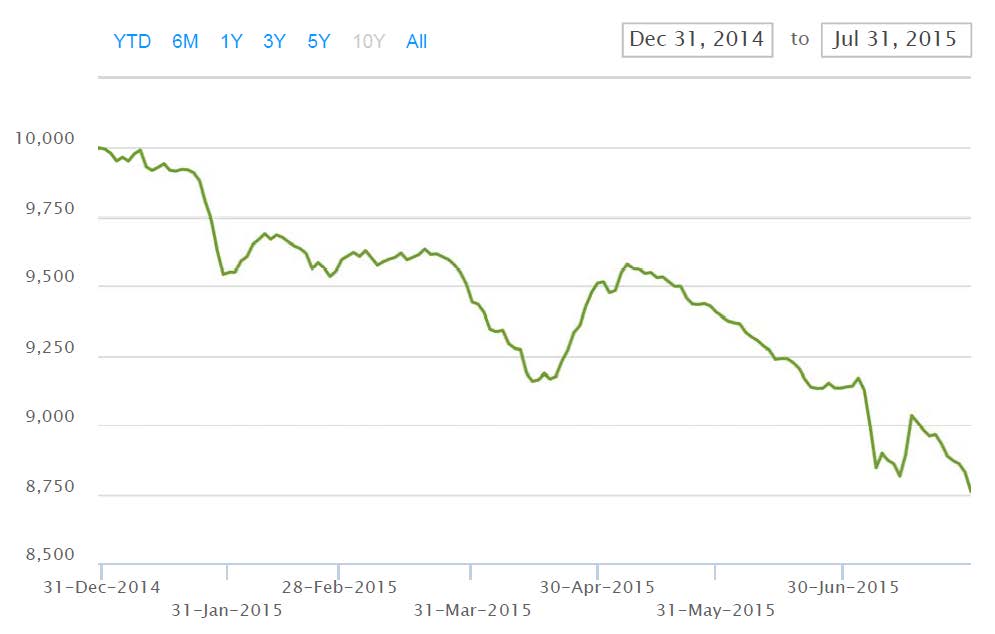

There has been a very steep decline in the Canadian preferred share index in 2015 – so steep, in fact, that some investors are selling simply because their investment has lost value, which has to be one of the worst trade techniques ever (it imposes a form of negative convexity on your portfolio, among other bad things).

Still, it is unnerving. Look at the graph of the value of an investment in CPD, as published by Blackrock:

Click for big

This isn’t the smooth ride that some were expecting! The broad TXPR index was down 4.10% on the month and is down 11.47% over the past year. The FixedReset TXPL index has fared even worse, down 5.31% on the month and a horrific 17.26% on the year. I don’t have figures for the BMO-CM 50 at this time, but if I plug in the TXPR results for July, I can draw the following graph, which shows the rolling twelve month and twenty four month total returns from December 31, 1992:

Click for Big

So both the one- and two-year returns for the index now show losses exceeded only by the depths of the Credit Crunch in the 20+ years of data I have available. And, I will note, the four year total return for TXPR is now negative – in fact, you have to go back to January, 2011, to find a starting point that will give you a better than zero return through the period.

So I received an eMail from a client that said, in part:

But my real problem is that in trying to decide whether to stay in your fund or pull out, I do not know what I am betting on. The prospect of rising CDN interest rates (seems unlikely that would help), the overall Cdn economy? Something else?

What is your take on what it would take for preferred values to start moving in the right direction?

What follows is my answer, with minor edits to ensure anonymity and to reflect the medium of the message.

I can appreciate your concern.

Your first investment was valued on 2012-11-19; the second on 2013-1-21.

From the end of November, 2012, to June, 2015, the fund’s total return (reinvesting dividends, before fees) was -0.35%, compared to the BMO-CM “50” index return of -3.64%. TXPR (the broad S&P/TSX Preferred Share index) returned -4.04%, while TXPL (S&P/TSX, FixedResets only) returned -9.65%.

For the period beginning 2013-1-31 I find: Fund, -1.95%; BMO, -4.86%; TXPR, -5.56%; TXPL, -11.42%.

So the problem is not with the fund so much as it is with the market.

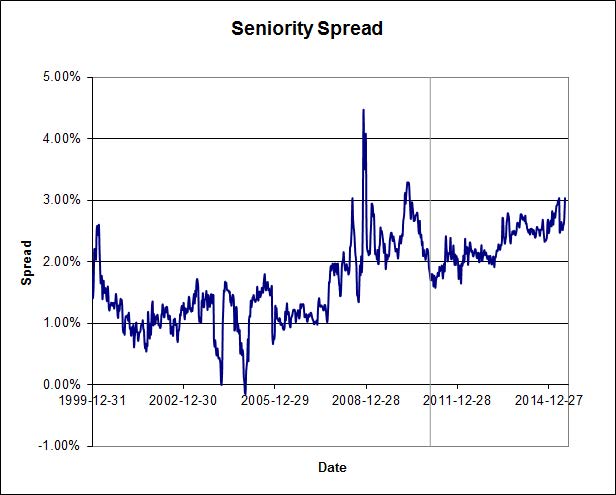

The indices are currently comprised of about 1/3 Straight Perpetuals, 2/3 FixedResets. For an idea of what has happened to Straights, see the attached Chart #22 from the July PrefLetter, which shows the interest-equivalent spread between Straight Perpetuals and long-term Corporate bonds (the “Seniority Spread”).

Click for Big

Market Yields changed as follows, from November 28, 2012 to June 30 , 2015

Five Year Canadas: 1.31% … 0.81%

Long Canadas: 2.38% … 2.37%

Long Corporates: 4.2% … 4.0%

Straight Perpetuals: 4.88% … 5.20%

Interest-Equivalent Straight Perpetuals: 6.35% … 6.76%

These changes have had the effect of widening the Seniority Spread from 215bp to 276bp. I can think of two rationales for this widening:

i) the retail investors who dominate the preferred share space are demanding a higher spread to compensate for perceived risks of losses once “interest rates start to rise”; that is, they are reacting more than the institutional investors in the bond market to risks of loss. This could be due to higher risk-aversion (defining “risk” as chance of loss), less binding duration constraints on the portfolio, simple lack of sophistication, or any combination of these three considerations. Note that I have not made a formal study of the subject and there may be other factors, but those are the ones that occur to me through my experience talking to investors.

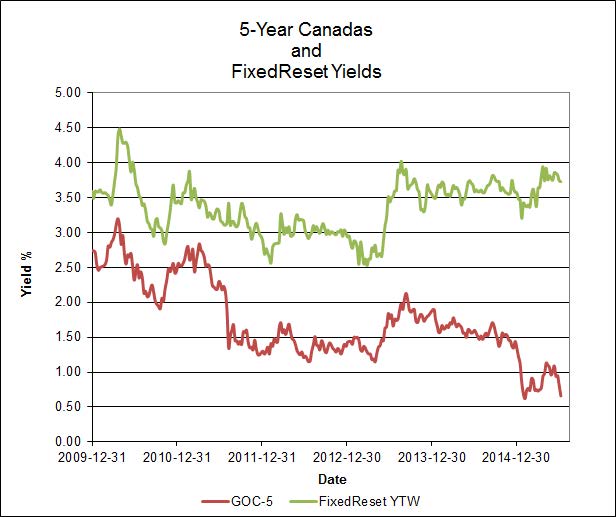

ii) Straight Perpetual yields are being pushed up (or at least supported) by FixedReset yields (see chart FR-44, below, from the extract from the July PrefLetter ). This would be due to a perception amongst investors that Straight Perpetuals are more “risky” (whatever that means!) than FixedResets and hence deserving of a positive spread; note that this effect is not observed when comparing sovereign inflation-indexed bonds to nominals (the Inflation Risk Premium).

Click for Big

These spreads use Yield-To-Worst, not Current Yield

This is Chart FR-44

With respect to FixedResets, it is clear from the horrible performance of TXPL referenced above relative to that of the broader TXPR (which one can approximate as being comprised of about 2/3 TXPL throughout the period of interest, although it has, of course, varied, with FixedReset issuance slightly overcompensating for capital losses) that FixedResets have been whacked.

I have hypothesized a rationale for this underperformance in the attached extract from PrefLetter under the heading “An Experimental Data Series”, to wit: in the face of declines in the Five-Year Canada yield (which is the basis for the resets of of this type of preferred share), investors are attempting to maintain a constant yield irregardless of what is happening with other yields. This is hard to justify on rational grounds, but there has always been an element of irrationality in preferred share pricing! Thus, declines in the GOC-5 yield have been 100% compensated for by declines in price, without referencing yields of comparable long-term instruments; this contradicts one of the features of FixedResets that was used (perhaps inadvertently through indiscriminate use of the term “interest rates”) to help sell the issues when they were developed – that price would remain constant given parallel shifts in the yield curve (with credit spreads assumed, again implicitly, to be constant).

Click for Big

This 100% dependence of FixedReset price on GOC-5 has a very large effect, as derived in the last equation on page 3 of the extract:

i) The base Modified Duration of FixedResets is equal to (1 / EFCY). The term EFCY (“Expected Future Current Yield”) is about 3.75%, implying a Modified Duration of about 27 – not only far higher than long bonds, but dependent upon more volatile five-year yields to boot!

ii) The term (25/P) in the equation implies negative convexity

So to summarize, I feel that the poor performance of the market since your initial investment is due to:

i) very high dependence of FixedReset prices on GOC-5 levels, which has contradicted prior assumptions of an equal and opposite co-dependence on long-term yield levels.

ii) maintenance of a spread to PerpetualDiscounts, which has prevented Straight Perpetuals from participating in price increases due to declines in long-term corporate yields.

Click for Big

The “Bozo Spread” is the Current Yield of PerpetualDiscounts less the Current Yield of FixedResets

It is not yet clear whether the market pays more attention to these Current Yields, or to the Yields-to-Worst, when relating FixedResets to PerpetualDiscounts

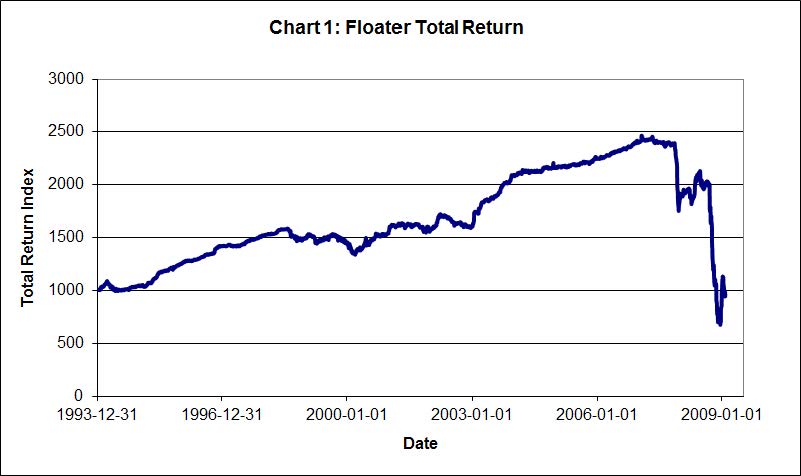

I will also note that to a certain extent, we’ve seen this movie before: during the Credit Crunch Floating Rate issues performed appallingly poorly, since their dividends were linked to contemporary (as opposed to expected!) Canada Prime while their yields were linked to PerpetualDiscounts (see my contemporary article and the next chart)

Click for Big

Negative Total Return Over Fifteen Years!

So, while I can appreciate your dismay regarding the performance of your investment, I will point out that:

i) the key consideration is not past performance but how the characteristics of the asset class may be expected to fit into your portfolio requirements going forward.

ii) Expected income per unit in the fund has actually increased over the period, from $0.4643 in December 2012 to $0.5217 in June 2015 (see MAPF Performance: June 2015 ). This calculation is dependent upon various assumptions which you may or may not accept, but it represents my best guess!

iii) The increase in spreads over the period implies a significant reduction in expected income should you switch to another Fixed Income type of investment at this time.

iv) Expected future performance of FixedResets is highly geared to GOC-5, insofar as we can accept that the last equation on page 3 of the July PrefLetter extract reflects market reality. While I agree that we might be waiting a while for GOC-5 to increase substantially, I will suggest that current levels must be at or near a bottom. Mind you, I’ve been suggesting that continually for several years now and been wrong every time, so you may wish to disregard that particular exercise in market timing!

v) Expected future performance of Straights should be better than that of corporate long bonds over the medium term; and corporate long bonds should in turn outperform long Canadas; in both cases due to moderation of current high (by historical standards) spreads

I hope all this helps. I realize that I have used a fair bit of jargon in this eMail (and, what’s worse, jargon that I’ve developed myself!) so if there is anything in the above that makes no sense, feel free to ask for clarification. And, of course, if you would like to discuss this further prior to making an investment decision, that’s fine too – whether by eMail or telephone.

Sincerely,

James, thank you for this.

there is a definite dependence on prices for fixed resets on GOC-5 year yields. having said that, i’d add 2 points …

1. something you’ve mentioned before, canadian core inflation is running at 2%+ now. compared to a GoC 5 year yield of 0.75-0.80%. completely unsustainable. but when that changes, and how, who knows.

2. one can compare Canadian and US 5 and 10 year bond yields. it’s very rare for the Canadian rates to be BELOW US rates. i have slightly more data for 10 year Canadas than 5 year, but canadian 5 year yields are HALF US yields, and 10 year Canadas nearly 70 bps below US yields.

sorry. but no matter what, the bank of Canada can’t sustain these rates. not unless they want a 50 cent dollar.

I am very new (months) to this market but have experience in other markets. I have learned tremendously from reading Mr. Hymas who clearly understands this market, but is very careful to ensure his clients/readers make their own decisions. That is impressive.

My view, for what it is worth, is a confluence of factors have led this market to be “very out of favour” for a while:

1) Belated and then panic realization of impact of 5 year GOC’s by retail investors.

2) The “Enbridge” factor. While not a credit friendly transaction, Enbridge is still a fine company, but look at the yields (bozo yields, but still) on their prefs now (6%+ with attendant future reset risk/return, but healthy spreads). This is not a junk company, and these are real prefs, not quasi equity like the NVCC issues.

3) The squeeze occuring between bank common yields (4%ish) and the NVCC perp issues (5+% and rising rapidly) as investors realize there is little downside difference between the two instruments…so why not for 1% get some upside potential (but also downside MTM risk) with the common. When is the last time a Sched A bank reduced common dividends paid?

These things would work their way through a normal market, but the stunning thing for me is the illiquidity. Mr. Hymas points it out today with some of the price movements in FTS and TRP. Something is not functioning properly, but in that is an opportunity I think. Maybe a few people sold small lots on Friday afternoon before the long weekend. Smart buyer.

On a go forward basis, the yields on some of the preferred shares are simply and attractively high and one could not even approach these after tax yields in similar credit instruments. And while the 5 year GOC issue has been a liability for the last 6 months, it actually offers substantial protection in the future should the world change (3-5 years out).

Maybe we just clip the dividends for a year or so and ignore the MTM’s.

I will respond to these excellent comments some time soon, but in the interim I can’t resist one point …

The “Enbridge” factor.

Have a look at Chart FR-51 in the extract from PrefLetter. See those purple Pfd-2 group issues slap bang on top of the Pfd-3 regression line? That’s Enbridge!

So, one might say, they are basically fairly valued after taking into account a downgrade.

but is very careful to ensure his clients/readers make their own decisions.

As the girls say, who will buy the cow if I give away the milk?!

Also, I’m terrified of the potential for somebody blindly following what they think is my free advice and doing something that I would never, ever, recommend to anybody in their particular position. There are enough disclaimers on this site that I won’t be legally liable, but I don’t want that to happen to anybody anyway.

OMG…

I should have seen this discussion earlier before i jump into the pref market and get some lots of BMO.PR.Z and RY.PR.O. though IPO

🙁

Two weeks ago when i heard the news that the Bank of Canada is cutting interest rates again, i applied for these IPOs right away, hoping to generate some higer income than keeping my money in a savings account with negligible interest. But as soon as these news inssues come into the market, they have been sold off, i don’t even have a chance to get out and minimize my cpital loss.

I just can not understand why people are selling off the perpetual preferred shares nowadays even they have 5% plus dividend, compared to the 1% interest from a saving account, which is still going down.

So James, could you kindly give some further explanation about the recent sell-off of perpetual issues, and tell me what economic factors could make investors confidence come back?

Thanks.

Really appreciate your blog. The last time I posted was under some other name in 2008 when some wheels were coming off the financial bus and I was busy buying commercial paper at dirt cheap.

Different date same thing. Over the last four weeks I have been selling most of what I had and am aggressively buying prefs. It has been painful. But I think it will provide a good return for the 7-10 yr. time. If it does not maybe I’ll need to advertise for a small sleeping quarters in someones garage.

I retired at 51 (thanks to the 2007/08 mess) and my other half still works b/c of dedication and character. But we have a hard date for both of us to become useless. Prefs are allowing me to place some bets w/ fixed dates in mind. And I might say tucked away in TFSAs and RSPs they provide for some good income and cap gains.

My take on the market for prefs (and I know nothing, nothing) is that folks are selling to sell. BMO.PR.Q, from my perspective, is a good case in point.

Second take is that most folks look for that magic 4-5% stable return for themselves or their clients. And an under performer in that mindset gets wacked (EMA?).

Thanks for the blog

The last comment of BarleyandHops as well as the work done by Mr. Hymas is my view also. Reset Pref investors seem to want circa 4-5% yields almost irrespective of the GOC 5 year rate (within some upward bound of say 6% on the GOC 5 year maybe). Put in Mr. Hymas’ terms, the P (price) of the reset pref is almost totally dependent on the GOC 5 year rate after adjusting for credit. The implication for me of this is that currently longer dated resets with lower reset spreads (the type Mr. Hymas has been moving into) are very much a “coiled spring”. If over the next 3-5 years GOC rates return to the low end of normalized levels (2.5-3% let us say), almost all of these quality resets will spring back towards par. In some cases this could be a 40%ish capital gain or recoupment of unrealized losses. If rates stay near zero, well I think we have other problems and one would think return expectations of pref investors would eventually come down limiting the downside of the investment.

I have been trying to think of any other conventional retail financial instrument available which not only protect one from possible rising interest rates but actually allow one to gain from them and I cannot think of any although others may be able to. It seems the cost of the now present embedded option to participate in gains from possible higher interest rates with these resets, this may be heretical to say, very small or virtually zero because of the fat current yields, relative to other markets, that one is getting.

klargenf , its not only the pref shares that have sold off look at all the bank common or bce , igm , trp all of the are of their highs . are they acting as a leading indicator of higher rates ? as far as the nvcc bank issues selling off so much it seems to me it is way over done , if things get so bad that they are converted none of the bank common or pref will have much value

klargenf , its not only the pref shares that have sold off look at all the bank common or bce , igm , trp all of them are off their highs . are they acting as a leading indicator of higher rates ? as far as the nvcc bank issues selling off so much it seems to me it is way over done , if things get so bad that they are converted none of the bank common or pref will have much value ,prob not much else in the stock market will have much value either .

” If over the next 3-5 years GOC rates return to the low end of normalized levels (2.5-3% let us say), almost all of these quality resets will spring back towards par.”

one might think so, but that may not be the case.

not having a chance to elaborate last night, here goes…

let’s take FTS.pr.h as an example. trading at 16.15 (close today) with a 3.87% yield. so, it’s about 3% more than 5 year GOC.

this resets again in 2020? ok. so say, the 5 year GOC in 2020 is 5%. then this will reset at 6.45% of par, or have a new dividend of $1.625/yr.

well, ok, you say, that’s great. your dividend income has gone ballistic…. what about the price of the shares?

well, IF there is still a 3% spread between fixed resets and GOC 5 years, you’re looking at 8% yields on the resets, and the $1.6125 income would result in a $20.15 price for FTS.pr.h

if the spread goes back to relatively normal, say, 2%, the shares should be worth $23

this is a VERY simplistic approach, and i’m sure James will elaborate, and correct me if needed. but it’s not as simple as saying the preferred shares will bounce back to $25.

still, if you buy today these shares, and rates DO go to 5% … your YIELD on the investment will earn you nearly 10% on your original 16$

so, i’m personally looking NOT at the potential for capital gains, but the potential in increased dividend income … and 5% i would say is just a number i pulled out of the air. i have no real idea where rates will be in 5 years. my GUESS is higher. but 2%? 4%? who knows.

canadian core inflation is running at 2%+ now. compared to a GoC 5 year yield of 0.75-0.80%. completely unsustainable. but when that changes, and how, who knows.

Nestor, I agree completely.

it’s very rare for the Canadian rates to be BELOW US rates.

Again, I agree. If we can agree that long-term inflation is likely to be more or less the same, then US yields should get a reserve-currency discount while Canadian ones are hit with a commodity currency premium.

The squeeze occuring between bank common yields (4%ish) and the NVCC perp issues (5+% and rising rapidly)

Yes, David, this could well be a factor. RY common now has a yield of 4.03%, while the recently issued PerpetualDiscount, RY.PR.O now yields 5.19% at its bid price of 23.71.

Maybe what we need is a good old-fashioned made in Canada bank crisis to give people a little respect for first loss protection! It will happen someday!

Maybe we just clip the dividends for a year or so and ignore the MTM’s.

I think that’s most sensible. Asset allocation decisions should be made on the long-term characteristics of the asset classes.

Good day, what does first loss protection refer to ?

Thanks in advance…

“…then US yields should get a reserve-currency discount while Canadian ones are hit with a commodity currency premium. ”

and if we get a minority NDP government this fall, lol… i’m CERTAIN they won’t be able to keep rates lower than US rates.

what does first loss protection refer to ?

First loss protection refers to the subordination of the common stock to the preferred stock; up to some amount, X, any loss that is suffered by the company will be borne by the common shareholders, letting more senior suppliers of capital off the hook completely. The credit quality of preferred shares – and bonds, and anything else in the capital structure subordinated to common – is influenced by the size of X; the higher the better.

if we get a minority NDP government this fall

That will be really interesting!

I just can not understand why people are selling off the perpetual preferred shares nowadays even they have 5% plus dividend, compared to the 1% interest from a saving account, which is still going down.

As I commented with respect to TD.PF.F’s poor opening day, there’s other stuff around that I like more – the CU issues still look attractive!

But it is interesting, in view of the very high Seniority Spread that continues to puzzle me … a reasonable case can be made that the market hates straights because yields might go up, while hating FixedResets because yields might go down!

My take on the market for prefs (and I know nothing, nothing) is that folks are selling to sell.

Yes, I think you’re right. People see the value of their investment going down precipitously – an investment that, in many cases, was sold to them with an explanation that the Magic Reset would keep the price constant – and don’t understand why and head for the exits.

Second take is that most folks look for that magic 4-5% stable return for themselves or their clients.

You may well be right – certainly the constancy of the ~3.75% YTW for FixedResets over the past few years argues in favour of that notion.

I wonder if the sell off is also due to the declining Canadian dollar. Perhaps people feel it will drop further, and are simply pulling large amounts of their fixed income investments out of Canada, including prefer ends of all sorts.

The drop in the Canadian dollar would not explain why the US prefs, such as ENB.PR.U, are dropping as well. In fact these are very perplexing as the US 5 year rates are roughly equal to last year and the reset rate should be higher than when issued (if the trend continues) but the price keeps going down… I understand that the credit quality is not what is used to be, but the drop appears steep to me….

Another perplexing situation is the drop in prime related floaters such as BCE.PR.Y. These are also dropping like a rock and while I understand that the prime rate dropped, you would expect that these floating instruments would retain their value given that the appeal is maily based on the better tax treatment versus other short term instruments. At today’s pricing they yeld 4.2 % with no interest rate risk. Based on today’s BCE results, I don’t think that the default risk is any higher than it was last year but these dropped from 22$ to 16$… I have to admit it puzzles me…

I have been trying to think of any other conventional retail financial instrument available which not only protect one from possible rising interest rates but actually allow one to gain from them and I cannot think of any although others may be able to. It seems the cost of the now present embedded option to participate in gains from possible higher interest rates with these resets, this may be heretical to say, very small or virtually zero because of the fat current yields, relative to other markets, that one is getting.

That’s very well put. I’ll steal it sometime.

” If over the next 3-5 years GOC rates return to the low end of normalized levels (2.5-3% let us say), almost all of these quality resets will spring back towards par.”

one might think so, but that may not be the case.

Quite right. In the equation I derived in the PrefLetter extract, I assumed that EFCY (Expected Future Current Yield) was constant while GOC-5 was varied and this will not normally be the case. It is entirely possible that a rise in government five-year yields will be accompanied by a 1:1 increase in long-term preferred share yields, which would leave the price flat – although the yield would increase and PerpetualDiscounts would get hammered, so “flat” might look pretty good!

this is a VERY simplistic approach, and i’m sure James will elaborate, and correct me if needed. but it’s not as simple as saying the preferred shares will bounce back to $25.

still, if you buy today these shares, and rates DO go to 5% … your YIELD on the investment will earn you nearly 10% on your original 16$

Your calculations are good enough for the back of an envelope!

There may be a significant proportion of the market that agrees with you. I have noticed recently that Implied Volatilities of FixedReset series are increasing … this implies that lower-spread issues have been outperforming … which MAY BE because there is a little more buying pressure at the low end of the spectrum.

I wonder if the sell off is also due to the declining Canadian dollar.

It’s certainly possible, but I doubt it – foreign investors don’t get the benefit of the Dividend Tax Credit And Gross Up, so they have much less incentive to invest in preferred shares.

Which is not to say that they don’t! CNPF was a US-based Canadian preferred share ETF which, as noted by Assiduous Reader gsp, shut down in 2014 after attracting a pitiful $5.4-million in assets.