The treasury curve flattened today:

Enough distractions! Treasury investors are turning their attention back to the business of when U.S. interest rates go up.

The yield curve has flattened the most in four months in a week when Greece signed a deal to secure more bailout aid and a bear-market rout in Chinese stocks stabilized, allaying concern that turmoil abroad would delay the Federal Reserve’s first rate increase since 2006. Fed Chair Janet Yellen made it plain over two days of testimony before Congress this week that she believes the central bank can raise interest rates in 2015.

…

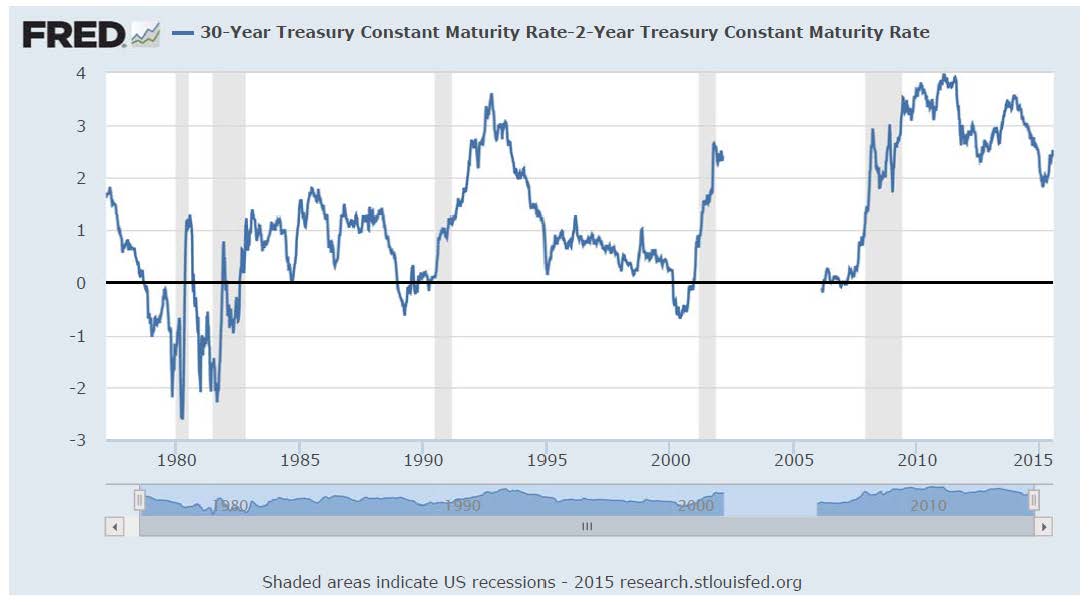

The difference between yields on two- and 30-year government debt has narrowed 9.4 percentage points this week to 246 basis points. It reached 244 basis points Thursday, the least since July 9.

Yellen’s testimony preached restraint:

Speaking Thursday before the Senate Banking Committee, Yellen said that raising rates prematurely could derail the recovery. Waiting too long, on the other hand, might force the Fed to tighten at a faster pace to keep the economy from overheating.

“My own preference would be to be able proceed to tighten in a prudent and gradual manner,” she said.

Yellen’s comments this week were consistent with her often-stated advice to investors: the date of liftoff matters less than the subsequent pace of increases. And she has assured them that those increases would be measured.

The concern that tightening prematurely could throw the recovery off track is one reason why the federal funds rate has been kept near zero as long it has, Yellen said.

“We also want to be careful not to tighten too late because, if we do that, arguably we could overshoot both of our goals and be faced with this situation where we would then need to tighten monetary policy in a very sharp way that could be disruptive,” she told lawmakers.

…

Yellen offered other reasons for an upbeat assessment of the economy in her testimony Thursday. She said the job market is returning to a “more normal state,” even though the 5.3 percent unemployment rate understates the degree of slack. And she expects to see further gains in wages.Fed officials say they will let the latest data on employment and inflation guide their decision on when to raise rates. To drive the point home, the San Francisco Fed has printed T-shirts with the message: “Monetary Policy — It’s Data Dependent.”

Only in America would the central bank print t-shirts!

By way of context, here’s the historical 2-year and 30-year Treasury yields from FRED:

Click for Big

and the spread between the two:

Click for Big

Note that there’s a gap in the 30-year series during the period in which they didn’t exist. That was the peace dividend.

And there’s more squabbling over the ORPP:

Ottawa is putting Queen’s Park on notice that it will not help set up a provincial pension plan.

Finance Minister Joe Oliver wrote to his provincial counterpart on Thursday afternoon saying that Ottawa would not help collect contributions or make the legislative changes the province would likely require.

“The Ontario Government’s proposed [plan] would take money from workers and their families, kill jobs, and damage the economy,” Mr. Oliver wrote in the letter, which was obtained by The Globe and Mail.

“Furthermore, it would impose a one-size-fits-all scheme on Ontarians and their families, without consideration for their age, family situation or financial circumstance.”

…

According to Mr. Oliver’s letter, Ontario officials have approached federal civil servants in recent months to discuss the possibility of having the federal government involved in the administration of the new provincial plan.“We will not assist the Ontario government in the implementation of the ORPP,” Mr. Oliver wrote to Ontario Finance Minister Charles Sousa.

“This includes any legislative changes to allow the ORPP to be treated like the Canada Pension Plan for tax purposes, or to integrate the ORPP within the [registered retirement savings plan] contribution limits. Administration of the ORPP will be the sole responsibility of the Ontario Government, including the collection of contributions and any required information. We will be pleased to discuss with the Ontario Government the potential for voluntary contributions to the CPP, which we believe would better serve the interests of Ontarians and all Canadians.”

DBRS kept the ratings of the Big-6 banks’ senior debt on Trend-Negative today, confirming their conclusion reported in May:

Preferred share ratings and trends are unaffected.

It was a different sort of day for preferreds than it has been lately. In fact…

Click for Big

It was a superb day for the Canadian preferred share market, with PerpetualDiscounts gaining 43bp, FixedResets up 86bp and DeemedRetractibles off 7bp. The Performance Highlights table was fairly lengthy, but shorter than I expected given the overall index numbers. Volume was very high.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

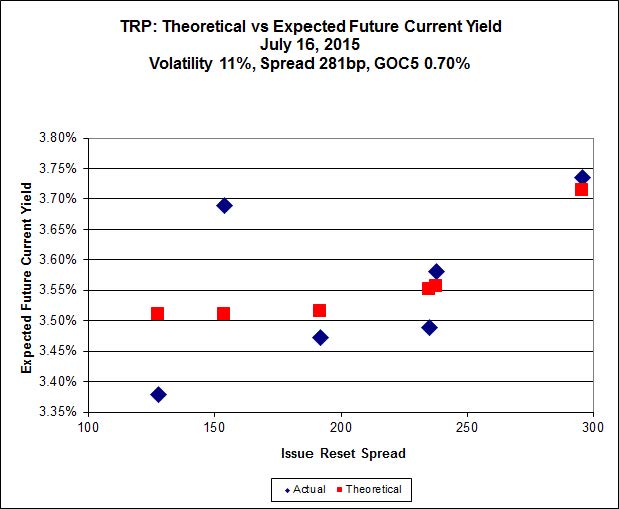

Here’s TRP:

Click for Big

TRP.PR.B, which resets 2020-6-30 at +128, is bid at 14.65 to be $0.55 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $0.77 cheap at its bid price of 15.20.

Most expensive is MFC.PR.F, resetting at +141bp on 2016-6-19, bid at 17.10 to be $0.82 rich, while MFC.PR.N, resetting at +230bp on 2020-3-19, is bid at 21.43 to be $0.57 cheap.

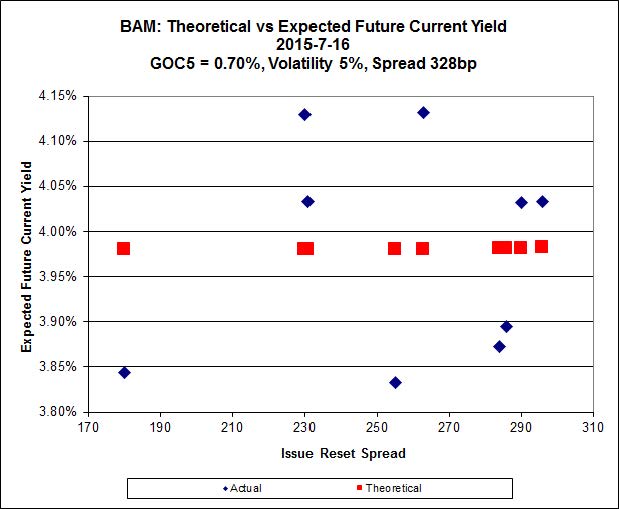

Click for Big

The cheapest issue relative to its peers is BAM.PF.B, resetting at +263bp on 2019-3-31, bid at 20.15 to be $0.77 cheap. BAM.PF.E, resetting at +255bp on 2020-3-31 is bid at 21.20 and appears to be $0.79 rich.

Click for Big

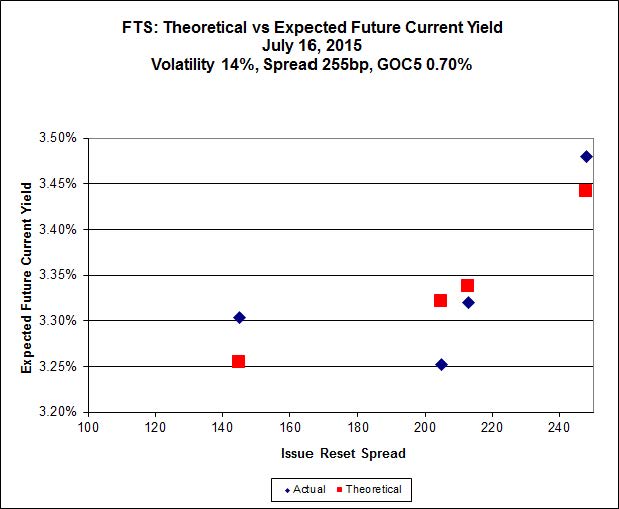

FTS.PR.K, with a spread of +205bp, and bid at 21.14, looks $0.44 expensive and resets 2019-3-1. FTS.PR.M, with a spread of +248bp and resetting 2019-12-1, is bid at 22.85 and is $0.25 cheap.

Click for Big

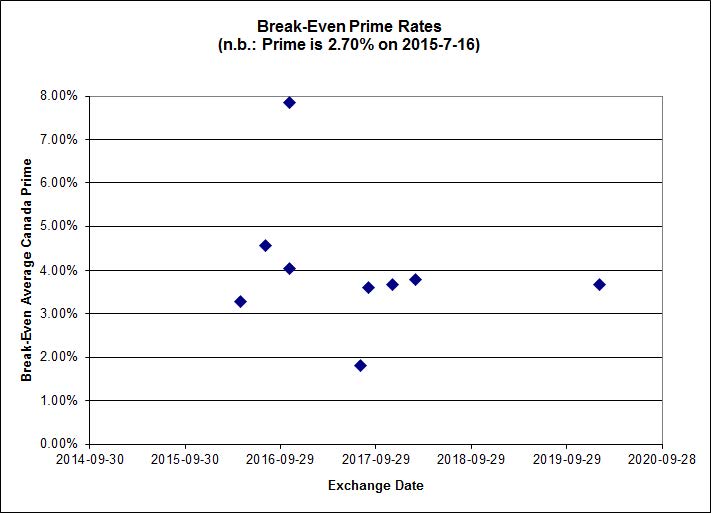

There is only one outlier; one of the junk pairs is below -1.00%.

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of 0.01% (which seems a little extreme!).

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0503 % | 2,056.9 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0503 % | 3,596.5 |

| Floater | 3.57 % | 3.61 % | 61,454 | 18.29 | 3 | -0.0503 % | 2,186.7 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.4975 % | 2,776.3 |

| SplitShare | 4.58 % | 4.83 % | 68,287 | 3.20 | 3 | 0.4975 % | 3,253.6 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.4975 % | 2,538.6 |

| Perpetual-Premium | 5.51 % | 2.77 % | 74,115 | 0.29 | 13 | 0.0640 % | 2,513.0 |

| Perpetual-Discount | 5.41 % | 5.38 % | 88,640 | 14.87 | 21 | 0.4303 % | 2,648.3 |

| FixedReset | 4.66 % | 3.84 % | 218,979 | 16.05 | 88 | 0.8061 % | 2,254.9 |

| Deemed-Retractible | 5.05 % | 4.98 % | 110,268 | 3.32 | 34 | -0.0661 % | 2,607.5 |

| FloatingReset | 2.54 % | 3.12 % | 49,205 | 6.06 | 10 | -0.2981 % | 2,264.0 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| TRP.PR.F | FloatingReset | -7.10 % | Technically this is real, since the low for the day was, in fact, 17.00. On the other hand, that was one trade, for 100 shares, at 3:54pm, when the trade immediately before it was done at 17.91 which was the low for the day for two minutes before being superseded. At one point, I know, there was no bid for the issue, which tells me first that the market maker is incompetent and second that nobody in all of Canada is running an algorithm to make a market arbitraging this issue against its Strong Pair TRP.PR.A. The day’s volume was 3,900 shares in a range of 17.00-18.41, and the VWAP was 18.272821. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-16 Maturity Price : 17.00 Evaluated at bid price : 17.00 Bid-YTW : 3.61 % |

| CIU.PR.C | FixedReset | -3.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-16 Maturity Price : 15.70 Evaluated at bid price : 15.70 Bid-YTW : 3.59 % |

| BNS.PR.D | FloatingReset | -1.80 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.24 Bid-YTW : 4.11 % |

| VNR.PR.A | FixedReset | -1.47 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-16 Maturity Price : 21.46 Evaluated at bid price : 21.46 Bid-YTW : 4.33 % |

| HSB.PR.C | Deemed-Retractible | -1.03 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.00 Bid-YTW : 5.17 % |

| SLF.PR.H | FixedReset | 1.11 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.08 Bid-YTW : 5.86 % |

| CU.PR.G | Perpetual-Discount | 1.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-16 Maturity Price : 21.87 Evaluated at bid price : 22.17 Bid-YTW : 5.13 % |

| BNS.PR.B | FloatingReset | 1.20 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.67 Bid-YTW : 3.04 % |

| BAM.PF.C | Perpetual-Discount | 1.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-16 Maturity Price : 20.50 Evaluated at bid price : 20.50 Bid-YTW : 5.98 % |

| BAM.PR.K | Floater | 1.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-16 Maturity Price : 13.18 Evaluated at bid price : 13.18 Bid-YTW : 3.61 % |

| RY.PR.M | FixedReset | 1.42 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-16 Maturity Price : 22.90 Evaluated at bid price : 24.35 Bid-YTW : 3.53 % |

| BAM.PR.R | FixedReset | 1.45 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-16 Maturity Price : 18.16 Evaluated at bid price : 18.16 Bid-YTW : 4.45 % |

| BAM.PF.B | FixedReset | 1.51 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-16 Maturity Price : 20.15 Evaluated at bid price : 20.15 Bid-YTW : 4.49 % |

| CM.PR.O | FixedReset | 1.58 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-16 Maturity Price : 22.02 Evaluated at bid price : 22.49 Bid-YTW : 3.62 % |

| BAM.PF.A | FixedReset | 1.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-16 Maturity Price : 21.97 Evaluated at bid price : 22.32 Bid-YTW : 4.30 % |

| BAM.PR.M | Perpetual-Discount | 1.61 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-16 Maturity Price : 20.16 Evaluated at bid price : 20.16 Bid-YTW : 5.95 % |

| TD.PF.C | FixedReset | 1.62 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-16 Maturity Price : 21.66 Evaluated at bid price : 22.00 Bid-YTW : 3.62 % |

| BAM.PR.N | Perpetual-Discount | 1.66 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-16 Maturity Price : 20.18 Evaluated at bid price : 20.18 Bid-YTW : 5.95 % |

| BAM.PR.X | FixedReset | 1.75 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-16 Maturity Price : 16.26 Evaluated at bid price : 16.26 Bid-YTW : 4.34 % |

| BMO.PR.W | FixedReset | 1.85 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-16 Maturity Price : 21.67 Evaluated at bid price : 22.00 Bid-YTW : 3.64 % |

| BMO.PR.T | FixedReset | 1.86 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-16 Maturity Price : 21.97 Evaluated at bid price : 22.42 Bid-YTW : 3.59 % |

| HSE.PR.G | FixedReset | 1.89 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-16 Maturity Price : 22.67 Evaluated at bid price : 23.75 Bid-YTW : 4.60 % |

| TD.PF.B | FixedReset | 1.90 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-16 Maturity Price : 21.67 Evaluated at bid price : 21.98 Bid-YTW : 3.64 % |

| ENB.PR.N | FixedReset | 1.90 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-16 Maturity Price : 17.68 Evaluated at bid price : 17.68 Bid-YTW : 5.10 % |

| SLF.PR.J | FloatingReset | 1.91 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.00 Bid-YTW : 7.24 % |

| BAM.PF.G | FixedReset | 1.96 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-16 Maturity Price : 22.19 Evaluated at bid price : 22.85 Bid-YTW : 4.20 % |

| BMO.PR.S | FixedReset | 2.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-16 Maturity Price : 22.30 Evaluated at bid price : 22.91 Bid-YTW : 3.59 % |

| MFC.PR.J | FixedReset | 2.17 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.50 Bid-YTW : 4.42 % |

| RY.PR.H | FixedReset | 2.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-16 Maturity Price : 21.86 Evaluated at bid price : 22.25 Bid-YTW : 3.64 % |

| ENB.PR.J | FixedReset | 2.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-16 Maturity Price : 18.26 Evaluated at bid price : 18.26 Bid-YTW : 4.97 % |

| CM.PR.P | FixedReset | 2.42 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-16 Maturity Price : 21.67 Evaluated at bid price : 22.02 Bid-YTW : 3.62 % |

| RY.PR.Z | FixedReset | 2.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-16 Maturity Price : 22.20 Evaluated at bid price : 22.74 Bid-YTW : 3.51 % |

| BAM.PF.F | FixedReset | 2.47 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-16 Maturity Price : 22.24 Evaluated at bid price : 22.85 Bid-YTW : 4.19 % |

| MFC.PR.K | FixedReset | 2.57 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.12 Bid-YTW : 5.48 % |

| NA.PR.W | FixedReset | 2.61 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-16 Maturity Price : 21.35 Evaluated at bid price : 21.65 Bid-YTW : 3.71 % |

| ENB.PF.G | FixedReset | 2.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-16 Maturity Price : 19.20 Evaluated at bid price : 19.20 Bid-YTW : 4.94 % |

| NA.PR.S | FixedReset | 2.79 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-16 Maturity Price : 22.66 Evaluated at bid price : 23.56 Bid-YTW : 3.49 % |

| GWO.PR.N | FixedReset | 2.90 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.99 Bid-YTW : 7.64 % |

| ENB.PR.T | FixedReset | 2.91 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-16 Maturity Price : 17.70 Evaluated at bid price : 17.70 Bid-YTW : 4.95 % |

| TD.PF.A | FixedReset | 3.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-16 Maturity Price : 21.85 Evaluated at bid price : 22.25 Bid-YTW : 3.59 % |

| BAM.PR.Z | FixedReset | 3.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-16 Maturity Price : 22.30 Evaluated at bid price : 22.69 Bid-YTW : 4.31 % |

| ENB.PR.Y | FixedReset | 3.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-16 Maturity Price : 17.31 Evaluated at bid price : 17.31 Bid-YTW : 4.94 % |

| HSE.PR.E | FixedReset | 4.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-16 Maturity Price : 22.77 Evaluated at bid price : 23.95 Bid-YTW : 4.56 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| PWF.PR.T | FixedReset | 64,136 | Desjardins crossed 15,000 at 24.60; TD crossed 44,800 at the same price. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-16 Maturity Price : 23.12 Evaluated at bid price : 24.50 Bid-YTW : 3.30 % |

| BNS.PR.M | Deemed-Retractible | 55,162 | TD crossed 52,000 at 25.20. YTW SCENARIO Maturity Type : Call Maturity Date : 2016-07-27 Maturity Price : 25.00 Evaluated at bid price : 25.17 Bid-YTW : 3.65 % |

| TD.PF.C | FixedReset | 47,952 | TD crossed 20,000 at 21.75. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-16 Maturity Price : 21.66 Evaluated at bid price : 22.00 Bid-YTW : 3.62 % |

| ENB.PR.B | FixedReset | 40,209 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-16 Maturity Price : 16.22 Evaluated at bid price : 16.22 Bid-YTW : 5.14 % |

| RY.PR.I | FixedReset | 34,895 | Scotia crossed 15,000 at 25.17. Nesbitt crossed 15,000 at 25.18. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.18 Bid-YTW : 3.15 % |

| NA.PR.S | FixedReset | 34,867 | Desjardins crossed 25,000 at 23.50. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-16 Maturity Price : 22.66 Evaluated at bid price : 23.56 Bid-YTW : 3.49 % |

| There were 53 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| ENB.PR.P | FixedReset | Quote: 17.31 – 18.19 Spot Rate : 0.8800 Average : 0.5277 YTW SCENARIO |

| TRP.PR.F | FloatingReset | Quote: 17.00 – 17.83 Spot Rate : 0.8300 Average : 0.5397 YTW SCENARIO |

| IFC.PR.A | FixedReset | Quote: 18.01 – 19.00 Spot Rate : 0.9900 Average : 0.7250 YTW SCENARIO |

| CIU.PR.C | FixedReset | Quote: 15.70 – 16.74 Spot Rate : 1.0400 Average : 0.7837 YTW SCENARIO |

| NA.PR.W | FixedReset | Quote: 21.65 – 22.40 Spot Rate : 0.7500 Average : 0.5259 YTW SCENARIO |

| ENB.PF.A | FixedReset | Quote: 18.63 – 19.35 Spot Rate : 0.7200 Average : 0.5205 YTW SCENARIO |