Canadian Utilities Limited has announced:

it has closed its previously announced public offering of Cumulative Redeemable Second Preferred Shares Series EE, by a syndicate of underwriters co-led by BMO Capital Markets and RBC Capital Markets, and including TD Securities Inc., Scotiabank, CIBC, Canaccord Genuity Corp., and GMP Securities L.P. Canadian Utilities Limited issued 5,000,000 Series EE Preferred Shares for gross proceeds of $125,000,000. The Series EE Preferred Shares will begin trading on the TSX today under the symbol CU.PR.H. The proceeds will be used for capital expenditures, to repay indebtedness and for other general corporate purposes.

CU.PR.H is a Straight Perpetual, 5.25%, announced July 27. It will be tracked by HIMIPref™ and is assigned to the PerpetualDiscount subindex.

The issue traded 12,380 (sic) shares today (consolidated exchanges) in a range of 23.87-00 before closing at 23.87-00. Vital Statistics are:

| CU.PR.H | Perpetual-Discount | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-07 Maturity Price : 23.55 Evaluated at bid price : 23.87 Bid-YTW : 5.52 % |

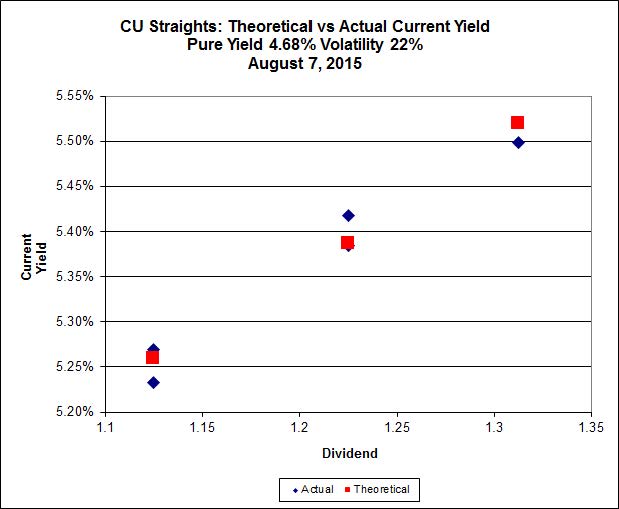

The PerpetualDiscounts index was down 1.96% from July 27 to August 7, so the drop in CU.PR.H from its issue price far exceeds the drop in the index. Implied Volatility theory suggests that CU.PR.H is now slightly preferable to other CU PerpetualDiscounts:

| Ticker | Dividend | Quote 2015-8-7 |

Bid Yield-to-Worst |

| CU.PR.D | 1.2250 | 22.75-99 | 5.38% |

| CU.PR.E | 1.225 | 22.61-95 | 5.41% |

| CU.PR.F | 1.125 | 21.35-39 | 5.28% |

| CU.PR.G | 1.125 | 21.50-59 | 5.24% |

| CU.PR.H | 1.3125 | 23.87-00 | 5.52% |

Click for Big

The fit to the curve is very good, but the Implied Volatility is very high at 22%. In a world in which all the assumptions of Implied Volatility theory are correct, this would suggest CU.PR.H will – on average, over all possible outcomes – outperform its siblings as Implied Volatility declines to a more reasonable level (say, about 15%). A decline in Implied Volatility (which would be reflected at a flattening of the curve in the chart) will also be expected simply from an increase in yields, even though this makes no sense.

There will be those who argue that market yields are more likely to decrease than to increase and which will leave us with the problem of estimating “how much of a decrease” and whether the relatively long period before a par call of CU.PR.H is possible compensates for it having the highest dividend rate. It’s never easy!

All in all, though, I’d say it’s a pretty good issue at the current price.