Matt Levine writes a good piece on bond market ethics, whatever those are:

And Edward Jones’s behavior seems to have been even worse than that: It didn’t just put the bonds in inventory, wait until they started trading, and hope to flip them for a profit (which would be bad!); it actually sometimes sold bonds to customers at prices above the offering price while the offering was still going on.5 As far as I can tell, this worked mostly because customers didn’t know any better, and Edward Jones didn’t tell them.6 (There’s no suggestion that Edward Jones lied to the customers about the price it paid, though.)

…

The real point here is that there is a “well-established industry practice” that, if you’re an underwriter for municipal bonds, and you buy bonds from the issuer at the offer price,8 you have to re-sell them to customers at the offer price. You just can’t do what Edward Jones did.

I’d say the party injured by Edward Jones’ misconduct is not the customers – who were buying from the broker as principal and knew this – but the issuer. The underwriters are acting as agents for the issuer and are paid a commission for doing so. If the underwriters then turn around and skimming off the concession for themselves, then it seems to me they have a powerful incentive to give their client – to whom yes, they have a fiduciary obligation – some very gloomy advice about how difficult it will be to sell the issue and how big, therefore, the concession should be.

New Zealand demonstrates good news for Canadian housing markets:

Auckland home prices are up more than 20 percent in the past year. If you’re a buyer from China or the U.S., they’re not.

The slump in New Zealand’s currency has made properties in the country’s largest city a bargain for foreigners, creating a headache for central bank Governor Graeme Wheeler, who has been trying to put a lid on the country’s overheated property market.

“Five years ago I would have estimated two or three percent of Auckland properties were bought from overseas,” said Peter Thompson, managing director of Barfoot & Thompson, which says it sells one-in-three homes in the so-called City of Sails. “These days it’s 10 or 12 percent.”

Wheeler has lowered interest rates to offset faltering economic growth and weaken the currency, but the cuts are stoking Auckland’s housing prices, which are already the second highest relative to income among developed economies. Worse still, with foreign buyers tripling their participation in the city of 1.5 million people, the price surge is starting to spread to cheaper neighboring regions.

…

The main opposition Labour Party last month claimed that 40 percent of Auckland house sales between February and April were purchased by people with Chinese-sounding names, and criticized the government for soaring prices.While the claim drew accusations of xenophobic politics, a subsequent poll of 1,000 voters showed 61 percent wanted the government to ban non-resident foreigners from buying houses.

Meanwhile, PrefBlog’s Better Living Through Technology Departments highlights a good news story from Saudi Arabia:

If she had chosen the traditional route to opening her accessories business in Jeddah, Rozana al-Daini would have had to enlist a male sponsor to represent her before government agencies and sign official documents on her behalf.

Instead, she sells jewelry, watches and wallets on Instagram, where Saudi businesswomen can avoid the gender restrictions they face in the kingdom. Her two-year-old business, Accessories_ar, has two employees, 67,000 followers and handles up to 25 orders a day. It also provides her with the ultimate empowerment: her own income.

…

Saudis spend an average of 2.65 hours per day social networking, compared to a global average of 1.69 hours, according to a survey this year by London-based market research firm GlobalWebIndex. Saudi Arabia also ranked first in the world for Twitter penetration, according to a 2013 study by Amsterdam-based PeerReach. The GlobalWebIndex survey found that nearly half of Saudi Internet users are members of Instagram, compared with a global average of 23 percent.While entrepreneurs also use Twitter and other social networks, al-Daini said Instagram’s photo-based interface was a natural fit for her business. “The photography affects people,” she said.

Designed for smartphones, the application provides an easy way for creative Saudis to share their talent, Moustakas said.

It was yet another grim day for the Canadian preferred share market, with PerpetualDiscounts losing 42bp, FixedResets down 41bp and DeemedRetractibles off 9bp. TRP issues continue to be notable in the Performance Highlights table, mostly in a bad way. Volume was very low.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

Here’s TRP:

Click for Big

TRP.PR.A, which resets 2019-12-31 at +192, is bid at 17.15 to be $0.51 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $0.83 cheap at its bid price of 13.41.

Click for Big

Another good fit today!

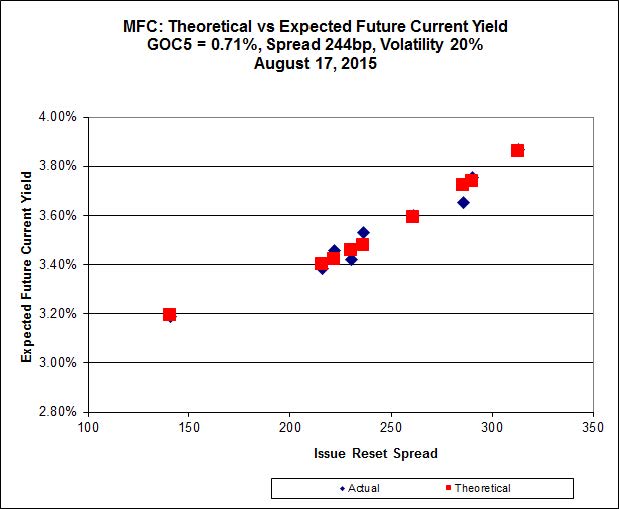

Most expensive is MFC.PR.I, resetting at +286bp on 2017-9-19, bid at 24.45 to be 0.46 rich, while MFC.PR.M, resetting at +236bp on 2019-12-19, is bid at 21.75 to be $0.31 cheap.

Click for Big

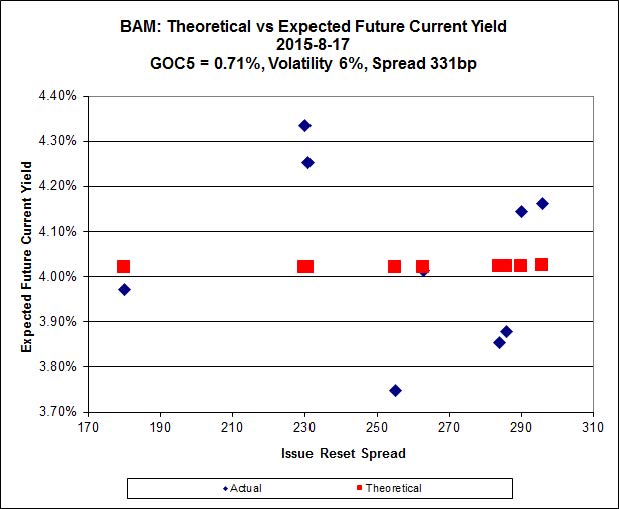

The fit on the BAM issues continues to be horrible.

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 17.36 to be $1.36 cheap. BAM.PF.E, resetting at +255bp on 2020-3-31 is bid at 21.75 and appears to be $1.48 rich.

Click for Big

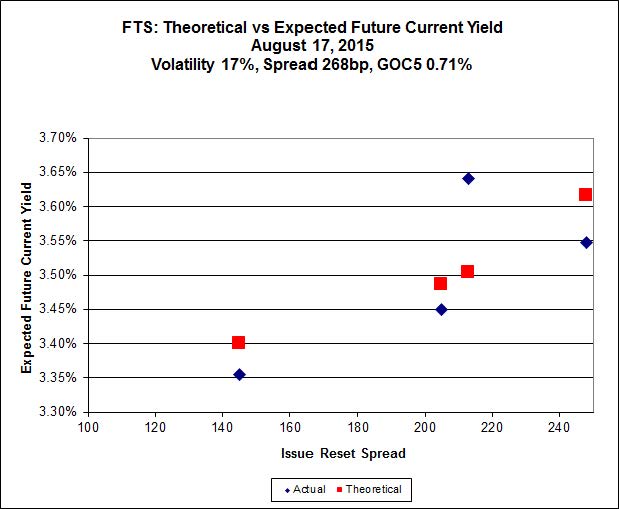

FTS.PR.M, with a spread of +248bp, and bid at 22.48, looks $0.43 expensive and resets 2019-12-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 19.50 and is $0.77 cheap.

Click for Big

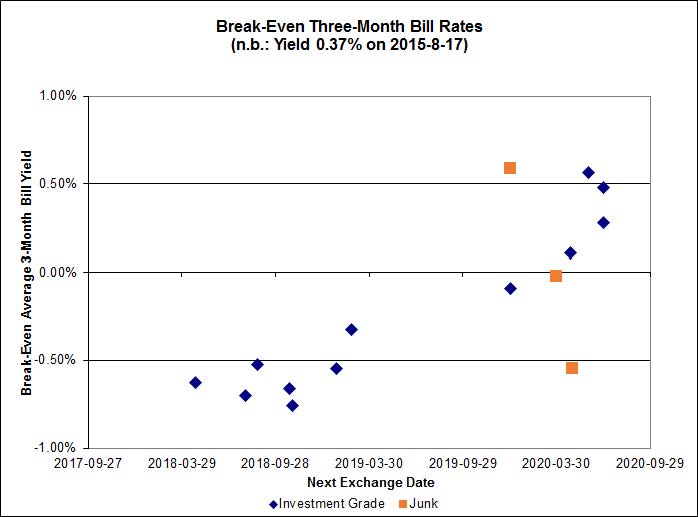

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.23%, with no outliers. Note that the distribution is bimodal, with NVCC non-compliant bank issues averaging -0.53% and the unregulated issues averaging +0.36%. There are three junk outliers below -1.00% and one above +1.00%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 1.3613 % | 2,004.1 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 1.3613 % | 3,504.2 |

| Floater | 3.66 % | 3.72 % | 52,700 | 17.98 | 3 | 1.3613 % | 2,130.5 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0134 % | 2,777.4 |

| SplitShare | 4.58 % | 4.85 % | 54,982 | 3.12 | 3 | 0.0134 % | 3,254.9 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0134 % | 2,539.6 |

| Perpetual-Premium | 5.72 % | 5.38 % | 60,327 | 2.06 | 9 | -0.0265 % | 2,483.7 |

| Perpetual-Discount | 5.43 % | 5.48 % | 80,043 | 14.69 | 29 | -0.4176 % | 2,604.3 |

| FixedReset | 4.77 % | 3.91 % | 196,690 | 15.90 | 87 | -0.4096 % | 2,211.9 |

| Deemed-Retractible | 5.11 % | 5.25 % | 98,641 | 5.43 | 34 | -0.0924 % | 2,587.0 |

| FloatingReset | 2.35 % | 3.29 % | 47,365 | 5.99 | 9 | 0.0199 % | 2,246.3 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| TRP.PR.C | FixedReset | -2.97 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-17 Maturity Price : 13.41 Evaluated at bid price : 13.41 Bid-YTW : 3.99 % |

| ELF.PR.H | Perpetual-Discount | -2.95 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-17 Maturity Price : 23.57 Evaluated at bid price : 24.02 Bid-YTW : 5.77 % |

| ENB.PR.F | FixedReset | -2.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-17 Maturity Price : 15.83 Evaluated at bid price : 15.83 Bid-YTW : 5.08 % |

| HSE.PR.A | FixedReset | -2.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-17 Maturity Price : 14.20 Evaluated at bid price : 14.20 Bid-YTW : 4.24 % |

| TRP.PR.D | FixedReset | -1.99 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-17 Maturity Price : 19.21 Evaluated at bid price : 19.21 Bid-YTW : 4.11 % |

| TRP.PR.B | FixedReset | -1.98 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-17 Maturity Price : 12.90 Evaluated at bid price : 12.90 Bid-YTW : 3.74 % |

| FTS.PR.F | Perpetual-Discount | -1.91 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-17 Maturity Price : 22.22 Evaluated at bid price : 22.50 Bid-YTW : 5.45 % |

| GWO.PR.N | FixedReset | -1.83 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.05 Bid-YTW : 7.37 % |

| TD.PF.D | FixedReset | -1.73 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-17 Maturity Price : 22.69 Evaluated at bid price : 23.81 Bid-YTW : 3.51 % |

| FTS.PR.G | FixedReset | -1.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-17 Maturity Price : 19.50 Evaluated at bid price : 19.50 Bid-YTW : 3.67 % |

| ELF.PR.F | Perpetual-Discount | -1.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-17 Maturity Price : 23.33 Evaluated at bid price : 23.61 Bid-YTW : 5.67 % |

| CU.PR.C | FixedReset | -1.47 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-17 Maturity Price : 22.45 Evaluated at bid price : 22.80 Bid-YTW : 3.30 % |

| TRP.PR.A | FixedReset | -1.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-17 Maturity Price : 17.15 Evaluated at bid price : 17.15 Bid-YTW : 3.92 % |

| MFC.PR.L | FixedReset | -1.40 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.20 Bid-YTW : 5.28 % |

| FTS.PR.M | FixedReset | -1.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-17 Maturity Price : 22.00 Evaluated at bid price : 22.48 Bid-YTW : 3.58 % |

| IFC.PR.C | FixedReset | -1.22 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.05 Bid-YTW : 5.60 % |

| ENB.PR.Y | FixedReset | -1.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-17 Maturity Price : 16.50 Evaluated at bid price : 16.50 Bid-YTW : 4.81 % |

| RY.PR.H | FixedReset | -1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-17 Maturity Price : 21.86 Evaluated at bid price : 22.25 Bid-YTW : 3.37 % |

| MFC.PR.M | FixedReset | -1.14 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.75 Bid-YTW : 5.13 % |

| SLF.PR.C | Deemed-Retractible | -1.06 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.37 Bid-YTW : 6.66 % |

| BAM.PR.B | Floater | 1.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-17 Maturity Price : 13.15 Evaluated at bid price : 13.15 Bid-YTW : 3.63 % |

| BAM.PR.C | Floater | 1.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-17 Maturity Price : 12.75 Evaluated at bid price : 12.75 Bid-YTW : 3.74 % |

| TRP.PR.G | FixedReset | 1.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-17 Maturity Price : 22.09 Evaluated at bid price : 22.70 Bid-YTW : 3.91 % |

| PWF.PR.T | FixedReset | 1.47 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-17 Maturity Price : 22.96 Evaluated at bid price : 24.10 Bid-YTW : 3.17 % |

| BAM.PR.K | Floater | 1.75 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-17 Maturity Price : 12.82 Evaluated at bid price : 12.82 Bid-YTW : 3.72 % |

| ENB.PF.G | FixedReset | 1.85 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-17 Maturity Price : 18.20 Evaluated at bid price : 18.20 Bid-YTW : 4.89 % |

| VNR.PR.A | FixedReset | 2.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-17 Maturity Price : 20.43 Evaluated at bid price : 20.43 Bid-YTW : 4.30 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| RY.PR.J | FixedReset | 121,480 | RBC crossed 32,200 at 23.85, then another 49,800 at 23.77. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-17 Maturity Price : 22.68 Evaluated at bid price : 23.75 Bid-YTW : 3.46 % |

| BAM.PR.T | FixedReset | 109,200 | Scotia crossed blocks of 49,100 and 50,000, both at 17.80. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-17 Maturity Price : 17.75 Evaluated at bid price : 17.75 Bid-YTW : 4.32 % |

| BMO.PR.Z | Perpetual-Discount | 72,655 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-17 Maturity Price : 24.18 Evaluated at bid price : 24.55 Bid-YTW : 5.12 % |

| TD.PF.D | FixedReset | 61,525 | RBC crossed 50,000 at 24.15. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-17 Maturity Price : 22.69 Evaluated at bid price : 23.81 Bid-YTW : 3.51 % |

| TD.PF.E | FixedReset | 34,200 | RBC bought 10,000 from Scotia at 24.70. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-17 Maturity Price : 23.01 Evaluated at bid price : 24.61 Bid-YTW : 3.44 % |

| ENB.PR.H | FixedReset | 24,600 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-17 Maturity Price : 15.05 Evaluated at bid price : 15.05 Bid-YTW : 4.82 % |

| There were 18 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| ELF.PR.H | Perpetual-Discount | Quote: 24.02 – 24.75 Spot Rate : 0.7300 Average : 0.4377 YTW SCENARIO |

| GWO.PR.S | Deemed-Retractible | Quote: 24.86 – 25.45 Spot Rate : 0.5900 Average : 0.3977 YTW SCENARIO |

| PWF.PR.O | Perpetual-Premium | Quote: 25.52 – 26.19 Spot Rate : 0.6700 Average : 0.4989 YTW SCENARIO |

| TD.PF.D | FixedReset | Quote: 23.81 – 24.30 Spot Rate : 0.4900 Average : 0.3228 YTW SCENARIO |

| HSB.PR.D | Deemed-Retractible | Quote: 24.86 – 25.36 Spot Rate : 0.5000 Average : 0.3624 YTW SCENARIO |

| SLF.PR.C | Deemed-Retractible | Quote: 21.37 – 21.82 Spot Rate : 0.4500 Average : 0.3264 YTW SCENARIO |