Employers added 215,000 jobs in July and the unemployment rate held at a seven-year low of 5.3 percent, a Labor Department report showed Friday in Washington. The gain in payrolls last month followed a 231,000 advance in June that was bigger than previously estimated.

…

While the data also showed a pickup in hours worked, average hourly earnings climbed a less-than-forecast 2.1 percent from a year earlier, indicating little momentum in wage growth.Retail and professional business services led the industries adding to headcounts in July, followed by health care and leisure and hospitality. Manufacturing payrolls rose by the most in six months on gains among non-durable goods producers. More jobs were also added in construction.

The report also showed a jump in full-time employment, while the number of part-time workers declined.

…

The average work week for all employees increased 6 minutes to 34.6 hours. A longer workweek often amounts to greater take-home pay for many employees.The labor force participation rate, which indicates the share of working-age people who are employed or looking for work, held at 62.6 percent.

Factories boosted payrolls by 15,000, the most since January. The gains were led by more hiring in the non-durables industries, including food, plastics and paper.

Retailers added almost 36,000 workers and employment in the health care and leisure industries each climbed by about 30,000 in July.

We have another hilarious example of the law of unintended consequences:

London’s swankiest neighborhoods of Knightsbridge and Belgravia are becoming no-go areas for even the wealthiest property investors.

They are being driven out by higher sales taxes introduced by Chancellor of the Exchequer George Osborne in December, which rise to as much as 12 percent of the cost of the most expensive homes.

Buying agent Camilla Dell says that her clients are spending an average of 2 million pounds ($3.1 million) less on each transaction this year and they’re more interested in cheaper areas such as Hackney and Shoreditch. That’s because an investor buying a 5 million-pound home pays almost 364,000 pounds more in tax than if they spent the same amount of money on 10 apartments costing 500,000 pounds each.

…

With investors now buying more homes in less expensive districts, prices below Osborne’s threshold are climbing and owner-occupiers, who should have benefited from his tax cuts, are being penalized, Dell said. The tax increases kick in at 937,000 pounds.“The very buyers Osborne was setting out to help, he’s put at a disadvantage,” she said. “At the same time, sales at the higher end have frozen. It was a very, very bad move.”

…

Investors who buy multiple apartments for about 500,000 pounds in London typically receive a rental yield of 4 percent to 5 percent, compared with about 2 percent for a luxury home in London’s best districts, Morris said.

And, interestingly with respect to Supply Management and the TPP, there is a global oversupply of milk:

Just months after the European Union lifted caps on milk production, there’s too much of it and some farmers are going broke. EU prices have tumbled to a five-year low, compounded by a global surplus and shrinking demand that’s disrupted exports. China is cutting back purchases and Russia, once the largest buyer of EU butter and cheese, halted imports last year in retaliation for sanctions over its conflict with Ukraine.

…

An EU gauge tracking consumer prices for milk, cheese and eggs has dropped 2.1 percent from last year. Retail prices for whole milk in France fell 5.6 percent since last year, according to the latest government data from June.With prices so low, there’s little incentive for European producers to increase supply, even after EU regulators in April ended a system that had capped production for 30 years. This year, the EU expects output to rise 1 percent to 161.4 million tons.

The removal of quotas marked a change to an open-market system. Before the limits, government purchases of surpluses were intended to aid farmers but instead led to overproduction.

…

The plunge in dairy costs helped push down a gauge of global food prices in July to the lowest since September 2009, the United Nations’ Food & Agriculture Organization said Thursday.

It’s nice to see Rob Ford fairly treated:

DBRS notes that the City’s operating fiscal discipline has improved notably in recent years, with nearly $1.0 billion in ongoing operational savings or efficiencies achieved from 2011 to 2014 through a comprehensive service review process and through negotiated provisions in collective agreements.

There’s more fuss at the SEC about the Pay-Ratio Disclosure Rule discussed August 5, with Piwowar adding to his remarks:

The pay ratio disclosure rulemaking has flaws throughout. I further enumerate a number of those defects below.

I. The Proposing Release did not provide sufficient notice under the Administrative Procedure Act.[2]

…

II. Once the Commission decided what objectives Section 953(b) was intended to accomplish, it failed to publicly disclose such understanding prior to adoption.

…

III. The Commission failed to consider what the quantitative effects of providing flexibility would be on the accuracy of the pay ratio. By not evaluating such quantitative effects, the Commission acted in an arbitrary and capricious manner when it limited the de minimis exclusion of non-U.S. employees to 5%.

…

IV. The Commission acted arbitrarily and capriciously when it defined “employee” to include contract workers only if they are employed by an unaffiliated third party.

…

V. The Commission’s economic analysis failed to consider academic studies as to whether the pay ratio might create pressure to increase CEO compensation.

…

VI. Use of the pay ratio for comparative purposes among companies may violate an investment adviser’s fiduciary duty under the Investment Advisers Act of 1940.[69]

…

VII. ConclusionI have many objections to the pay ratio disclosure, as set forth in my remarks at the Commission’s open meeting and my comments above. Should the final rule become effective, I have one request for companies. Please keep track of your compliance costs and consider voluntarily disclosing that information alongside your pay ratio. The Commission and others should have an understanding of your actual compliance costs, and voluntary disclosures would make the likely incredibly high costs evident. But even then, be careful; such information must be “clearly identified, not misleading, and not presented with greater prominence than the required ratio.”[76]

It was a positive day for the Canadian preferred share market, with PerpetualDiscounts winning 32bp, FixedResets up 5bp and DeemedRetractibles gaining 2bp. PerpetualDiscounts were notable on the good side of the Performance Highlights table. Volume was very low.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

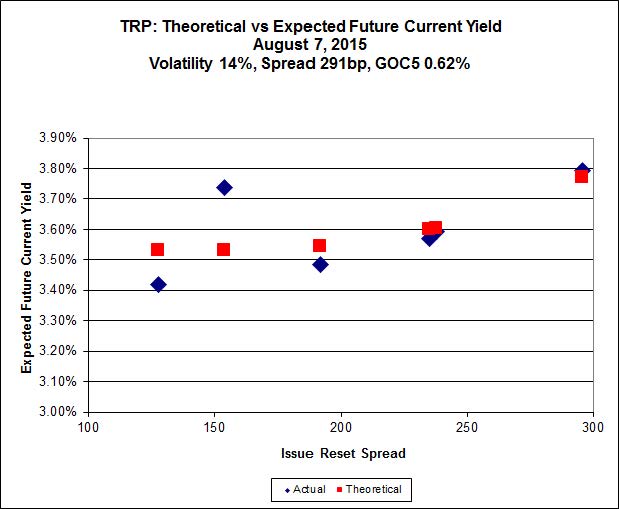

Here’s TRP:

Click for Big

TRP.PR.B, which resets 2020-6-30 at +128, is bid at 13.90 to be $0.44 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $0.84 cheap at its bid price of 14.50.

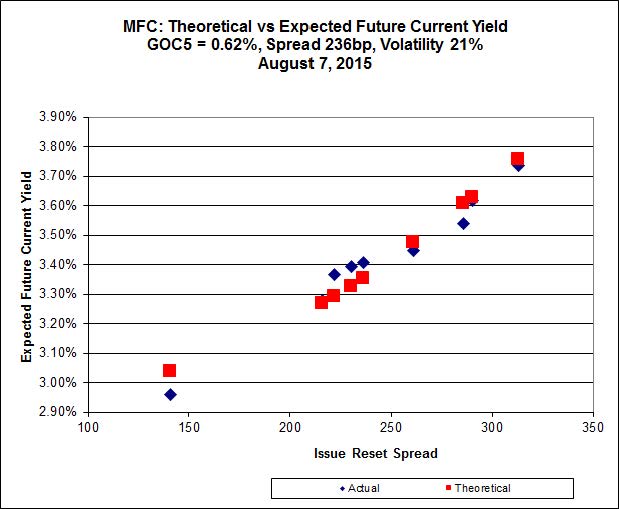

Click for Big

Another good fit today!

Most expensive is MFC.PR.I, resetting at +286bp on 2017-9-19, bid at 24.58 to be 0.46 rich, while MFC.PR.K, resetting at +222bp on 2018-9-19, is bid at 21.09 to be $0.49 cheap.

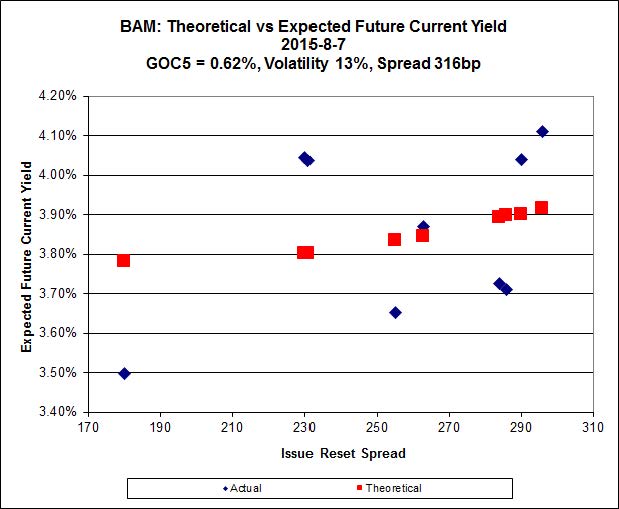

Click for Big

The fit on the BAM issues continues to be horrible.

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 18.05 to be $1.16 cheap. BAM.PR.X, resetting at +180bp on 2017-6-30 is bid at 17.30 and appears to be $1.30 rich.

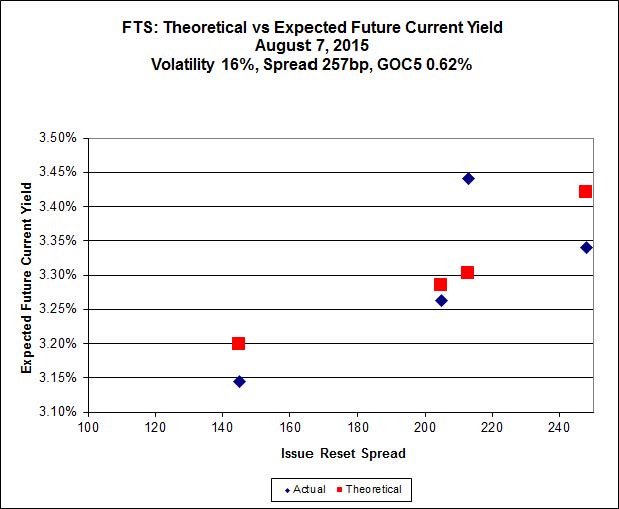

Click for Big

FTS.PR.K, with a spread of +205bp, and bid at 20.46, looks $0.54 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 19.98 and is $0.84 cheap.

Click for Big

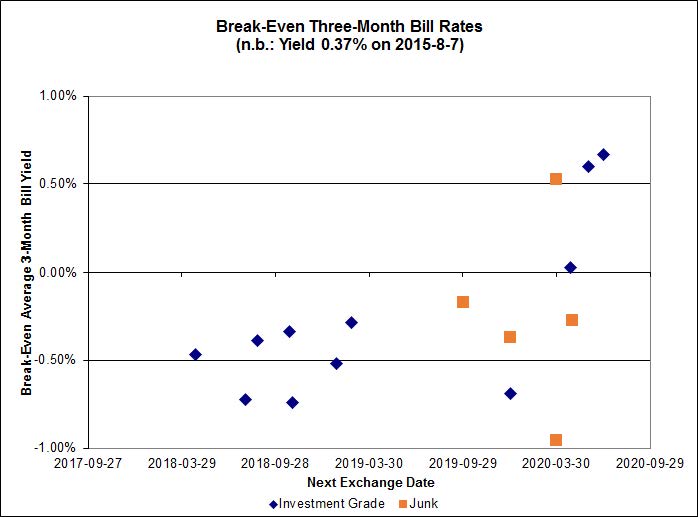

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.08%, with one outlier above 1.00%. There is one junk outlier below -1.00%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.5846 % | 2,024.3 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.5846 % | 3,539.4 |

| Floater | 3.62 % | 3.66 % | 55,008 | 18.12 | 3 | -0.5846 % | 2,152.0 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.2819 % | 2,774.8 |

| SplitShare | 4.59 % | 4.80 % | 57,506 | 3.14 | 3 | 0.2819 % | 3,251.9 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.2819 % | 2,537.3 |

| Perpetual-Premium | 5.72 % | 5.33 % | 65,963 | 2.08 | 9 | 0.0000 % | 2,484.9 |

| Perpetual-Discount | 5.40 % | 5.41 % | 81,815 | 14.82 | 29 | 0.3250 % | 2,610.5 |

| FixedReset | 4.71 % | 3.80 % | 207,666 | 16.08 | 87 | 0.0480 % | 2,232.4 |

| Deemed-Retractible | 5.12 % | 5.17 % | 104,809 | 5.46 | 34 | 0.0195 % | 2,579.6 |

| FloatingReset | 2.33 % | 3.27 % | 45,369 | 6.02 | 9 | -0.2134 % | 2,252.0 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| TRP.PR.F | FloatingReset | -2.97 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-07 Maturity Price : 16.35 Evaluated at bid price : 16.35 Bid-YTW : 3.53 % |

| TRP.PR.A | FixedReset | -1.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-07 Maturity Price : 18.22 Evaluated at bid price : 18.22 Bid-YTW : 3.70 % |

| ENB.PR.J | FixedReset | -1.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-07 Maturity Price : 17.31 Evaluated at bid price : 17.31 Bid-YTW : 5.00 % |

| MFC.PR.N | FixedReset | -1.65 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.52 Bid-YTW : 5.34 % |

| ENB.PR.Y | FixedReset | -1.58 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-07 Maturity Price : 16.78 Evaluated at bid price : 16.78 Bid-YTW : 4.84 % |

| HSE.PR.A | FixedReset | -1.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-07 Maturity Price : 14.81 Evaluated at bid price : 14.81 Bid-YTW : 4.09 % |

| MFC.PR.G | FixedReset | -1.30 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.33 Bid-YTW : 4.04 % |

| SLF.PR.G | FixedReset | -1.26 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.46 Bid-YTW : 7.25 % |

| ENB.PR.T | FixedReset | -1.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-07 Maturity Price : 16.70 Evaluated at bid price : 16.70 Bid-YTW : 4.99 % |

| ELF.PR.H | Perpetual-Discount | 1.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-07 Maturity Price : 24.31 Evaluated at bid price : 24.80 Bid-YTW : 5.58 % |

| BAM.PF.F | FixedReset | 1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-07 Maturity Price : 22.58 Evaluated at bid price : 23.45 Bid-YTW : 3.87 % |

| CU.PR.E | Perpetual-Discount | 1.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-07 Maturity Price : 22.24 Evaluated at bid price : 22.61 Bid-YTW : 5.41 % |

| FTS.PR.G | FixedReset | 1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-07 Maturity Price : 19.98 Evaluated at bid price : 19.98 Bid-YTW : 3.67 % |

| FTS.PR.F | Perpetual-Discount | 1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-07 Maturity Price : 23.02 Evaluated at bid price : 23.30 Bid-YTW : 5.34 % |

| RY.PR.J | FixedReset | 1.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-07 Maturity Price : 22.72 Evaluated at bid price : 23.85 Bid-YTW : 3.45 % |

| BMO.PR.W | FixedReset | 1.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-07 Maturity Price : 21.63 Evaluated at bid price : 21.95 Bid-YTW : 3.39 % |

| FTS.PR.H | FixedReset | 1.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-07 Maturity Price : 16.46 Evaluated at bid price : 16.46 Bid-YTW : 3.28 % |

| CU.PR.G | Perpetual-Discount | 1.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-07 Maturity Price : 21.50 Evaluated at bid price : 21.50 Bid-YTW : 5.24 % |

| TRP.PR.D | FixedReset | 1.36 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-07 Maturity Price : 20.88 Evaluated at bid price : 20.88 Bid-YTW : 3.78 % |

| CU.PR.F | Perpetual-Discount | 2.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-07 Maturity Price : 21.35 Evaluated at bid price : 21.35 Bid-YTW : 5.28 % |

| ENB.PR.F | FixedReset | 2.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-07 Maturity Price : 16.71 Evaluated at bid price : 16.71 Bid-YTW : 4.92 % |

| TRP.PR.C | FixedReset | 2.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-07 Maturity Price : 14.45 Evaluated at bid price : 14.45 Bid-YTW : 3.73 % |

| POW.PR.B | Perpetual-Discount | 6.95 % | Rebounding most of the way from yesterday‘s nonsense. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-07 Maturity Price : 23.71 Evaluated at bid price : 24.02 Bid-YTW : 5.61 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BNS.PR.M | Deemed-Retractible | 132,649 | TD crossed blocks of 50,000 and 75,200, both at 25.20. YTW SCENARIO Maturity Type : Call Maturity Date : 2016-07-27 Maturity Price : 25.00 Evaluated at bid price : 25.19 Bid-YTW : 3.79 % |

| BNS.PR.Z | FixedReset | 105,620 | Nesbitt crossed 22,900 at 22.60; TD crossed 74,100 at the same price. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.64 Bid-YTW : 3.80 % |

| HSB.PR.C | Deemed-Retractible | 100,500 | Scotia crossed 100,000 at 25.20. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.10 Bid-YTW : 5.15 % |

| FTS.PR.H | FixedReset | 65,560 | RBC crossed 49,400 at 16.55. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-07 Maturity Price : 16.46 Evaluated at bid price : 16.46 Bid-YTW : 3.28 % |

| BNS.PR.B | FloatingReset | 51,650 | TD crossed 50,000 at 23.18. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.18 Bid-YTW : 3.27 % |

| CU.PR.G | Perpetual-Discount | 50,541 | RBC bought 25,000 from anonymous at 21.50. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-07 Maturity Price : 21.50 Evaluated at bid price : 21.50 Bid-YTW : 5.24 % |

| There were 18 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| GWO.PR.N | FixedReset | Quote: 16.12 – 17.00 Spot Rate : 0.8800 Average : 0.5782 YTW SCENARIO |

| MFC.PR.L | FixedReset | Quote: 21.21 – 22.00 Spot Rate : 0.7900 Average : 0.5006 YTW SCENARIO |

| BAM.PR.N | Perpetual-Discount | Quote: 21.23 – 21.67 Spot Rate : 0.4400 Average : 0.2691 YTW SCENARIO |

| MFC.PR.M | FixedReset | Quote: 21.87 – 22.25 Spot Rate : 0.3800 Average : 0.2400 YTW SCENARIO |

| BAM.PR.M | Perpetual-Discount | Quote: 21.21 – 21.60 Spot Rate : 0.3900 Average : 0.2737 YTW SCENARIO |

| MFC.PR.C | Deemed-Retractible | Quote: 21.41 – 21.96 Spot Rate : 0.5500 Average : 0.4481 YTW SCENARIO |