In order to address an alarming shortage of employment opportunities for bureaucrats, the OECD has inaugurated publication of the OECD Business and Finance Outlook. The full publication is here; it’s a long paean to the glories of state intervention.

I’ve seen a lot of whining in the press about the effect of Chinese buying on the price of Vancouver real-estate, but in Sydney, Australia, it’s a full-court press:

Since announcing a crackdown on unlawful home purchases in February, the government has forced only one foreigner to sell up. Chinese already buy almost a quarter of new homes in Sydney and their outlay will more than double to A$60 billion ($46 billion) in the six years to 2020, according to Credit Suisse Group AG.

“Forget the anti-corruption,” said Ray Chan, managing director of Sydney-based Henson Properties, which sells homes almost exclusively to Chinese. “A lot of money is coming through.”

Amid concern that offshore demand is pricing locals out of the market, Treasurer Joe Hockey plans bigger fines and jail time for those flouting restrictions. Yet more than six months after a parliamentary inquiry called for a national register of the citizenship of buyers, the database is still a work in progress — leaving officials with no firm grasp of the scale of overseas purchases.

We don’t really like competition, do we?

And Bloomberg introduces us to a real live compliance guy:

Several tax brackets down from [JPMorgan Chase CEO Jamie] Dimon, Justin “the Compliance Guru” Hall is betting that Dimon’s scourge will, by contrast, ensure his own upward mobility. Hall, 28, is a compliance officer at Charles Schwab Corp.’s retail bank. He and thousands of others like him, at every company in finance, are charged with keeping their revenue-obsessed colleagues on the right side of the rules. Compliance, not banking, has been the real growth business since 2008, when free-market liberties turned to liabilities and markets collapsed.

Hall, who uses the self-awarded “guru” designation on his LinkedIn profile, couldn’t be happier with his choice of career. “There’s definitely no shortage of opportunity,” he says. “You’re usually involved with all the big dogs in the company. Your visibility is huge.”

…

Compliance types point to these big numbers [of post-crisis fines paid] as proof that hiring a few of their ilk really pays off. JPMorgan has hired 8,000 compliance and control people since the crisis. Employees completed 800,000 hours of compliance training in the bank’s mortgage business alone in 2014.

…

In another era, someone like Justin Hall might have gone into plastics, or semiconductors, to make his fortune. Growing up in Chandler, Arizona, Hall spent half his time living in a trailer park with one of his divorced parents. He sold phone books and magazines door-to-door, then switched to selling phone service for WorldCom, where his charm helped him pull down $98,000 the year he turned 17. “I have a knack for picking up people’s cues,” he says.He got into financial services in 2005 at age 18, right out of high school, through a neighbor who worked at Bank of America and told him about a job there as a credit risk analyst. After a promotion, Hall ended up on a BofA team examining Countrywide Financial and its assets before the bank took a $2 billion stake in the troubled lender in 2007. That got him into compliance. He went to college, earning a bachelor’s degree in project management and finance from the University of Phoenix in 2012 and a master’s in management of information systems from Arizona State in 2014. He joined Schwab’s in-house bank, based in Phoenix, in October, working on an oversight program for ensuring that third-party vendors comply with banks’ risk regulations.

So the 800,000 hours of compliance training (at what? Maybe $50 per hour?) and 8,000 compliance and control people (at what? Maybe $75,000 each per year?) are only the tip of the iceberg. We’ve got guys like Justin Hall, obviously a real go-getter with a knack for sales, going into the ticky-box business because that’s where the action is. What a waste. What a completely useless drag on society. And, remember, pointing at those huge fine numbers to justify the expense assumes that (i) the fines would have been avoided with the big compliance push, and (ii) the fines represent an actual business cost, rather than a completely disproportionate (as discussed on June 10) element of the war on banks.

And there’s a report brewing that will probably serve to provide a fig-leaf for yet more regulation:

Regulators including the Fed and the Treasury Department are working on a report analyzing liquidity, including the events of Oct. 15, 2014, when yields on 10-year Treasuries plunged the most since 2009.

If rising interest rates prompt investors to flee debt markets, bank bonds could be the hardest hit among corporate securities, according to Bank of America Corp.

“We’re now moving into an environment of outflows, which means a lot of investors are going to have to sell bonds for an extended period of time,” Hans Mikkelsen, head of U.S. investment-grade credit strategy at Bank of America Merrill Lynch, said in a telephone interview.

Investors will have to ignore the fundamental fact that higher rates and a stronger economy are actually good for banks, he said, because they’ll just have to offload what they can.

Two factors make bank bonds an easy sell: they are widely owned and actively traded. A Bank of America survey of 94 credit investors last month showed a majority were overweight bank bonds. Trading in bank bonds made up more than 30 percent of the total volume of corporate debt traded in the past three months, according to Trace, the bond-price reporting system of the Financial Industry Regulatory Authority.

…

That’s one reason bank bonds are attractive to investors. Banks including JPMorgan Chase & Co., Citigroup Inc. and Goldman Sachs Group Inc. have sold $1.3 trillion of bonds since the financial crisis, according to data compiled by Bloomberg. That’s a fifth of the total $6.5 trillion investment-grade bonds issued in that period.Six of America’s biggest banks — JPMorgan, Bank of America, Goldman Sachs, Morgan Stanley, Citigroup and Wells Fargo & Co. — are among the top 11 most actively traded names in the corporate-bond market over the past three months, Trace data show.

I’m not sure I buy that. If there’s selling pressure on bank bonds, there will be pressure on everything else. After all, if we start with a ‘fair’ market and your bank bond then goes down $1 while the quote on your less-liquid industrial bond goes down $0.50, you’re going to try to sell the industrial bond. But you won’t be able to: as soon as you get on the ‘phone, the quote’s going to drop another buck as the traders adjust their pricing matrix. This warning implicitly assumes that in a tight liquidity environment, the liquidity (price) premium is going to change to a discount, and that’s a little hard to swallow.

It was another mixed day for the Canadian preferred share market, with PerpetualDiscounts down 26bp, FixedResets gaining 4bp and DeemedRetractibles off 4bp. Floaters got hammered. The Performance Highlights table reveals that beneath the very calm overall index result is a violent maelstrom of churning FixedResets. Volume was on the low side of average.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

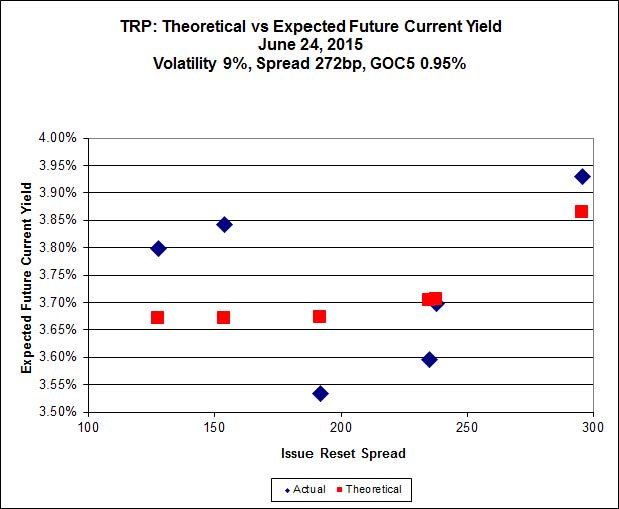

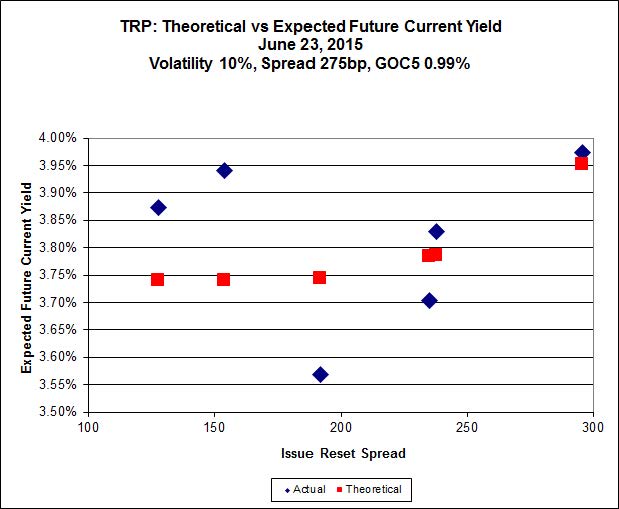

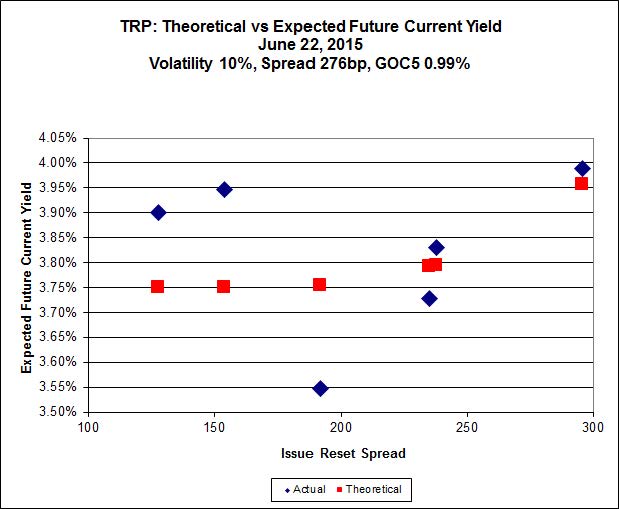

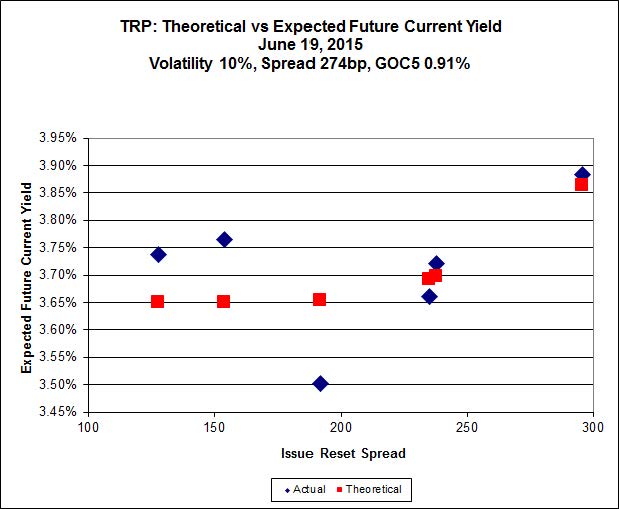

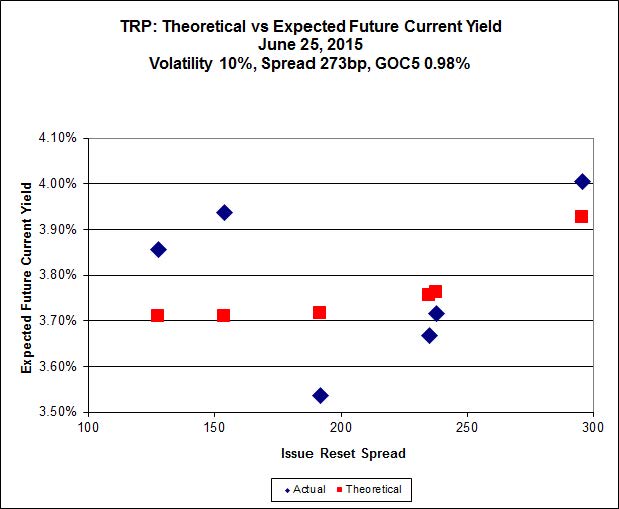

Here’s TRP:

Click for Big

TRP.PR.A, which resets 2019-12-31 at +192, is bid at 20.50 to be $0.98 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $0.98 cheap at its bid price of 16.00.

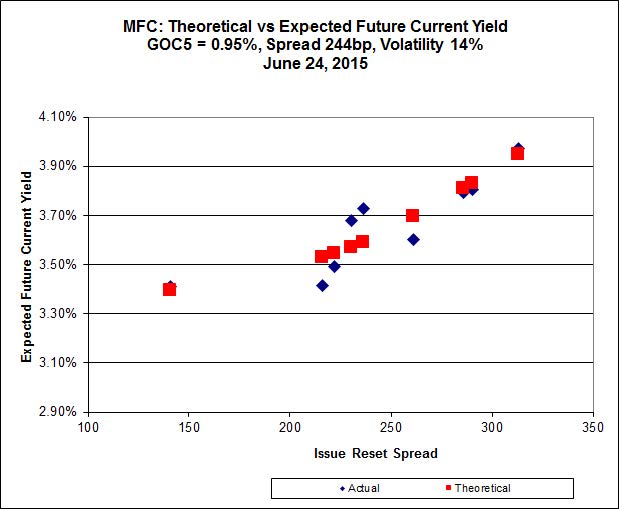

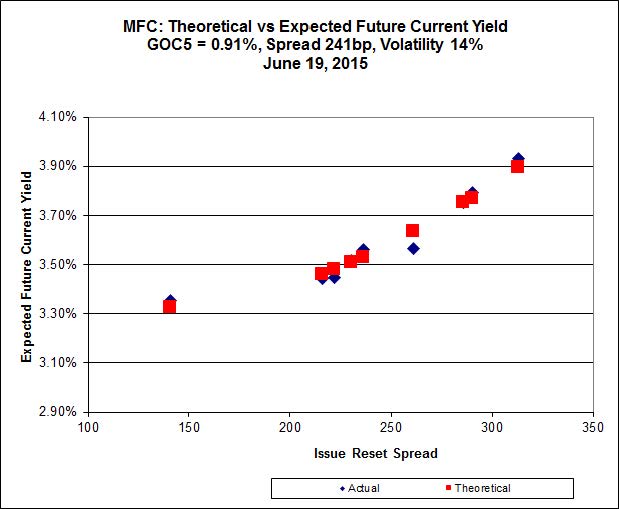

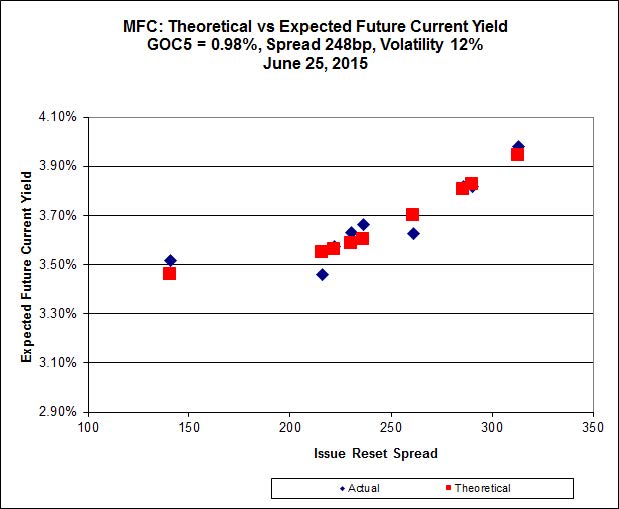

Click for Big

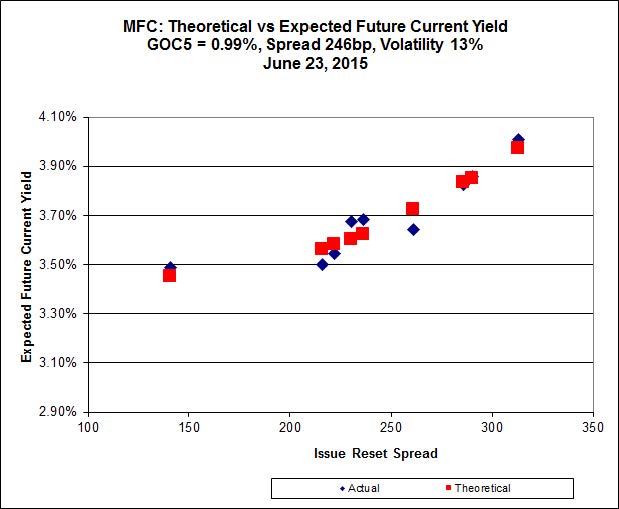

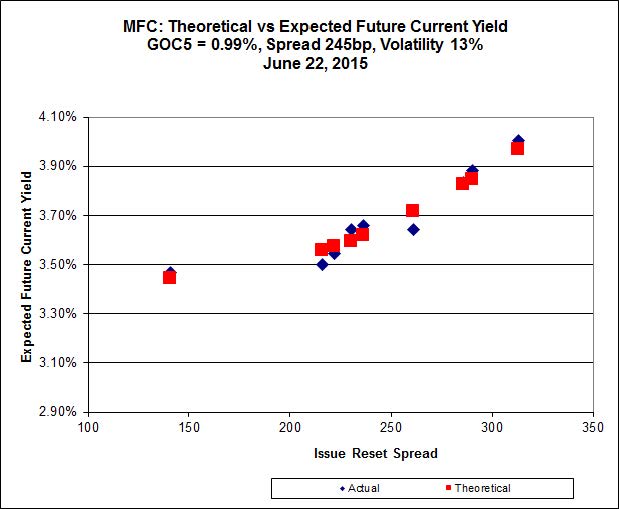

Another excellent fit, but the numbers are perplexing. Implied Volatility for MFC continues to be a conundrum. It is still too high if we consider that NVCC rules will never apply to these issues; it is still too low if we consider them to be NVCC non-compliant issues (and therefore with Deemed Maturities in the call schedule). The lowest spread issue, MFC.PR.F, is again noticeably off the line defined by the higher-spread issues.

Most expensive is MFC.PR.L, resetting at +216bp on 2019-6-19, bid at 22.70 to be $0.58 rich, while MFC.PR.M, resetting at +236bp on 2019-12-19, is bid at 22.80 to be $0.38 cheap.

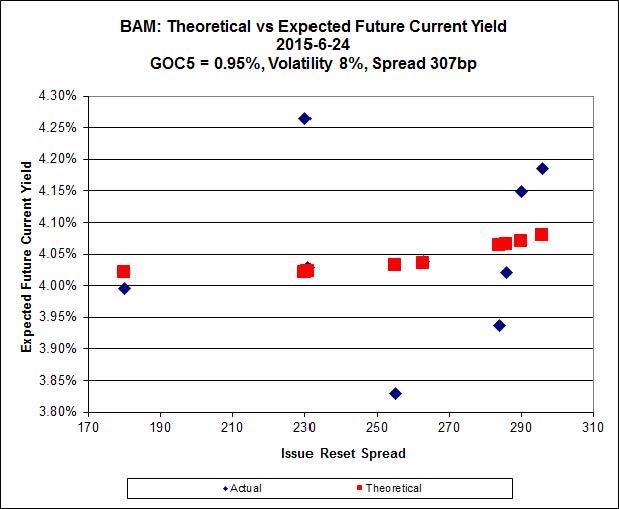

Click for Big

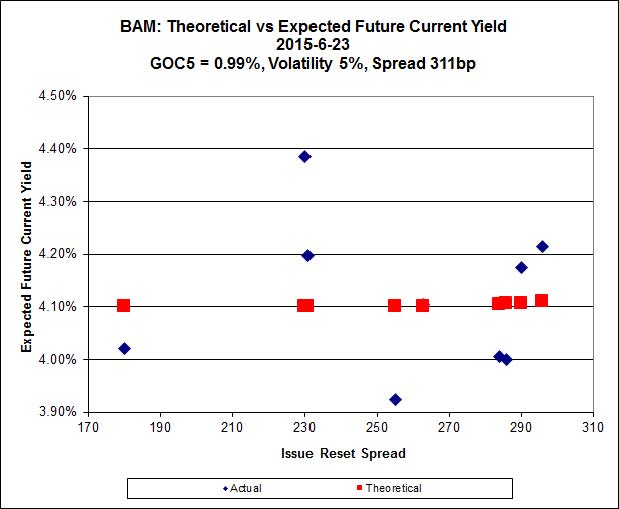

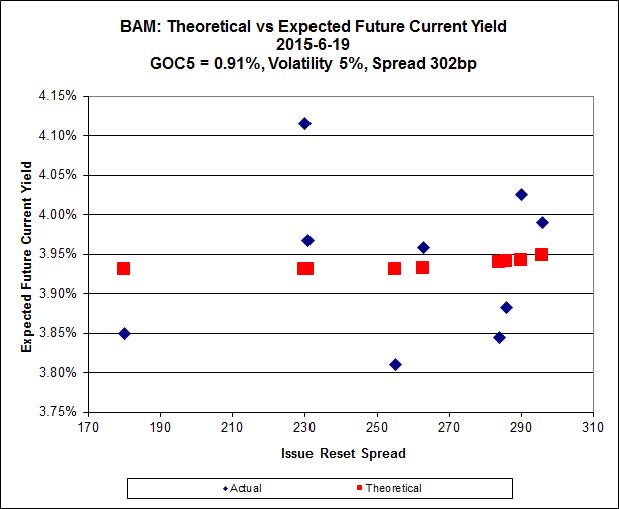

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 19.35 to be $0.83 cheap. BAM.PF.E, resetting at +255bp 2020-3-31 is bid at 22.75 and appears to be $1.12 rich.

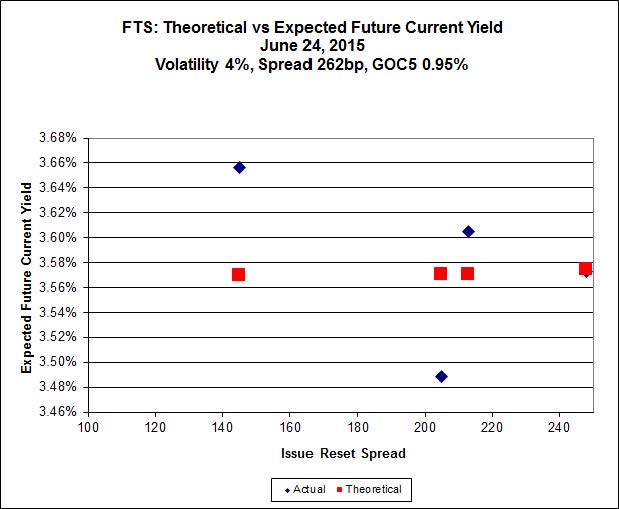

Click for Big

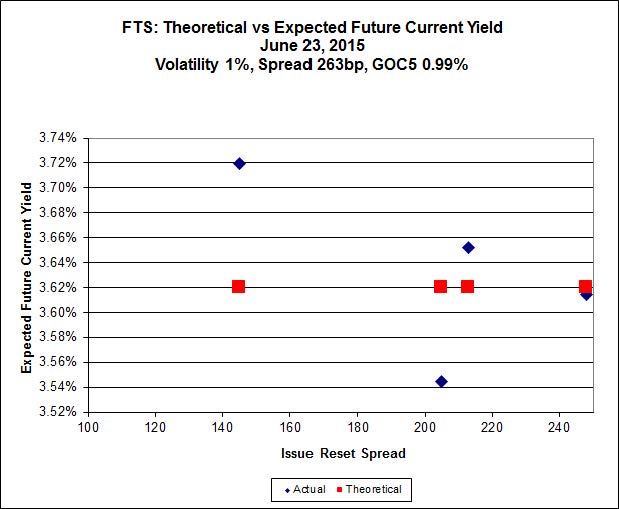

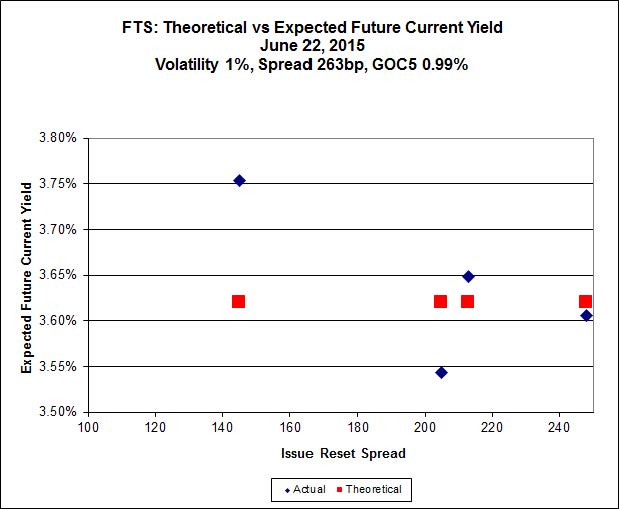

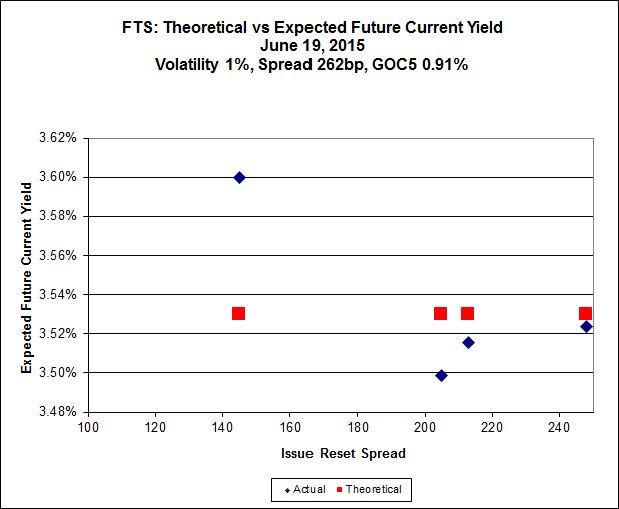

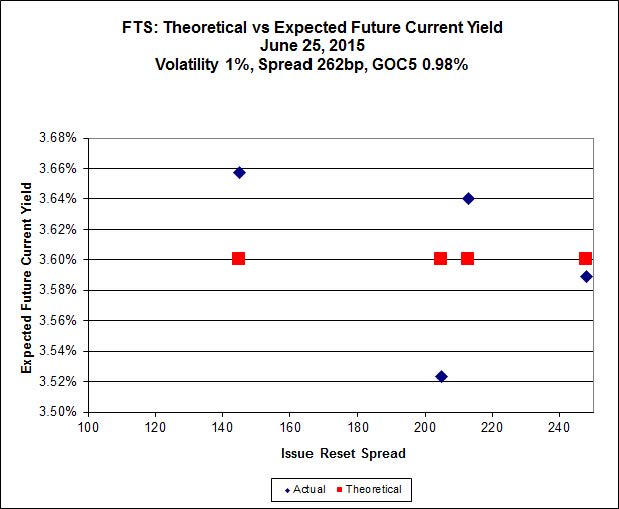

FTS.PR.H, with a spread of +145bp, and bid at 16.61, looks $0.27 cheap and resets 2020-6-1. FTS.PR.K, with a spread of +205bp and resetting 2019-3-1, is bid at 21.50 and is $0.46 rich.

Click for Big

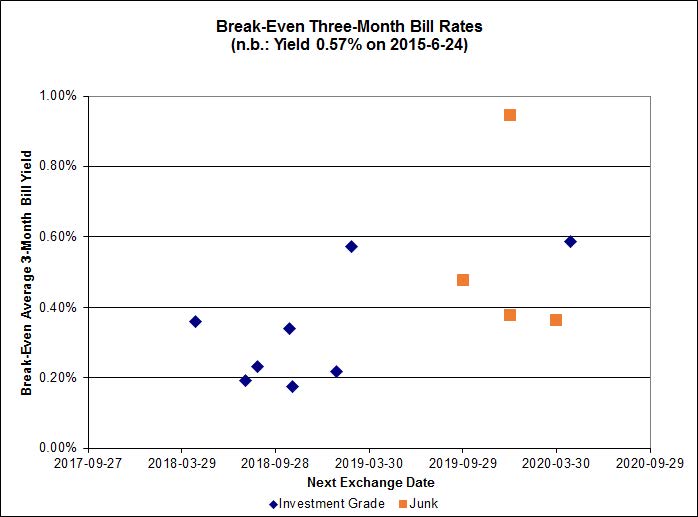

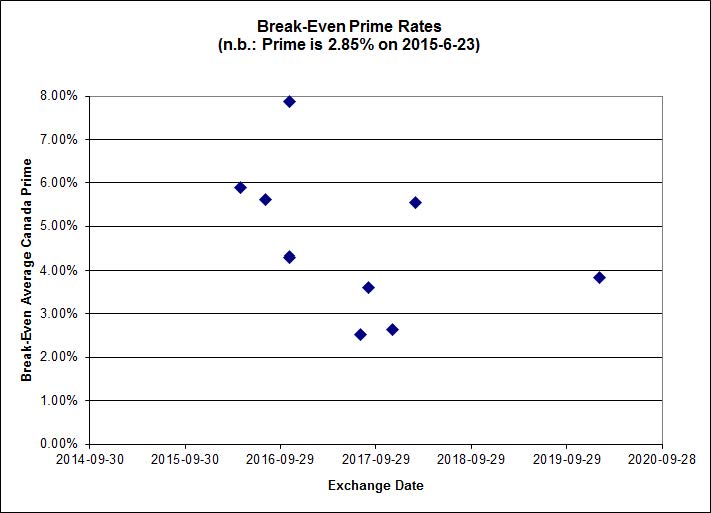

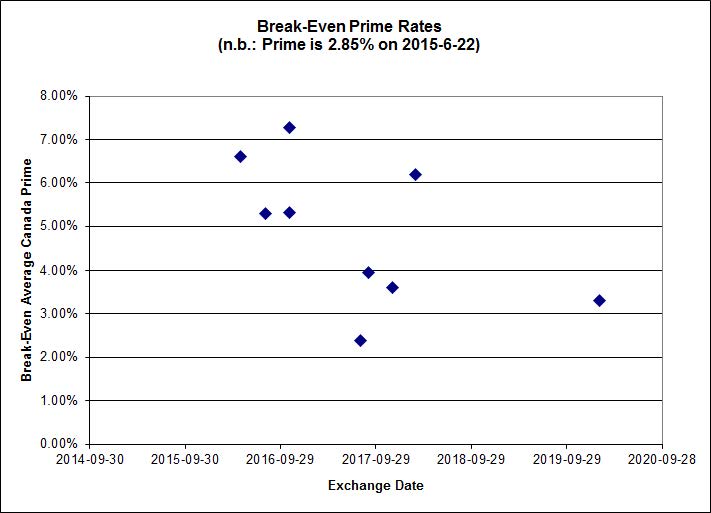

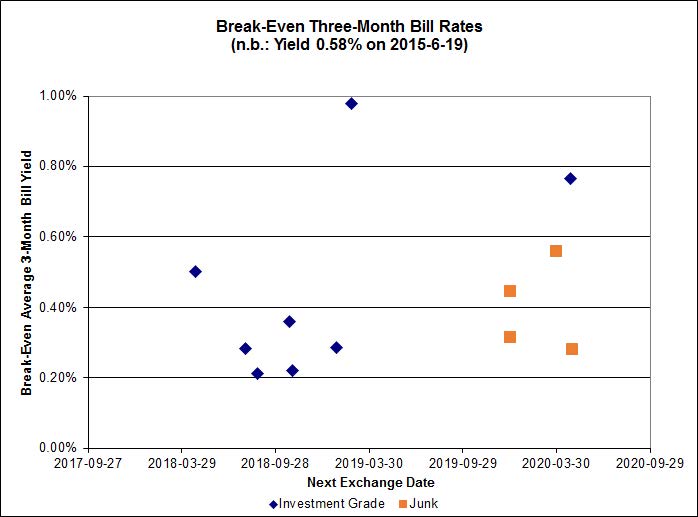

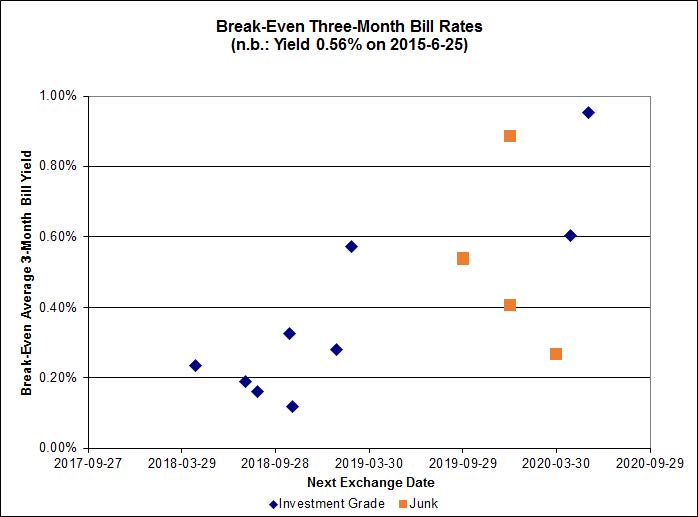

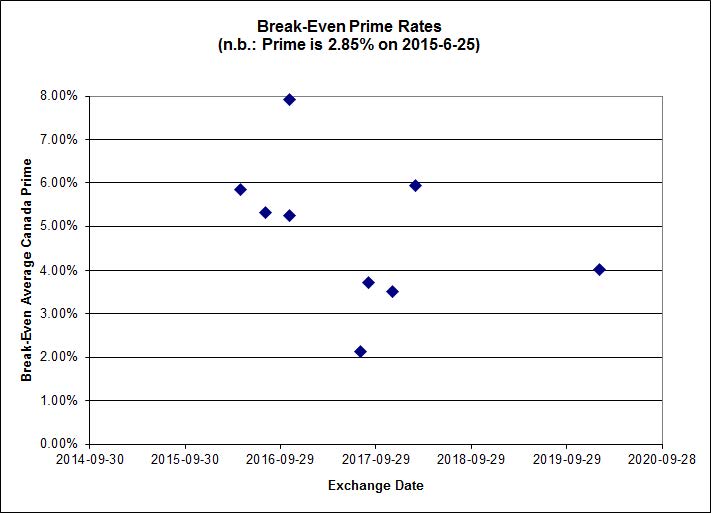

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of about 0.35%, including the outlier TRP.PR.A / TRP.PR.F at -0.53%. On the junk side there are two outliers: FFH.PR.E / FFH.PR.F at -0.65%; and BRF.PR.A / BRF.PR.B at -0.39%.

Click for Big

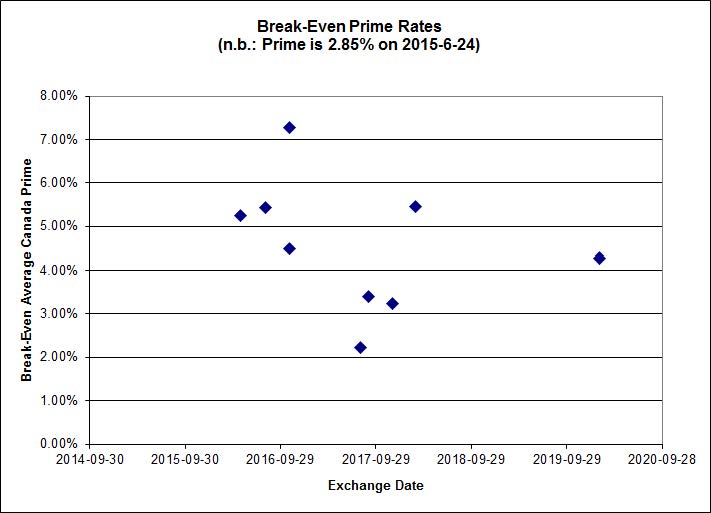

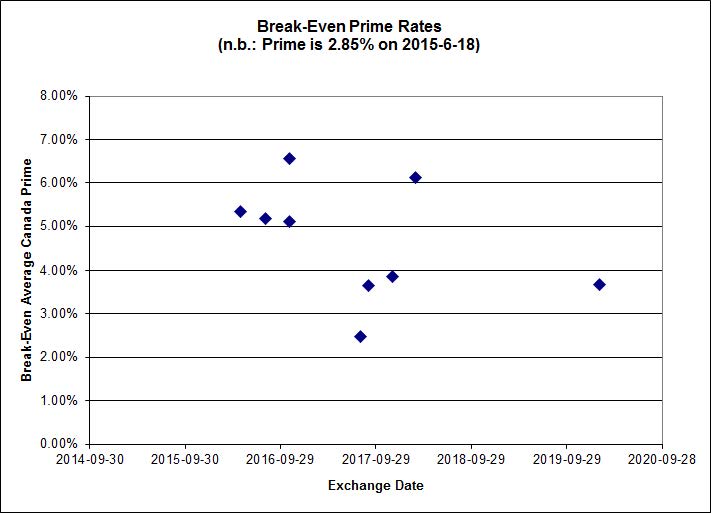

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -3.0070 % | 2,153.7 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -3.0070 % | 3,765.7 |

| Floater | 3.60 % | 3.61 % | 61,865 | 18.27 | 3 | -3.0070 % | 2,289.6 |

| OpRet | 4.78 % | -8.35 % | 22,912 | 0.08 | 1 | -0.1559 % | 2,781.3 |

| SplitShare | 4.59 % | 4.80 % | 74,849 | 3.26 | 3 | -0.1873 % | 3,248.4 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.1559 % | 2,543.2 |

| Perpetual-Premium | 5.48 % | 4.80 % | 62,992 | 4.22 | 19 | 0.0187 % | 2,513.2 |

| Perpetual-Discount | 5.27 % | 5.19 % | 118,412 | 15.09 | 15 | -0.2593 % | 2,672.0 |

| FixedReset | 4.56 % | 3.86 % | 235,833 | 16.15 | 88 | 0.0402 % | 2,326.3 |

| Deemed-Retractible | 5.03 % | 3.20 % | 111,993 | 0.65 | 34 | -0.0360 % | 2,610.2 |

| FloatingReset | 2.49 % | 2.99 % | 57,846 | 6.09 | 9 | -0.0591 % | 2,333.5 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| IAG.PR.G | FixedReset | -3.37 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.06 Bid-YTW : 4.43 % |

| BAM.PR.K | Floater | -3.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-25 Maturity Price : 13.81 Evaluated at bid price : 13.81 Bid-YTW : 3.61 % |

| BAM.PR.C | Floater | -3.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-25 Maturity Price : 13.65 Evaluated at bid price : 13.65 Bid-YTW : 3.65 % |

| BAM.PR.B | Floater | -2.55 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-25 Maturity Price : 14.15 Evaluated at bid price : 14.15 Bid-YTW : 3.52 % |

| CU.PR.D | Perpetual-Discount | -2.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-25 Maturity Price : 23.42 Evaluated at bid price : 23.81 Bid-YTW : 5.18 % |

| HSE.PR.A | FixedReset | -2.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-25 Maturity Price : 15.66 Evaluated at bid price : 15.66 Bid-YTW : 4.48 % |

| MFC.PR.F | FixedReset | -1.73 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.00 Bid-YTW : 7.32 % |

| BAM.PF.A | FixedReset | -1.72 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-25 Maturity Price : 22.29 Evaluated at bid price : 22.80 Bid-YTW : 4.35 % |

| IAG.PR.A | Deemed-Retractible | -1.57 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.54 Bid-YTW : 5.99 % |

| MFC.PR.K | FixedReset | -1.32 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.40 Bid-YTW : 4.82 % |

| TRP.PR.C | FixedReset | -1.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-25 Maturity Price : 16.00 Evaluated at bid price : 16.00 Bid-YTW : 4.08 % |

| ENB.PR.H | FixedReset | -1.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-25 Maturity Price : 16.80 Evaluated at bid price : 16.80 Bid-YTW : 4.90 % |

| BMO.PR.T | FixedReset | -1.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-25 Maturity Price : 21.85 Evaluated at bid price : 22.25 Bid-YTW : 3.78 % |

| TRP.PR.G | FixedReset | -1.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-25 Maturity Price : 22.99 Evaluated at bid price : 24.60 Bid-YTW : 3.88 % |

| PWF.PR.S | Perpetual-Discount | -1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-25 Maturity Price : 23.39 Evaluated at bid price : 23.75 Bid-YTW : 5.11 % |

| TRP.PR.E | FixedReset | -1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-25 Maturity Price : 22.14 Evaluated at bid price : 22.70 Bid-YTW : 3.90 % |

| ENB.PF.A | FixedReset | 1.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-25 Maturity Price : 20.20 Evaluated at bid price : 20.20 Bid-YTW : 4.78 % |

| NA.PR.W | FixedReset | 1.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-25 Maturity Price : 22.09 Evaluated at bid price : 22.66 Bid-YTW : 3.73 % |

| ENB.PF.E | FixedReset | 1.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-25 Maturity Price : 20.24 Evaluated at bid price : 20.24 Bid-YTW : 4.79 % |

| FTS.PR.H | FixedReset | 1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-25 Maturity Price : 16.61 Evaluated at bid price : 16.61 Bid-YTW : 3.71 % |

| SLF.PR.G | FixedReset | 1.48 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.51 Bid-YTW : 7.43 % |

| POW.PR.G | Perpetual-Premium | 1.57 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2020-04-15 Maturity Price : 25.25 Evaluated at bid price : 25.82 Bid-YTW : 4.97 % |

| BAM.PR.R | FixedReset | 1.57 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-25 Maturity Price : 19.35 Evaluated at bid price : 19.35 Bid-YTW : 4.39 % |

| ENB.PF.G | FixedReset | 1.64 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-25 Maturity Price : 20.50 Evaluated at bid price : 20.50 Bid-YTW : 4.76 % |

| ENB.PF.C | FixedReset | 1.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-25 Maturity Price : 20.19 Evaluated at bid price : 20.19 Bid-YTW : 4.77 % |

| ENB.PR.J | FixedReset | 1.91 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-25 Maturity Price : 19.77 Evaluated at bid price : 19.77 Bid-YTW : 4.75 % |

| MFC.PR.N | FixedReset | 2.36 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.60 Bid-YTW : 4.85 % |

| MFC.PR.M | FixedReset | 2.70 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.80 Bid-YTW : 4.81 % |

| PWF.PR.P | FixedReset | 2.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-25 Maturity Price : 18.50 Evaluated at bid price : 18.50 Bid-YTW : 3.64 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| TD.PR.T | FloatingReset | 139,638 | TD crossed blocks of 88,400 and 50,000, both at 24.05. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.04 Bid-YTW : 2.88 % |

| BNS.PR.P | FixedReset | 95,800 | TD crossed blocks of 45,000 and 50,000, both at 25.30. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.24 Bid-YTW : 3.10 % |

| TD.PR.Z | FloatingReset | 60,929 | TD crossed 60,000 at 24.05. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.01 Bid-YTW : 2.99 % |

| TD.PR.Y | FixedReset | 54,800 | TD crossed 50,000 at 25.50. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.33 Bid-YTW : 3.02 % |

| HSE.PR.A | FixedReset | 50,290 | Scotia crossed 40,000 at 16.30. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-25 Maturity Price : 15.66 Evaluated at bid price : 15.66 Bid-YTW : 4.48 % |

| BNS.PR.R | FixedReset | 42,860 | Nesbitt crossed 35,000 at 25.53. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.52 Bid-YTW : 3.14 % |

| There were 29 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| BAM.PR.K | Floater | Quote: 13.81 – 14.68 Spot Rate : 0.8700 Average : 0.6878 YTW SCENARIO |

| ENB.PF.G | FixedReset | Quote: 20.50 – 21.00 Spot Rate : 0.5000 Average : 0.3218 YTW SCENARIO |

| BAM.PR.C | Floater | Quote: 13.65 – 14.60 Spot Rate : 0.9500 Average : 0.7874 YTW SCENARIO |

| TRP.PR.E | FixedReset | Quote: 22.70 – 23.20 Spot Rate : 0.5000 Average : 0.3489 YTW SCENARIO |

| MFC.PR.K | FixedReset | Quote: 22.40 – 22.80 Spot Rate : 0.4000 Average : 0.2491 YTW SCENARIO |

| TD.PF.A | FixedReset | Quote: 22.00 – 23.06 Spot Rate : 1.0600 Average : 0.9273 YTW SCENARIO |