The hot news of the day is the FOMC Statement:

Information received since the Federal Open Market Committee met in October suggests that economic activity has been expanding at a moderate pace. Household spending and business fixed investment have been increasing at solid rates in recent months, and the housing sector has improved further; however, net exports have been soft. A range of recent labor market indicators, including ongoing job gains and declining unemployment, shows further improvement and confirms that underutilization of labor resources has diminished appreciably since early this year. Inflation has continued to run below the Committee’s 2 percent longer-run objective, partly reflecting declines in energy prices and in prices of non-energy imports. Market-based measures of inflation compensation remain low; some survey-based measures of longer-term inflation expectations have edged down.

…

Overall, taking into account domestic and international developments, the Committee sees the risks to the outlook for both economic activity and the labor market as balanced. Inflation is expected to rise to 2 percent over the medium term as the transitory effects of declines in energy and import prices dissipate and the labor market strengthens further. The Committee continues to monitor inflation developments closely.The Committee judges that there has been considerable improvement in labor market conditions this year, and it is reasonably confident that inflation will rise, over the medium term, to its 2 percent objective. Given the economic outlook, and recognizing the time it takes for policy actions to affect future economic outcomes, the Committee decided to raise the target range for the federal funds rate to 1/4 to 1/2 percent. The stance of monetary policy remains accommodative after this increase, thereby supporting further improvement in labor market conditions and a return to 2 percent inflation.

…

The Committee expects that economic conditions will evolve in a manner that will warrant only gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.

There were no dissents. The move was met with cheers:

“Americans should realize that the Fed’s decision today reflects our confidence in the U.S. economy,” Yellen said. “While things may be uneven across regions of the country and different industrial sectors, we see an economy that is on a path of sustainable improvement.”

Equity prices rallied in response, with the Standard & Poor’s 500 Index of U.S. stocks rising 1.5 percent to 2,073.07 in New York. Bond prices fell on the prospects of higher short-term interest rates, though yields on the benchmark 10-year Treasury note remained below levels seen last month.

…

Policy makers forecast that the short-term policy rate will rise to 1.375 percent at the end of 2016, implying four quarter-point increases in the target range next year, based on the median number from 17 officials.“I do want to emphasize that while we have said gradual, gradual does not mean mechanical — evenly timed, equally sized, interest-rate changes,” she said. “As the outlook evolves, we’ll respond appropriately. I strongly doubt that it will mean equally spaced hikes,” she added.

The Fed will be able to take such an approach because inflation is so far below its 2 percent goal. As measured by the personal consumption expenditure price index, it rose by 0.2 percent in the 12 months through October.

Shaw Communications Inc. is finally poised to enter the wireless business, with a $1.6-billion deal to buy Toronto startup carrier Wind Mobile Corp.

Calgary-based cable operator Shaw announced the transaction on Wednesday evening, noting that while the deal still requires approval from the federal government and the Competition Bureau, it expects it to close during the third quarter of fiscal 2016 (the first half of the calendar year).

Wind, which operates in urban areas in Ontario, British Columbia and Alberta, has 940,000 subscribers, and Shaw said the small carrier is expected to generate $485-million in revenue and $65-million in earnings before interest, taxes, depreciation and amortization (EBITDA) in 2015.

…

Wind has provided a lower-priced alternative to Canada’s Big Three carriers – Telus, BCE Inc. and Rogers Communications Inc. – and consumers will be wondering whether that will evaporate with this sale.[Shaw CEO] Mr. [Brad] Shaw said as the wireless company improves its coverage and upgrades to LTE (fourth-generation), “I see pricing somewhat discounted, but probably closer to the incumbents as we go forward, which allows us to increase ARPU [average revenue per user]. But listen, growth is very important to us and that’s going to be a key driver, as well as making sure consumers feel there’s value.”

HSBC Bank Canada, proud issuer of HSB.PR.C and HSB.PR.D, has been confirmed at Pfd-2 by DBRS:

DBRS Limited (DBRS) has today confirmed all the ratings of HSBC Bank Canada (HSBC Canada or the Bank) including the Bank’s Long-Term Deposits and Senior Debt at A (high) and the Short-Term Instruments at R-1 (middle). All trends are Stable. Additionally, DBRS discontinued the rating of HSBC Canada Asset Trust (HaTS HSBC Bank Canada’s innovative Tier 1 capital instruments) following repayment of the final instrument.

Earlier this year, on September 29, 2015, DBRS downgraded the Long-Term Deposits and Senior Debt, and Subordinated Debt ratings of HSBC Canada following the conclusion of a review of government support at HSBC Holdings plc, the indirect parent entity of HSBC Canada. The changes reflect DBRS’s view that developments in European regulation and legislation mean that there is less certainty about the likelihood of timely systemic support. Given HSBC Canada’s position in the global franchise of HSBC Group (the Group), DBRS has assigned an SA1 designation to the bank under “DBRS Criteria: Support Assessments for Banks and Banking Organisations,” which implies strong and predictable support from the Group, should it be required. As a result, HSBC Canada’s rating generally moves in tandem with HSBC Holdings plc’s rating. Accordingly, HSBC Canada’s senior debt rating is notched down by one notch from HSBC Holdings plc’s rating of AA (low).

…

Some factors that may improve HSBC Canada’s overall credit strength include reductions in geographic and/or sector loan concentrations, or a successful growth of retail wealth management. On the other hand, any significant increase in provisions (particularly related to energy sector lending), evidence of compliance failings or a change in DBRS’s assessment of likely support from the HSBC Group could put negative pressure on the rating assessment.

The trouble nowadays, though, is that when people refer to “lift-off”, I don’t know whether they’re talking about the Fed rate increase or the Canadian preferred share market!

Click for Big

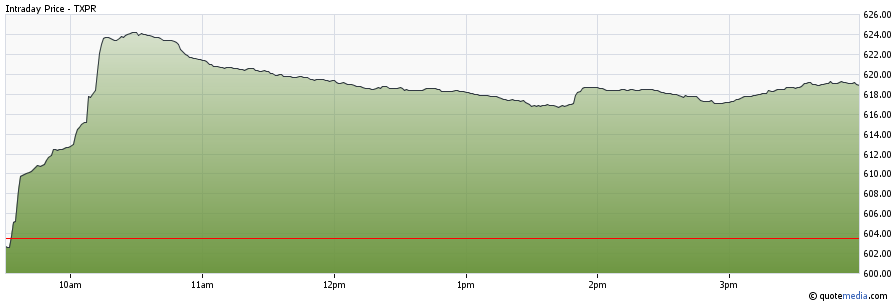

The Canadian preferred share market was on fire again today, with PerpetualDiscounts up 102bp, FixedResets winning 336bp and DeemedRetractibles gaining 59bp. The Performance Highlights table is ridiculously long again, of course, with no less than fifteen issues returning more than 5.00% on the day. Volume was again very, very heavy.

PerpetualDiscounts now yield 5.86%, equivalent to 7.62% interest at the standard equivalency factor of 1.3x. Long corporates now yield a little over 4.2%, so the pre-tax interest-equivalent spread (in this context, the “Seniority Spread”) is now about 340bp, down only slightly (and perhaps spuriously) from the 345bp reported December 9

At time of writing the TMXMoney website doesn’t have the Total Return Index Value for TXPL, but I guess it’s about maybe 1,256.41, which would put the index down 3.22% on the month-to-date, but 6.36% above the December 14 low.

Click for Big

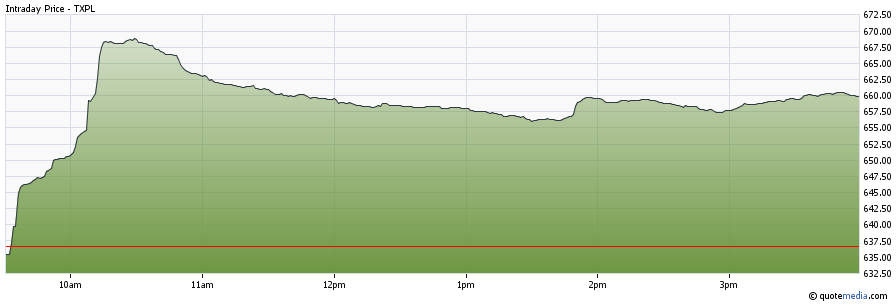

Similarly, TXPL is somewhere close to 773.32, down 3.68% on the month-to-date but 9.08% above the December 14 low.

Click for Big

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

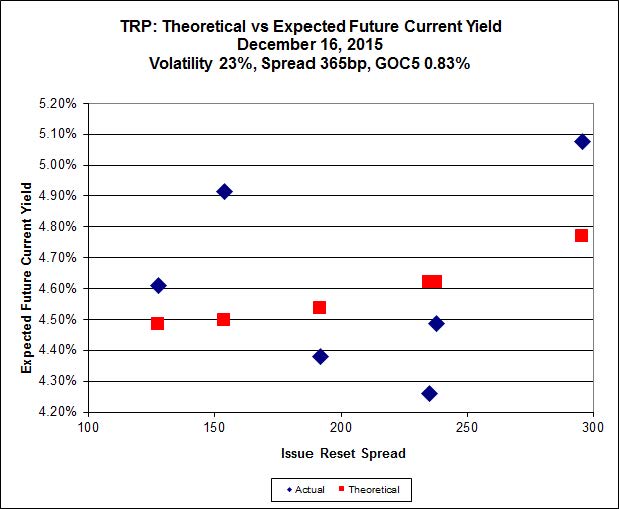

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 18.66 to be $1.45 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $1.12 cheap at its bid price of 12.06.

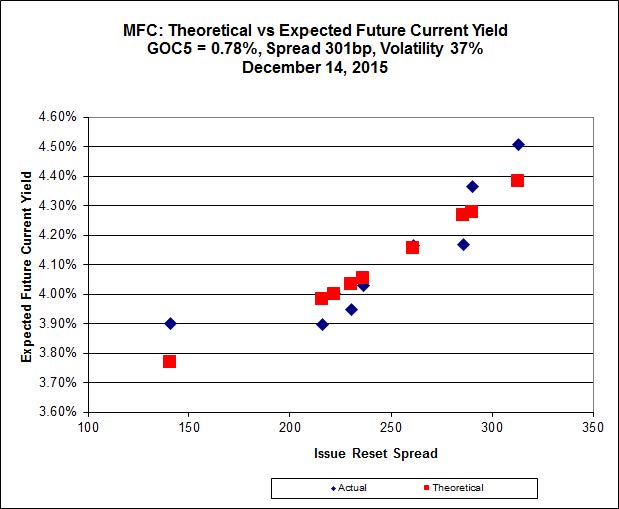

Click for Big

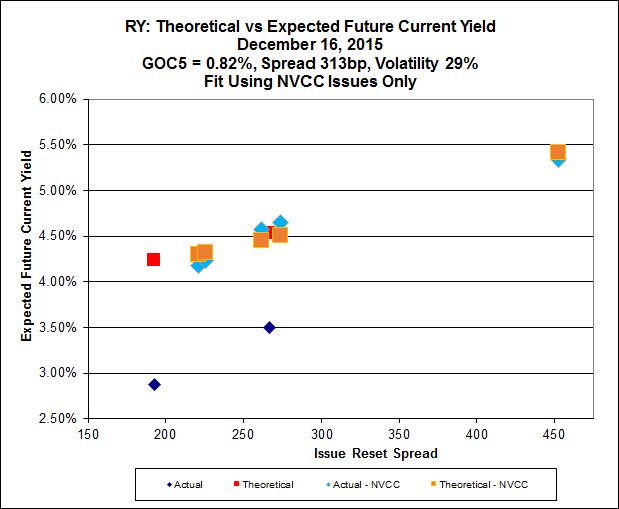

Most expensive is MFC.PR.H, resetting at +313bp on 2017-3-19, bid at 21.96 to be 0.64 cheap, while MFC.PR.I, resetting at +286bp on 2017-9-19, is bid at 22.13 to be 0.51 rich.

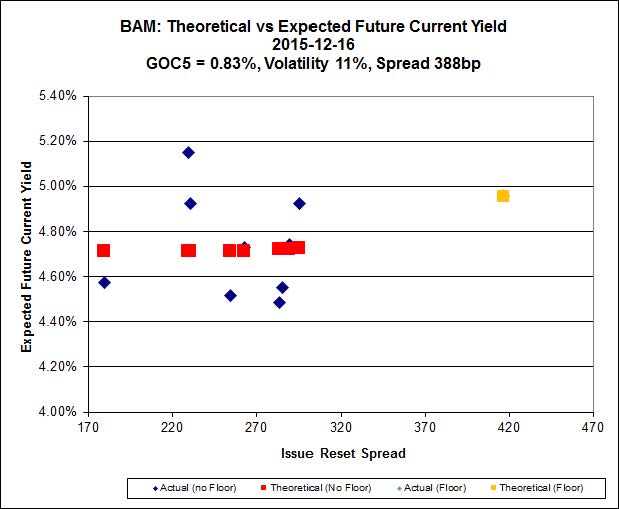

Click for Big

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 15.20 to be $1.41 cheap. BAM.PF.G, resetting at +284bp on 2020-6-30 is bid at 20.45 and appears to be $1.01 rich.

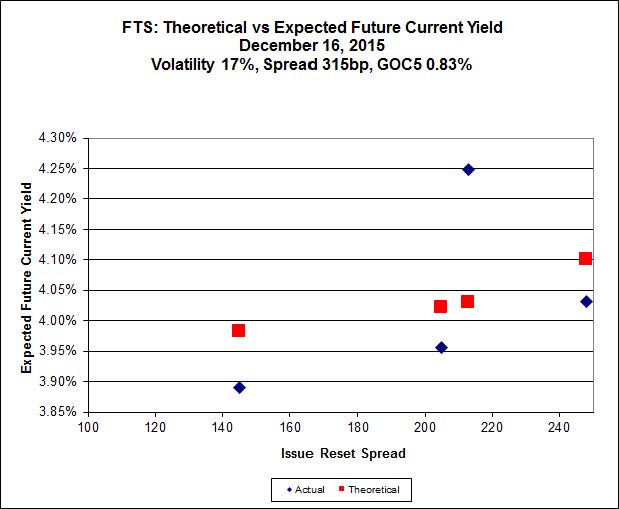

Click for Big

FTS.PR.M, with a spread of +248bp, and bid at 20.53, looks $0.35 expensive and resets 2019-12-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 17.42 and is $0.94 cheap.

Click for Big

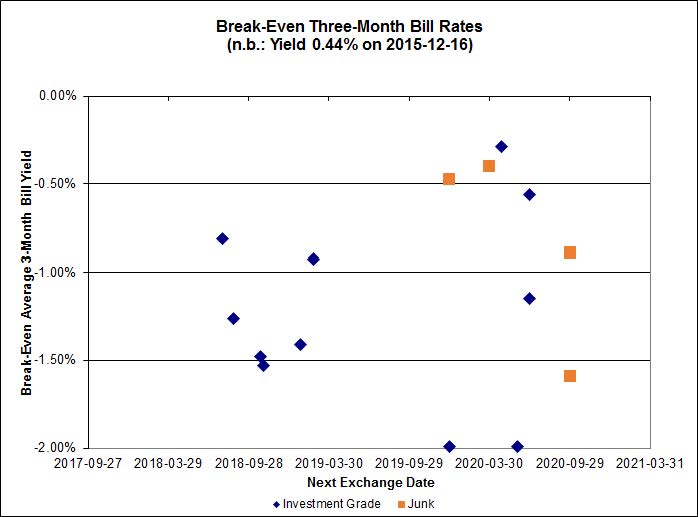

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -1.33%, with one outlier below -2.00%. There are two junk outliers below -2.00% and four above 0.00%. Note the vertical axis of this graph has been changed.

Click for Big

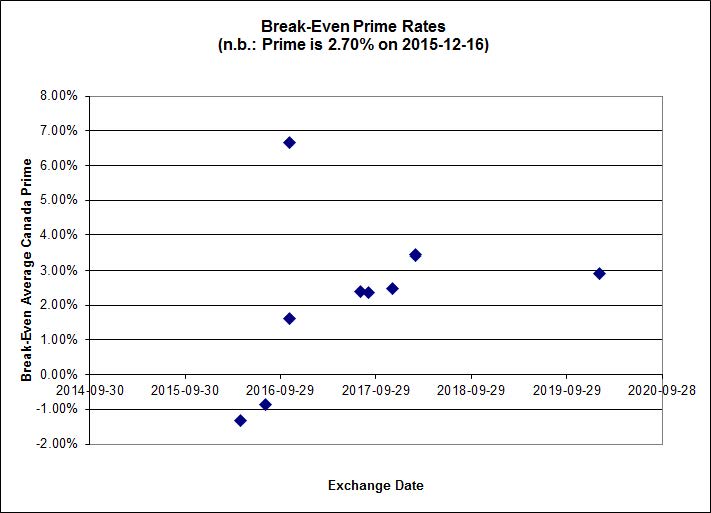

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 4.96 % | 6.03 % | 33,638 | 16.60 | 1 | 0.3663 % | 1,563.8 |

| FixedFloater | 7.25 % | 6.42 % | 35,518 | 15.72 | 1 | 1.9440 % | 2,693.1 |

| Floater | 4.31 % | 4.36 % | 84,444 | 16.72 | 4 | 0.5739 % | 1,771.4 |

| OpRet | 4.87 % | 4.28 % | 26,297 | 0.69 | 1 | 0.0000 % | 2,734.3 |

| SplitShare | 4.87 % | 5.81 % | 82,956 | 1.87 | 6 | 0.0415 % | 3,175.7 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0415 % | 2,477.8 |

| Perpetual-Premium | 5.85 % | 5.91 % | 98,476 | 13.90 | 7 | 0.5310 % | 2,477.8 |

| Perpetual-Discount | 5.78 % | 5.86 % | 104,697 | 14.05 | 33 | 1.0227 % | 2,477.5 |

| FixedReset | 5.22 % | 4.72 % | 265,864 | 15.31 | 80 | 3.3632 % | 1,977.0 |

| Deemed-Retractible | 5.25 % | 5.30 % | 135,940 | 5.31 | 33 | 0.5933 % | 2,556.1 |

| FloatingReset | 2.81 % | 4.27 % | 68,373 | 5.67 | 11 | 1.9011 % | 2,103.5 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| PVS.PR.E | SplitShare | -1.98 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-10-31 Maturity Price : 25.00 Evaluated at bid price : 23.82 Bid-YTW : 6.43 % |

| BAM.PR.K | Floater | -1.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 10.52 Evaluated at bid price : 10.52 Bid-YTW : 4.49 % |

| BAM.PF.H | FixedReset | 1.00 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2020-12-31 Maturity Price : 25.00 Evaluated at bid price : 25.20 Bid-YTW : 4.80 % |

| CU.PR.I | FixedReset | 1.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 23.13 Evaluated at bid price : 24.90 Bid-YTW : 4.44 % |

| RY.PR.B | Deemed-Retractible | 1.05 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.97 Bid-YTW : 4.80 % |

| RY.PR.D | Deemed-Retractible | 1.06 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.88 Bid-YTW : 4.67 % |

| MFC.PR.C | Deemed-Retractible | 1.10 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.31 Bid-YTW : 7.40 % |

| IFC.PR.C | FixedReset | 1.10 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.26 Bid-YTW : 6.91 % |

| PWF.PR.H | Perpetual-Premium | 1.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 24.43 Evaluated at bid price : 24.67 Bid-YTW : 5.91 % |

| FTS.PR.K | FixedReset | 1.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 18.20 Evaluated at bid price : 18.20 Bid-YTW : 4.15 % |

| SLF.PR.C | Deemed-Retractible | 1.14 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.32 Bid-YTW : 7.31 % |

| CU.PR.D | Perpetual-Discount | 1.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 21.19 Evaluated at bid price : 21.19 Bid-YTW : 5.84 % |

| PWF.PR.L | Perpetual-Discount | 1.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 21.82 Evaluated at bid price : 22.06 Bid-YTW : 5.86 % |

| POW.PR.A | Perpetual-Discount | 1.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 23.99 Evaluated at bid price : 24.24 Bid-YTW : 5.87 % |

| GWO.PR.P | Deemed-Retractible | 1.23 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.96 Bid-YTW : 6.01 % |

| TRP.PR.B | FixedReset | 1.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 11.44 Evaluated at bid price : 11.44 Bid-YTW : 4.51 % |

| SLF.PR.D | Deemed-Retractible | 1.25 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.21 Bid-YTW : 7.38 % |

| ELF.PR.F | Perpetual-Discount | 1.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 22.06 Evaluated at bid price : 22.35 Bid-YTW : 6.03 % |

| TRP.PR.E | FixedReset | 1.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 18.66 Evaluated at bid price : 18.66 Bid-YTW : 4.54 % |

| BAM.PR.B | Floater | 1.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 10.84 Evaluated at bid price : 10.84 Bid-YTW : 4.36 % |

| BIP.PR.A | FixedReset | 1.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 19.22 Evaluated at bid price : 19.22 Bid-YTW : 5.70 % |

| PWF.PR.F | Perpetual-Discount | 1.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 22.29 Evaluated at bid price : 22.56 Bid-YTW : 5.90 % |

| PVS.PR.D | SplitShare | 1.38 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2021-10-08 Maturity Price : 25.00 Evaluated at bid price : 22.06 Bid-YTW : 7.06 % |

| IAG.PR.A | Deemed-Retractible | 1.38 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.55 Bid-YTW : 7.32 % |

| BAM.PR.T | FixedReset | 1.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 15.95 Evaluated at bid price : 15.95 Bid-YTW : 4.96 % |

| FTS.PR.J | Perpetual-Discount | 1.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 21.55 Evaluated at bid price : 21.55 Bid-YTW : 5.56 % |

| TD.PR.T | FloatingReset | 1.51 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.25 Bid-YTW : 4.07 % |

| CU.PR.E | Perpetual-Discount | 1.53 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 21.25 Evaluated at bid price : 21.25 Bid-YTW : 5.82 % |

| ELF.PR.G | Perpetual-Discount | 1.54 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 20.46 Evaluated at bid price : 20.46 Bid-YTW : 5.91 % |

| CU.PR.F | Perpetual-Discount | 1.55 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 19.70 Evaluated at bid price : 19.70 Bid-YTW : 5.77 % |

| PWF.PR.E | Perpetual-Discount | 1.55 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 23.33 Evaluated at bid price : 23.61 Bid-YTW : 5.90 % |

| MFC.PR.B | Deemed-Retractible | 1.56 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.88 Bid-YTW : 7.18 % |

| CM.PR.Q | FixedReset | 1.57 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 19.40 Evaluated at bid price : 19.40 Bid-YTW : 4.64 % |

| TD.PF.A | FixedReset | 1.57 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 18.07 Evaluated at bid price : 18.07 Bid-YTW : 4.46 % |

| CU.PR.H | Perpetual-Discount | 1.58 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 22.15 Evaluated at bid price : 22.50 Bid-YTW : 5.87 % |

| BIP.PR.B | FixedReset | 1.60 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 22.20 Evaluated at bid price : 22.87 Bid-YTW : 6.03 % |

| PWF.PR.K | Perpetual-Discount | 1.64 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 21.42 Evaluated at bid price : 21.68 Bid-YTW : 5.78 % |

| CM.PR.P | FixedReset | 1.67 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 17.03 Evaluated at bid price : 17.03 Bid-YTW : 4.72 % |

| BAM.PR.R | FixedReset | 1.67 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 15.20 Evaluated at bid price : 15.20 Bid-YTW : 5.11 % |

| TRP.PR.H | FloatingReset | 1.71 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 10.10 Evaluated at bid price : 10.10 Bid-YTW : 4.25 % |

| ENB.PR.A | Perpetual-Discount | 1.72 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 22.22 Evaluated at bid price : 22.50 Bid-YTW : 6.16 % |

| TD.PR.Z | FloatingReset | 1.75 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.15 Bid-YTW : 4.23 % |

| TRP.PR.D | FixedReset | 1.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 17.88 Evaluated at bid price : 17.88 Bid-YTW : 4.67 % |

| VNR.PR.A | FixedReset | 1.82 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 19.00 Evaluated at bid price : 19.00 Bid-YTW : 4.88 % |

| BAM.PR.Z | FixedReset | 1.85 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 19.25 Evaluated at bid price : 19.25 Bid-YTW : 4.99 % |

| SLF.PR.J | FloatingReset | 1.87 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.05 Bid-YTW : 9.93 % |

| BAM.PR.C | Floater | 1.90 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 10.70 Evaluated at bid price : 10.70 Bid-YTW : 4.41 % |

| RY.PR.I | FixedReset | 1.91 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.00 Bid-YTW : 3.93 % |

| CU.PR.G | Perpetual-Discount | 1.91 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 19.70 Evaluated at bid price : 19.70 Bid-YTW : 5.77 % |

| BAM.PR.G | FixedFloater | 1.94 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 25.00 Evaluated at bid price : 13.11 Bid-YTW : 6.42 % |

| CIU.PR.C | FixedReset | 2.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 13.60 Evaluated at bid price : 13.60 Bid-YTW : 3.95 % |

| BNS.PR.R | FixedReset | 2.14 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.33 Bid-YTW : 3.87 % |

| TD.PF.B | FixedReset | 2.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 17.83 Evaluated at bid price : 17.83 Bid-YTW : 4.51 % |

| BNS.PR.C | FloatingReset | 2.23 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.00 Bid-YTW : 4.57 % |

| PWF.PR.T | FixedReset | 2.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 21.93 Evaluated at bid price : 22.25 Bid-YTW : 3.71 % |

| BNS.PR.B | FloatingReset | 2.29 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.87 Bid-YTW : 4.48 % |

| BNS.PR.D | FloatingReset | 2.50 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.45 Bid-YTW : 6.73 % |

| NA.PR.Q | FixedReset | 2.54 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.62 Bid-YTW : 3.74 % |

| W.PR.J | Perpetual-Discount | 2.56 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 22.93 Evaluated at bid price : 23.21 Bid-YTW : 6.14 % |

| W.PR.H | Perpetual-Discount | 2.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 22.71 Evaluated at bid price : 23.00 Bid-YTW : 6.08 % |

| BNS.PR.Z | FixedReset | 2.81 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.37 Bid-YTW : 6.86 % |

| MFC.PR.H | FixedReset | 2.86 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.96 Bid-YTW : 5.74 % |

| RY.PR.M | FixedReset | 2.89 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 18.86 Evaluated at bid price : 18.86 Bid-YTW : 4.59 % |

| BNS.PR.Y | FixedReset | 2.89 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.55 Bid-YTW : 6.19 % |

| TRP.PR.G | FixedReset | 2.90 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 19.86 Evaluated at bid price : 19.86 Bid-YTW : 4.74 % |

| BMO.PR.S | FixedReset | 2.91 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 18.42 Evaluated at bid price : 18.42 Bid-YTW : 4.45 % |

| MFC.PR.F | FixedReset | 2.94 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.36 Bid-YTW : 9.30 % |

| TRP.PR.C | FixedReset | 3.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 12.06 Evaluated at bid price : 12.06 Bid-YTW : 4.82 % |

| NA.PR.W | FixedReset | 3.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 17.02 Evaluated at bid price : 17.02 Bid-YTW : 4.76 % |

| TD.PR.S | FixedReset | 3.12 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.80 Bid-YTW : 3.79 % |

| FTS.PR.H | FixedReset | 3.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 14.65 Evaluated at bid price : 14.65 Bid-YTW : 3.90 % |

| MFC.PR.J | FixedReset | 3.25 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.65 Bid-YTW : 6.07 % |

| HSE.PR.E | FixedReset | 3.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 19.00 Evaluated at bid price : 19.00 Bid-YTW : 5.77 % |

| NA.PR.S | FixedReset | 3.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 17.68 Evaluated at bid price : 17.68 Bid-YTW : 4.76 % |

| BMO.PR.W | FixedReset | 3.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 17.60 Evaluated at bid price : 17.60 Bid-YTW : 4.51 % |

| BMO.PR.R | FloatingReset | 3.41 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.75 Bid-YTW : 3.72 % |

| SLF.PR.G | FixedReset | 3.45 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.00 Bid-YTW : 8.67 % |

| BMO.PR.M | FixedReset | 3.49 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.60 Bid-YTW : 3.18 % |

| RY.PR.J | FixedReset | 3.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 19.20 Evaluated at bid price : 19.20 Bid-YTW : 4.62 % |

| BAM.PF.B | FixedReset | 3.51 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 18.29 Evaluated at bid price : 18.29 Bid-YTW : 4.84 % |

| TD.PF.C | FixedReset | 3.57 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 18.01 Evaluated at bid price : 18.01 Bid-YTW : 4.45 % |

| TD.PF.D | FixedReset | 3.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 19.99 Evaluated at bid price : 19.99 Bid-YTW : 4.50 % |

| TD.PF.E | FixedReset | 3.74 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 20.50 Evaluated at bid price : 20.50 Bid-YTW : 4.50 % |

| BMO.PR.T | FixedReset | 3.75 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 17.71 Evaluated at bid price : 17.71 Bid-YTW : 4.51 % |

| IFC.PR.A | FixedReset | 3.84 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.24 Bid-YTW : 8.54 % |

| MFC.PR.L | FixedReset | 3.84 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.18 Bid-YTW : 6.84 % |

| BNS.PR.P | FixedReset | 3.87 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.68 Bid-YTW : 3.34 % |

| IAG.PR.G | FixedReset | 3.91 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.25 Bid-YTW : 5.88 % |

| FTS.PR.I | FloatingReset | 3.96 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 11.80 Evaluated at bid price : 11.80 Bid-YTW : 4.03 % |

| RY.PR.H | FixedReset | 3.99 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 18.25 Evaluated at bid price : 18.25 Bid-YTW : 4.40 % |

| RY.PR.Z | FixedReset | 4.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 18.21 Evaluated at bid price : 18.21 Bid-YTW : 4.36 % |

| CM.PR.O | FixedReset | 4.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 17.91 Evaluated at bid price : 17.91 Bid-YTW : 4.59 % |

| MFC.PR.G | FixedReset | 4.09 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.36 Bid-YTW : 5.84 % |

| HSE.PR.C | FixedReset | 4.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 17.71 Evaluated at bid price : 17.71 Bid-YTW : 5.71 % |

| BMO.PR.Q | FixedReset | 4.37 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.54 Bid-YTW : 5.66 % |

| MFC.PR.K | FixedReset | 4.38 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.05 Bid-YTW : 6.83 % |

| BNS.PR.Q | FixedReset | 4.43 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.06 Bid-YTW : 3.81 % |

| FTS.PR.M | FixedReset | 4.64 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 20.53 Evaluated at bid price : 20.53 Bid-YTW : 4.18 % |

| TRP.PR.A | FixedReset | 4.67 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 15.70 Evaluated at bid price : 15.70 Bid-YTW : 4.47 % |

| HSE.PR.G | FixedReset | 4.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 19.00 Evaluated at bid price : 19.00 Bid-YTW : 5.76 % |

| GWO.PR.N | FixedReset | 5.04 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.76 Bid-YTW : 9.56 % |

| CU.PR.C | FixedReset | 5.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 18.92 Evaluated at bid price : 18.92 Bid-YTW : 4.28 % |

| MFC.PR.N | FixedReset | 5.15 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.82 Bid-YTW : 6.51 % |

| MFC.PR.I | FixedReset | 5.23 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.13 Bid-YTW : 5.41 % |

| FTS.PR.G | FixedReset | 5.58 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 17.42 Evaluated at bid price : 17.42 Bid-YTW : 4.37 % |

| MFC.PR.M | FixedReset | 5.60 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.80 Bid-YTW : 6.59 % |

| SLF.PR.I | FixedReset | 5.71 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.35 Bid-YTW : 6.28 % |

| TD.PR.Y | FixedReset | 5.82 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.37 Bid-YTW : 3.54 % |

| BAM.PF.A | FixedReset | 6.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 19.67 Evaluated at bid price : 19.67 Bid-YTW : 4.82 % |

| BAM.PF.G | FixedReset | 6.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 20.45 Evaluated at bid price : 20.45 Bid-YTW : 4.67 % |

| BAM.PF.F | FixedReset | 6.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 20.26 Evaluated at bid price : 20.26 Bid-YTW : 4.69 % |

| SLF.PR.H | FixedReset | 6.99 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.60 Bid-YTW : 7.56 % |

| BAM.PR.X | FixedReset | 7.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 14.38 Evaluated at bid price : 14.38 Bid-YTW : 4.73 % |

| BAM.PF.E | FixedReset | 7.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 18.71 Evaluated at bid price : 18.71 Bid-YTW : 4.76 % |

| PWF.PR.P | FixedReset | 9.92 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 14.30 Evaluated at bid price : 14.30 Bid-YTW : 4.17 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| RY.PR.Q | FixedReset | 1,558,368 | New issue settled today. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 23.17 Evaluated at bid price : 25.10 Bid-YTW : 5.25 % |

| IFC.PR.A | FixedReset | 135,504 | Desjardins crossed blocks of 39,600 and 58,100, both at 16.20. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.24 Bid-YTW : 8.54 % |

| W.PR.K | FixedReset | 102,801 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 22.89 Evaluated at bid price : 24.28 Bid-YTW : 5.36 % |

| RY.PR.W | Perpetual-Discount | 92,464 | Nesbitt crossed 75,000 at 21.87. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 21.69 Evaluated at bid price : 21.94 Bid-YTW : 5.63 % |

| HSE.PR.G | FixedReset | 87,537 | Scotia crossed 65,600 at 18.72. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 19.00 Evaluated at bid price : 19.00 Bid-YTW : 5.76 % |

| RY.PR.N | Perpetual-Discount | 86,776 | Nesbitt crossed 75,000 at 22.05. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-16 Maturity Price : 21.79 Evaluated at bid price : 22.11 Bid-YTW : 5.58 % |

| There were 93 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| BAM.PR.E | Ratchet | Quote: 13.70 – 15.50 Spot Rate : 1.8000 Average : 1.3113 YTW SCENARIO |

| TD.PR.T | FloatingReset | Quote: 22.25 – 23.35 Spot Rate : 1.1000 Average : 0.6731 YTW SCENARIO |

| PWF.PR.A | Floater | Quote: 11.75 – 12.75 Spot Rate : 1.0000 Average : 0.6683 YTW SCENARIO |

| IGM.PR.B | Perpetual-Premium | Quote: 24.99 – 25.74 Spot Rate : 0.7500 Average : 0.4456 YTW SCENARIO |

| TD.PR.Z | FloatingReset | Quote: 22.15 – 22.97 Spot Rate : 0.8200 Average : 0.5641 YTW SCENARIO |

| VNR.PR.A | FixedReset | Quote: 19.00 – 19.66 Spot Rate : 0.6600 Average : 0.4336 YTW SCENARIO |