So evidence is accumulating that the deterioration of the Treasury market is having an effect on corporate new issues (although some might say it’s the other way ’round):

News of a debt offering from Intel Corp. took Treasuries on a rollercoaster ride.

The swings Wednesday are the latest sign that corporate-bond offerings are driving bigger moves in U.S. government debt prices this year, as a historic wave of issuance competes with Treasuries for space in investors’ portfolios, according to strategists at Bank of America Corp. The trend has picked up as post-financial crisis regulations prompt dealers to step back from Treasury trading, which means smaller trades can move prices.

Click for big

When a corporate comes out, the underwriters will short sovereigns to hedge their interest-rate risk. Some of the initial buyers might do this as well to lock in the new issue concession prior to flipping the issue in the next little while. This was discussed on May 26; there may also be a little pop in price due to index-inclusion subsequent to the initial trading period, although attribution of pops due to these different effects might prove to be a little difficult!

At any rate, what this means is that hedging a sizable purchase of new issues corporates is going to be (a) more expensive and (b) less certain. Therefore the concessions will have to be higher than otherwise; therefore the issuer will have to eat extra costs when issuing bonds; therefore the market has become less efficient in transmitting capital from lenders to borrowers. But who cares? The important thing about markets is that Granny’s investment of $5,000 is priced fairly. If industry is crippled due to the necessity of accommodating Granny, it’s a small price to pay.

Speaking of borrowing, there is speculation that Canada’s books won’t be balanced this year:

The federal government is headed for a deficit this year, Parliament’s budget watchdog warns in a fresh assessment of finances that sows doubt about the Conservatives’ centrepiece pledge to balance the books in 2015 as well as about their credentials as economic managers.

The Parliamentary Budget Officer says calculations using the Bank of Canada’s latest economic forecast show that Ottawa is on track to dip into the red by about $1-billion in the 2015-16 fiscal year.

This bleaker prediction was immediately rejected by Prime Minister Stephen Harper’s government, which insists that Ottawa will avoid a deficit this year even after it doled out $3-billion in enriched child-care benefits this week

And speaking of operating losses:

Bombardier Inc.’s shares and bonds tumbled on concern that demand is weakening for business jets, a pillar of profit at a company struggling to develop its first commercial airliner.

The sell-off probably was triggered by comments Wednesday from an aviation-parts supplier, B/E Aerospace Inc. about softening buyer interest in large-cabin executive aircraft, said Benoit Poirier, a Desjardins Securities Inc. analyst.

…

Bombardier’s widely traded Class B shares sank 3.9 percent to C$1.72 at the close in Toronto, paring an earlier plunge of as much as 18 percent. The 6 percent bonds due October 2022 fell 4.8 percent to 79 cents on the dollar. They had traded above par value in January.

Amin Khoury, the executive chairman of B/E Aerospace Inc. of Florida, had told analysts on a conference call that “energy-producing companies and governments have put a damper on capital spending, which has negatively impacted business-jet sales. On a regional basis, new large-cabin business-jet demand has come under pressure as international markets that represented a significant source of demand have now become sellers, putting their used aircraft on the market, including China, Russia and Latin America.”

And the loonie got smacked:

The Canadian dollar ended the day at its lowest closing level in more than a decade as falling oil prices, which may have plunged the economy into recession in the first half of the year, resumed their descent.

The currency has been falling since last week when the Bank of Canada cut its benchmark interest rate and forecast two straight quarters of economic contraction, saying the hit from crude oil’s collapse was proving to be more severe than expected. Oil prices fell again Wednesday, with the North American benchmark trading below $50 per barrel.

…

The loonie, as the currency is known for the image of the aquatic bird on the C$1 coin, ended trading Wednesday at C$1.3033 per U.S. dollar, or 76.73 U.S cents, the lowest closing level for the currency since September 2004.

Which is good news for the tourist industry! I remember the glory days of the early 2000’s … in the evening, busses with US plates would be parked all over the theatre district … it was great!

And backtracking a bit and speaking of simple-minded trading strategies:

Buy when the stock market opens. Sell at the close. Repeat.

As far as trading strategies go, that’s about as simple as it gets. Turns out it’s also been a great way to make money in China, thanks to what analysts say is a pattern of afternoon equity purchases by state-backed funds.

When applied to the Shanghai Composite Index, the trading rule generated a 23 percent return since July 8, compared with 8 percent for a buy-and-hold approach. Use it on PetroChina Co., an obvious target of state support given the stock’s heavy weighting in benchmark indexes, and the difference is even starker: 43 percent versus 0.5 percent.

Late-day rallies are the latest quirk to emerge from an equity market where government intervention — from price ceilings on initial public offerings to bans on stake sales by major shareholders — has increased to unprecedented levels after a $4 trillion selloff.

Hat tip to Assiduous Reader JP for sending me this!

I see that New York is implementing a higher minimum wage – for fast food chains only:

A panel appointed by Gov. Andrew M. Cuomo recommended on Wednesday that the minimum wage be raised for employees of fast-food chain restaurants throughout the state to $15 an hour over the next few years. Wages would be raised faster in New York City than in the rest of the state to account for the higher cost of living there.

I can’t think of any sensible rationale for carving out fast-food chains from the rest of the economy.

I support a higher (across the board) minimum wage for precisely the reason that jobs will be lost – although if I were king, implementation would be delayed until the economy started looking a little better.

Low wages encourage low-skill industries; increasing the minimum wage will encourage automation as discussed October 15, 2013.

It is not redistribution that makes us rich; productivity makes us rich.

Westcoast Energy Inc., proud issuer of W.PR.H and W.PR.J, has been confirmed at Pfd-2(low) by DBRS:

DBRS Limited (DBRS) has today confirmed the Issuer Rating and Unsecured Debentures rating of Westcoast Energy Inc. (Westcoast or the Company) at A (low) as well as its Commercial Paper rating at R-1 (low) and First Preferred Shares rating at Pfd-2 (low). All trends are Stable. The rating confirmations reflect Westcoast’s strong business risk profile supported by low-risk regulated or fee-for-service operations accounting for nearly 95% of the Company’s earnings and provide downside protection from the current low commodity price environment. The Company’s financial profile remained reasonable for the current rating category.

It was a mixed day for the Canadian preferred share market, with PerpetualDiscounts off 13bp, FixedResets down 16bp and DeemedRetractibles gaining 6bp. The Performance Highlights table is its usual lively self. Volume was average.

PerpetualDiscounts now yield 5.29%, equivalent to 6.88% interest at the standard equivalency factor of 1.3x. Long corporates now yield 4.02%, so the pre-tax interest-equivalent spread (in this context, the “Seniority Spread”) is now about 285bp, a slight (and perhaps spurious) narrowing from the 290bp reported July 15.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

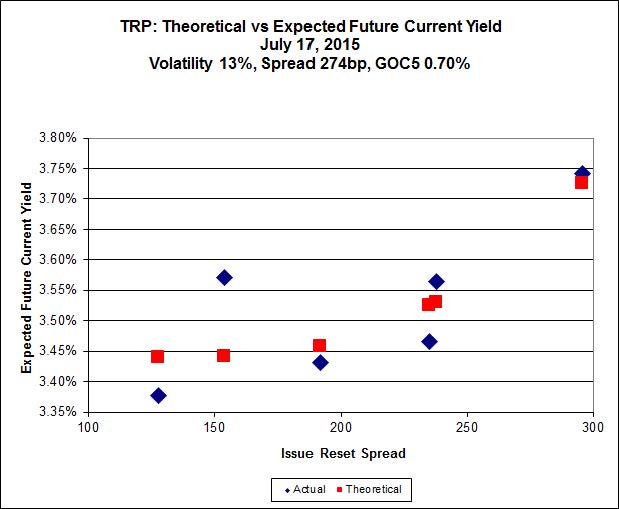

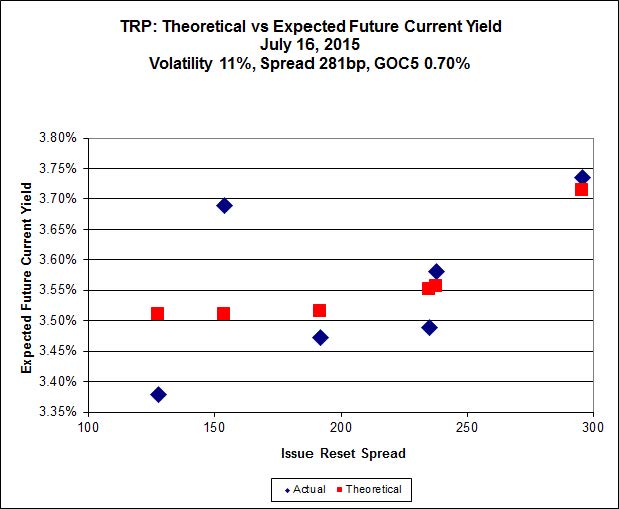

Here’s TRP:

Click for Big

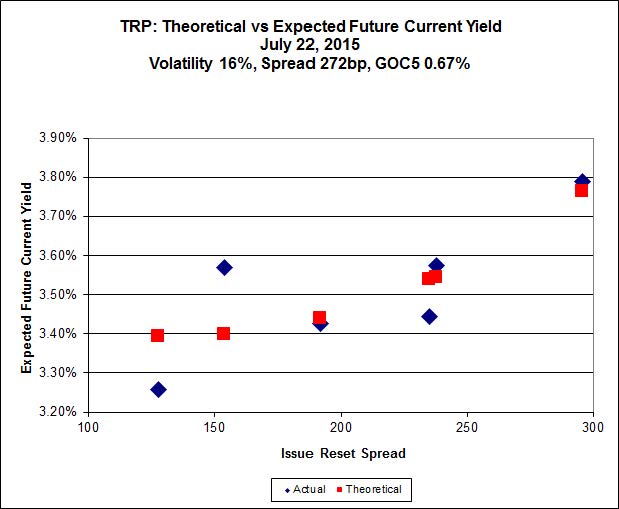

TRP.PR.B, which resets 2020-6-30 at +128, is bid at 14.97 to be $0.60 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $0.77 cheap at its bid price of 15.50.

Click for Big

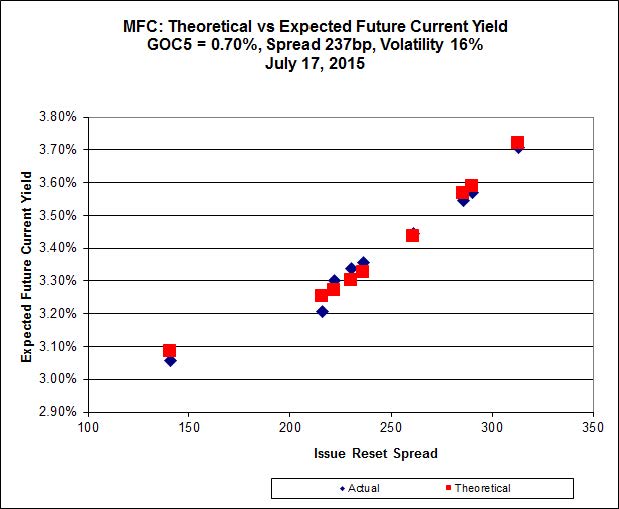

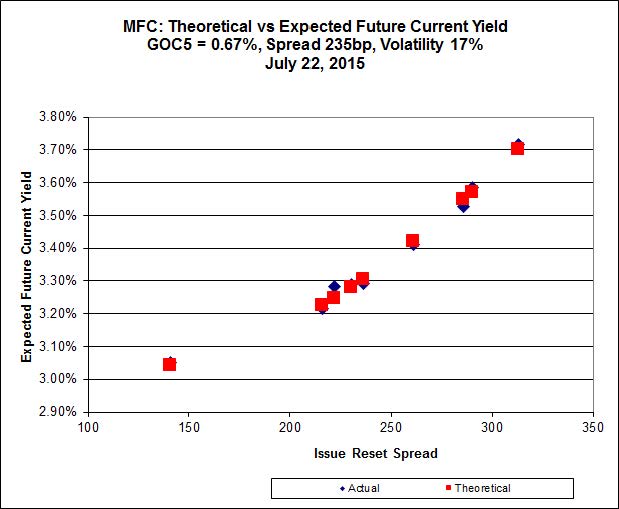

Another good fit today!

Most expensive is MFC.PR.I, resetting at +286bp on 2017-9-19, bid at 25.03 to be $0.17 rich, while MFC.PR.K, resetting at +222bp on 2018-9-19, is bid at 22.00 to be $0.25 cheap.

Click for Big

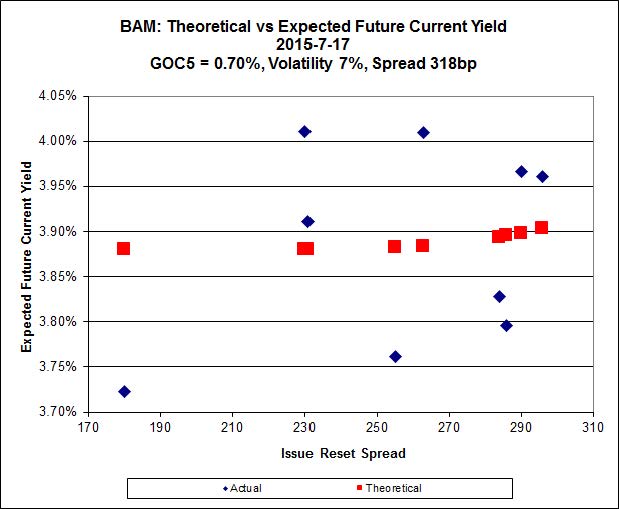

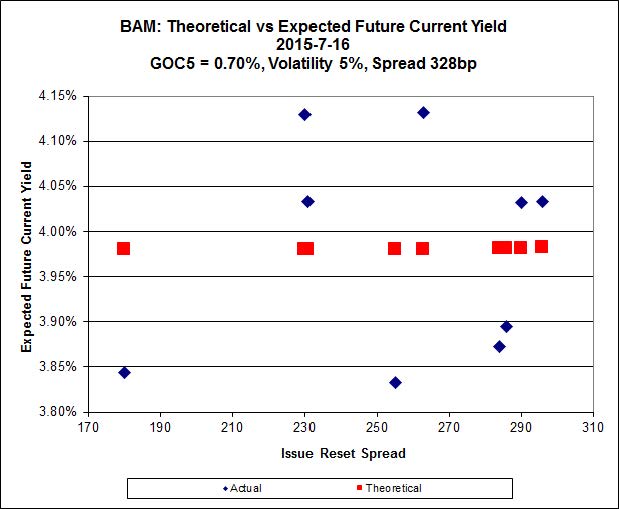

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-06-30, bid at 18.38 to be $1.05 cheap. BAM.PR.X, resetting at +180bp on 2017-6-30 is bid at 17.20 and appears to be $1.04 rich.

Click for Big

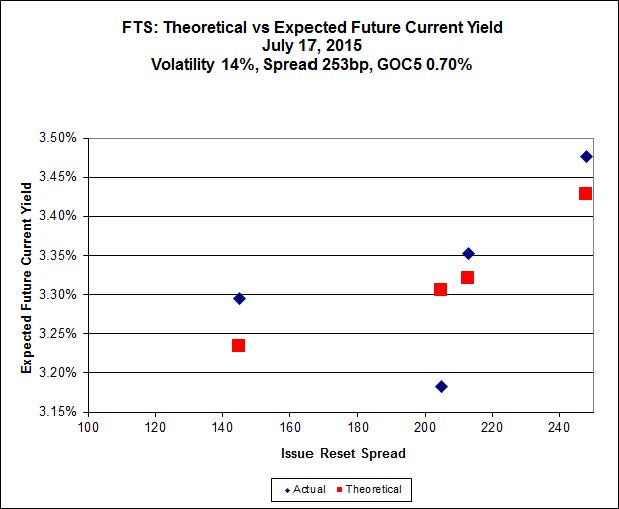

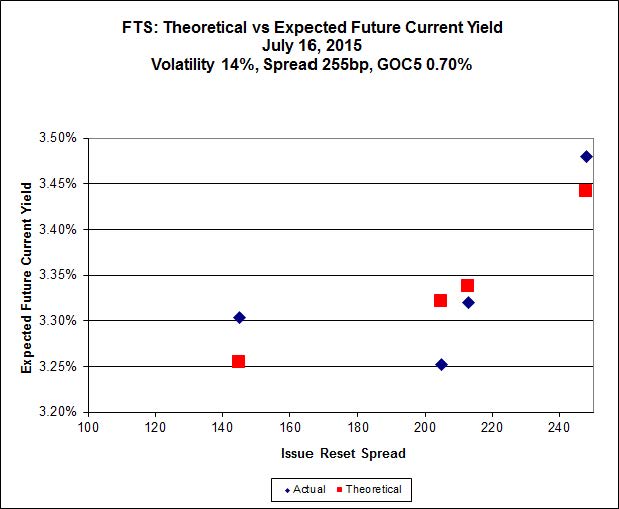

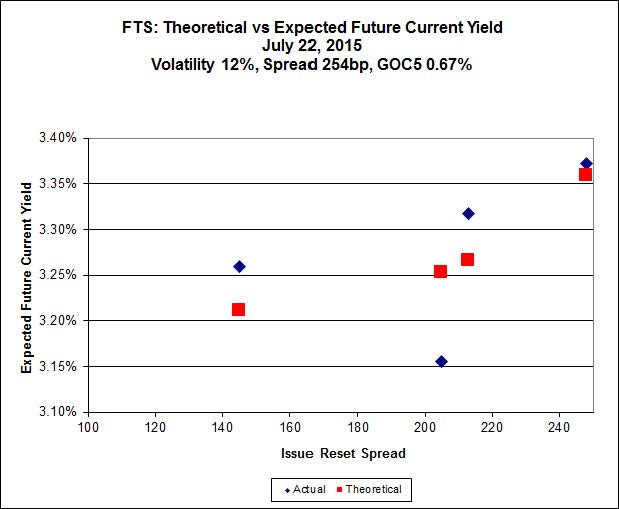

FTS.PR.K, with a spread of +205bp, and bid at 21.55, looks $0.65 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 21.10 and is $0.34 cheap.

Click for Big

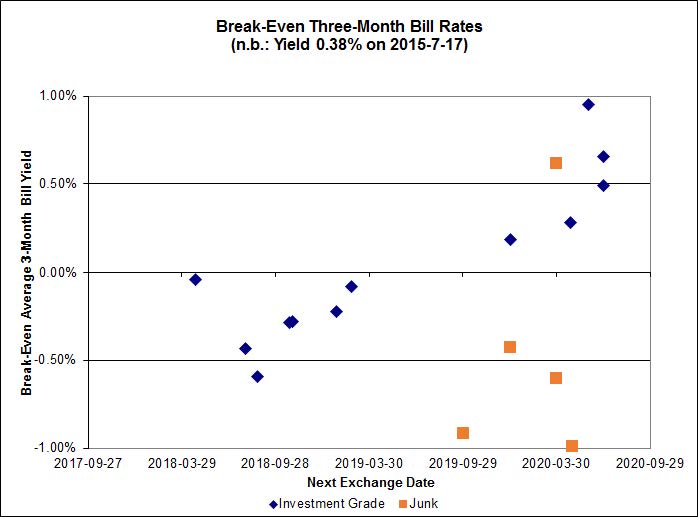

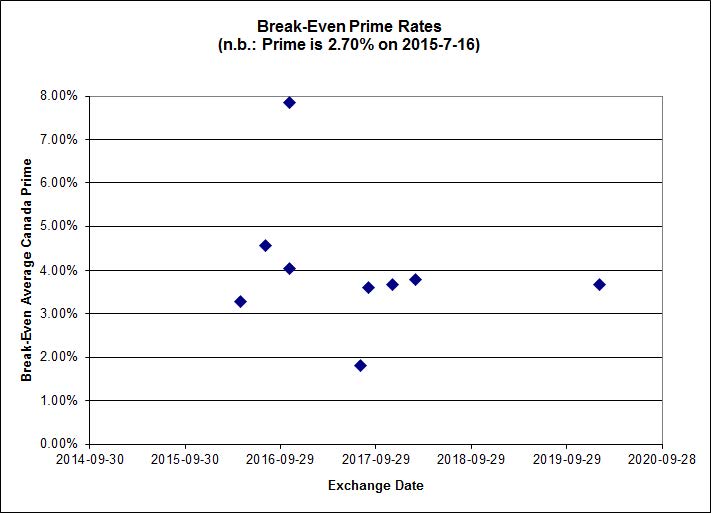

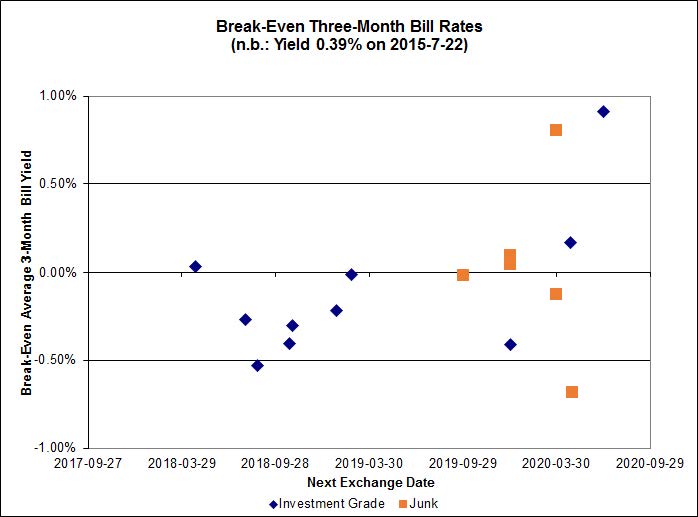

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of 0.09%, with two outliers above 1.00%. There are no junk outliers.

Click for Big

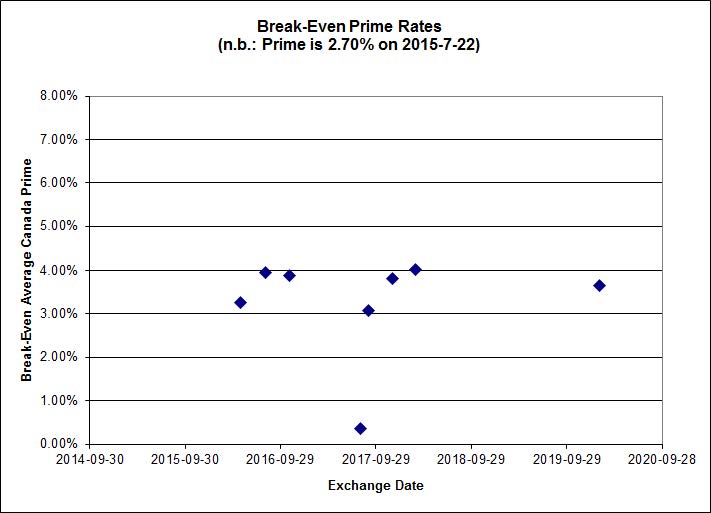

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 1.1824 % | 2,081.8 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 1.1824 % | 3,639.9 |

| Floater | 3.52 % | 3.58 % | 61,760 | 18.35 | 3 | 1.1824 % | 2,213.1 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0671 % | 2,770.0 |

| SplitShare | 4.59 % | 4.95 % | 64,433 | 3.19 | 3 | 0.0671 % | 3,246.2 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0671 % | 2,532.8 |

| Perpetual-Premium | 5.52 % | 4.96 % | 73,554 | 2.27 | 13 | -0.0152 % | 2,509.9 |

| Perpetual-Discount | 5.32 % | 5.29 % | 93,931 | 14.91 | 23 | -0.1319 % | 2,672.8 |

| FixedReset | 4.62 % | 3.75 % | 218,681 | 16.12 | 88 | -0.1589 % | 2,276.6 |

| Deemed-Retractible | 5.03 % | 4.90 % | 111,852 | 3.30 | 34 | 0.0648 % | 2,614.8 |

| FloatingReset | 2.36 % | 3.05 % | 44,529 | 6.07 | 10 | 0.1320 % | 2,283.1 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| CM.PR.Q | FixedReset | -2.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-22 Maturity Price : 22.78 Evaluated at bid price : 24.02 Bid-YTW : 3.58 % |

| SLF.PR.H | FixedReset | -2.10 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.54 Bid-YTW : 6.12 % |

| HSE.PR.C | FixedReset | -1.88 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-22 Maturity Price : 21.95 Evaluated at bid price : 22.42 Bid-YTW : 4.46 % |

| TRP.PR.E | FixedReset | -1.70 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-22 Maturity Price : 21.61 Evaluated at bid price : 21.92 Bid-YTW : 3.75 % |

| HSE.PR.G | FixedReset | -1.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-22 Maturity Price : 22.47 Evaluated at bid price : 23.35 Bid-YTW : 4.62 % |

| BAM.PR.R | FixedReset | -1.61 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-22 Maturity Price : 18.38 Evaluated at bid price : 18.38 Bid-YTW : 4.26 % |

| IFC.PR.A | FixedReset | -1.58 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.07 Bid-YTW : 7.12 % |

| FTS.PR.J | Perpetual-Discount | -1.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-22 Maturity Price : 23.51 Evaluated at bid price : 23.90 Bid-YTW : 5.02 % |

| TRP.PR.F | FloatingReset | -1.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-22 Maturity Price : 17.26 Evaluated at bid price : 17.26 Bid-YTW : 3.35 % |

| TRP.PR.D | FixedReset | -1.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-22 Maturity Price : 21.33 Evaluated at bid price : 21.33 Bid-YTW : 3.82 % |

| BNS.PR.Y | FixedReset | -1.15 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.26 Bid-YTW : 3.69 % |

| BAM.PF.C | Perpetual-Discount | -1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-22 Maturity Price : 21.03 Evaluated at bid price : 21.03 Bid-YTW : 5.83 % |

| MFC.PR.J | FixedReset | -1.07 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.05 Bid-YTW : 4.06 % |

| BAM.PR.Z | FixedReset | -1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-22 Maturity Price : 22.67 Evaluated at bid price : 23.26 Bid-YTW : 4.09 % |

| ENB.PR.B | FixedReset | -1.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-22 Maturity Price : 16.63 Evaluated at bid price : 16.63 Bid-YTW : 4.88 % |

| BAM.PR.K | Floater | 1.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-22 Maturity Price : 13.30 Evaluated at bid price : 13.30 Bid-YTW : 3.58 % |

| FTS.PR.F | Perpetual-Discount | 1.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-22 Maturity Price : 23.98 Evaluated at bid price : 24.26 Bid-YTW : 5.11 % |

| TRP.PR.C | FixedReset | 1.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-22 Maturity Price : 15.48 Evaluated at bid price : 15.48 Bid-YTW : 3.69 % |

| NA.PR.S | FixedReset | 1.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-22 Maturity Price : 22.80 Evaluated at bid price : 23.85 Bid-YTW : 3.35 % |

| FTS.PR.M | FixedReset | 1.52 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-22 Maturity Price : 22.51 Evaluated at bid price : 23.35 Bid-YTW : 3.59 % |

| SLF.PR.J | FloatingReset | 1.53 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.60 Bid-YTW : 6.63 % |

| HSE.PR.A | FixedReset | 1.75 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-22 Maturity Price : 16.28 Evaluated at bid price : 16.28 Bid-YTW : 3.90 % |

| TRP.PR.B | FixedReset | 1.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-22 Maturity Price : 14.97 Evaluated at bid price : 14.97 Bid-YTW : 3.40 % |

| RY.PR.J | FixedReset | 2.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-22 Maturity Price : 23.00 Evaluated at bid price : 24.53 Bid-YTW : 3.47 % |

| PWF.PR.P | FixedReset | 2.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-22 Maturity Price : 16.90 Evaluated at bid price : 16.90 Bid-YTW : 3.47 % |

| BAM.PR.B | Floater | 2.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-22 Maturity Price : 13.82 Evaluated at bid price : 13.82 Bid-YTW : 3.44 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| RY.PR.O | Perpetual-Discount | 254,478 | New issue settled today. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-22 Maturity Price : 24.20 Evaluated at bid price : 24.57 Bid-YTW : 4.99 % |

| BNS.PR.Z | FixedReset | 144,280 | RBC crossed 100,000 at 22.75. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.70 Bid-YTW : 3.84 % |

| RY.PR.F | Deemed-Retractible | 117,800 | TD crossed blocks of 55,000 and 50,000, both at 25.30. YTW SCENARIO Maturity Type : Call Maturity Date : 2016-05-24 Maturity Price : 25.00 Evaluated at bid price : 25.30 Bid-YTW : 3.85 % |

| RY.PR.A | Deemed-Retractible | 111,756 | RBC crossed 99,100 at 25.15. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.16 Bid-YTW : 4.49 % |

| RY.PR.B | Deemed-Retractible | 108,316 | Scotia crossed 80,000 at 25.22. National sold 10,000 each to Nesbitt and TD, both at 25.22. YTW SCENARIO Maturity Type : Call Maturity Date : 2015-08-24 Maturity Price : 25.00 Evaluated at bid price : 25.24 Bid-YTW : 2.47 % |

| TD.PF.E | FixedReset | 104,050 | RBC crossed 50,000 at 24.90. TD crossed 50,000 at the same price. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-22 Maturity Price : 23.11 Evaluated at bid price : 24.90 Bid-YTW : 3.49 % |

| There were 30 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| IFC.PR.A | FixedReset | Quote: 18.07 – 18.83 Spot Rate : 0.7600 Average : 0.5419 YTW SCENARIO |

| SLF.PR.H | FixedReset | Quote: 19.54 – 20.07 Spot Rate : 0.5300 Average : 0.3513 YTW SCENARIO |

| FTS.PR.J | Perpetual-Discount | Quote: 23.90 – 24.39 Spot Rate : 0.4900 Average : 0.3528 YTW SCENARIO |

| BAM.PF.E | FixedReset | Quote: 22.00 – 22.45 Spot Rate : 0.4500 Average : 0.3186 YTW SCENARIO |

| BAM.PR.R | FixedReset | Quote: 18.38 – 18.79 Spot Rate : 0.4100 Average : 0.2843 YTW SCENARIO |

| CM.PR.Q | FixedReset | Quote: 24.02 – 24.45 Spot Rate : 0.4300 Average : 0.3158 YTW SCENARIO |