.18

Evaluated at bid price : 20.18

Bid-YTW : 3.59 % |

| TRP.PR.F |

FloatingReset |

-1.25 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-08-14

Maturity Price : 15.80

Evaluated at bid price : 15.80

Bid-YTW : 3.67 % |

| HSE.PR.A |

FixedReset |

-1.23 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-08-14

Maturity Price : 14.49

Evaluated at bid price : 14.49

Bid-YTW : 4.15 % |

| ENB.PR.D |

FixedReset |

-1.09 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-08-14

Maturity Price : 15.48

Evaluated at bid price : 15.48

Bid-YTW : 4.97 % |

| BAM.PF.C |

Perpetual-Discount |

-1.08 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-08-14

Maturity Price : 21.09

Evaluated at bid price : 21.09

Bid-YTW : 5.84 % |

| ENB.PR.B |

FixedReset |

-1.03 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-08-14

Maturity Price : 15.40

Evaluated at bid price : 15.40

Bid-YTW : 4.97 % |

| BAM.PR.K |

Floater |

1.04 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-08-14

Maturity Price : 12.60

Evaluated at bid price : 12.60

Bid-YTW : 3.78 % |

| RY.PR.O |

Perpetual-Discount |

1.12 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-08-14

Maturity Price : 24.01

Evaluated at bid price : 24.37

Bid-YTW : 5.06 % |

| SLF.PR.D |

Deemed-Retractible |

1.13 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.54

Bid-YTW : 6.55 % |

| ENB.PR.Y |

FixedReset |

1.21 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-08-14

Maturity Price : 16.70

Evaluated at bid price : 16.70

Bid-YTW : 4.75 % |

| HSE.PR.C |

FixedReset |

1.23 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-08-14

Maturity Price : 21.84

Evaluated at bid price : 22.25

Bid-YTW : 4.39 % |

| RY.PR.N |

Perpetual-Discount |

1.27 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-08-14

Maturity Price : 24.29

Evaluated at bid price : 24.66

Bid-YTW : 5.04 % |

| MFC.PR.C |

Deemed-Retractible |

1.29 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.75

Bid-YTW : 6.32 % |

| MFC.PR.L |

FixedReset |

1.32 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.50

Bid-YTW : 5.09 % |

| ENB.PR.P |

FixedReset |

1.48 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-08-14

Maturity Price : 16.44

Evaluated at bid price : 16.44

Bid-YTW : 4.93 % |

| ENB.PR.T |

FixedReset |

1.54 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-08-14

Maturity Price : 16.46

Evaluated at bid price : 16.46

Bid-YTW : 4.95 % |

| PWF.PR.S |

Perpetual-Discount |

1.88 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-08-14

Maturity Price : 22.41

Evaluated at bid price : 22.80

Bid-YTW : 5.29 % |

| Volume Highlights |

| Issue |

Index |

Shares

Traded |

Notes |

| TD.PR.Y |

FixedReset |

40,201 |

Scotia crossed 35,000 at 25.10.

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 25.06

Bid-YTW : 2.91 % |

| SLF.PR.H |

FixedReset |

33,836 |

Scotia crossed 26,900 at 20.20.

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.30

Bid-YTW : 5.53 % |

| TD.PF.F |

Perpetual-Discount |

29,831 |

Recent new issue.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-08-14

Maturity Price : 24.22

Evaluated at bid price : 24.59

Bid-YTW : 5.01 % |

| CU.PR.H |

Perpetual-Discount |

24,360 |

Recent new issue.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-08-14

Maturity Price : 23.48

Evaluated at bid price : 23.80

Bid-YTW : 5.54 % |

| ENB.PF.G |

FixedReset |

23,950 |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-08-14

Maturity Price : 17.87

Evaluated at bid price : 17.87

Bid-YTW : 4.98 % |

| BMO.PR.Z |

Perpetual-Discount |

21,490 |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-08-14

Maturity Price : 24.14

Evaluated at bid price : 24.51

Bid-YTW : 5.13 % |

| There were 19 other index-included issues trading in excess of 10,000 shares. |

| Wide Spread Highlights |

| Issue |

Index |

Quote Data and Yield Notes |

| VNR.PR.A |

FixedReset |

Quote: 20.02 – 21.60

Spot Rate : 1.5800

Average : 1.1142

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-08-14

Maturity Price : 20.02

Evaluated at bid price : 20.02

Bid-YTW : 4.38 % |

| TRP.PR.G |

FixedReset |

Quote: 22.40 – 23.45

Spot Rate : 1.0500

Average : 0.6783

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-08-14

Maturity Price : 21.90

Evaluated at bid price : 22.40

Bid-YTW : 3.97 % |

| IFC.PR.C |

FixedReset |

Quote: 21.31 – 22.05

Spot Rate : 0.7400

Average : 0.4278

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.31

Bid-YTW : 5.44 % |

| HSE.PR.G |

FixedReset |

Quote: 22.82 – 23.69

Spot Rate : 0.8700

Average : 0.6120

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-08-14

Maturity Price : 22.18

Evaluated at bid price : 22.82

Bid-YTW : 4.64 % |

| MFC.PR.F |

FixedReset |

Quote: 16.60 – 17.19

Spot Rate : 0.5900

Average : 0.3737

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 16.60

Bid-YTW : 7.05 % |

| IFC.PR.A |

FixedReset |

Quote: 17.71 – 18.10

Spot Rate : 0.3900

Average : 0.2250

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 17.71

Bid-YTW : 7.32 % |