The Bank of Nova Scotia has announced:

that it has completed the domestic public offering of Non-cumulative 5-Year Rate Reset Preferred Shares Series 40 (Non-Viability Contingent Capital (NVCC)) (the “Preferred Shares Series 40”).

Scotiabank sold 12 million Preferred Shares Series 40 at a price of $25.00 per share and holders will be entitled to receive a non-cumulative quarterly fixed dividend for the initial period ending January 26, 2024 yielding 4.85% per annum, as and when declared by the Board of Directors of Scotiabank. The gross proceeds of the offering were $300 million.

The offering was made through a syndicate of underwriters led by Scotia Capital Inc. The Preferred Shares Series 40 commenced trading on the Toronto Stock Exchange today under the symbol BNS.PR.I.

On January 27, 2024 and on January 27 every five years thereafter, Scotiabank may, at its option, subject to regulatory approval, redeem all or any number of the then outstanding Preferred Shares Series 40 at a redemption price of $25 per share. Thereafter, the dividend rate will reset every five years at a rate equal to 2.43% over the 5-year Government of Canada bond yield. Holders of Preferred Shares Series 40 will, subject to certain conditions, have the right to convert all or any part of their shares to Non-cumulative Floating Rate Preferred Shares Series 41 (Non-Viability Contingent Capital (NVCC)) (the “Preferred Shares Series 41”) of Scotiabank on January 27, 2024 and on January 27 every five years thereafter.

Holders of the Preferred Shares Series 41 will be entitled to receive a non-cumulative quarterly floating dividend at a rate equal to the 3-month Government of Canada Treasury Bill yield plus 2.43%, as and when declared by the Board of Directors of Scotiabank. Holders of Preferred Shares Series 41 will, subject to certain conditions, have the right to convert all or any part of their shares to Preferred Shares Series 40 on January 27, 2029 and on January 27 every five years thereafter.

BNS.PR.I is a FixedReset, 4.85%+243, NVCC, issue that was announced 2018-10-2. It will be tracked by HIMIPref™ and has been assigned to the FixedReset-Discount sub-index.

The issue traded 644,420 shares today in a range of 24.90-97 before closing at 24.93-97. Vital statistics are:

| BNS.PR.I | FixedReset Disc | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2048-10-12 Maturity Price : 23.12 Evaluated at bid price : 24.93 Bid-YTW : 4.76 % |

The new issue is quite expensive according to Implied Volatility Analysis:

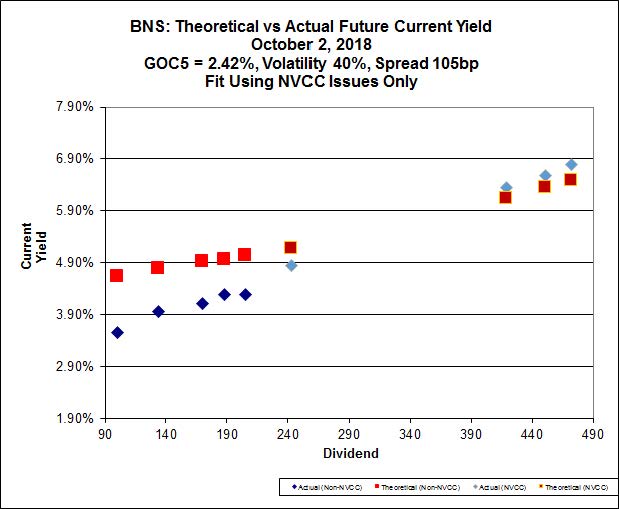

Click for Big

According to this analysis, the fair value of the new issue on October 12 is 23.05, down from the October 2 fair value of 23.43. However, it should be noted that the analysis is forced to do some major extrapolation, as the only other BNS FixedReset NVCC-compliant issues are BNS.PR.E, BNS.PR.G and BNS.PR.H, all of which have Issue Reset Spreads in excess of 400bp. On the other hand, the issue seems well aligned with the NVCC non-compliant issues, whereas it should be well above the regression line they form.

The ludicrously high figure of Implied Volatility is something I take to mean that the underlying assumption of the Black-Scholes model, that of no directionality of prices, is not accepted by the market; the market seems to be taking the view that since things seem rosy now, they will always be rosy and everything will trade near par in the future.

I balk at ascribing a 100% probability to the ‘all issues will be called, or at least exhibit price stability’ hypothesis. There may still be a few old geezers amongst the Assiduous Readers of this blog who can still (faintly) remember the Great Bear Market of 2014-16, in which quite a few similar assumptions made earlier turned out to be slightly inaccurate. The extra cushion implied by an Issue Reset Spread that is well over the market spread is worth something, even if nothing gets called. Or, to put it another way, one can buy a whole lot of downside protection for very little extra money, relative to this issue.