I periodically get asked why my assets under management are so small. Perhaps I should behave more like the big boys:

Staff of the Compliance and Registrant Regulation Branch (Staff or we) of the Ontario Securities Commission (OSC) recently conducted a targeted review or sweep of a sample of large investment fund managers (IFMs), based on assets under management. The reviews focused on the IFMs’ compliance with Ontario securities law in key operational areas. This Notice provides a summary of our findings and related guidance.

…

Aside from the issuance of deficiency reports, the sweep did not result in further regulatory action on any of the IFMs reviewed. However, we identified areas where deficiencies were more prevalent and additional guidance is needed. These areas are discussed in dedicated parts below and include:

- I. sales practices

- II. allocation of expenses to investment funds

- III. mutual fund borrowings

- IV. prohibited cross trades

- V. outsourcing and oversight of service providers

…

Section 5.1 permits IFMs to pay a portion of the costs of a sales communication, investor conference or investor seminar (collectively, cooperative marketing practices) that participating dealers organize and present to investors.The major findings in this area, shown along with their incidence rate, were:

- • cooperative marketing practices did not meet the primary purpose of promoting or providing educational information concerning a mutual fund, a mutual fund family or mutual funds generally in order to be eligible for support (25%)

- • inadequate disclosure on cooperative marketing materials to indicate that the IFM paid for a portion of the costs of the cooperative marketing practice (25%)

- • inconsistent application of the IFM’s methodology to calculate primary purpose across all cooperative marketing practice requests (13%)

ii) Section 5.2 — Mutual fund sponsored conferences

Section 5.2 outlines the conditions under which IFMs may provide a non-monetary benefit to a sales representative of a participating dealer to attend a conference or seminar organized and presented by the IFM.

The major findings in this area, shown along with their incidence rate, were:

- • IFMs paid for expenses of the sales representatives, such as travel and accommodation, not permitted under section 5.2 (50%)

- • the non-monetary benefits relating to the mutual fund sponsored conference, such as meals and entertainment, were excessive having regard to the purpose of the conference (25%)

iii) Section 5.5 — Participating dealer sponsored events

Section 5.5 permits IFMs to pay a portion of the costs of conferences and seminars organized and presented by dealers (that are not investor conferences or seminars referred to in section 5.1), within certain parameters.

The major findings in this area, shown along with their incidence rate, were:

- • IFMs provided support for dealer organized conferences which included amounts related to meals and entertainment that were excessive having regard to the purpose of the conference (25%)

- • IFMs provided support for dealer organized conferences in excess of the 10% reimbursement limit of direct costs incurred by the dealer relating to the conference (25%)

The municipal pension wars are starting:

Police officers and firefighters lighting a bonfire on the street in front of Montreal’s City Hall are an unusual sight. They were among several hundred union members protesting the Quebec government’s intention to reform the pension plans for municipal workers.

One of the proposals is a 50-50 split between Quebec’s cities and their 122,000 employees when it comes to premiums and covering future shortfalls. Indexation would be partly frozen. Current plan members and retirees would be tapped to pay down past deficits. The aim is to reach a negotiated settlement within 12 months.

Municipal Affairs Minister Pierre Moreau estimated the pension plans have a combined deficit of $3.9-billion – late last year it was pegged at north of $5-billion – when he unveiled draft legislation last week.

Eighty Montreal firefighters retired on the spot, causing the brief closure of two stations.

The OMERS deficit is being erased … slowly:

OMERS manages $65.1-billion in pension assets for 440,000 employees and retirees of municipal governments across Ontario. The fund said its assets climbed by over $4-billion from $60.8-billion in 2012, and its funded ratio improved last year by three per cent to 88 per cent, which means the fund has assets equal to 88 per cent of its long-term obligation to fund members’ pensions on a solvency basis.

The pension manager said the remaining $8.6-billion deficit will probably be erased at some point between 2021 and 2025 depending on investment returns. OMERS plan members have increased their pension contributions since 2011 to help improve plan funding, but the increases are expected to be removed when OMERS returns to a surplus.

… which is OK, but:

OMERS needs to earn a long-term annualized return of 7 per cent on its investments to meet its pension obligations.

…

Mr. Nobrega, who is retiring on April 1, said the introduction of the new “risk-balanced” portfolio last year was the final step in a restructuring launched in 2004 to reduce volatility risk in the investment portfolio. The fund now has 57 per cent of its investments in public markets and 43 per cent in private markets, and is working toward a goal of 53 per cent public market holdings.

Split Share aficionados will be familiar with the concept of Sequence of Returns risk – average return doesn’t mean as much as one might think in the presence of cash flows and portfolio volatility. And let’s just hope they are very conservative with the private equity valuations. Ha ha. By the way – the CPPIB’s return assumption is:

The Chief Actuary’s projections are based on the assumption that the fund will attain an average annual real rate of return, which takes into account the impact of inflation, of 4% over the 75-year projection period in his report, to help sustain the plan at the current contribution rate.

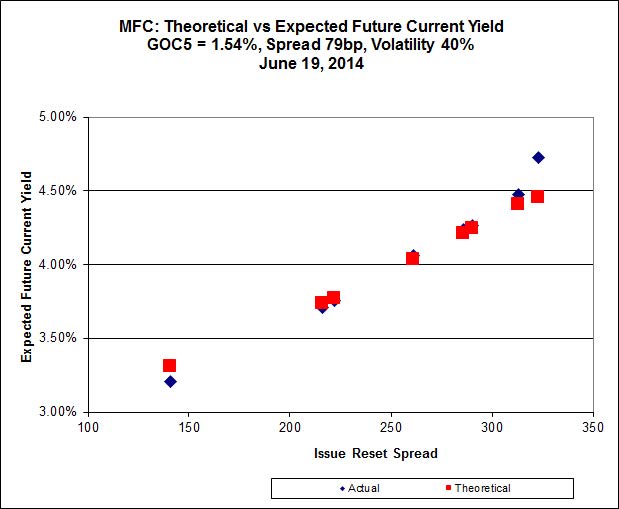

Today’s redemption of MFC.PR.D hasn’t changed anything with respect to the MFC FixedReset Implied Volatility … still 40%+:

Click for Big

It was a positive day for the Canadian preferred share market, with PerpetualDiscounts winning 13bp, FixedResets gaining 1bp and DeemedRetractibles up 10bp. Volatility was very low, except for the illiquid and hypervolatile Floaters. Volume was average.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.9445 % | 2,500.1 |

| FixedFloater | 4.44 % | 3.69 % | 31,111 | 17.96 | 1 | -0.6032 % | 3,871.4 |

| Floater | 2.93 % | 3.05 % | 44,740 | 19.62 | 4 | 0.9445 % | 2,699.5 |

| OpRet | 4.38 % | -7.84 % | 23,106 | 0.08 | 2 | -0.0389 % | 2,709.0 |

| SplitShare | 4.81 % | 4.25 % | 60,749 | 4.11 | 5 | -0.1033 % | 3,114.9 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0389 % | 2,477.1 |

| Perpetual-Premium | 5.52 % | -2.64 % | 83,293 | 0.09 | 17 | 0.2036 % | 2,407.9 |

| Perpetual-Discount | 5.26 % | 5.27 % | 115,133 | 14.97 | 20 | 0.1277 % | 2,556.0 |

| FixedReset | 4.46 % | 3.70 % | 214,611 | 6.69 | 78 | 0.0113 % | 2,540.8 |

| Deemed-Retractible | 4.99 % | -0.30 % | 134,595 | 0.11 | 43 | 0.1002 % | 2,537.0 |

| FloatingReset | 2.66 % | 2.37 % | 124,928 | 3.95 | 6 | 0.2772 % | 2,499.2 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| IFC.PR.A | FixedReset | -1.20 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.81 Bid-YTW : 4.22 % |

| BAM.PR.B | Floater | 1.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-06-19 Maturity Price : 17.13 Evaluated at bid price : 17.13 Bid-YTW : 3.06 % |

| BAM.PR.C | Floater | 1.36 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-06-19 Maturity Price : 17.20 Evaluated at bid price : 17.20 Bid-YTW : 3.05 % |

| BAM.PR.K | Floater | 1.42 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-06-19 Maturity Price : 17.13 Evaluated at bid price : 17.13 Bid-YTW : 3.06 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| CM.PR.O | FixedReset | 173,845 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-06-19 Maturity Price : 23.21 Evaluated at bid price : 25.18 Bid-YTW : 3.76 % |

| ENB.PF.C | FixedReset | 167,618 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-06-19 Maturity Price : 23.14 Evaluated at bid price : 25.06 Bid-YTW : 4.18 % |

| TD.PR.K | FixedReset | 110,240 | Called for redemption. YTW SCENARIO Maturity Type : Call Maturity Date : 2014-07-31 Maturity Price : 25.00 Evaluated at bid price : 25.38 Bid-YTW : 0.51 % |

| TD.PF.A | FixedReset | 93,810 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-06-19 Maturity Price : 23.19 Evaluated at bid price : 25.17 Bid-YTW : 3.70 % |

| ENB.PR.J | FixedReset | 83,600 | Scotia crossed 75,000 at 25.30. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-06-19 Maturity Price : 23.27 Evaluated at bid price : 25.25 Bid-YTW : 4.07 % |

| RY.PR.H | FixedReset | 78,797 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-06-19 Maturity Price : 23.20 Evaluated at bid price : 25.17 Bid-YTW : 3.72 % |

| There were 33 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| SLF.PR.B | Deemed-Retractible | Quote: 24.01 – 24.25 Spot Rate : 0.2400 Average : 0.1474 YTW SCENARIO |

| TRP.PR.B | FixedReset | Quote: 20.15 – 20.48 Spot Rate : 0.3300 Average : 0.2481 YTW SCENARIO |

| SLF.PR.I | FixedReset | Quote: 25.70 – 25.99 Spot Rate : 0.2900 Average : 0.2129 YTW SCENARIO |

| BAM.PR.G | FixedFloater | Quote: 21.42 – 21.79 Spot Rate : 0.3700 Average : 0.3059 YTW SCENARIO |

| POW.PR.A | Perpetual-Premium | Quote: 25.07 – 25.26 Spot Rate : 0.1900 Average : 0.1266 YTW SCENARIO |

| ENB.PR.H | FixedReset | Quote: 23.70 – 23.97 Spot Rate : 0.2700 Average : 0.2093 YTW SCENARIO |