Well, it looks like one source of PrefBlog entertainment is coming to an end … Sprott is on the verge of winning the battle for Gold Trust:

Sprott Asset Management LP (“Sprott” or “Sprott Asset Management”), together with Sprott Physical Gold Trust (NYSE:PHYS) (TSX:PHY.U) and Sprott Physical Silver Trust (NYSE:PSLV) (TSX:PHS.U), today announced that a majority of Central GoldTrust (“GTU”) (TSX:GTU.UN) (TSX:GTU.U) (NYSEMKT:GTU) unitholders have tendered into the Sprott offer for GTU, and as a result Sprott, on behalf of tendering GTU unitholders and as described in Sprott’s November 20, 2015 Notice of Extension and Variation, has removed Brian Felske, Glenn Fox, Bruce Heagle, Ian McAvity, Michael Parente and Jason Schwandt as GTU trustees and appointed Marc Faber, James Fox, Sharon Ranson, John Wilson and Rosemary Zigrossi as new trustees of GTU. Stefan Spicer remains a trustee of GTU.

Following the replacement of GTU’s trustees, Sprott, also on behalf of tendering GTU unitholders, submitted a unitholder meeting requisition to the reconstituted GTU board proposing that the Merger transaction forming part of the Sprott offer for GTU be considered at a special meeting of GTU unitholders.

Sprott has extended the expiry times of the Sprott offers for GTU and for Silver Bullion Trust (“SBT”) (TSX:SBT.UN) (TSX:SBT.U) (collectively, the “Sprott offers”) to 5:00 p.m. (Toronto time) on January 12, 2016. Notices of extension will be filed shortly.

As of 5:00 p.m. (Toronto time) on December 7, 2015, there were 10,641,033 GTU units (55.14% of all outstanding GTU units) and 2,294,963 SBT units (41.98% of all outstanding SBT units) tendered to the respective Sprott offers.

Fortunately, the battle for Silver Trust still rages and incumbent management had this to say:

Silver Bullion Trust (“SBT”) (TSX:SBT.UN) (C$) and (TSX:SBT.U) (US$) confirmed today that the unsolicited offer by Sprott Asset Management LP and Sprott Physical Silver Trust (“Sprott PSLV”; and collectively, “Sprott”) for all of the outstanding units of SBT has once again failed to achieve sufficient acceptance to satisfy the required minimum tender condition. As a result, Sprott has yet again, for the 8th time, extended the expiry date of their offer, which is now set to expire on January 12, 2016.

Bruce Heagle, Chair of the Special Committee of the Board of Trustees, stated: “Yet again, Sprott’s inadequate offer has failed to achieve sufficient support from SBT unitholders. We expect that unitholder support for Sprott’s offer will erode further and support for the proposed conversion (the “ETF Conversion”) of SBT into a silver bullion exchange-traded fund will gain momentum as unitholders review the Trustees’ Information Circular (the “Circular”), which describes the benefits of the ETF Conversion for all unitholders and its clear advantages relative to Sprott’s offer. We are confident that unitholders will reach the same conclusion as the Independent Trustees have; that the proposed ETF Conversion is a superior alternative to Sprott’s inadequate offer.”

Gold Trust, regrettably, was silent.

I understand there will be a new publication devoted to the Canadian preferred share market:

Click for Big

It was another appalling day for the Canadian preferred share market, with PerpetualDiscounts down 3bp, FixedResets losing 133bp and DeemedRetractibles off 45bp. FixedReset yields have now broken through the 5.00% barrier. The Performance Highlights table is its usual ridiculous self. Volume was, again, incredibly high.

PerpetualDiscounts now yield 5.91%, equivalent to 7.68% interest at the standard equivalency factor of 1.3x. Long corporates now yield a little over 4.2%, so the pre-tax interest-equivalent spread [in this context, the “Seniority Spread”] is now about 345bp, an incredibly high number, representing an explosive widening from the 310bp reported December 2.

For those keeping score, TXPR is now down about 7.16% on the month to date and is now only 0.93% above the low of October 14.

Click for Big

TXPL is down about 8.76% on the month to date and is 0.74% above the October 14 low.

Click for Big

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

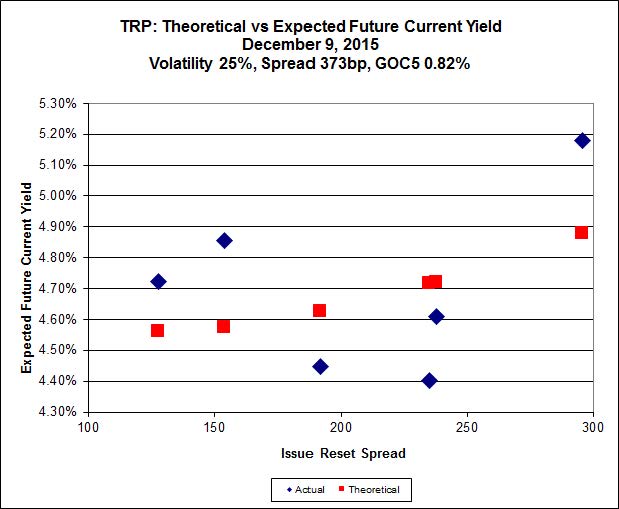

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 18.00 to be $1.20 rich, while TRP.PR.G, resetting 2020-11-30 at +154, is $1.13 cheap at its bid price of 18.25.

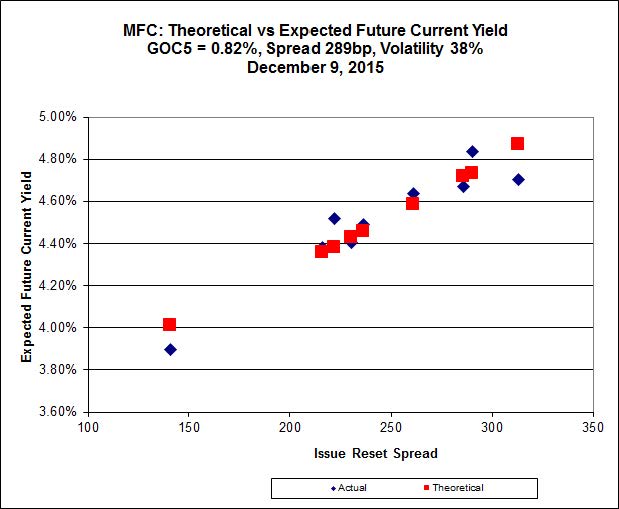

Click for Big

Most expensive is MFC.PR.H, resetting at +313bp on 2017-3-19, bid at 21.00 to be 0.72 rich, while MFC.PR.K, resetting at +222bp on 2018-9-19, is bid at 16.82 to be 0.52 cheap.

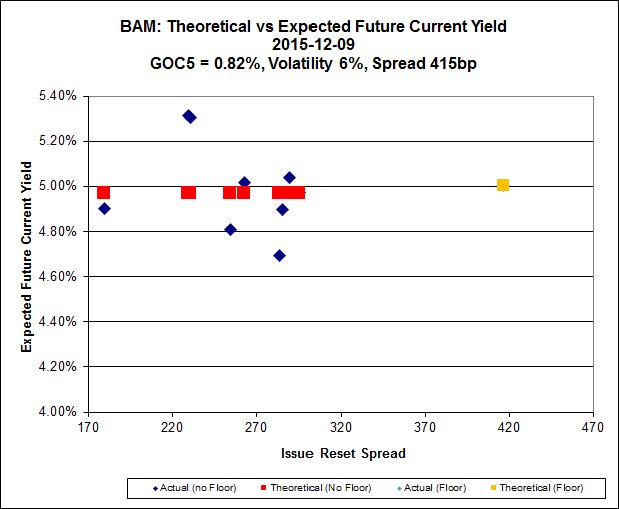

Click for Big

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 14.68 to be $1.01 cheap. BAM.PF.G, resetting at +284bp on 2020-6-30 is bid at 19.50 and appears to be $1.09 rich.

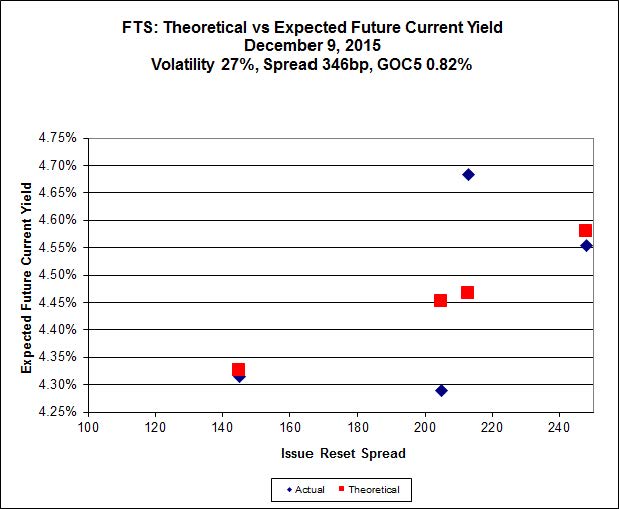

Click for Big

FTS.PR.K, with a spread of +205bp, and bid at 16.73, looks $0.61 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 15.75 and is $0.76 cheap.

Click for Big

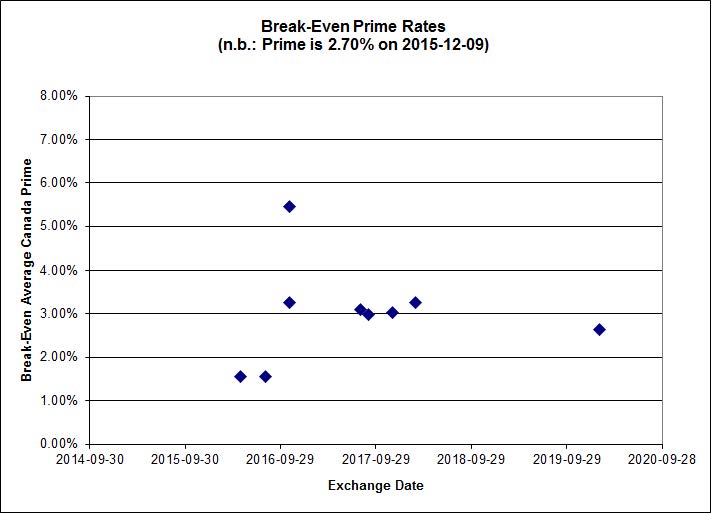

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.41%, with one outlier below -1.50%. There is one junk outlier below -1.50%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 4.98 % | 6.05 % | 34,207 | 16.59 | 1 | 1.1111 % | 1,558.0 |

| FixedFloater | 7.14 % | 6.32 % | 32,909 | 15.86 | 1 | -1.4815 % | 2,732.1 |

| Floater | 4.20 % | 4.39 % | 75,601 | 16.53 | 4 | 1.5801 % | 1,802.8 |

| OpRet | 4.87 % | 4.17 % | 27,812 | 0.71 | 1 | 0.0000 % | 2,734.3 |

| SplitShare | 4.82 % | 5.25 % | 84,704 | 2.86 | 6 | 0.3504 % | 3,202.2 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.3504 % | 2,498.5 |

| Perpetual-Premium | 5.89 % | 5.96 % | 95,692 | 13.88 | 7 | -0.4143 % | 2,461.9 |

| Perpetual-Discount | 5.83 % | 5.91 % | 99,616 | 14.00 | 33 | -0.9342 % | 2,454.8 |

| FixedReset | 5.49 % | 5.06 % | 253,245 | 14.45 | 78 | -1.3343 % | 1,874.7 |

| Deemed-Retractible | 5.33 % | 5.51 % | 133,768 | 5.33 | 33 | -0.4532 % | 2,515.8 |

| FloatingReset | 2.80 % | 4.29 % | 64,866 | 5.69 | 11 | -0.6531 % | 2,096.7 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| HSE.PR.E | FixedReset | -7.36 % | Not real, as the issue traded 32,700 shares in a range of 18.47-19.60 before closing at 17.88-19.00, 12×4. Almost all of the last 25 trades were at 19.00, with a few dipping as low as 18.87. I have not checked whether this lamentable state of affairs is due to inadequate Toronto Stock Exchange reporting or inadequate Toronto Stock Exchange supervision of market-makers. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 17.88 Evaluated at bid price : 17.88 Bid-YTW : 6.27 % |

| HSE.PR.G | FixedReset | -5.64 % | Real enough, as the issue traded 14,921 shares in a range of 18.10-19.60 before closing at 18.40-00, 1×1. Only two of the last twenty-five trades were executed below 18.80 and most were comfortably above 19.00. However, there were trades [for 100 shares apiece] at 18.55 and 18.45, timestamped 3:36, so I guess we can call this one “real enough”, while faulting the market maker for an unnecessarily volatile market. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 18.40 Evaluated at bid price : 18.40 Bid-YTW : 6.08 % |

| BIP.PR.A | FixedReset | -5.35 % | This is real, as the issue traded 11,461 shares in a range of 18.21-20 before closing at 18.22-45, 3×2. The trade price slipped below 18.40 at 3:01 and remained there for the day’s last sixteen trades. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 18.22 Evaluated at bid price : 18.22 Bid-YTW : 6.14 % |

| MFC.PR.M | FixedReset | -4.48 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.70 Bid-YTW : 8.20 % |

| BAM.PR.X | FixedReset | -3.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 13.36 Evaluated at bid price : 13.36 Bid-YTW : 5.50 % |

| SLF.PR.H | FixedReset | -3.60 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.53 Bid-YTW : 9.40 % |

| MFC.PR.K | FixedReset | -3.56 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.82 Bid-YTW : 8.63 % |

| TD.PF.D | FixedReset | -3.53 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 18.31 Evaluated at bid price : 18.31 Bid-YTW : 5.06 % |

| MFC.PR.N | FixedReset | -3.33 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.70 Bid-YTW : 8.12 % |

| ENB.PR.A | Perpetual-Discount | -3.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 22.39 Evaluated at bid price : 22.65 Bid-YTW : 6.11 % |

| TD.PR.Y | FixedReset | -3.16 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.26 Bid-YTW : 4.46 % |

| MFC.PR.L | FixedReset | -2.91 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.01 Bid-YTW : 8.57 % |

| NA.PR.W | FixedReset | -2.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 16.35 Evaluated at bid price : 16.35 Bid-YTW : 5.13 % |

| BMO.PR.Q | FixedReset | -2.50 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.50 Bid-YTW : 6.73 % |

| BAM.PR.N | Perpetual-Discount | -2.48 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 18.91 Evaluated at bid price : 18.91 Bid-YTW : 6.42 % |

| BAM.PF.C | Perpetual-Discount | -2.45 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 19.12 Evaluated at bid price : 19.12 Bid-YTW : 6.48 % |

| BAM.PR.T | FixedReset | -2.45 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 14.75 Evaluated at bid price : 14.75 Bid-YTW : 5.73 % |

| RY.PR.H | FixedReset | -2.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 17.10 Evaluated at bid price : 17.10 Bid-YTW : 4.87 % |

| TD.PF.C | FixedReset | -2.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 16.85 Evaluated at bid price : 16.85 Bid-YTW : 4.93 % |

| BMO.PR.Y | FixedReset | -2.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 19.15 Evaluated at bid price : 19.15 Bid-YTW : 4.81 % |

| TRP.PR.F | FloatingReset | -2.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 12.96 Evaluated at bid price : 12.96 Bid-YTW : 4.53 % |

| CU.PR.G | Perpetual-Discount | -2.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 19.55 Evaluated at bid price : 19.55 Bid-YTW : 5.80 % |

| RY.PR.J | FixedReset | -2.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 18.05 Evaluated at bid price : 18.05 Bid-YTW : 5.06 % |

| BNS.PR.Z | FixedReset | -2.16 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.48 Bid-YTW : 6.88 % |

| CU.PR.E | Perpetual-Discount | -2.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 21.02 Evaluated at bid price : 21.02 Bid-YTW : 5.88 % |

| BAM.PR.R | FixedReset | -2.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 14.68 Evaluated at bid price : 14.68 Bid-YTW : 5.68 % |

| NA.PR.S | FixedReset | -2.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 17.05 Evaluated at bid price : 17.05 Bid-YTW : 5.11 % |

| RY.PR.Z | FixedReset | -2.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 17.04 Evaluated at bid price : 17.04 Bid-YTW : 4.84 % |

| BNS.PR.Y | FixedReset | -2.04 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.69 Bid-YTW : 6.08 % |

| HSE.PR.A | FixedReset | -1.94 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 12.14 Evaluated at bid price : 12.14 Bid-YTW : 5.42 % |

| POW.PR.C | Perpetual-Premium | -1.88 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 24.23 Evaluated at bid price : 24.53 Bid-YTW : 6.00 % |

| BNS.PR.R | FixedReset | -1.86 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.75 Bid-YTW : 4.37 % |

| TD.PF.A | FixedReset | -1.83 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 17.15 Evaluated at bid price : 17.15 Bid-YTW : 4.87 % |

| BNS.PR.Q | FixedReset | -1.82 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.25 Bid-YTW : 4.50 % |

| BAM.PF.D | Perpetual-Discount | -1.82 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 19.47 Evaluated at bid price : 19.47 Bid-YTW : 6.43 % |

| BAM.PF.E | FixedReset | -1.79 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 17.52 Evaluated at bid price : 17.52 Bid-YTW : 5.36 % |

| FTS.PR.K | FixedReset | -1.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 16.73 Evaluated at bid price : 16.73 Bid-YTW : 4.70 % |

| RY.PR.W | Perpetual-Discount | -1.74 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 21.25 Evaluated at bid price : 21.52 Bid-YTW : 5.73 % |

| FTS.PR.J | Perpetual-Discount | -1.70 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 20.80 Evaluated at bid price : 20.80 Bid-YTW : 5.76 % |

| TD.PF.E | FixedReset | -1.66 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 19.57 Evaluated at bid price : 19.57 Bid-YTW : 4.84 % |

| BMO.PR.W | FixedReset | -1.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 16.71 Evaluated at bid price : 16.71 Bid-YTW : 4.92 % |

| BAM.PR.M | Perpetual-Discount | -1.61 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 18.96 Evaluated at bid price : 18.96 Bid-YTW : 6.40 % |

| MFC.PR.F | FixedReset | -1.58 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.30 Bid-YTW : 9.52 % |

| BMO.PR.S | FixedReset | -1.58 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 17.43 Evaluated at bid price : 17.43 Bid-YTW : 4.87 % |

| CU.PR.D | Perpetual-Discount | -1.54 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 21.15 Evaluated at bid price : 21.15 Bid-YTW : 5.84 % |

| TRP.PR.H | FloatingReset | -1.52 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 9.71 Evaluated at bid price : 9.71 Bid-YTW : 4.40 % |

| CU.PR.F | Perpetual-Discount | -1.51 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 19.57 Evaluated at bid price : 19.57 Bid-YTW : 5.80 % |

| BAM.PR.G | FixedFloater | -1.48 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 25.00 Evaluated at bid price : 13.30 Bid-YTW : 6.32 % |

| TD.PF.B | FixedReset | -1.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 17.10 Evaluated at bid price : 17.10 Bid-YTW : 4.87 % |

| GWO.PR.I | Deemed-Retractible | -1.39 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.92 Bid-YTW : 7.63 % |

| RY.PR.M | FixedReset | -1.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 17.95 Evaluated at bid price : 17.95 Bid-YTW : 4.97 % |

| BMO.PR.Z | Perpetual-Discount | -1.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 22.52 Evaluated at bid price : 22.85 Bid-YTW : 5.50 % |

| POW.PR.B | Perpetual-Discount | -1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 22.40 Evaluated at bid price : 22.66 Bid-YTW : 6.00 % |

| CM.PR.Q | FixedReset | -1.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 18.37 Evaluated at bid price : 18.37 Bid-YTW : 5.04 % |

| BMO.PR.T | FixedReset | -1.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 16.90 Evaluated at bid price : 16.90 Bid-YTW : 4.90 % |

| BNS.PR.P | FixedReset | -1.17 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.72 Bid-YTW : 4.14 % |

| PWF.PR.K | Perpetual-Discount | -1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 21.25 Evaluated at bid price : 21.25 Bid-YTW : 5.91 % |

| SLF.PR.J | FloatingReset | -1.15 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 12.95 Bid-YTW : 10.00 % |

| FTS.PR.I | FloatingReset | -1.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 11.70 Evaluated at bid price : 11.70 Bid-YTW : 4.04 % |

| MFC.PR.J | FixedReset | -1.07 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.49 Bid-YTW : 7.68 % |

| GWO.PR.Q | Deemed-Retractible | -1.02 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.22 Bid-YTW : 6.80 % |

| BNS.PR.O | Deemed-Retractible | -1.02 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2017-04-26 Maturity Price : 25.00 Evaluated at bid price : 25.28 Bid-YTW : 5.21 % |

| FTS.PR.M | FixedReset | 1.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 18.12 Evaluated at bid price : 18.12 Bid-YTW : 4.90 % |

| BAM.PR.E | Ratchet | 1.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 25.00 Evaluated at bid price : 13.65 Bid-YTW : 6.05 % |

| BAM.PR.C | Floater | 1.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 10.80 Evaluated at bid price : 10.80 Bid-YTW : 4.44 % |

| HSE.PR.C | FixedReset | 1.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 17.68 Evaluated at bid price : 17.68 Bid-YTW : 5.86 % |

| PWF.PR.A | Floater | 1.64 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 12.40 Evaluated at bid price : 12.40 Bid-YTW : 3.84 % |

| BAM.PR.K | Floater | 2.64 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 10.90 Evaluated at bid price : 10.90 Bid-YTW : 4.39 % |

| PVS.PR.D | SplitShare | 3.04 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2021-10-08 Maturity Price : 25.00 Evaluated at bid price : 22.68 Bid-YTW : 6.48 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| RY.PR.I | FixedReset | 203,946 | Nesbitt crossed 100,000 at 23.10 and 99,800 at 23.20. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.16 Bid-YTW : 4.63 % |

| FTS.PR.M | FixedReset | 154,838 | Scotia crossed blocks of 48,500 and 70,000, both at 18.10. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 18.12 Evaluated at bid price : 18.12 Bid-YTW : 4.90 % |

| TD.PF.A | FixedReset | 84,381 | Nesbitt crossed 50,400 at 17.20. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 17.15 Evaluated at bid price : 17.15 Bid-YTW : 4.87 % |

| RY.PR.Z | FixedReset | 75,757 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 17.04 Evaluated at bid price : 17.04 Bid-YTW : 4.84 % |

| RY.PR.J | FixedReset | 73,576 | Scotia crossed 40,000 at 18.50. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 18.05 Evaluated at bid price : 18.05 Bid-YTW : 5.06 % |

| TRP.PR.D | FixedReset | 73,240 | RBC crossed 25,000 at 17.40. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-09 Maturity Price : 17.35 Evaluated at bid price : 17.35 Bid-YTW : 4.98 % |

| There were 88 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| TD.PR.Y | FixedReset | Quote: 23.26 – 23.99 Spot Rate : 0.7300 Average : 0.4573 YTW SCENARIO |

| HSE.PR.E | FixedReset | Quote: 17.88 – 19.00 Spot Rate : 1.1200 Average : 0.8576 YTW SCENARIO |

| BAM.PR.X | FixedReset | Quote: 13.36 – 13.96 Spot Rate : 0.6000 Average : 0.3915 YTW SCENARIO |

| SLF.PR.H | FixedReset | Quote: 15.53 – 16.10 Spot Rate : 0.5700 Average : 0.3677 YTW SCENARIO |

| RY.PR.N | Perpetual-Discount | Quote: 22.05 – 22.50 Spot Rate : 0.4500 Average : 0.2914 YTW SCENARIO |

| POW.PR.C | Perpetual-Premium | Quote: 24.53 – 25.00 Spot Rate : 0.4700 Average : 0.3137 YTW SCENARIO |