It’s nice to see a hint of due process in the war on banks:

First there was one. Then three. Now the U.K. Financial Conduct Authority is facing nine lawsuits for improperly identifying traders in penalty notices, in what has quickly become a nightmare for the agency.

In a London court Thursday, the FCA faced a roomful of more than 20 lawyers protesting the reputational damage their clients suffered as a result of its failure to sufficiently disguise them in bank settlement reports. The hearing was the first in a series of headaches the FCA faces on the matter and could change the future of U.K. enforcement proceedings.

“Part of deterrence is telling the story and if you’re telling it with one hand behind your back,” because you can’t allude to individuals, it will make things difficult, said FCA Chief Executive Officer Martin Wheatley in a London interview with Bloomberg last week.

The deluge of cases comes after the FCA lost a landmark appeal in May when a judge said it failed to properly hide the identity of Achilles Macris, the former JPMorgan Chase & Co. manager of the London Whale trader, in its settlement with the bank. The FCA is seeking permission to appeal the judgment to the Supreme Court. A judge will rule as soon as Tuesday on whether the other eight pending cases can proceed before the top court makes a decision on the FCA’s Macris appeal.

…

If the Macris ruling stands, the FCA is faced with two choices: taking years to complete investigations to give all parties the chance to participate or publishing anodyne settlements that won’t fully explain the misconduct.

…

While calling someone trader A in a report might seem anonymous, insiders can often figure out who’s who by references to nicknames or even position on the floor. That can damage traders’ reputation, and their ability to get another job, said Ben Rose, a London lawyer at Hickman & Rose.“It is imperative that regulators and prosecutors prevent ‘join-the-dots’ identification,” Rose said. Regulators must “give those concerned a proper opportunity of being heard before any damaging accusations are made.”

Brookfield Renewable Energy Partners L.P., proud (indirect) issuer of BRF.PR.A, BRF.PR.B, BRF.PR.C, BRF.PR.E and BRF.PR.F, has announced:

that the Toronto Stock Exchange (the “TSX”) accepted notice of Brookfield Renewable Power Preferred Equity Inc.’s (“BRP Equity”) intention to commence a normal course issuer bid for its outstanding Class A Preference Shares (“Preferred Shares”). BRP Equity is a wholly-owned subsidiary of Brookfield Renewable. Brookfield Renewable believes that in the event that the Preferred Shares trade in a price range that does not fully reflect their value, the acquisition of Preferred Shares may represent an attractive use of available funds. There are currently five series of Preferred Shares outstanding.

I take issuer-bid announcements with a grain of salt, which is why this announcement isn’t getting a dedicated post. If they actually buy some, that will be news!

It was yet another poor day for the Canadian preferred share market, with PerpetualDiscounts losing 46bp, FixedResets down 23bp and DeemedRetractibles off 15bp. The Performance Highlights table was dominated by losers, predictably enough. Volume was slightly below average.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

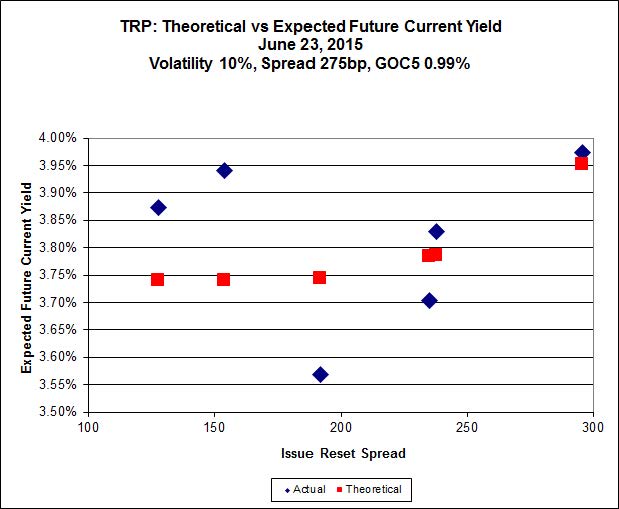

Here’s TRP:

Click for Big

TRP.PR.A, which resets 2019-12-31 at +192, is bid at 20.39 to be $0.96 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $0.86 cheap at its bid price of 16.05.

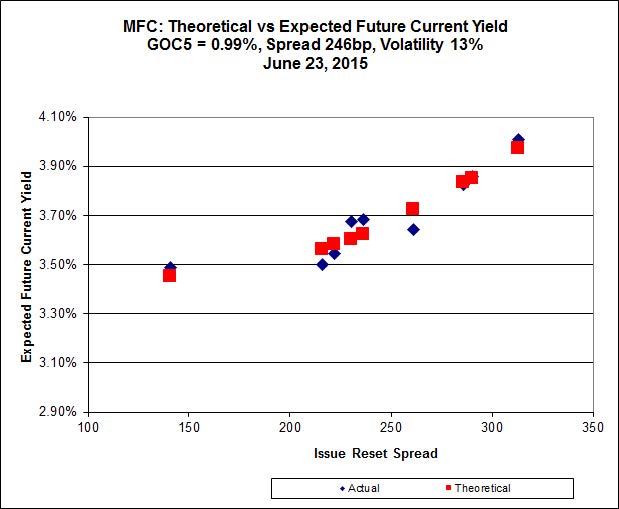

Click for Big

Another excellent fit, but the numbers are perplexing. Implied Volatility for MFC continues to be a conundrum. It is still too high if we consider that NVCC rules will never apply to these issues; it is still too low if we consider them to be NVCC non-compliant issues (and therefore with Deemed Maturities in the call schedule). The lowest spread issue, MFC.PR.F, is again noticeably off the line defined by the higher-spread issues.

Most expensive is MFC.PR.J, resetting at +261bp on 2018-3-19, bid at 24.70 to be $0.53 rich, while MFC.PR.N, resetting at +230bp on 2020-3-19, is bid at 22.39 to be $0.45 cheap.

Click for Big

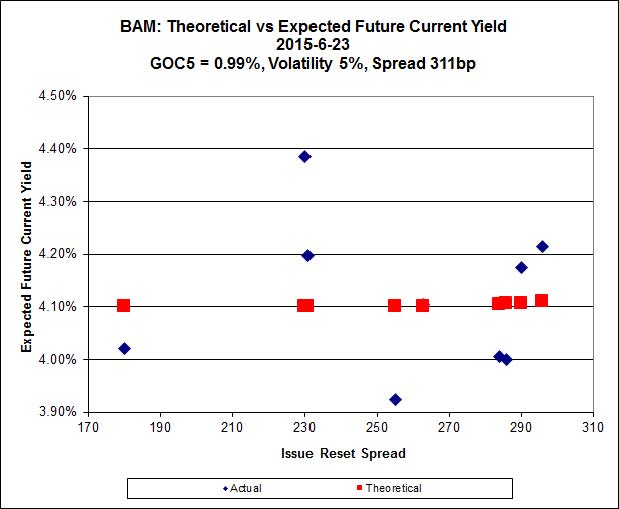

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 18.76 to be $1.30 cheap. BAM.PF.E, resetting at +255bp 2020-3-31 is bid at 22.55 and appears to be $0.97 rich.

Click for Big

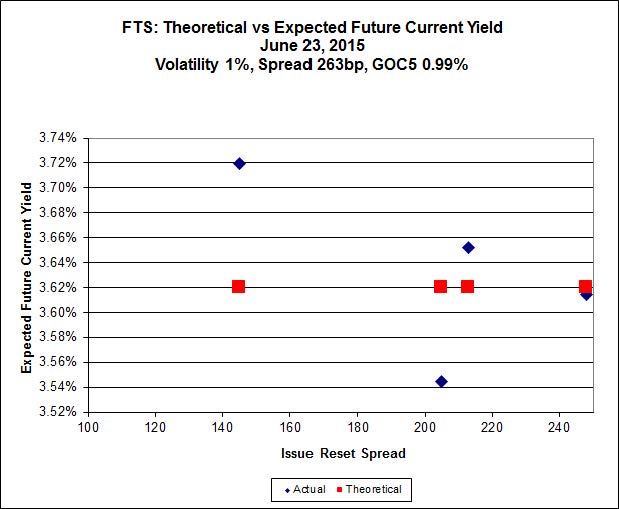

FTS.PR.H, with a spread of +145bp, and bid at 16.40, looks $0.45 cheap and resets 2020-6-1. FTS.PR.K, with a spread of +205bp and resetting 2019-3-1, is bid at 21.44 and is $0.45 rich.

Click for Big

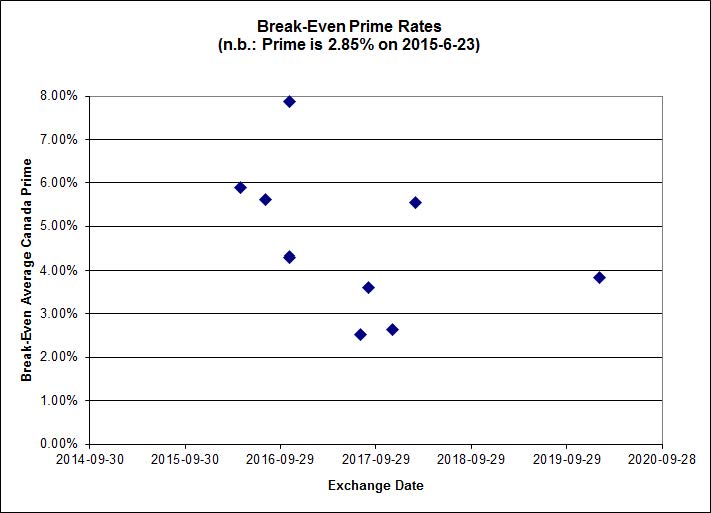

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of about 0.40%, including the outliers TRP.PR.A / TRP.PR.F at -0.57% and FTS.PR.H / FTS.PR.I at +1.16%. On the junk side there are four outliers: FFH.PR.E / FFH.PR.F at -0.87%; DC.PR.B / DC.PR.D at -0.07%; BRF.PR.A / BRF.PR.B at -0.68%; and FFH.PR.C / FFH.PR.F at +1.26%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 1.5673 % | 2,247.4 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 1.5673 % | 3,929.5 |

| Floater | 3.45 % | 3.44 % | 64,667 | 18.67 | 3 | 1.5673 % | 2,389.1 |

| OpRet | 4.78 % | -10.47 % | 23,642 | 0.08 | 1 | 0.0000 % | 2,785.6 |

| SplitShare | 4.56 % | 4.48 % | 66,700 | 3.27 | 3 | 0.3340 % | 3,269.7 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0000 % | 2,547.2 |

| Perpetual-Premium | 5.47 % | 3.70 % | 60,571 | 0.51 | 19 | -0.1182 % | 2,516.8 |

| Perpetual-Discount | 5.23 % | 5.18 % | 118,533 | 15.12 | 15 | -0.4648 % | 2,691.0 |

| FixedReset | 4.56 % | 3.88 % | 236,639 | 16.14 | 88 | -0.2287 % | 2,325.0 |

| Deemed-Retractible | 5.03 % | 3.29 % | 111,986 | 0.82 | 34 | -0.1459 % | 2,613.7 |

| FloatingReset | 2.49 % | 2.96 % | 53,738 | 6.10 | 9 | -0.2750 % | 2,333.1 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| CM.PR.P | FixedReset | -6.04 % | Not real. The day’s range for the 29,550 shares traded was 22.30-70, with a closing price of 22.33. This is simply another example either of the Exchange’s shoddy reporting or their inability to enforce market-making responsibilities. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-23 Maturity Price : 21.30 Evaluated at bid price : 21.30 Bid-YTW : 3.99 % |

| CM.PR.O | FixedReset | -2.57 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-23 Maturity Price : 21.97 Evaluated at bid price : 22.41 Bid-YTW : 3.84 % |

| BAM.PR.Z | FixedReset | -2.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-23 Maturity Price : 22.75 Evaluated at bid price : 23.43 Bid-YTW : 4.31 % |

| BAM.PR.T | FixedReset | -2.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-23 Maturity Price : 19.66 Evaluated at bid price : 19.66 Bid-YTW : 4.36 % |

| PWF.PR.S | Perpetual-Discount | -2.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-23 Maturity Price : 23.63 Evaluated at bid price : 24.01 Bid-YTW : 5.05 % |

| BAM.PR.R | FixedReset | -2.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-23 Maturity Price : 18.76 Evaluated at bid price : 18.76 Bid-YTW : 4.53 % |

| CU.PR.D | Perpetual-Discount | -1.86 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-23 Maturity Price : 23.83 Evaluated at bid price : 24.25 Bid-YTW : 5.08 % |

| MFC.PR.B | Deemed-Retractible | -1.80 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.34 Bid-YTW : 6.18 % |

| CU.PR.E | Perpetual-Discount | -1.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-23 Maturity Price : 23.62 Evaluated at bid price : 24.02 Bid-YTW : 5.13 % |

| BMO.PR.T | FixedReset | -1.52 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-23 Maturity Price : 22.18 Evaluated at bid price : 22.75 Bid-YTW : 3.68 % |

| BMO.PR.W | FixedReset | -1.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-23 Maturity Price : 21.95 Evaluated at bid price : 22.41 Bid-YTW : 3.71 % |

| NA.PR.W | FixedReset | -1.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-23 Maturity Price : 22.30 Evaluated at bid price : 23.00 Bid-YTW : 3.66 % |

| BMO.PR.S | FixedReset | -1.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-23 Maturity Price : 22.35 Evaluated at bid price : 23.00 Bid-YTW : 3.72 % |

| RY.PR.K | FloatingReset | -1.13 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.40 Bid-YTW : 2.89 % |

| RY.PR.Z | FixedReset | -1.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-23 Maturity Price : 22.34 Evaluated at bid price : 22.99 Bid-YTW : 3.62 % |

| BAM.PF.G | FixedReset | -1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-23 Maturity Price : 22.73 Evaluated at bid price : 23.90 Bid-YTW : 4.11 % |

| GWO.PR.I | Deemed-Retractible | -1.01 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.57 Bid-YTW : 5.86 % |

| ENB.PF.E | FixedReset | 1.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-23 Maturity Price : 19.80 Evaluated at bid price : 19.80 Bid-YTW : 4.90 % |

| IFC.PR.A | FixedReset | 1.14 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.58 Bid-YTW : 6.24 % |

| BAM.PR.B | Floater | 1.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-23 Maturity Price : 14.67 Evaluated at bid price : 14.67 Bid-YTW : 3.40 % |

| IAG.PR.A | Deemed-Retractible | 1.28 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.90 Bid-YTW : 5.77 % |

| ENB.PF.C | FixedReset | 1.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-23 Maturity Price : 19.67 Evaluated at bid price : 19.67 Bid-YTW : 4.90 % |

| ENB.PR.N | FixedReset | 1.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-23 Maturity Price : 18.95 Evaluated at bid price : 18.95 Bid-YTW : 4.93 % |

| ENB.PF.A | FixedReset | 1.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-23 Maturity Price : 19.73 Evaluated at bid price : 19.73 Bid-YTW : 4.89 % |

| BAM.PR.K | Floater | 2.84 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-23 Maturity Price : 14.50 Evaluated at bid price : 14.50 Bid-YTW : 3.44 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BNS.PR.Z | FixedReset | 65,900 | RBC bought 41,300 from Scotia at 23.75. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.77 Bid-YTW : 3.40 % |

| TRP.PR.E | FixedReset | 34,460 | TD crossed 22,500 at 22.60. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-23 Maturity Price : 22.04 Evaluated at bid price : 22.55 Bid-YTW : 3.93 % |

| RY.PR.L | FixedReset | 33,500 | Nesbitt crossed 25,000 at 25.94. YTW SCENARIO Maturity Type : Call Maturity Date : 2019-02-24 Maturity Price : 25.00 Evaluated at bid price : 25.94 Bid-YTW : 3.28 % |

| ENB.PR.P | FixedReset | 33,360 | TD crossed 11,600 at 18.27. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-23 Maturity Price : 18.20 Evaluated at bid price : 18.20 Bid-YTW : 4.98 % |

| HSE.PR.G | FixedReset | 27,156 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-23 Maturity Price : 22.99 Evaluated at bid price : 24.53 Bid-YTW : 4.54 % |

| CM.PR.P | FixedReset | 26,250 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-23 Maturity Price : 21.30 Evaluated at bid price : 21.30 Bid-YTW : 3.99 % |

| There were 28 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| CM.PR.P | FixedReset | Quote: 21.30 – 22.30 Spot Rate : 1.0000 Average : 0.6112 YTW SCENARIO |

| BAM.PR.C | Floater | Quote: 14.25 – 14.88 Spot Rate : 0.6300 Average : 0.4109 YTW SCENARIO |

| POW.PR.G | Perpetual-Premium | Quote: 25.68 – 26.31 Spot Rate : 0.6300 Average : 0.4221 YTW SCENARIO |

| BAM.PR.B | Floater | Quote: 14.67 – 15.15 Spot Rate : 0.4800 Average : 0.3094 YTW SCENARIO |

| BAM.PF.E | FixedReset | Quote: 22.55 – 23.00 Spot Rate : 0.4500 Average : 0.2879 YTW SCENARIO |

| PWF.PR.S | Perpetual-Discount | Quote: 24.01 – 24.50 Spot Rate : 0.4900 Average : 0.3289 YTW SCENARIO |