Today’s parable illustrates the adage that you should never trust a stockbroker:

The Securities and Exchange Commission today announced that ITG Inc. and its affiliate AlterNet Securities have agreed to pay $20.3 million to settle charges that they operated a secret trading desk and misused the confidential trading information of dark pool subscribers.

An SEC investigation found that despite telling the public that it was an “agency-only” broker whose interests don’t conflict with its customers, ITG operated an undisclosed proprietary trading desk known as “Project Omega” for more than a year. While ITG claimed to protect the confidentiality of its dark pool subscribers’ trading information, during an eight-month period Project Omega accessed live feeds of order and execution information of its subscribers and used it to implement high-frequency algorithmic trading strategies, including one in which it traded against subscribers in ITG’s dark pool called POSIT.

ITG agreed to admit wrongdoing and pay disgorgement of $2,081,034 (the total proprietary revenues generated by Project Omega) plus prejudgment interest of $256,532 and a penalty of $18 million that is the SEC’s largest to date against an alternative trading system.

…

According to the SEC’s order instituting a settled administrative proceeding:

- • Project Omega traded a total of approximately 1.3 billion shares, including approximately 262 million shares with unsuspecting subscribers in ITG’s own dark pool.

- • Project Omega employed an algorithmic trading strategy called the “Facilitation Strategy” in which it executed trades based on a live feed of information concerning orders that its sell-side subscribers sent to ITG’s algorithms for handling.

- • Project Omega accessed the feed by connecting to a software utility that was used by ITG’s sales and support teams. As a result, Project Omega had a real-time view of subscriber orders being placed through ITG’s algorithms.

- • From April to December 2010, the Facilitation Strategy was designed to detect open orders of sell-side subscribers being handled by ITG. Based on that information, Project Omega opened positions in displayed markets on the same side of the market as the detected orders, and then closed these positions in POSIT by trading against the detected orders. By employing this strategy, Project Omega sought to capture the full “bid-ask spread” between the National Best Bid and Offer (NBBO).

- • Project Omega had access to the identities of POSIT subscribers and used this information to identify sell-side subscribers and trade with them in the dark pool in connection with the Facilitation Strategy.

- • To earn the full “bid-ask spread” in connection with the Facilitation Strategy, Project Omega needed the subscribers with which it traded in POSIT to be configured to trade “aggressively” so that the subscribers would “cross the spread” to trade with Project Omega. Project Omega took steps to ensure that the sell-side subscribers were configured to trade aggressively in POSIT.

- • Project Omega’s other primary strategy called the “Heatmap Strategy” involved trading on markets other than POSIT based on a live feed of confidential information relating to customer executions in other dark pools. Based on customer executions, Project Omega’s Heatmap algorithm was designed to open positions in specific securities in displayed markets at the bid or the offer and then close them at midpoint or better in the external dark pools where customers had received midpoint executions. The goal of this strategy was to earn a “half spread” or better based on knowledge of ITG customers’ executions.

My Christ. Front-running with a vengeance ITG’s press release states, in part:

ITG is an independent execution broker and research provider that partners with global portfolio managers and traders to provide unique data-driven insights throughout the investment process.

ITG was once recommended to me by an influential and knowledgeable guy as having good algorithms that I could use for accounts held in third-party custody; I never had any need for them, but tucked away the information for potential use. Well, I’ve scratched out that memo. I hope they get sued for bazillions (having admitted wrongdoing!), go bankrupt and have all members of management starve to death on the streets. But we’ll see.

Brookfield Asset Management has announced:

it has received approval from the Toronto Stock Exchange (“TSX”) for its proposed normal course issuer bid to purchase up to 10% of the public float of each series of the company’s outstanding Class A Preference Shares, excluding the Series 14 Class A Preference Shares, that are listed on the TSX (the “Preferred Shares”). Purchases under the bid will be made through the facilities of the TSX. The period of the normal course issuer bid will extend from August 12, 2015 to August 11, 2016, or an earlier date should Brookfield complete its purchases. Brookfield will pay the market price at the time of acquisition for any Preferred Shares purchased. All Preferred Shares acquired by Brookfield under this bid will be cancelled. Brookfield has not repurchased any Preferred Shares in the past 12 months.

Under the normal course issuer bid, Brookfield is authorized to repurchase each respective series of the Preferred Shares as follows: … [list of all preferred shares, with data on daily and total maximal purchases]

This press release, which was brought to my attention by Assiduous Reader Louisprefs, follows the June 23 announcement of a NCIB by BRF and the June 29 follow-up to this announcing an automatic purchase plan with its designated broker. As it turns out, this NCIB was real (they’re usually just cheerleading) and I’ll post about the results soon.

CU Inc., proud issuer of CIU.PR.A and CIU.PR.C was confirmed at Pfd-2(high) by DBRS:

DBRS Limited (DBRS) has today confirmed the Issuer Rating and Unsecured Debentures & Medium Term Notes rating of CU Inc. (CUI or the Company) at A (high), Commercial Paper rating at R-1 (low), and Cumulative Preferred Shares rating at Pfd-2 (high). All trends are Stable. The confirmation reflects DBRS’s expectation that (1) the quality of transmission and distribution regulatory regimes in Alberta, which has shown signs of deterioration in 2015, will remain reasonable for the current rating category; (2) CUI’s diversification across different energy segments will continue to support the stability of earnings and cash flow; and (3) overall key credit metrics will remain within the “A” rating category despite the continued large capital expenditure (capex) program over the next two years. The debt-to-cash flow ratio, which is currently at the lower end of the “A” rating range, is expected to improve gradually over the next three years.

…

With the downshifting of Alberta’s economy and expected completion of the “big build” associated with electric transmission infrastructure over the next two years, capex will likely further normalize, while earnings and cash flow will benefit from a higher rate base. As a result, DBRS expects free cash flow before dividends to become positive in 2017, and the cash flow-to-debt ratio to gradually recover to around historical levels (15%) more consistent with the current rating category. The rating assumes excess cash, which is not required to maintain the regulatory capital structure, will flow up to its parent company, Canadian Utilities Limited (rated “A” by DBRS).

It was a mixed day for the Canadian preferred share market, with PerpetualDiscounts off 5bp, FixedResets gaining 17bp and DeemedRetractibles up 25bp. TRP issues are again notable in the bad part of the Performance Highlights table, while ENB FixedResets occupy a more desirable neighborhood. Volume was very low.

PerpetualDiscounts now yield 5.44%, equivalent to 7.07% interest at the standard equivalency factor of 1.3x. Long corporates now yield about 3.95%, so the pre-tax interest-equivalent spread (in this context, the “Seniority Spread” is now about 310bp, a small (and perhaps spurious) widening from the 305bp reported August 5.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

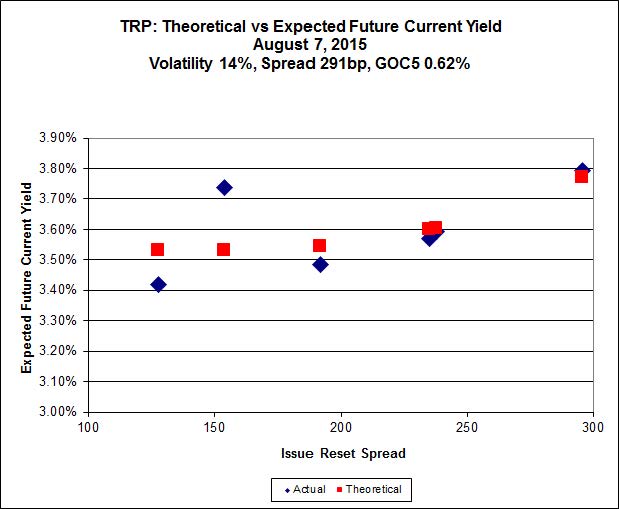

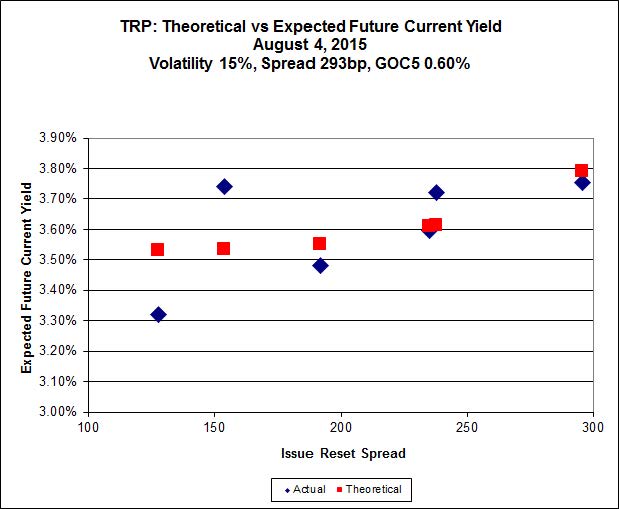

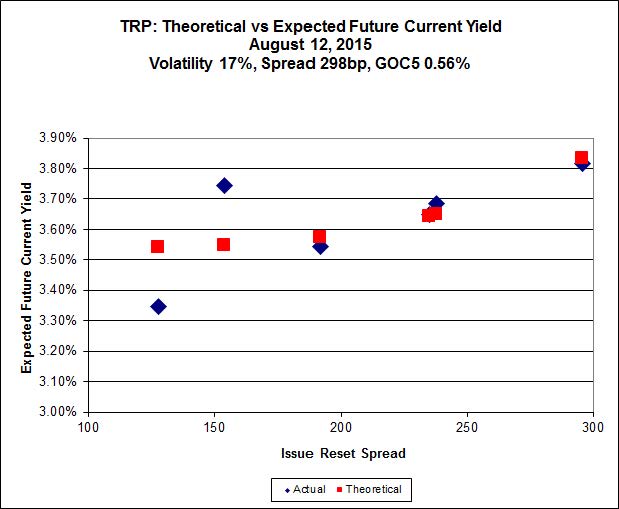

Here’s TRP:

Click for Big

TRP.PR.B, which resets 2020-6-30 at +128, is bid at 13.75 to be $0.76 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $0.79 cheap at its bid price of 14.02.

Click for Big

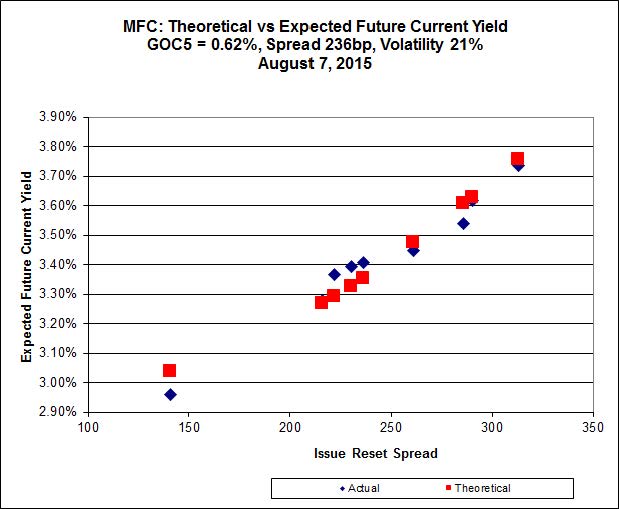

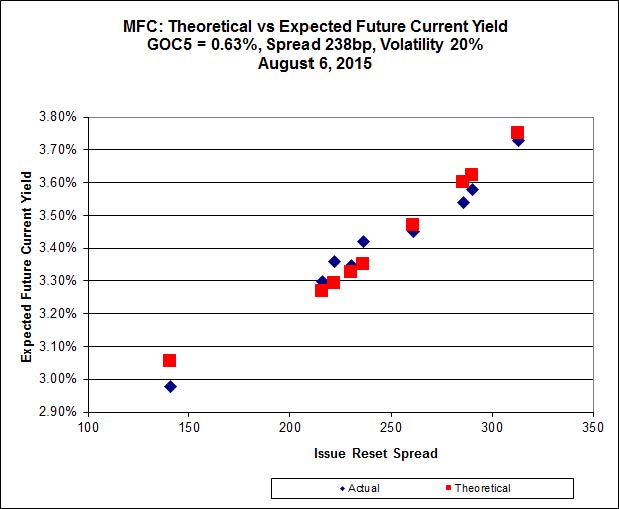

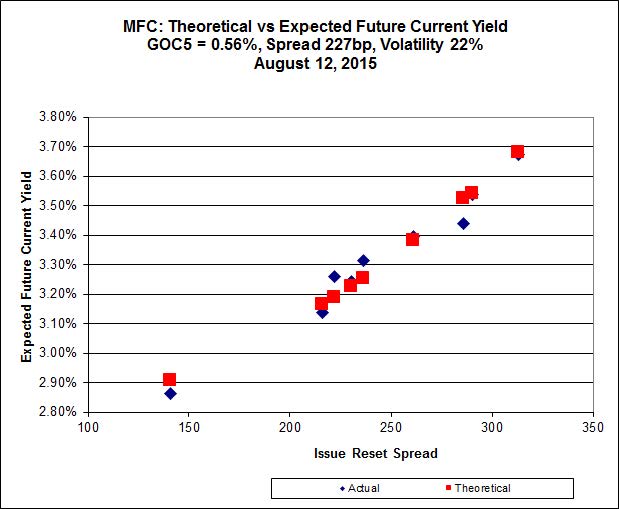

Another good fit today!

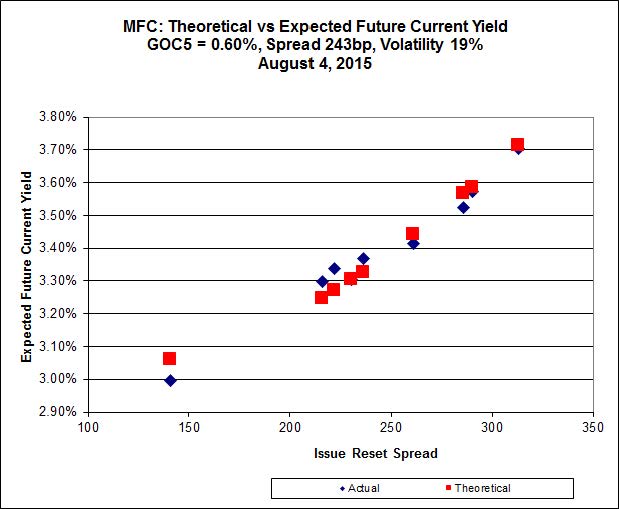

Most expensive is MFC.PR.I, resetting at +286bp on 2017-9-19, bid at 24.84 to be 0.59 rich, while MFC.PR.K, resetting at +222bp on 2018-9-19, is bid at 21.32 to be $0.48 cheap.

Click for Big

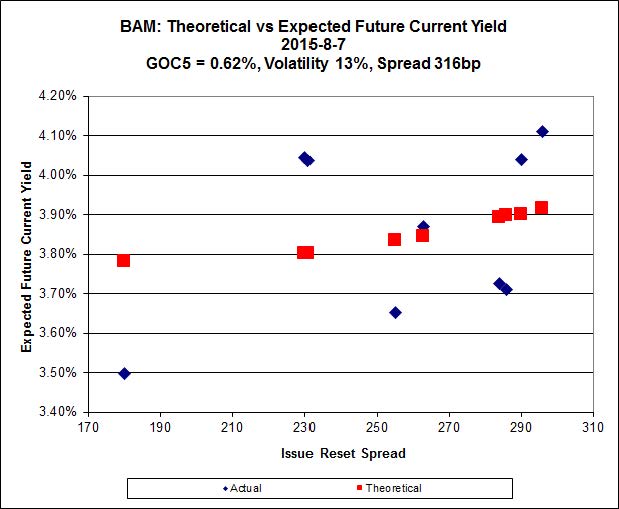

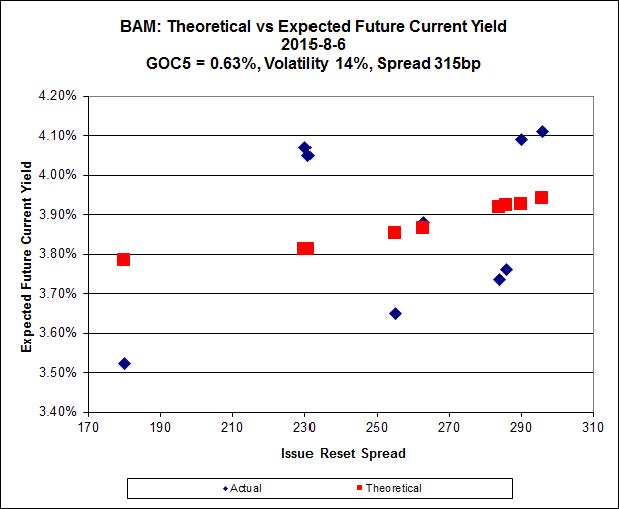

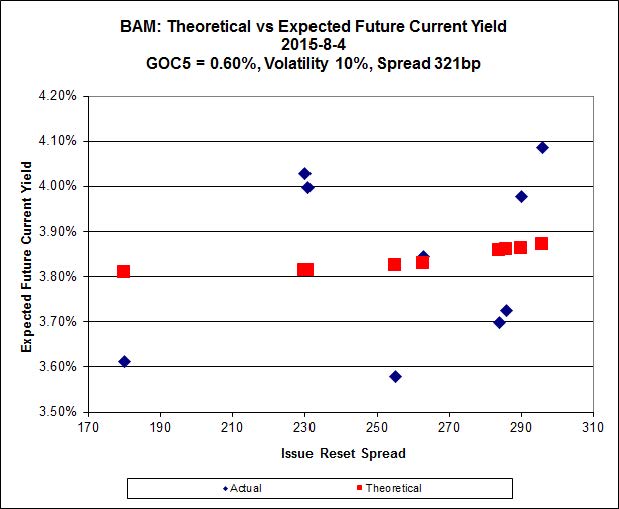

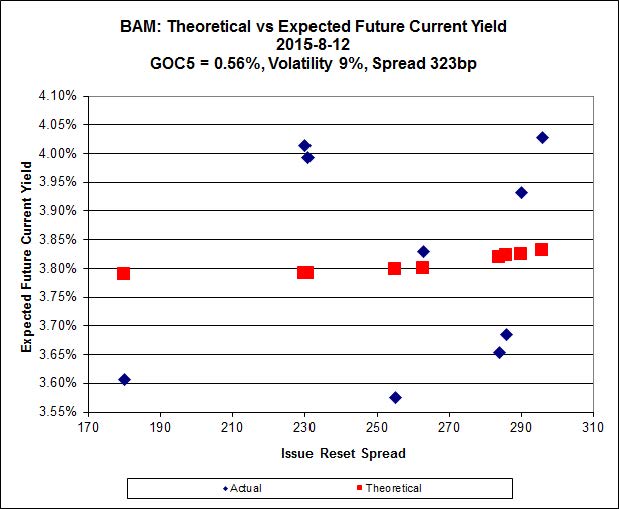

The fit on the BAM issues continues to be horrible.

The cheapest issue relative to its peers is BAM.PR.Z, resetting at +296bp on 2017-12-31, bid at 21.85 to be $1.12 cheap. BAM.PF.E, resetting at +255bp on 2020-3-31 is bid at 21.75 and appears to be $1.28 rich.

Click for Big

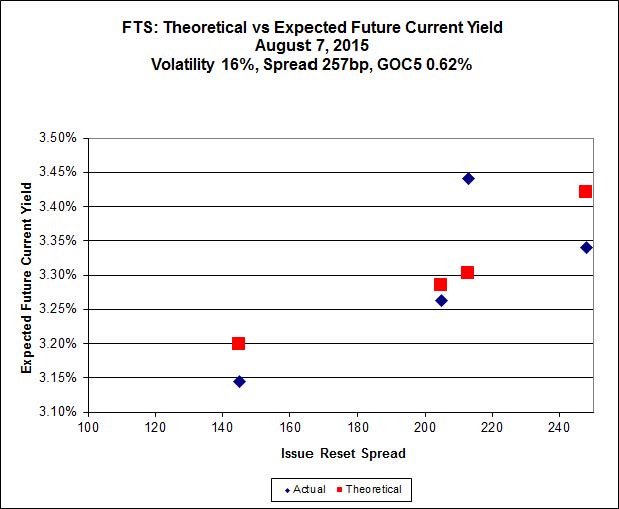

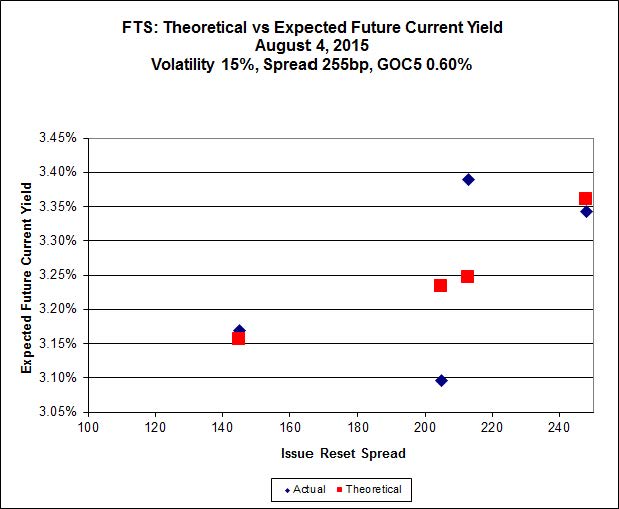

FTS.PR.M, with a spread of +248bp, and bid at 23.35, looks $0.38 expensive and resets 2019-12-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 20.09 and is $0.83 cheap.

Click for Big

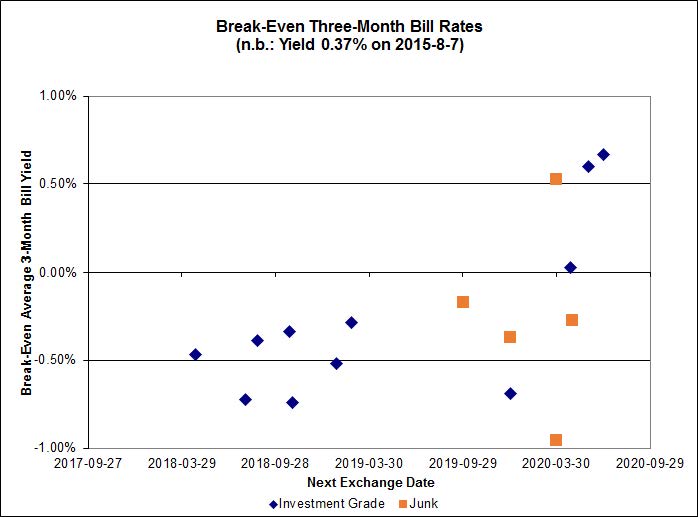

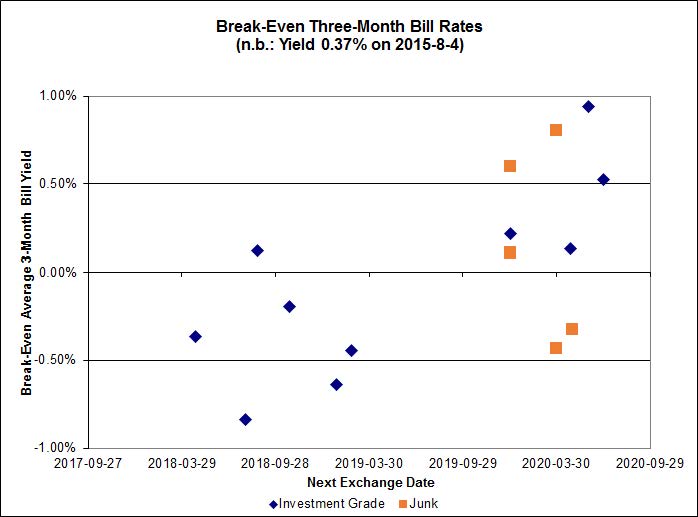

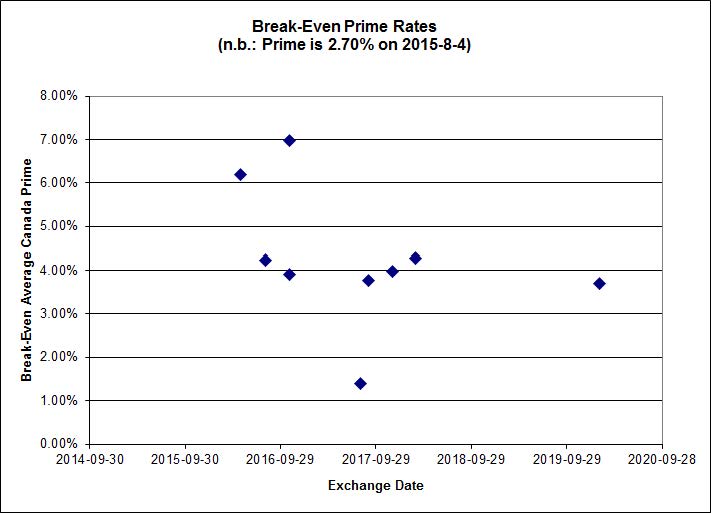

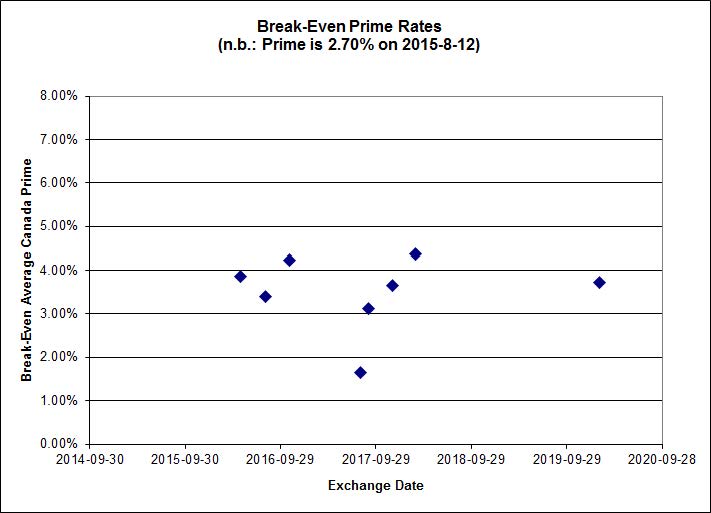

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.30%, with no outliers. There is one junk outlier below -1.00% and one above +1.00%.

Click for Big

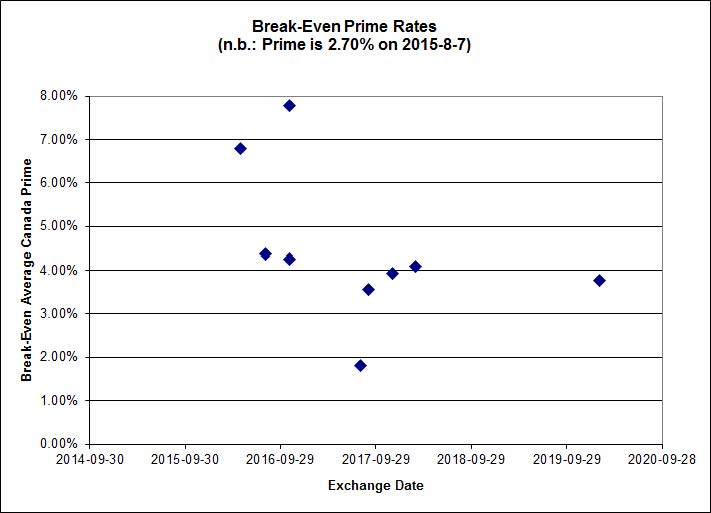

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -1.2727 % | 1,967.4 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -1.2727 % | 3,439.9 |

| Floater | 3.73 % | 3.75 % | 52,931 | 17.92 | 3 | -1.2727 % | 2,091.5 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0937 % | 2,778.9 |

| SplitShare | 4.58 % | 4.82 % | 57,419 | 3.13 | 3 | 0.0937 % | 3,256.7 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0937 % | 2,541.0 |

| Perpetual-Premium | 5.72 % | 5.38 % | 63,588 | 2.07 | 9 | -0.0265 % | 2,484.0 |

| Perpetual-Discount | 5.41 % | 5.44 % | 78,212 | 14.70 | 29 | -0.0455 % | 2,608.2 |

| FixedReset | 4.72 % | 3.98 % | 202,984 | 15.87 | 87 | 0.1739 % | 2,232.0 |

| Deemed-Retractible | 5.11 % | 5.24 % | 103,625 | 5.45 | 34 | 0.2550 % | 2,584.2 |

| FloatingReset | 2.32 % | 3.26 % | 47,736 | 6.01 | 9 | -0.0697 % | 2,246.0 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BAM.PR.K | Floater | -4.98 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-12 Maturity Price : 12.21 Evaluated at bid price : 12.21 Bid-YTW : 3.91 % |

| TRP.PR.F | FloatingReset | -1.80 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-12 Maturity Price : 15.81 Evaluated at bid price : 15.81 Bid-YTW : 3.64 % |

| CU.PR.C | FixedReset | -1.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-12 Maturity Price : 22.69 Evaluated at bid price : 23.05 Bid-YTW : 3.38 % |

| ELF.PR.F | Perpetual-Discount | -1.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-12 Maturity Price : 23.50 Evaluated at bid price : 23.77 Bid-YTW : 5.62 % |

| TRP.PR.E | FixedReset | -1.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-12 Maturity Price : 19.94 Evaluated at bid price : 19.94 Bid-YTW : 4.13 % |

| BAM.PF.F | FixedReset | -1.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-12 Maturity Price : 22.44 Evaluated at bid price : 23.20 Bid-YTW : 4.01 % |

| TRP.PR.D | FixedReset | -1.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-12 Maturity Price : 19.95 Evaluated at bid price : 19.95 Bid-YTW : 4.06 % |

| BIP.PR.A | FixedReset | -1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-12 Maturity Price : 21.52 Evaluated at bid price : 21.83 Bid-YTW : 4.97 % |

| TRP.PR.B | FixedReset | -1.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-12 Maturity Price : 13.75 Evaluated at bid price : 13.75 Bid-YTW : 3.66 % |

| ENB.PR.D | FixedReset | 1.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-12 Maturity Price : 15.62 Evaluated at bid price : 15.62 Bid-YTW : 5.08 % |

| BAM.PR.N | Perpetual-Discount | 1.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-12 Maturity Price : 21.41 Evaluated at bid price : 21.41 Bid-YTW : 5.63 % |

| SLF.PR.E | Deemed-Retractible | 1.12 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.66 Bid-YTW : 6.52 % |

| IAG.PR.A | Deemed-Retractible | 1.14 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.20 Bid-YTW : 6.30 % |

| SLF.PR.D | Deemed-Retractible | 1.18 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.45 Bid-YTW : 6.60 % |

| ENB.PF.C | FixedReset | 1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-12 Maturity Price : 17.87 Evaluated at bid price : 17.87 Bid-YTW : 5.01 % |

| RY.PR.O | Perpetual-Discount | 1.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-12 Maturity Price : 23.67 Evaluated at bid price : 24.00 Bid-YTW : 5.14 % |

| SLF.PR.A | Deemed-Retractible | 1.27 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.36 Bid-YTW : 6.37 % |

| FTS.PR.H | FixedReset | 1.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-12 Maturity Price : 16.26 Evaluated at bid price : 16.26 Bid-YTW : 3.44 % |

| ENB.PF.G | FixedReset | 1.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-12 Maturity Price : 18.07 Evaluated at bid price : 18.07 Bid-YTW : 5.04 % |

| ENB.PR.T | FixedReset | 1.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-12 Maturity Price : 16.59 Evaluated at bid price : 16.59 Bid-YTW : 5.04 % |

| MFC.PR.I | FixedReset | 1.43 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.85 Bid-YTW : 3.90 % |

| ENB.PF.A | FixedReset | 1.54 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-12 Maturity Price : 17.90 Evaluated at bid price : 17.90 Bid-YTW : 5.01 % |

| ENB.PR.F | FixedReset | 1.71 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-12 Maturity Price : 16.38 Evaluated at bid price : 16.38 Bid-YTW : 5.05 % |

| RY.PR.M | FixedReset | 1.90 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-12 Maturity Price : 22.57 Evaluated at bid price : 23.58 Bid-YTW : 3.49 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| TD.PF.D | FixedReset | 63,450 | TD sold 20,300 to Scotia at 24.37, then crossed 14,600 at the same price. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-12 Maturity Price : 22.93 Evaluated at bid price : 24.35 Bid-YTW : 3.49 % |

| IAG.PR.G | FixedReset | 59,613 | RBC crossed 48,600 at 24.45. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.43 Bid-YTW : 4.05 % |

| CU.PR.H | Perpetual-Discount | 56,629 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-12 Maturity Price : 23.48 Evaluated at bid price : 23.80 Bid-YTW : 5.54 % |

| TRP.PR.D | FixedReset | 34,292 | RBC bought 11,300 from National at 20.27. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-12 Maturity Price : 19.95 Evaluated at bid price : 19.95 Bid-YTW : 4.06 % |

| FTS.PR.H | FixedReset | 28,600 | RBC crossed 25,000 at 16.55. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-12 Maturity Price : 16.26 Evaluated at bid price : 16.26 Bid-YTW : 3.44 % |

| BMO.PR.Z | Perpetual-Discount | 22,900 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-12 Maturity Price : 23.95 Evaluated at bid price : 24.30 Bid-YTW : 5.17 % |

| There were 18 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| BAM.PR.K | Floater | Quote: 12.21 – 12.90 Spot Rate : 0.6900 Average : 0.4364 YTW SCENARIO |

| HSE.PR.G | FixedReset | Quote: 22.90 – 23.69 Spot Rate : 0.7900 Average : 0.5476 YTW SCENARIO |

| IAG.PR.A | Deemed-Retractible | Quote: 22.20 – 22.82 Spot Rate : 0.6200 Average : 0.4194 YTW SCENARIO |

| TRP.PR.E | FixedReset | Quote: 19.94 – 20.70 Spot Rate : 0.7600 Average : 0.5907 YTW SCENARIO |

| HSE.PR.C | FixedReset | Quote: 21.92 – 22.41 Spot Rate : 0.4900 Average : 0.3416 YTW SCENARIO |

| MFC.PR.N | FixedReset | Quote: 22.05 – 22.57 Spot Rate : 0.5200 Average : 0.3744 YTW SCENARIO |