The equity jocks are off their meds:

After plunging 1.5 percent on Oct. 7 and rallying almost 1.8 percent yesterday, the Standard & Poor’s 500 Index dropped 2.1 percent at 4 p.m. in New York today, the biggest turnaround in almost three years. As investors weigh the prospect of slower economic growth overseas against the benefit of U.S. interest rates staying near zero, a measure of 10-day volatility has risen to the highest level since April, data compiled by Bloomberg show.

The only phrase that generates more comments on this site than “real estate” is “trailer fees”. So it is with some glee that I report that the trailer fee wars are heating up:

“Trailer fees – the meteor is closer than you think” was the title of a recent note put out by Mr. Sedran and Mr. Holden [of CIBC]. The meteor in question is a ban on trailer fees.

“Regulators are studying the impact of these fees, with the results of those studies and a recommendation expected early 2015. A ban on trailer fees would follow a global trend and would address the regulators’ conflict of interest concerns. We think such a ban is coming, and sooner than many think.”

The story is marred by an inaccuracy:

The big knock against trailer fees is that despite the advisor having a fiduciary duty to put the client in the product that best serves their needs, there is a financial incentive for the advisor to sell the client the fund with the highest trailer fee – a glaring conflict of interest.

… but we may see a lot of “portfolio managers” without track records:

Mr. Sedran and Mr. Holden say the industry will likely transition to a model where advisors would be paid for managing a client’s entire portfolio, similar to how financial planners are paid today. Furthermore, under such a model, the advisor’s compensation would be tied to whether their client’s portfolio appreciates in value. The implication is that it will also be in the advisor’s interest to put clients into the funds they believe will perform the best over time.

The so-called implication is laughable – it will continue to be a lot easier for salesmen to get a fresh $1,000 into the account from the client than it is to outperform by 1% on a $100,000 portfolio. But people like to dream.

There’s a laugh line:

The bigger players, such as the Canadian banks who already have vast mutual fund sales forces in branches, should be able to manage the transition just fine, according to Mr. Sedran and Mr. Holden.

Well, of course. If it hurt the banks, their future employees at the regulatory agencies wouldn’t dream of the idea. I remain interested in the regulatory agencies views on new issue commissions and proxy solicitation fees – which are functionally equivalent to trailer fees – but the silence continues.

I have often remarked at the superiority of US institutions over their Canadian counterparts with respect to transparency. It is very useful to gain insight into the policy-setting process by reviewing the countervailing arguments within the various committees – but, of course, there are always some who would prefer a two-line press release:

Joseph LaVorgna, chief U.S. economist at Deutsche Bank AG in New York, said officials risk sowing confusion.

“It’s hard to have a unifying message when you have this many people who feel it’s incumbent on them to tell you what the Fed is thinking,” he said.

“I wish the Fed would answer generalities with generalities,” he said. “When they try to quantify, that’s when the problems come up.”

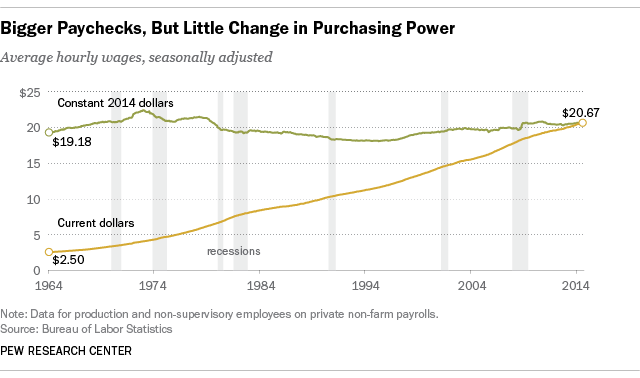

There’s some more information from Pew Research regarding stagnant wages:

Following the better-than-expected September jobs report, several economic analyses have pointed out the continuing lack of meaningful wage growth, even as tens of thousands of people head back to work. Economic theory, after all, predicts that as labor markets tighten, employers will offer higher wages to entice workers their way.

But a look at five decades’ worth of government wage data suggests that the better question might be, why should now be any different? For most U.S. workers, real wages — that is, after inflation is taken into account — have been flat or even falling for decades, regardless of whether the economy has been adding or subtracting jobs.

Cash money isn’t the only way workers are compensated, of course — health insurance, retirement-account contributions, education and transit subsidies and other benefits all can be part of the package. But wages and salaries are the biggest (about 70%, according to the Bureau of Labor Statistics) and most visible component of employee compensation.

…

But after adjusting for inflation, today’s average hourly wage has just about the same purchasing power as it did in 1979, following a long slide in the 1980s and early 1990s and bumpy, inconsistent growth since then. In fact, in real terms the average wage peaked more than 40 years ago: The $4.03-an-hour rate recorded in January 1973 has the same purchasing power as $22.41 would today.

A similar measure, “usual weekly earnings” of employed, full-time, wage and salary workers, tells much the same story, albeit over a shorter time period. In seasonally adjusted current dollars, median usual weekly earnings rose from $232 in the first quarter 0f 1979 (when the series began) to $782 in the second quarter of this year (the most recent data available). But in real terms, the median has barely budged over that period.

Click for Big

Click for BigBut amidst all the gloom and doom, there’s some good news:

Prince Edward Island has joined Ottawa’s move to create a national securities regulator, bringing the total to five provinces who have signed onto the plan.

The federal Finance Department said Thursday the province has signed a memorandum of agreement to join the Co-operative Capital Markets Regulatory System.

The addition of P.E.I. follows a decision in July by Saskatchewan and New Brunswick to join B.C., Ontario and the federal government in establishing a national regulator.

I have said for a long, long time that piecemeal cooperation is better than none and much more attainable than the single-regulator pipedream. Mind you, I think the commentary we occasionally see regarding the wonderfulness of a national-mostly regulator is highly overwrought. All that will happen is that some unnecessarily duplicated paperwork will be eliminated. But that’s good reason enough.

It was a poor day for the Canadian preferred share market, with PerpetualDiscounts down 12bp, FixedResets losing 13bp and DeemedRetractibles off 8bp. Volatility was average and balanced, but comprised entirely of FixedResets. Volume was on the low side of average.

HIMIPref™ Preferred Indices

These values reflect the December 2008 revision of the HIMIPref™ Indices

Values are provisional and are finalized monthly |

| Index |

Mean

Current

Yield

(at bid) |

Median

YTW |

Median

Average

Trading

Value |

Median

Mod Dur

(YTW) |

Issues |

Day’s Perf. |

Index Value |

| Ratchet |

3.14 % |

3.13 % |

23,337 |

19.41 |

1 |

-0.4167 % |

2,660.4 |

| FixedFloater |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

-0.5950 % |

4,074.6 |

| Floater |

2.92 % |

3.09 % |

62,765 |

19.52 |

4 |

-0.5950 % |

2,735.9 |

| OpRet |

4.04 % |

0.98 % |

110,907 |

0.08 |

1 |

0.0789 % |

2,734.6 |

| SplitShare |

4.29 % |

4.00 % |

89,024 |

3.85 |

5 |

-0.1361 % |

3,151.9 |

| Interest-Bearing |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.0789 % |

2,500.5 |

| Perpetual-Premium |

5.50 % |

1.69 % |

77,694 |

0.08 |

18 |

-0.1687 % |

2,449.8 |

| Perpetual-Discount |

5.33 % |

5.14 % |

96,578 |

15.08 |

18 |

-0.1218 % |

2,589.3 |

| FixedReset |

4.22 % |

3.74 % |

169,967 |

16.37 |

75 |

-0.1278 % |

2,549.6 |

| Deemed-Retractible |

5.03 % |

2.13 % |

104,351 |

0.37 |

42 |

-0.0764 % |

2,559.5 |

| FloatingReset |

2.57 % |

-2.37 % |

79,699 |

0.08 |

6 |

0.1436 % |

2,552.5 |

| Performance Highlights |

| Issue |

Index |

Change |

Notes |

| FTS.PR.H |

FixedReset |

-1.34 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2044-10-09

Maturity Price : 20.60

Evaluated at bid price : 20.60

Bid-YTW : 3.76 % |

| FTS.PR.K |

FixedReset |

-1.25 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2044-10-09

Maturity Price : 23.01

Evaluated at bid price : 24.45

Bid-YTW : 3.73 % |

| TRP.PR.B |

FixedReset |

1.26 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2044-10-09

Maturity Price : 19.29

Evaluated at bid price : 19.29

Bid-YTW : 3.77 % |

| PWF.PR.P |

FixedReset |

1.57 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2044-10-09

Maturity Price : 22.02

Evaluated at bid price : 22.64

Bid-YTW : 3.54 % |

| Volume Highlights |

| Issue |

Index |

Shares

Traded |

Notes |

| NA.PR.W |

FixedReset |

314,800 |

Recent new issue.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2044-10-09

Maturity Price : 23.06

Evaluated at bid price : 24.78

Bid-YTW : 3.77 % |

| NA.PR.M |

Deemed-Retractible |

107,456 |

Nesbitt crossed 103,900 at 26.30.

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2014-11-08

Maturity Price : 25.75

Evaluated at bid price : 26.30

Bid-YTW : -25.34 % |

| BAM.PF.G |

FixedReset |

88,955 |

Recent new issue.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2044-10-09

Maturity Price : 23.12

Evaluated at bid price : 25.01

Bid-YTW : 4.34 % |

| BMO.PR.M |

FixedReset |

82,561 |

Nesbitt crossed blocks of 51,000 and 31,000, both at 25.44.

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2018-08-25

Maturity Price : 25.00

Evaluated at bid price : 25.37

Bid-YTW : 3.11 % |

| HSE.PR.A |

FixedReset |

74,704 |

Nesbitt crossed 65,000 at 22.92.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2044-10-09

Maturity Price : 22.47

Evaluated at bid price : 22.87

Bid-YTW : 3.71 % |

| BMO.PR.T |

FixedReset |

67,725 |

Nesbitt crossed 51,000 at 25.34.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2044-10-09

Maturity Price : 23.27

Evaluated at bid price : 25.31

Bid-YTW : 3.73 % |

| There were 29 other index-included issues trading in excess of 10,000 shares. |

| Wide Spread Highlights |

| Issue |

Index |

Quote Data and Yield Notes |

| ENB.PR.B |

FixedReset |

Quote: 24.32 – 24.75

Spot Rate : 0.4300

Average : 0.2646

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2044-10-09

Maturity Price : 23.18

Evaluated at bid price : 24.32

Bid-YTW : 4.06 % |

| IGM.PR.B |

Perpetual-Premium |

Quote: 25.90 – 26.21

Spot Rate : 0.3100

Average : 0.2124

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2018-12-31

Maturity Price : 25.00

Evaluated at bid price : 25.90

Bid-YTW : 4.89 % |

| FTS.PR.K |

FixedReset |

Quote: 24.45 – 24.79

Spot Rate : 0.3400

Average : 0.2440

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2044-10-09

Maturity Price : 23.01

Evaluated at bid price : 24.45

Bid-YTW : 3.73 % |

| FTS.PR.F |

Perpetual-Discount |

Quote: 23.75 – 23.99

Spot Rate : 0.2400

Average : 0.1613

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2044-10-09

Maturity Price : 23.50

Evaluated at bid price : 23.75

Bid-YTW : 5.21 % |

| CU.PR.D |

Perpetual-Discount |

Quote: 24.02 – 24.19

Spot Rate : 0.1700

Average : 0.1100

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2044-10-09

Maturity Price : 23.64

Evaluated at bid price : 24.02

Bid-YTW : 5.14 % |

| BAM.PR.B |

Floater |

Quote: 17.04 – 17.20

Spot Rate : 0.1600

Average : 0.1035

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2044-10-09

Maturity Price : 17.04

Evaluated at bid price : 17.04

Bid-YTW : 3.10 % |